💥Prescription-Grade Problems?💥

Walgreens posted a surprise quarter but problems persist. Also: Intrum AB.

Walgreens Boots Alliance Inc. ($WBA)(“Walgreens”) operates a jaw-dropping 8.5k(!) retail pharmacy stores across the US, easily making it the second largest pharmacy chain in the country behind fellow behemoth CVS Health Corporation ($CVS). Size, however, doesn’t necessarily translate to success: Walgreens’ stock is down a brutal 77% over the past five years and for its part, CVS is down ~33% over the past year. Investors likely need some potent drugs to blunt that level of pain.

It should obviously come as no surprise whatsoever to long-time PETITION readers that retail pharmacy chains are struggling. We reckon there are quite a few of you out there who still have Rite Aid Corp. PTSD:

Why the struggles across the sector? There’s been a perfect storm of sh*t over the past number of years. To name a few issues, (i) pesky pharmacy benefit managers have pressured the pharmacy chains on pricing, causing increasingly squeezed margins, (ii) massive opioid litigation sparked panic and pause amongst investors, and (iii) new online entrants like Amazon Pharmacy increasingly threaten incumbents and what was historically their most competitive advantage, a convenient neighborhood location. You know what’s more convenient than a convenient neighborhood location? A prescription landing in your mailbox the next day without you having to get off your fat a$$!

To counteract these headwinds, Walgreens decided to make a synergistic acquisition. Enter value-based primary care operator, Village Practice Management Company LLC (d/b/a “VillageMD”).

In July ‘20, Walgreens announced a $1b investment in VillageMD for a ~30% equity stake. The thesis was simple: having an in-store primary care clinic attached to a drugstore should drive higher prescription counts. Patients (with a special focus on those with chronic conditions) will go straight from the physician to the pharmacy next door to fill the prescription. This convenience, the thinking went, would drive higher medication adherence rates and, in turn, improve patient outcomes.

In October ‘21, Walgreens put an additional $5.2b into VillageMD and increased its ownership from 30% to 63%. Curious to see if this strategy worked? Here is the stock performance since the VillageMD acquisition:

That’s right. The stock was trading at nearly $49/share at the time of the acquisition. In other words, this chart is bloody AF.

Since the company started reporting VillageMD as a consolidated subsidiary in FY’21, the value-based care company has accumulated negative $1.1b in adjusted operating losses and negative $678mm in adjusted EBITDA.

And these results weren’t for a lack of trying. The company invested $678mm worth of capex into VillageMD and also made an $8.9b acquisition of primary care provider, WP CityMD TopCo (d/b/a “Summit Health”).

The company originally had plans to expand VillageMD’s footprint and aggressively open clinics, but, for obvious reasons, the company has changed its tune. VillageMD is now set to close locations instead. Walgreens is even weighing a potential sale of the subsidiary.*

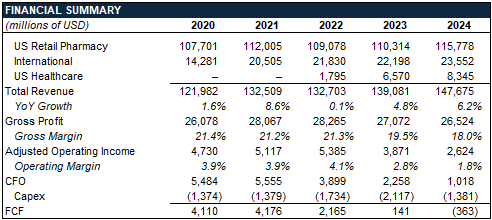

On top of a struggling pharmacy business, the lackluster value based care acquisition has further dragged down consolidated Walgreens performance:

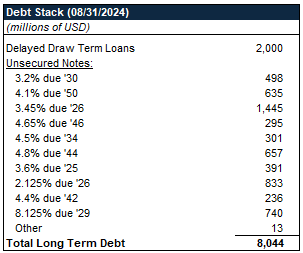

Most noticeably, cash flow has trended significantly downwards since FY’21. The company is sitting on $859mm of cash and $332mm of marketable securities as of November 30, 2024 — down from $1.3b and $1.8b at the end of the prior quarter. Some of that decline is a result of the company’s decision to pay down $290mm under its delayed draw term loans and repay $1.2b of unsecured notes. Even with that paydown, the company has a tremendous debt load:

The farther out on the curve you get, the greater the concern — for obvious reasons. The 3.45% notes due ‘26 were last pricing at $97.31, the 4.5% notes due ‘34 were last pricing at $79.65, and the 4.8% notes due ‘44 were last pricing at $74.77.

The stock and debt prices reflect Walgreen’s eventful ‘24. The company announced additional store closures (~1.2k over the next three years), S&P Global downgraded the credit rating on the company’s unsecured notes from BBB- to BB, and, back in December ‘24, there were even reports of a takeover offer from Sycamore Partners — not to mention rumors of bankruptcy for VillageMD. All of this was so compelling that certain lawyers could be forgiven for jumping to a new law firm dangling then-client Walgreens as a potential juicy future bankruptcy candidate, 😉! Investors, however, were going the other way: the stock promptly jumped 28% on the Sycamore news.

The stock has since pulled ahead over $12/share after last week’s well received Q1’25 earnings release (on January 10, 2025). The company reported positive sales growth in all three segments with VillageMD sales increasing 9% YoY and pharmacy growing comparable sales at 8.5% YoY. However, margins were still low (17.2% gross margins and 1.3% adjusted operating margins) and free cash flow was still negative ($424mm incinerated in Q1’25).

But, there seem to still be levers available for the company to pull. The company raised $750mm in unsecured notes due ‘29 back in August ‘24, with the proceeds used to help pay off the aforementioned $1.2b worth of notes due November ‘24. The company also owns 10.2% of Cencora Inc. ($COR, f/k/a AmerisourceBergen — up 6.2% YTD) and has previously played around with the disposition/public listing of UK pharmacy chain, Boots UK Ltd, for, allegedly, $7b. Coupled with the stronger-than-expected Q1 performance, there appears to be some optionality/runway here — even more so if the company can figure out a way to either continue to improve or dump the VillageMD albatross.

We’ll be keeping an eye on this one.

*Walgreens made this decision on the heels of VillageMD defaulting on a $2.25b intercompany loan.

⚡️Update: Intrum AB⚡️

Way back on November 15, 2024, Intrum AB ($INTRUM.ST) (“Intrum”) and one absolutely bona fide — 😉😉 — affiliate (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez) to effectuate a prepackaged restructuring.*

If you’ve never heard of this company, that checks out: it is a Stockholm, Sweden-based “debt purchase and collection company” and “one of Europe’s largest credit management companies [with] operations in 22 countries.” You might think that, given we have a U.S. chapter 11 on our hands, one of those 22 countries would be the good ol’ US of A, but …

Nope. Not. Even. A. Little. Bit. A few weeks before the filing, Intrum formed a sham totally legitimate subsidiary, Intrum AB of Texas LLC (“Intrum Texas”), for the sole and express purpose of making a U.S. bankruptcy even possible. Outside of cash parked in retainer accounts, the company has absolutely zero, zilch, noll connections to these United States.** It’s not even clear that Intrum Texas has an actual lease for its purported Houston office. When questioned by Quinn Emanuel Urquhart & Sullivan, LLP’s Ben Finestone, representing an objecting ad hoc group of minority bondholders, the debtors’ CEO Andres Rubio certainly didn’t know:

Ben Finestone: [Y]ou don't have any explanation for me, do you, sir, as to how Intrum Texas has its principal place of business at 801 Travis Street if it doesn't own or lease the place, can you?

Andres Rubio, CEO: I do not.So, whether these cases should even continue in ‘Murica, rather than, you know, be heard in any one of 22 potential other jurisdictions, was a bit of a hot button issue.

But before we get there, why are the debtors looking to restructure? Per Mr. Rubio, things haven’t exactly been going great over in Sweden. High inflation, high interest rates, a slowing European economy, and of course, our favorite first-day boilerplate, COVID have put pressure on the company and negatively impacted its portfolios. Moreover, in recent years, the company decided to branch out: rather than just servicing the loans of others, it purchased its own “portfolio investments.” Ahhh, servicers becoming investors, what could go wrong? Anyone want to guess how that went? Yuuuuup, turns out picking winners and losers is a helluva lot harder than servicing, so in ‘23, the company tucked its tail between its legs, “embarked on a shift to a ‘capital-light’ business,” and “pivot[ed] towards its investment management capabilities.”

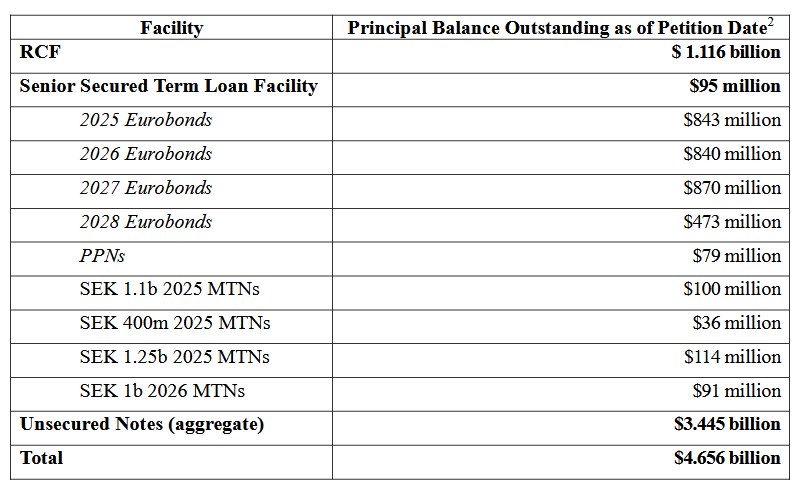

In connection with that “strategic direction,” Intrum offloaded a bunch of that crap those investments to Cerberus in January ‘24 as part of a JV transaction, which the market dumped all over.*** Since then, the company’s suffered more headwinds in the form of credit downgrades (“Between January and July of 2024, Moody’s and S&P each downgraded the Company’s corporate family rating four times (Moody’s was downgraded from B1 to Caa2)”), low debt trading values (“The Company’s unsecured notes traded as low as in the 50-cent range immediately prior to the Company’s restructuring efforts”), and a decline in equity value (“During the course of 2024, Intrum AB’s equity shares have lost more than 80% of their value”). Here’s the company’s capital structure:

Sure, those are real challenges and a healthy amount of debt, but not everything was going to sh*t: over the following months, the company “consistently confirm[ed] that it expected to have cash on hand to repay 2024 and 2025 maturities” and, as of the confirmation hearing, still had a market cap in excess of $3.3 billion (which has subsequently risen about a cool hundo million to ~$3.4b as of writing).

At the same time, and remarkably able to speak out of both sides of its mouth, the company determined it needed a good old-fashioned deleveraging and hired Milbank LLP and Houlihan Lokey ($HLI) to pitch in on that process. That resulted in two noteholder groups forming: a “majority ad hoc group” represented by Latham & Watkins LLP**** and the minority ad hoc group represented by Weil Gotshal & Manges LLP (Quinn Emanuel Urquhart & Sullivan, LLP has since subbed in).*****

After months of “extensive, good faith” (y’all, this phrasing is so, so tired…) negotiations, the company entered into a lock-up agreement with the majority ad hoc group — given the group’s name, hopefully this doesn’t come as a surprise to anyone — which was amended in August ‘24 to bring in the company’s revolving lenders.****** As of filing, 97% of the company’s revolving lenders and 73% of its noteholders support the debtors’ restructuring. Under the proposed deal, (i) the revolving facility would be extended by two years in exchange for more fees, higher pricing, and more collateral (🤑) and (ii) the unsecured notes would take a 10% discount to face in exchange for 10% post-dilution equity, a second lien security interest, and, for consenting noteholders, fees, fees, fees. All other claims would be paid in full, the company would receive $573mm in new money from the issuance of new 1.5-lien secured notes, and equity would ride right on through.

But unfortunately for Intrum and its cohort of cheerleaders, that level of support wasn’t enough to get this deal done without an 11, so in October ‘24, Intrum Texas — with a certificate of formation that was still warm — did what it was born to do: stepped up and, in a brazen act of fraudulent transfer, obligated itself on Intrum’s debt to give the debtors some argument for why they wound up in an American bankruptcy court. The debtors also commenced solicitation of their chapter 11 plan, which happens to contain a very convenient injunction (discussed 👇) arguably prohibiting creditors from objecting to any follow-along Swedish proceeding, which everyone agrees is necessary here. You see, Swedish courts aren’t heaps keen on U.S. courts restructuring Swedish companies, so they don’t recognize those U.S. proceedings (and a Swedish proceeding was always in the cards).

Three days after filing, and not in love with the prospect of taking a haircut on near-maturity debt, the minority ad hoc group dropped a motion to dismiss (“MTD”) for lack of good faith, taking shots at the company’s lack of financial distress, “blatant attempt to manufacture U.S. venue,” and the fact that any confirmation order entered by the court means exactly squat as far as Sweden is concerned.

A few weeks later, on December 12, that same group tossed in a confirmation objection, asserting the plan wasn’t filed in good faith, it impermissibly paid original issue discount (OID), and that the injunction noted above non-kosherly impaired creditor due process rights by preventing them from objecting to any future Swedish proceeding, teeing us up for a confirmation battle royale, which took place from December 16 through 19, 2024.

During that contest, the minority ad hoc group made a few pointed observations: (i) over the past year, the company had repeatedly affirmed its solvency, (ii) Mr. Rubio and the company’s chairman (Magnus Lindquist) were dumping several million dollars into Intrum stock purchases as recently as November ‘24, and (iii) the debtors had zero non-ginned up connections to the U.S. Here’s a live clip of Mr. Finestone in court:

You’d think that second point would be some decent evidence that the company wasn’t in too bad of a shape: rational actors don’t usually piss away their moolah, but then again, #YOLO.

Andrew Leblanc, counsel to the debtors: Mr. Lindquist, you were asked … whether you waste your money, I think it was?

Mr. Lindquist: Yes … I don't waste my money, no.

Mr. Leblanc: Mr. Lindquist, you had a successful career over decades in private equity. Is that right?

Mr. Lindquist: That's right. Thank you. I'll take that.

Mr. Leblanc: And subsequent to that career, you now serve as a chairman of board of a number of companies in Sweden, right?

Mr. Lindquist: Right. Yes.

Mr. Leblanc: Mr. Linquist, while I'm sure you don't want to waste your money, how, if at all, would your life change if you lost money on your investment in Intrum?

Mr. Lindquist: It wouldn't change my life in any circumstance … It wouldn't change my lifestyle, anything, nothing.Haha, is debtors’ counsel seriously trying to sell us on the company’s chairman burning cash for the lulz? Two things. First, we’re starting to understand why this whole “portfolio investments” business didn’t do so hot. And, second, Mr. Lindquist, if you’re reading this, be a sport: toss a few milli over to this hardworking, underpaid PETITION team. Your lifestyle won’t change at all, but ours sure as hell will! Plus, you’ll get all those warm fuzzies from being a righteous dude.

The debtors and their pep squad, of course, did their best to detract from those observations and focus on the company’s economic woes, downgraded credit ratings, and how red, white, and gosh darn blue Intrum Texas is, which seemed to miss, intentionally or not, the point the minority ad hoc group was making.

| image tagged in freedom eagle | made w/ Imgflip meme maker")

In any event, remember that they filed in the Southern District of Texas. Do we really need to tell you what happened?

Of course the court bought, hook, line, and sinker, into the debtors’ narrative and ruled in their favor on both the MTD and confirmation.******* Where do you think we are?

Taking a page from the Serta and Mitel courts, Judge Lopez delivered that ruling on every judge’s new favorite date: December 31. Up first, the MTD. While the court quickly noted that the Bankruptcy Code’s definition of “cause” for dismissal isn’t limiting (for the legal scholars out there, it’s an “includes” definition), it gives sixteen-odd examples. The court’s takeaway:

“...[W]e do learn something from [those examples]. They all refer to post petition acts, failures to act, or events that occur after an estate is created by the filing of a bankruptcy petition.”Therefore, this quite intentionally non-exhaustive, non-limited definition is very much limited after all, and we can — nay, must — happily ignore all the gamesmanship strategizing that made a chapter 11 even possible (like forming Intrum Texas in October ‘24, making it a guarantor of Intrum’s debt, moving cash into the United States). To boot, the court found that the company was in good, old-fashioned financial distress, at least enough to support a filing — debts were going to be coming due, dammit, and it’s quite inconvenient to have to give meaning to a few billion in equity value and the millions poured into stock purchases by management in recent months — best to ignore that. The Bankruptcy Code having been dealt with and inconvenient facts tucked away, the court arrived at good faith and the MTD was toast.

With that off the table, confirmation of the plan was a fait accompli. The court quickly found that it was filed in good faith — technically a different standard than the MTD, but all the same not surprising with the court’s ruling 👆 — and with a few general nods to “OID is a claims resolution issue,” “the plan is a global settlement,” and “the minority ad hoc group is relatively small” to dispose of the OID argument and sidestep fees paid only to consenting noteholders. Turning to the injunction, let’s start with the language:

“Upon entry of the [confirmation order], all Persons and Entities shall be enjoined from taking any actions to interfere with the implementation or consummation of this Plan or the vesting of the Estates’ assets in, and the enjoyment of such assets by, the Reorganized Debtors pursuant to this Plan.”After reading that provision, the court, with a straight face, delivered the following:

“[T]he injunction provisions are I think are customary and appropriate. I don't think they preclude parties from raising issues of Swedish law.”

Really? What do you think the chances are that, if the minority ad hoc group so much as lifts a finger in the Swedish court, the debtors will go tattling to Judge Lopez, arguing that the group is interfering with “the implementation or consummation” of the plan? We’ll peg it at “damn high.” To minimize that issue, perhaps the minority ad hoc group ought to borrow from the debtors’ playbook and form its own totally legit Swedish sub to contribute its claims into.

Taking this ruling on its face, what company, no matter how tenuous its connections to the United States, can’t seek chapter 11 relief? It seems nigh impossible not to qualify — just set up a sub in your choice jurisdiction (SDTX, obvi), load it up with the company’s debt, and throw some cash into a retainer account.

Somehow worse, creditors don’t even have an argument for transferring venue for these all-but foreign debtors. Unlike a U.S. entity that manufactures venue, there’s nowhere else to send them within the borders of the country. Here, there’s quite literally no chance any creditor ever expected to be dragged into a Houston, Texas-bankruptcy court some 5,211 miles from Stockholm — more than one-fifth of the way around the Earth — when purchasing the Euro and krona-denominated debt of a Swedish company lacking any genuine connection to the U.S.

With Serta freshly on our minds, we’d be curious for the Fifth Circuit’s take on this one, and as luck would have it, we might get it some day. The minority ad hoc group appealed both the order denying the MTD and the confirmation order on January 13, 2025.

Get the popcorn handy. 🍿

The debtors are represented by Milbank LLP (Dennis Dunne, Andrew Leblanc, Jaimie Fedell, Melanie Yanez) and Porter Hedges LLP (John Higgins, M. Shane Johnson, Eric Wade) as legal counsel, Advokatfirman Vinge KB (Mikael Ståhl) as special (Swedish) counsel, AlixPartners, LLP (Carrianne Basler) as financial advisor, and Houlihan Lokey ($HLI) (Manuel Martínez-Fidalgo) as investment banker. The majority ad hoc group is represented by Latham & Watkins (London) LLP (Adam Goldberg, Robert Malionek, Elizabeth Marks, Ebba Gebisa, Brian Rosen, Thomas Fafara) and Haynes and Boone, LLP (Charles Beckham, Jr., Arsalan Muhammad) as legal counsel. The ad hoc group of revolving lenders is represented by Clifford Chance US LLP (Brian J. Lohan, Maja Zerjal Fink, Robert Johnson, Madelyn Nicolini) as legal counsel. The minority ad hoc group is represented by Quinn Emanuel Urquhart & Sullivan, LLP (Benjamin Finestone, Sascha Rand, Katherine Scherling, Christopher Porter, Joanna Caytas, Melanie Guzman, Cameron Kelly) as legal counsel.

*We briefly noted it in passing here.

**After doing some soul (and books and records) searching, the debtors were able to find some U.S. A/R owed to Intrum’s non-debtor subsidiaries.

***Really hard to say why. You can read more about Cerberus’ “success” stories here and here.

****Per Docket 49, the majority ad hoc group is made up of BlackRock Investment Management (UK) Limited, Capital Four, Davidson Kempner European Partners LLP, Intermediate Capital Managers Limited, Mandatum Asset Management Ltd., H.I.G. Capital LLC, and Spiltan Fonder.

*****And, per docket 55, the minority ad hoc group is made up of: Boundary Creek Master Fund LP, CF INT Holdings Designated Activity Company, Caius Capital Master Fund, Diameter Master Fund LP, Diameter Dislocation Master Fund II LP, Fir Tree Credit Opportunity Master Fund LP, and Star V Partners LLC. Note that, subsequently, TQ Master Fund LP (Docket 141) and MAP 204 Segregated Portfolio (Docket 143) joined the minority ad hoc group.

******Who are, per docket 56, these fine Nordic financiers: Danske Bank A/S, DNB Bank ASA, Nordea Bank, Nykredit Bank, Skandinaviska Enskilda Banken AB, and Swedbank AB.

******* The court also overruled the US trustee’s confirmation objection, which focused on the opt-out, rather than opt-in, nature of the plan’s third-party releases.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

🍾Congratulations to…🍾

Brown Rudnick LLP (Robert Stark, Bennett Silverberg, Jeffrey Jonas, Steven Levine, Tristan Axelrod, Matthew Sawyer) and Kane Russell Coleman Logan PC (Joseph Coleman, John Kane, JaKayla DaBera) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Stoli Group (USA) LLC chapter 11 bankruptcy cases.

David Lorry for his promotion to Principal at The Brattle Group.