💥The "Golden Age." Part III.💥

Private Credit Takes a Bath in rue21; Adam Neumann Gets Doused with Rejection

We’re sure you’ve heard by now: on May 2, 2024, PA-based New rue21 Holdco, Inc. (“rue21”) and five affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Shannon) — the latest in a recent wave of retail cases to whirl around the bankruptcy bin and the first repeat offender in quite some time (chapter 33?!).*

But don’t be fooled.

While this may look like your run-of-the-mill retail bankruptcy story, it isn’t. Nope, it’s a story about the “golden age of private credit.” Let’s dig in.

rue21 is a specialty fashion retailer geared primarily towards adolescent and young adults; it designs, sources, markets and sells its own merchandise; it leases 540 brick-and-mortar locations and has an e-commerce website, rue21.com;** it leases its corporate headquarters in PA and its distribution center in WV. In other words, other than its merchandise and FF&E, it doesn’t really own anything other than some digital real estate and, lol, some intellectual property (🖕).

Now mind you, all of the foregoing is the result of years of work trying to fix this company. Indeed, you may remember the name from way back in ‘17 when we covered rue21’s first filing.*** The basis behind the ‘17 filing was to “(i) further revamp its e-commerce strategy, (ii) improve the in-store experience, (iii) right-size the store footprint and lease portfolio, (iv) de-lever its capital structure, and (v) effectuate a long-term business plan under its relatively new management.” The capital structure was relatively straight forward and the plan of reorganization confirmed at the time converted the “fulcrum security” — the then term loan — into the majority of ownership**** — with ~4% going to the then-existing unsecured creditors. The post-emergence capital structure comprised of a $125mm ABL and a $50mm term loan. In total, the restructuring wiped out $700mm in debt, killed ~400 stores, and amounted to a private equity retail wipeout for Apax Partners.

A few months later, the debtors popped back up on our radar after The Wall Street Journal published a piece stating that the debtors were in trouble again. That piece was followed by Reuters reporting that the company sought more financing after an underwhelming holiday season. In May ‘18, the debtors announced that they had received a $20mm line of credit from Bank of America Merrill Lynch, increasing the line of credit to $145mm. The next couple of years or so were relatively quiet heading into the pandemic. But then the pandemic hit and the company struggled to survive. Adjusted EBITDA for ‘20 and ‘21 came in at $62.5mm and $122.5mm, respectively, as the company “…renewed [its] focus on operational initiatives and margin improvement.” Compare this against the company’s financial projections from the ‘17 filing and, well, given the pandemic, performance wasn’t terribly far off!

But it was still bad. The company had to refinance its capital structure in mid-’21, which is when it entered into its current ABL facility with Bank of America NA ($BAC). That facility availed the company of $90mm (subject to borrowing base availability), including a $25mm letter of credit sublimit. This facility gave the ABL lenders a first priority interest and lien on “…substantially all personal property of the Debtors, including, but not limited to, accounts receivable, credit card receivables, other payment rights, inventory, cash, deposit accounts, securities and commodity accounts, documents and supporting obligations,” but, critically, excluded equity interests and intellectual property.

But the pandemic had lasting effects and by mid-’22, the company desperately needed additional financing to survive.

Enter Blue Torch Capital LLC (“Blue Torch”), LOLOLOLOLOLOLOLOLOLOLOLOLOLOL.

PETITION readers ought to be very familiar with Blue Torch by now.

It has been involved in a number of hairy dogsh*t restructuring names over the last year or so including, among others, Near Intelligence Inc. ($NIR) and Troika Media Group Inc ($TRKA). Like, these guys really ought to consider dropping “Torch” from their name lest they continue to remind investors prima facie how skillfully they incinerate cash. This situation? Well, it’s bad. Like, really f*cking bad. An all-timer, even.

In January ‘22, the company entered into an $85mm term loan credit agreement with Blue Torch secured by a first priority security interest and lien on the equity interests of rue21 and certain real and personal property (read: the FF&E and IP … remember, this company doesn’t own any real property). Blue Torch otherwise got a second priority lien on the ABL collateral (lol).

Of course, the company still struggled. And so in August ‘22, the company retained an investment banker to perform a capital raise to bolster liquidity. Where did the capital come from? Blue Torch!!

Unfamiliar with the old saying “good money after bad,” Blue Torch agreed to torch “invest” an additional $25mm in the company in exchange for warrants that were subsequently exercised, giving Blue Torch ~80% ownership of rue21.

Did that do the trick? LOL, OF COURSE NOT. Let’s get after it:

Per the debtors:

Notwithstanding the additional capital infusion from Blue Torch, in October 2022, the Debtors defaulted under the ABL Credit Agreement and Term Loan Agreement. Between October 2022 and December 2023, the Debtors entered into several amendments to both the ABL Credit Agreement and Term Loan Agreement, whereby the ABL Lender and Term Loan Lender agreed to waive certain events of default. In addition, as part of this process, the Term Loan Facility, originally issued in the principal amount of $85 million, was upsized to approximately $165 million in total commitments. (emphasis added)

THE $25mm LASTED ALL OF TWO MONTHS, LOLOLOLOLOLOL…

…AND THESE GUYS WERE LIKE, “HEY, LET’S DOUBLE DOWN AND 2X OUR EXPOSURE!” LOLOLOLOLOLOLOLOL (🖕).

THE. MOTHERF*CKING. GOLDEN. AGE. OF. PRIVATE. CREDIT. Y’ALL.

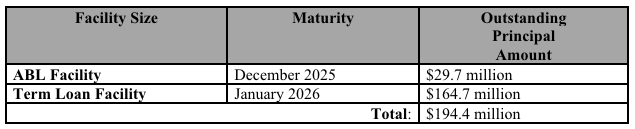

So this ⬇️ is what the capital structure currently looks like — a reflection of BofA ratcheting down its exposure as Blue Torch upped its own.

Behind the funded debt, there’s $65mm in unsecured claims. 😬

All of which leaves us where, exactly?

Well, this sh*t show is liquidating.*****

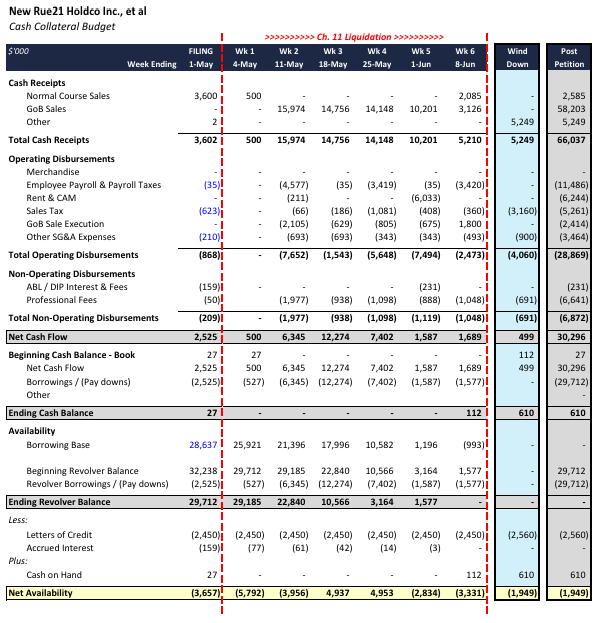

The stated purpose of this bankruptcy is to liquidate the debtors, using the proceeds of going out of business sales — read: BofA’s cash collateral****** — to fund the wind down and pay down the ABL. The debtors have hired Gordon Brothers Retail Partners LLC to effectuate some “GOB” sales over the next 4-6 weeks.******* You can see how this plays out in the debtors’ filed cash collateral budget:

Based on this, it looks like BofA’s security interest in and lien on receivables will be just enough to cover the outstanding pre-petition ABL nut. Good for them!

How will Blue Torch fare? How much will it recover on its tens of millions of dollars infused into this situation?

Well, they have that security interest in the equity (LOL … 🍩) and the FF&E and intellectual property. Contemporaneous with the GOB sales, the debtors will attempt to sell those assets to maximize value for creditors. LOLOLOLOL.

There was some mention at the debtors’ first day hearing that there might be a bid for the IP out there but, if not, we’ll get the bidding started at 99 cents only.

The debtors are represented by Willkie Farr & Gallagher LLP (Rachel Strickland, Andrew Mordkoff, Joseph Brandt, Jessica Graber, Benjamin McCallen) and, inexplicably, Young Conaway Stargatt & Taylor LLP (Edmon L. Morton, Matthew B. Lunn, Shane M. Riel, and Carol E. Cox)******* as legal counsel. Riveron RTS LLC (Colin Adams) is the financial advisor. BofA is represented by Morgan Lewis & Bockius LLP (Christopher Carter, Rachael Gonzalez) and Reed Smith LLP (Kurt Gwynne, Jason Angelo) while Blue Torch is represented by Schulte Roth & Zabel LLP (Adam Harris, Abbey Walsh) and Landis Rath & Cobb LLP (Adam Landis, Matthew McGuire).

*At the first day hearing, debtors’ counsel said “…if you’re keeping score at home, today marks the company’s chapter 33. But as they say, third time’s the charm…” to which 5000 people who are about to be out of jobs be like:

**This is what that site looks like as we write this (lol):

***The second if you count the ‘02 filing under the name Pennsylvania Fashions.

****The term lenders included Bayside Capital LLC, Benefit Street Partners LLC, Bennett Management Corporation, Citadel Advisors LLC, Eaton Vance Management, JPMorgan Chase Bank NA, Octagon Credit Investors LLC, Southpaw Credit Opportunity Master Fund LP, Stonehill Capital Management LLC, and Voya Investment Management.

*****Use those gift cards people! They’ll be invalid 21 days after the petition date, which reflects a compromise after the debtors originally proposed 14 days and the the United States Trustee raised an objection, arguing that it is not enough time. Somewhat perplexed by the notion that the UST would be arguing for the allowance of certain pre-petition claims against the debtors, Judge Shannon expressed some concerns about the issue of gift cards in bankruptcy but ultimately accepted the parties’ agreement.

******Blue Torch has a second lien on the ABL collateral and did not consent to its use. Moreover, Blue Torch did not agree to be subordinate to a carveout. Willkie must be thrilled with Blue Torch right now.

*******There was some solid first day hearing drama where Gordon Brothers expressed concerns that BofA might stiff them on fees and expenses incurred in connection with pursuit of the GOB sales. It, therefore, requested to be part of the proposed professional fee carveout. BofA wasn’t having it. Gordon Brothers, therefore, baked in language that they could terminate their agreement upon an emergency hearing, insisting that they didn’t want to be put in a position where they were taking on a lot of risk to effectively fund the liquidation of the business.

Moreover, Blue Torch had some concerns that proceeds from certain assets proposed to be liquidated by Gordon Brothers would not be segregated for their benefit but that concern was quickly dispensed with assurances of collateral proceeds segregation.

********For f*ck’s sake, y’all, why does this case need a NY law firm when it’s a liquidation? As much as Willkie must love Blue Torch for disrespecting its carveout, Blue Torch must be thrilled to see Willkie’s fees eat into its pittance of potential recovery.

💥Goodbye, Neumann💥

In last week’s edition…

…we set the stage for Monday’s consequential April 29 hearing on the WeWork Inc. debtors motion for conditional approval of their disclosure statement. Therein we wrote in reference to objector Adam Neumann:

“Bro. Nobody wants to hang with you. Those days are long over.”

Sadly for Mr. Neumann we were dead on. The hearing featured settlements from the left, settlements from the right, settlements from above, and settlements from below. Only none of them included Mr. Neumann.