💥Hello, Neumann💥

With fights brewing everywhere, WeWork could use a dose of "community."

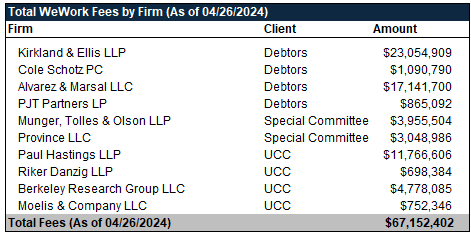

Johnny was being an impetuous f*ckwad this week so we figured we’d give him the sexiest research job imaginable. His mission, should he choose to accept it (lol, he had no choice), was to determine just what the professional admin burn in WeWork Inc. has been to date. And, whoa boy, did Johnny rise to the occasion.

As indicated by the wave of monthly fee statements on file, the recorded pro admin burn in the WE cases amounts to a staggering $67.1mm through the end of March — EXCLUDING what will surely be some hefty March bills from counsel Kirkland & Ellis LLP, financial advisor Alvarez & Marsal LLC and investment banker PJT Partners LP ($PJT). You’ll recall that WE filed the bankruptcy cases on November 6, 2023 and the official committee of unsecured creditors (“UCC”) formed on November 16, 2023, so we’re talking about five months of fees captured in the numbers. Here’s what the tally looks like:

Here’s a live shot of a bunch of WE professionals getting ready in the mornings:

Unsurprisingly, it sounds like these payments are putting at least a little bit of strain on the estate. Here is a significant mention by the debtors in their amended disclosure statement recently filed on April 19, 2024:

“In January 2024, the Debtors and their advisors determined it may be prudent for the Debtors to raise new money, debtor-in-possession financing to carry the Debtors through the remainder of the Chapter 11 Cases.”

And here is some crucial language from the debtors’ reply to UCC and unsecured ad hoc group objections to the debtors’ proposed shortened notice for conditional approval of their disclosure statement:

These Chapter 11 Cases have reached a critical juncture. The Debtors are working around the clock to finish rationalizing their real-estate portfolio and emerge from chapter 11 with a deleveraged balance sheet and renewed prospects for long-term, sustainable growth. Any delay in solicitating the Plan and achieving Confirmation means additional administrative expenses, diminished appeal to prospective new money financiers, and decreased leverage for the Company in its final lease negotiations with an approaching 365(d)(4) deadline. Indeed, as the Objectors themselves recognize, time is of the essence, and it is time to move these cases forward. The Objections should be overruled.

They added:

“As the Debtors previewed in the Disclosure Statement, the Debtors will either secure new money debtor-in-possession financing in the near term or exit financing prior to emergence from chapter 11. In either case, any financier’s willingness to provide funding will depend on the Debtors’ ability to minimize incremental administrative expenses and emerge from chapter 11 as soon as possible.”

Cash-incinerating squabbles aside, the good news is that, on April 24, 2024, Judge Sherwood overruled the objections and scheduled the conditional disclosure statement approval hearing for April 29, 2024 — a measure designed to move these cases forward.

The other good news is that the debtors have apparently addressed nearly 90% of their leases via assumptions, amendments, or rejections. The latter is quite the achievement, honestly, given the rollercoaster of a process that included allegations of unpaid post-petition rent and heaps and heaps of motions to compel payment from landlords.* We reckon several landlords got bent; we reckon several others told the debtors to get bent. And so some took haircuts and others didn’t but it’s hard to argue with the debtors approach to their situation. We already know that the strategy has saved the debtors significant sums of money.

Unfortunately, the UCC doesn’t agree that progress has been made. In an April 19, 2024, objection to the debtors’ request to extend plan exclusivity, the UCC be like:

They wrote:

The Debtors seek conditional approval of a disclosure statement on an emergency basis in an attempt to demonstrate progress towards confirmation of an amended chapter 11 plan, but in truth, the Debtors are no closer to finalizing their placeholder plan and obtaining critical post-petition financing than they were when these cases commenced. The Debtors entered these cases hand-in-hand with their purported secured creditors and equityholders to consummate a chapter 11 plan premised upon a restructuring support agreement (the “RSA”) through the negotiation of their lease portfolio and development of a revised business plan. Importantly, however, the RSA was missing the key economic terms needed for a feasible, confirmable plan of reorganization, including a commitment for post-petition and exit financing to consummate a chapter 11 plan and adequately capitalize the Debtors’ business.

Lol, “placeholder plan.” (Not wrong). They continue:

The Debtors filed an initial chapter 11 plan, consistent with the RSA, on February 4, 2024, and, in the days leading up to the hearing on this Motion (which was adjourned several times), filed the Proposed Plan and Revised Disclosure Statement, each of which raises more questions than answers. Specifically, the Proposed Plan fails to provide the full treatment for any class, contains a potential rights offering with no material terms and envisions a necessary, but nonexistent post-petition financing facility. Now, more than two months after filing the initial plan, the Proposed Plan remains a dead letter because the Debtors, the Ad Hoc Group, SoftBank, and Cupar (all parties to the RSA) have been unable to agree on the terms of the post-petition and exit financing that are necessary to get the Debtors through the remainder of their cases and successfully transition out of bankruptcy. As a result, the Debtors have missed nearly all of the RSA milestones, the cases have stagnated while their liquidity continues to shrink, and the Debtors are now seeking conditional approval of the Revised Disclosure Statement on an emergency basis in an effort to show “progress” in connection with the Motion, effectively trampling on stakeholders’ due process rights.

There it is again, concerns about liquidity. Note the UCC’s contribution to the admin burn in the chart above, LOL (🙄).

In addition to the laundry list of beefs in the quote above, the UCC also flagged the debtors’ alleged unwillingness to entertain potential alternative solutions. Wait. “Potential alternative solutions?” Yep, you guessed it:

Adam Neumann’s involvement isn’t breaking news, we covered it here. But Adam ended up filing a response to the UCC’s objection backing up everything stated therein. Anddd, here’s a live shot of Softbank hearing the name “Adam Neumann” once again:

Adam and the UCC claim the debtors have “refused to provide equal access to existing financial and due diligence” to Adam and his potential co-investors (together, the “Flow Group”).** In fact, according to them, an NDA isn’t even in place yet (LOL) due to the debtors (alleged) repeated rejections of the ones delivered by the Flow Group. Flow Group has apparently offered to provide a DIP alongside a proposed transaction, but the debtors (allegedly) be like:

In a response defending their exclusivity extension request, the debtors be like:

Not kidding. But, to be fair, they list the filing of schedules and statements of financial affairs (for 517 debtor entities!) as just one of many accomplishments over the course of the case — along with, for instance, filing a “viable chapter 11 plan and disclosure statement,” getting the DIP LOC in place, and, as discussed above, addressing 90% of the lease footprint. They underscore the complexity of the cases and their achievements by suggesting in Trumpian fashion that it was all done despite “parallel investigations being conducted by the Special Committee [of the board] and the [Official] Committee [of Unsecured Creditors,” not to mention two motions seeking derivative standing, one of which seeks the appointment of an examiner (we covered that bit here and it looks like the hearing on the examiner motion has been kicked from 4/29’s agenda). As for Neumann, the debtors say that none of his proposals were actionable given the massive debtload and the pre-existing lenders’ unwillingness to consent to a priming DIP. In support of the response, the debtors’ investment banker, Jamie Baird of PJT Partners LP ($PJT), filed a declaration recounting the interactions with Neumann and his band of merry real estate investors.

The UCC was not mollified. In addition to its objection vis-a-vis exclusivity, it filed an objection to conditional approval of the disclosure statement, using many of the same arguments from the exclusivity objection in addition to the normal weak-disclosure-oriented arguments customary for disclosure statement objections.

But Adam Neumann wasn’t mollified either; he filed a declaration featuring a major bone to pick with Mr. Baird. Relating to a $200mm DIP proposal made in January, he writes:

The Baird Declaration states that the Initial Flow DIP Proposal “sought to prime the Debtors’ existing secured lenders” and was therefore rejected by WeWork’s board of directors. But the Baird Declaration fails to mention that the Initial Flow DIP Proposal explicitly indicated that the Flow Group was willing to allow lenders under the existing DIP facility to participate in the Flow Group’s DIP on a pari passu basis, including by allowing such parties to “roll up” a portion of their 1L Notes into the DIP.

JUST KIDDING. THERE’S ZERO CHANCE HE ACTUALLY WROTE, LET ALONE UNDERSTOOD, ALL OF THAT.

The declaration gets better. It documents how, in typical Neumann fashion, he just started throwing hefty numbers around without even a glint of diligence to back them up. His proposal went from $200mm in January to $250mm in March. He writes (LOLOLOL):

On March 11, 2024, the Flow Group provided the Debtors with a revised proposal for up to $250 million of DIP financing (the “Revised Flow DIP Proposal”) which, as Mr. Baird concedes, addressed the Debtors’ purported concern that the Flow Group did not have the wherewithal to provide the financing offered … The Baird Declaration again misleadingly characterizes the Revised Flow DIP Proposal as a “non-consensual priming debtor-in-possession financing proposal,” … notwithstanding that the Revised Flow DIP Proposal—like the Initial Flow DIP Proposal—indicated that the Flow Group was willing to allow existing DIP lenders to participate in its DIP facility on a pari passu basis and would even consider supplying DIP financing on a junior priority basis.

Bro. Nobody wants to hang with you. Those days are long over.

Ok, fine. Mr. Neumann still knows how to get people to hang. Grab a jay and a box of Fruity Pebbles and throw out even bigger gobs of money (sans diligence):

But on March 11, 2024, the Flow Group provided the Debtors and their advisors—including Mr. Baird—with an offer to purchase WeWork or its assets for $650 million, subject to the receipt and completion of adequate due diligence….

Which it apparently didn’t get.

The best part, however, of Neumann’s declaration was when he dives into the newly filed valuation and projections.

The Baird Declaration states that Mr. Baird “believe[s] that the Plan is the most viable and value maximizing path forward.” That belief however is unsustainable given that the Plan sells 80% of the equity of Reorganized WeWork to Cupar (and possibly other “Consenting Stakeholders”) for $400 million, a price reflecting just $500 million of equity value. This appears to be a 34.6% discount to the midpoint equity value of $765 million estimated by Mr. Baird’s own firm. The Flow Group Offer to purchase WeWork’s equity for $650 million vastly exceeds the value afforded by the sale contemplated by the Plan. There is accordingly no basis for Mr. Baird to assert that the Plan maximizes value for the Debtors and their stakeholders.

We mean, get this dude qualified as an expert in valuation because after years of inflating his while at WE’s helm, he definitely knows a thing or two. He likewise knows a thing or two about bullsh*t operating assumptions and metrics. He adds:

Mr. Baird’s belief that the Plan provides “the most viable” path forward is likewise unsustainable in light of the razor-thin margin for error baked into the Plan’s financial projections. For example, the “Projected Statement of Operations” attached as an exhibit to the Proposed Disclosure Statement includes projections for “Occupancy %” and “Physical Member ARPM” (Average Revenue per Physical Member) that cannot be reconciled with the Company’s historic performance after the onset of the COVID-19 pandemic.

He continues:

Additionally, the Debtors’ projections predict a hockey-stick type of increase in occupancy percentage—anticipating a climb of historical occupancy from the mid-70% range to 85%. Neither the Proposed DS nor the Valuation and Liquidation Analysis provide an explanation for how the Debtors reasonably expect to achieve such unprecedented levels, or how those numbers can even be reconciled with the “All Access” membership plans promoted by the Debtors—where a certain cushion of available space must always be accessible.

The Debtors also provide no explanation for the projected increase in APRM from $493/month to $538/month—representing anticipated price hikes that find no comparable expectation in the industry. Just assuming flat and steady occupancy and ARPM over the projection period (no downturn or negative stress of any kind), the Debtors are woefully undercapitalized and would become cash-flow negative by 2025, and would fully deplete their cash by 2027.

Accordingly, the proposed Plan hinges upon overly optimistic financial revenue and cost projections that cannot be reconciled with the Debtors’ historic performance. If these unrealistic projectionsfail to materialize, the Debtors are likely to find themselves undercapitalized and cash-flow negative in the not-too-distant future, which could result in a return of WeWork to chapter 11. This makes the proposed Plan commercially unviable, contrary to Mr. Baird’s assertion.

We can’t speak to the reliability of his conclusions but we did enjoy the recently filed valuation analysis from the fine folks at PJT. Their best guess puts the enterprise value of reorganized WeWork between $650mm and $850mm. Compare that to Adam Neumann’s $650mm bid and to the co-working giant’s once lofty $47b valuation and 🤷♀️.

Neumann does have a point about the financial projections, however. They have reorganized WeWork ending FY’24 with 335 locations and 297.3k members (or nearly 76% occupancy). Revenue is projected to come in at $1.2b for FY’24 ramping up to $2.5b by FY’28 and adjusted EBITDA is expected to be $45mm in FY’24 ramping up to $344mm by FY’28. A far cry from the $3.2b in revenue for FY’22, but at least EBITDA margins are expected to be positive now.*** Oh, and these figures assume increased occupancy from 75.9% at emergence to 79.4%, 81.8%, 83.1%, and 84.7% in the ensuing years. When Mr. Neumann, of all people, is calling BS on optimistic occupancy numbers, we’re in uncharted territory folks.

But cutting through all of this, here’s the question Johnny is just dying to get answered by either the debtors or Mr. Neumann or the UCC for that matter: just what, exactly, is “community-adjusted EBITDA” projected to be in FY’28?

All of this is expected to be addressed — well, maybe not Johnny’s question — at the aforementioned April 29, 2024 conditional disclosure statement hearing — a hearing that is shaping up to be very interesting.

*See our previous WeWork updates for our extensive coverage on the lease issues.

**Flow Group retained Ropes & Gray LLP’s Gregg Galardi to facilitate the NDA discussions. The group is further represented by Quinn Emanuel Urquhart & Sullivan LLP and Friedman Kaplan Seiler Adelman & Robbins LLP.

***Reminder that bankruptcy projections are only incrementally more reliable than SPAC projections. Someone ought to do a law review study on this.

👎 Loser of the Week 👎

Hertz Global Holdings Inc. ($HTZ). Shares of Hertz Global ($HTZ) fell close to 26% on the week…