💥The Suspense is Killing Us💥

💥The Suspense is Killing Us💥

An Enviva Update, Farewell WeWork + DermTech Inc. files for bankruptcy.

⚡️Update: Enviva Inc⚡️

More Enviva Inc!

Just in case you’ve been living under a rock, you can refer to our previous coverage:

You’ll recall that the debtors originally filed these chapter 11 cases on March 12, 2024 in the Eastern District of Virginia (“EDVA”) with a restructuring support agreement (the “RSA”). These cases were supposed to be a simple and straightforward equitization process into an exit facility but sh*t hit the fan when the United States Trustee (“UST”) got up to the plate.

The UST objected to Vinson & Elkins LLP’s employment application as debtors’ counsel because one of Enviva’s major equity holders, Riverstone Holdings LLC (“Riverstone”, 43% ownership in Enviva), just so happens to also be a V&E client. This resulted in Judge Kenney issuing a memorandum of opinion that denied V&E’s retention and knocked the law firm face first into the ground. But just when you thought V&E was down for the count… BAM! V&E filed a reconsideration motion.

A June 14, 2024 hearing to consider the motion to reconsider sure did not disappoint.

V&E came into the hearing with its chest pumped out and head held high. After all, literally everyone on the planet — well, everyone other than the UST — seemed to have V&E’s back. We’re talking the Ad Hoc Group. The ‘26 notes trustee (Wilmington Savings Fund Society FSB), and even a newly organized ad hoc committee that purchased some RWE Supply & Trading GmbH (“RWE”) claims.*

So the UST be like…

But wait! What about the official committee of unsecured creditors (the “UCC”)? You know, the same guys who previously took a very adversarial posture against V&E with respect to the debtors’ DIP motion?

Here was UCC counsel Akin Gump Strauss Hauer & Feld LLP’s Scott Alberino at the June 14th hearing:

“Your Honor, last time I was in this courtroom, I was on the losing end of a DIP objection. You’re probably wondering why I'm here today saying nice things about Vinson & Elkins.”

Yes, what exactly was in the silver plate that the debtors offered up to the UCC for their support?

Apparently, a board delegated independent plan evaluation committee (the “PEC”)!** The PEC will have the powers to analyze, review, and approve any contemplated plan, which, from the perspective of the UCC, provides a useful safeguard.

The UST (who literally sat beside UCC counsel at the hearing) be like:

In addition to the PEC, V&E’s proposal would also commit the law firm to an ethical wall.*** We covered the details of that wall here:

Basically V&E proposed that its lawyers will be separated between any Riverstone representation and Enviva representation thus mitigating any potential conflicts of interest. And while these proposed mechanics satisfied all the economic stakeholders, the hearing was still anything but smooth for V&E. Was this surprising? Well, the writing was on the wall.

In his memorandum of opinion, Judge Kenney had this to say regarding conflicts counsel:

“[T]he Court cannot see how V&E could possibly negotiate a plan adversely to Riverstone’s position. The employment of conflicts counsel can be useful for a discrete portion of a case, such as the prosecution of preference or fraudulent transfer claims, but it cannot be used as a substitute for general bankruptcy counsel’s duties to negotiate a plan of reorganization.” (emphasis added)

So how does the appointment of the PEC differ from conflicts counsel here? Are the debtors not substituting the duties of V&E with the PEC and its respective independent counsel?

Here’s Judge Kenney:

“What I said in my opinion was that this is the core function of counsel in the chapter 11 cases to formulate a plan of reorganization and I didn't think it was okay to say well just delegate that to Kutak Rock. So what's the difference in saying now we're going to have a whole new committee and they'll have their own council and financial advisors. Isn't that the same thing functionally?”

Judge Kenney posed that same question to almost every attorney who stood up in support of V&E. Nobody seemed to give a fully satisfactory answer.

And what of the ethical wall?

Just a few minutes into Kutak Rock LLP’s Jeremy Williams’ opening statement, Judge Kenney made his thoughts known on the ethical wall:

“Mr. Williams, if you have reviewed the transcript of the May 9th hearing, it wasn't just that the Court was left with the impression that it was impossible because V&E lawyers were working both for Riverstone and Enviva at the same time. It was that V&E's counsel, Mr. Meyer, said on page 13, and I'm quoting here, ‘but a wall of separation where none is required would be incredibly harmful to Enviva at this critical phase of its restructuring efforts.’”

“So now you're proposing an ethical wall, which your co-counsel described previously as being incredibly harmful to the debtors.”

Is an ethical wall harmful to the debtors? Perhaps. But it seems the economic stakeholders all agree that losing V&E is a lot more costly than an ethical wall.

Mr. Alberino, on behalf of the UCC, put it rather succinctly:

“But to quote Voltaire, we didn't want to let the perfect be the enemy of the good here. And as you said, you know, you called it, you're asking me to choose between a bad situation and a worse situation. We're trying to get to a better situation.”

Of course, it isn’t just the intangible loss attributable to the wall, there’s also the very real cost of the independent PEC. After all, the PEC needs an independent legal counsel and probably a financial advisor/investment banker as well. So really how much worse is it to lose V&E versus the currently proposed solution?

Again, Judge Kenney:

“It's a little hard for the court to compare the cost for example of denying V&E's employment application and bringing in new 327(a) council with perhaps V&E coming on board for discrete matters under 327(e) versus this [] plan evaluation committee with its own set of counsel and its own financial advisors and so forth.”

The delta here is “unquantifiable.” Not “unquantifiable” in the sense that it’s so large and vast, “unquantifiable” as in nobody can give the court an actual number (because nobody knows)!

According to Judge Kenney:

“[H]ow do we compare [the cost of losing V&E] to the cost of new counsel and financial advisors for the plan evaluation committee? I mean, it's really not quantifiable, I mean, it's anybody's guess. You might say, well, it's just obvious that not granting your motion and the application to employ V&E would create more disruption in cost than the PEC.”

And while the UST harped on the procedural pitfalls regarding V&E’s use of 9023 and 9024 under the bankruptcy code, Judge Kenney made it clear:

“You know, for the most part, I'll just tell you, I'm not that concerned with the procedural niceties here and whether it's a rule 9023 or 24 motion it seems to me that, you know, we ought to get to the heart of the matter.”

And for Judge Kenney, the heart of the matter being?

“So the heart of the matter is: how is hiring, establishing the PEC, planned evaluation committee, and having its own counsel and presumably financial advisors different from the initial position, which is, we'll just farm this out to Kutak Rock and they'll handle it as conflicts counsel? Which I said was an impermissible delegation of the core function of 327(a) counsel. How is this different?”

🤷♀️

And so the parties are left in limbo awaiting Judge Kenney’s dramatic decision. While that decision is currently unknown, rest assured that the industry as a whole has come to one with respect to the EDVA.

*RWE is one of the debtors largest customers/counterparties. A new group has acquired from RWE ~$310mm in claims and made themselves heard for the first time during the June 14 hearing. This new RWE claimants group is represented by Milbank LLP (Dennis Dunne, Evan Fleck, Andrew Harmeyer, Andrew Leblanc, Erin Dexter, Robert Marsters) and Williams Mullen (Michael Mueller, Jennifer McLemore, Gabrielle Brill)

**See exhibit B here for the board resolution appointing the plan evaluation committee.

***Apparently by the time of the hearing, V&E had already erected the ethical wall.

⚡️Final Update: WeWork Inc.⚡️

We thought it’d be fitting for us to write up one last piece dedicated to a company from the bygone era of pre-pandemic optimism, ZIRP, and watchable Marvel movies.

And so to our favorite debtors of ‘23/’24, we say adieu to WeWork Inc.

The WeWork debtors filed their chapter 11 cases in the District of New Jersey (Judge Sherwood) back on November 6, 2023; they took almost seven months to get to a confirmation hearing. You can refer to all of our previous coverage here:

Yes, WeWork, you were an ocean’s worth of content and will be sorely missed.

The WeWork debtors originally filed with an restructuring support agreement that contemplated equitization of what included much of Softbank’s secured debt but, this being WeWork of course, the case wasn’t nearly that straightforward. To the contrary, the process took us through a rollercoaster that included aggressive lease negotiations against landlords (which included nonpayment of postpetition amounts due and owing), an (un)surprising appearance from Adam Neumann, mouth watering professional fees, and a last minute DIP facility. Ah, WeWork, we’re gonna miss you.

The new CEO is now John Santora — a man who has spent more than 40 years at Cushman & Wakefield Inc ($CWK) and holds an MBA from Wharton. Talk about hip! What an absolutely perfect ending for the once high flying “start up” that boasted about free flowing beer, La Colombe coffee, “community,” and the benefits of being a, LOL, “real estate tech company.”

You know it’s over when we go from this:

To this:

Reorganized WeWork is emerging with around 337 locations that, in total, are expected to generate $2.2b of total revenue and $184mm of adjusted EBITDA by ’25. Annual rent payments have been absolutely slashed by $800mm to $1.25b and the balance sheet is bolstered by the $400mm “DIP New Money Exit Facility” from Cupar Grimmond LLC (“Cupar”) (a/k/a Yardi).

Everyone who was involved is celebrating… with one notable exception. Here’s what seems to be Adam Neumann’s last statement on the subject of WeWork:

“For several months, we tried to work constructively with WeWork to create a strategy that would allow it to thrive. Instead, the company looks to be emerging from bankruptcy with a plan that appears unrealistic and unlikely to succeed.”

Talk about a salty ex.

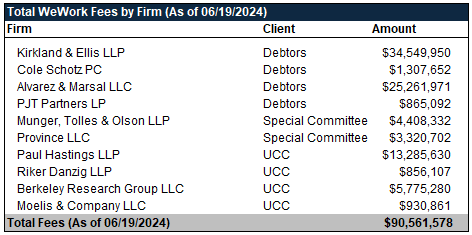

Not salty? RX professionals:

It’s official, we’re past the $90mm mark through April. In other words, on an annualized basis, professional fees for the WeWork cases are ~$180mm, a number befitting of Masa Son’s infamous goading of Mr. Neumann to think bigger.

| Video ...")

See ya WeWork and good luck on the other side.

💥New Chapter 11 Bankruptcy - DermTech Inc. ($DMTK)💥

On June 18, 2024, CA-based DermTech, Inc. ($DMTK) and one affiliate (collectively, the “debtors” or “the company”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Dorsey).

Founded in ‘95, DMTK is a molecular diagnostic company that creates small adhesive patches that people can put on their bodies to test for melanoma.

The company’s flagship product is the DermTech Melanoma Test (“the DMT”). Combined with the DermTech Smart Sticker (shown above), patients can perform a non-invasive test for melanoma with a negative predictive value* of 99%.

A quote from former CEO John Dobak in a Forbes piece sums the vision up nicely:

“Where it would cost $1,200 to $1,400 for each test to go through the conventional route, DermTech’s sticker costs most patients on average $75 or less out of pocket after their insurance is billed. We could essentially eliminate all those biopsies.”

The company operates a 13,000-square-foot lab in San Diego, CA, with 60 employees. All stickers come into this facility, where scientists test and return them to the physicians/patients with the results. The whole process takes about five days.

The company went public in ‘19 on the NASDAQ under the ticker “DMTK” via a de-SPAC with Constellation Alpha Capital Corp. The business combination gave the company access to $29mm in gross capital at a pro forma equity value of $81.6mm.

While the product might’ve worked, it definitely was not ready to enter the market at the scale the company anticipated. Scaling labs and increasing SG&A expenses quickly ate up all — and more of — the revenues the company generated. The company promptly realized it’d need more cash to fund operations. In November ‘20, the company launched an at-the-market offering with Cowen and Company LLC (“Cowen”) that allowed it to sell stock at its choosing at an aggregate price of up to $50mm. The company entered a similar agreement again in ‘22, allowing for the aggregate offering of up to $75mm. Both of these provided temporary lifelines; neither produced sustainable capital to figure out how to get costs under control.

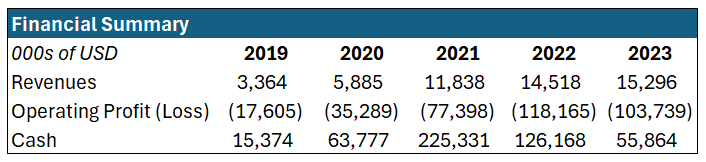

Just how bad were the costs? In ‘23, the company reported $15.3mm in revenues and a net operating loss of $104mm(!).

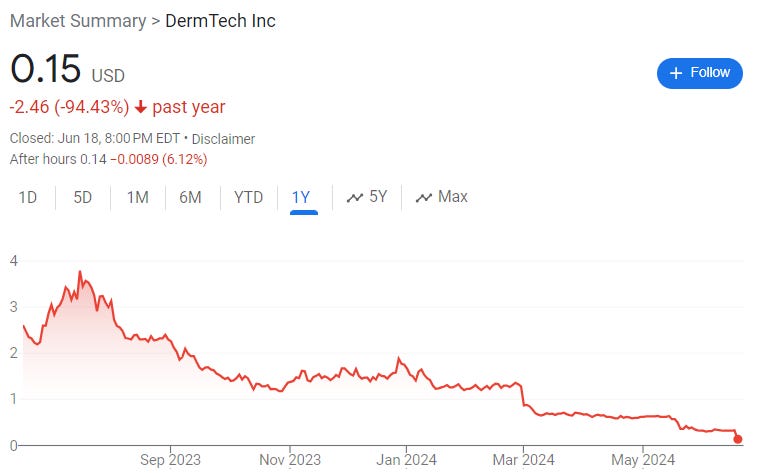

Outside of the operating expenses, the company also incurred significant expenses related to public listing requirements, lease obligations (more on this below), payor reimbursements, and securities litigations. All of this culminated in the stock price plummeting throughout ‘23 and into ‘24.

Good luck doing another ATM with performance like that ⬆️. This ain’t no meme stock.

And clearly no lender wanted anything to do with this cancerous performance. (Sorry, 🙄)

Multiple times throughout ‘23 and ‘24, the company reduced its workforce and implemented cost-savings plans. None of it accomplished much. In Jan. ‘24, the company initiated a sale process with Cowen (now “TD Cowen”), and in Mar. ‘24, it engaged AlixPartners LLP as a restructuring advisor. Ultimately, the sale process and advisor fees became too costly, forcing the company to file for bankruptcy protection. The debtors file with the hopes of securing a bidder in the near future. For those keeping score, YES!, this is yet another chapter 11 bankruptcy filing seeking a sale sans stalking horse purchaser.

The debtors come into the filing with no funded debt obligations. As of June 17, 2024, roughly 35mm shares were outstanding, along with 2.8mm outstanding SPAC warrants at an exercise price of $23/sh, and 570 placement agent warrants at an exercise price of $9.54/sh. Additionally, the debtors have an office lease with Kilroy Realty Corp. ($KRC) that is currently in default due to the failure to pay $662k in past rent — making KRC the debtors’ largest unsecured creditor.

The debtors are represented by Wilson Sonsini Goodrich & Rosati P.C. (Catherine Lyons, Marsha Sukach, Shane Reil, Benjamin Hoch, Erin Fay) as legal counsel, AlixPartners LLP (Stephen Hartman) as financial advisor, and TD Cowen as investment banker.

A first day hearing is scheduled for later today, June 20, 2024, at 1pm ET.

*True Negatives / (True Negatives + False Negatives).

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.