💥Risk on AF💥

Spirit Airlines Inc., Petroquest Energy Inc., Vroom Inc. + More

How’s this for consistency ⬇️:

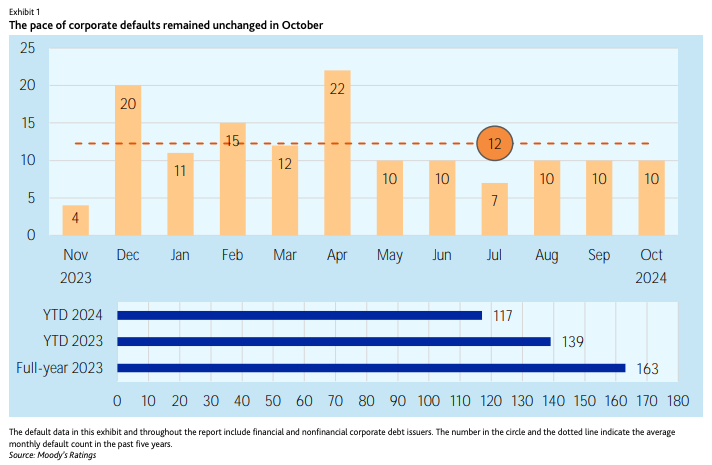

The chart — from Moody’s Ratings (“Moody’s) — shows (i) default activity across Moody’s-rated issuers in October ‘24 and for the TTM and (ii) YTD default default activity against ‘23 (which is down by 22).* The back half of the year has some impressive consistency. Per Moody’s:

"All of October's defaulters were from the US. Unlike recent years when distressed exchanges generally accounted for more than half the defaults, only three defaults were distressed exchanges in October. Nonetheless, we expect distressed exchanges to rebound through year end and remain elevated in the foreseeable future because they help issuers in cost savings and equity preservation."What a bold call, guys! Really going out on a limb there, 🙄. In the last week alone, we’ve seen iHeartMedia Inc. ($IHRT), Empire Today, Lasership and FinThrive all engage, at various stages, in liability management transactions.

Moody’s went on to note that the TTM global speculative-grade default rate dipped to 4.6% from 4.7% in October on a month-over-month basis. While they caveat the sh*t out of their predictions given the transfer of power to the second Trump administration in January … with tariffs, specifically, of concern …

… Moody’s continues to expect aggressive rate reductions in the US and in Europe, a clear benefit to highly levered issuers. Whether those benefits are offset by higher unemployment and consumer skittishness is to be seen.

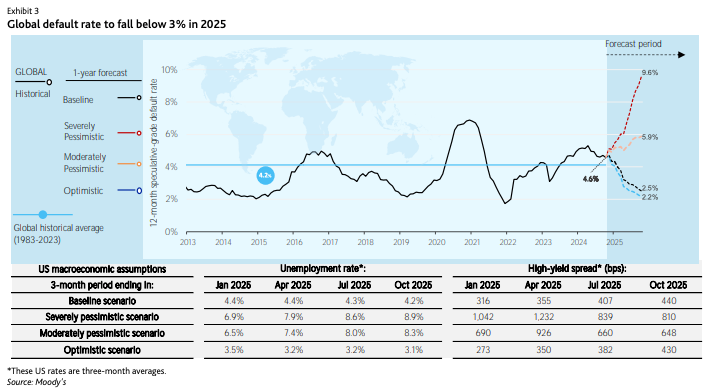

What does Moody’s see for ‘25? Well, this ⬇️:

What this shows is an expectation that the global default rate will dip to 2.5% by this time next year. Moody’s notes:

“Robust 2024 issuance has helped speculative-grade issuers reduce their near-term refinancing and default risk. However, risky credits with high leverage and low interest coverage ratios, will continue to struggle. Distressed companies that restructured through distressed exchanges in recent years without cutting debt to sustainable levels can default again.”Music to RX professionals’ ears!

But it gets better. Moody’s was talking about the rosiest of scenarios. Moody’s wants to manage expectations given macroeconomic and geopolitical risks out there:

“While our baseline scenario does not expect a sharp increase in corporate default rates over the next 12 months, certain economic and financial developments outside our baseline expectations could lead to a higher default rate. Therefore, we have also developed moderately pessimistic and severely pessimistic scenarios, which may unfold if one or more of the following were to crystallize: greater macroeconomic disruption because of geopolitical risks; growing protectionism including larger tariffs that lead to greater disruption in trade and supply chains, causing inflation re-acceleration and a sharper global economic slowdown; and stress in any part of the financial sector (e.g., commercial real estate) that spills over into the economy more broadly.

Under our moderately pessimistic scenario, the US high-yield spread would widen to as much as 926 bps in the coming four quarters and the unemployment rate would rise to 8.3%. Under this scenario, the global speculative-grade default rate would increase to 5.9% by the end of October 2025. Our severely pessimistic scenario assumes even weaker macroeconomic conditions, with a surge in the US high-yield spread to as much as 1,232 bps and a jump in the unemployment rate to 8.9%. Under this scenario, the global speculative grade default rate would rise to 9.6% in a year, reaching the peak level after the dot-com bubble burst in 2000.”Whoa. Nothing like f*cking around with a few assumptions, 💪. Really gets the juices flowing.

B. Cap Markets are WIDE Open

For now, though, it seems very few RX pros have visibility into ‘25 — Latham & Watkins LLP’s bullishness notwithstanding. Indeed, one reason for low defaults is that we’re risk-on-as-f*ck baby. And we’re not even talking about Bitcoin!

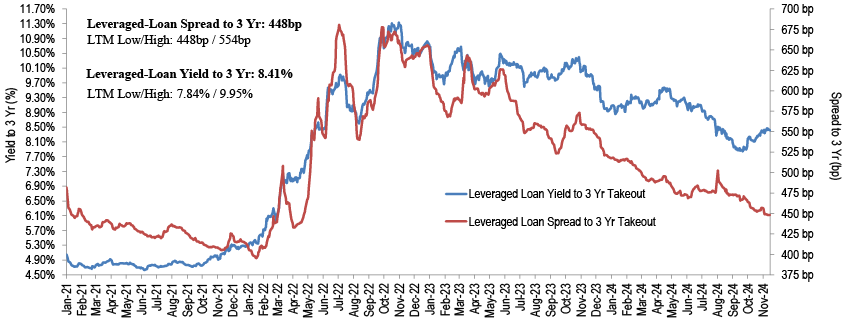

The leveraged loan market is absolutely HUMMING right now. YTD volume is over $1.1 trillion, making ‘24 the most active year EVER. And most of the volume is in the refinancing space given limited M&A activity (which people seem very optimistic about in ‘25 with a new administration and less regulatory scrutiny in place). Look left, look right, and you’ll find a new CLO being formed, eager as ever to gobble up loans. That’s right, CLO creation is on pace for its most robust year ever ($176b YTD!).

All of which has had the effect of compressing spreads.

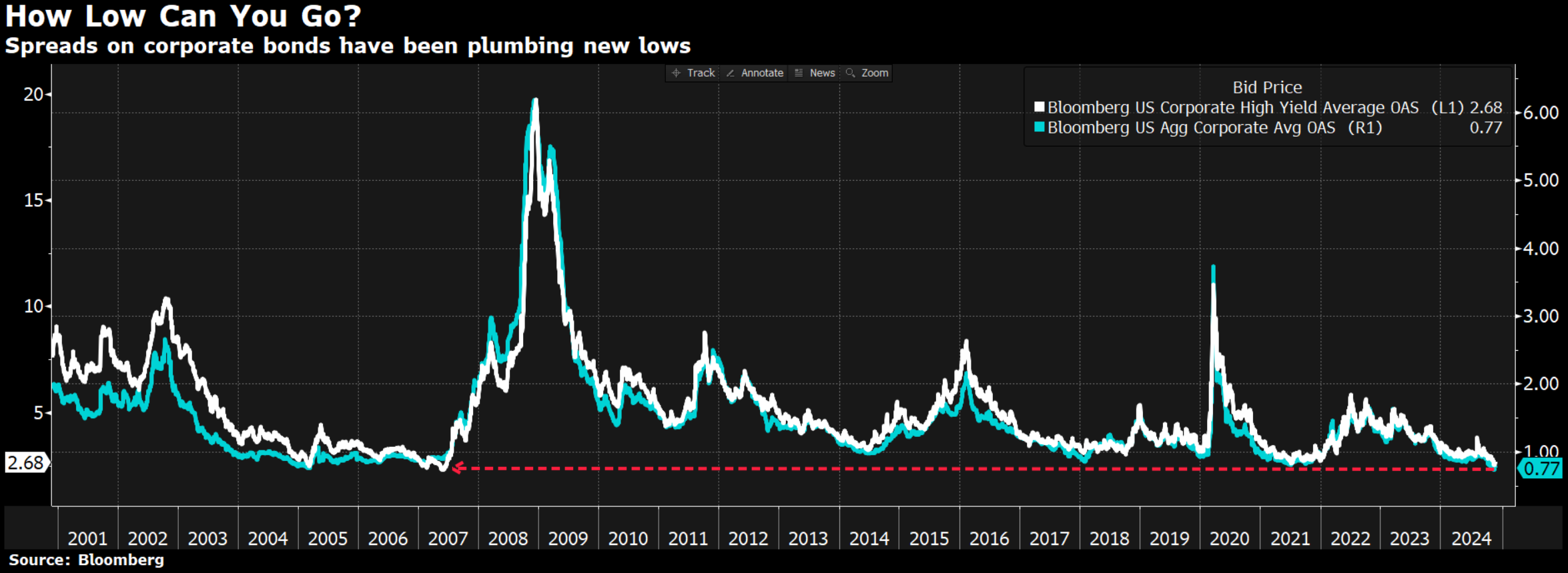

And then there’s corporate bond spreads, which are getting increasingly narrow …

… conjuring up concerns and comparisons to ‘07. Last week spreads hit a post-Great Financial Crisis low of 297 bps before ticking back up slightly this week. This is like taking a time machine back to June ‘07, folks.

C. Consumer

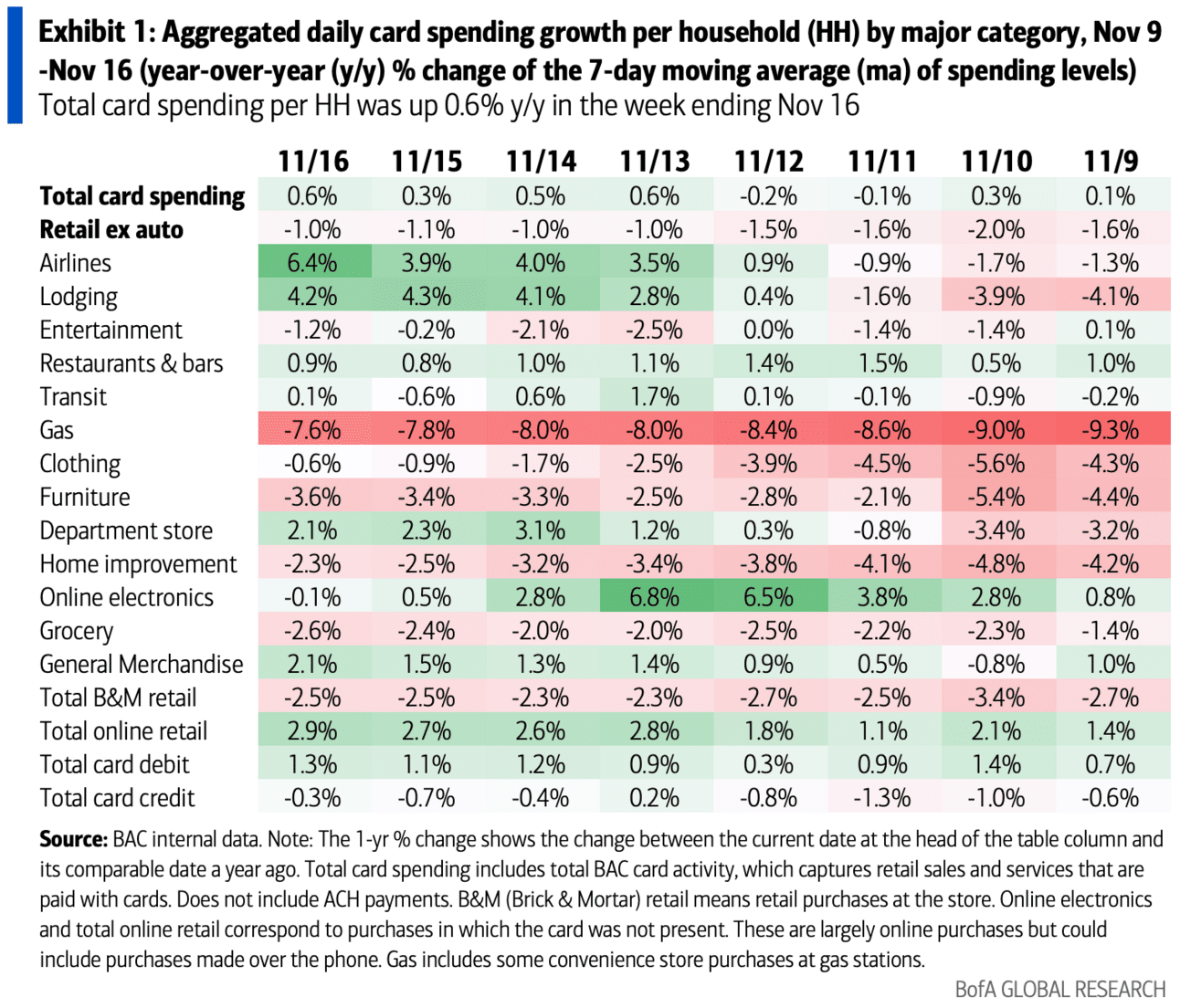

Consumers are consuming. Just take a look at card spending:

Bank of America ($BAC) CEO Bryan Moynihan recently exclaimed:

"The consumer was slowing down in late summer—we saw it. It was concerning me because I thought it was slowing down to the point where it may be underneath what would imply a stable 2% (plus or minus) growth economy with lower inflation. The good news is, as we came into September and October if you look at the two months together—particularly October—it looks like it's leveling out. The expectations of our consumers to spend more in the holiday season are up by 7%, which is good"Truist Financial’s ($TFC) Senior EVP Dontá Wilson added:

"If you look at consumers' liquidity position, this is retail consumer, they're indexing 120 to pre-Covid. So they have good liquidity... If you look at some of the things that's happening with their savings, they're saving 100 bps more than they were saving last year. And so that's putting the consumer in a really, really good place."The question going into this week was what earnings from Target Inc. ($TGT) and Walmart Inc. ($WMT) would indicate about the strength of the consumer. Well, here is TGT after reporting:

Riiiiiiiiiight. Clearly the market was very displeased with the report. Citing “lingering softeness in discretionary categories,” the bigbox retailer missed revenue estimates by 1% and came in $0.45 EPS below consensus. Same store sales rose merely 0.3% YOY. Comp sales fell 1.9% YOY. One positive: digital sales, which increased 10.8% YOY. After raising guidance last quarter, TGT lowered guidance back down — and the market punished them accordingly. Management here seems to … how should we put this … suck. They knew consumers were becoming more discerning with their spend and didn’t respond appropriately. For instance, costs remain elevated, unable to offset margin compression. The stock is down ~55% from its ATH. 😬

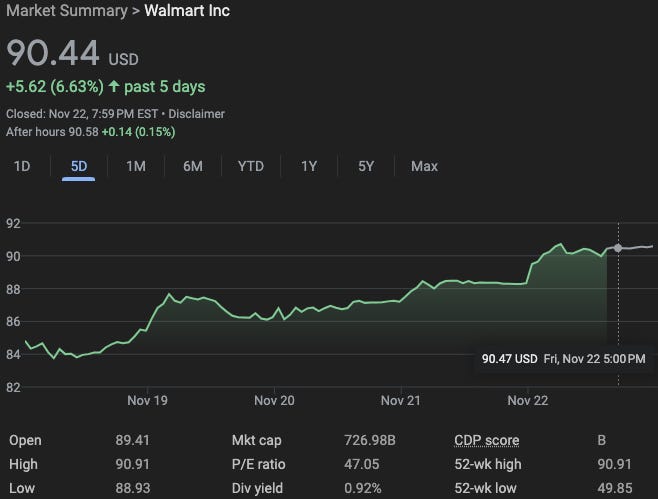

On the flip side, Walmart absolutely crushed. For its Q3’25, it surprised to the upside with revenues of $169.6b (beast!) up 5.5% YOY. E-commerce grew by 22% in the U.S., blowing away analyst expectations of roughly 2.2%. Yes, you read that correctly: twenty-two versus two-point-two. E-commerce sales were up 43% internationally. Grocery was a huge pick-up for the business, and EPS came in $0.05 greater than expected. The stock went up 6.6% on the week.

It seems TGT is an outlier and the consumer just keeps humming along.

D. Bankruptcy Activity

Wow, 🤯, chapter 11 volume — and size! — has suddenly picked up in November. In the last three weeks, there’s been a meaningful cohort of case filings with meaningful amounts of funded debt:

📍Franchise Group (Willkie Farr & Gallagher LLP)($1.9b);

📍Intrum AB (Milbank LLP)($4.56b);

📍Spirit Airlines Inc. (Davis Polk & Wardwell LLP)($3.6b);

📍Northvolt AB (Kirkland & Ellis LLP)($5.8b); and

📍H-Food Holdings LLC a/k/a Hearthside Foods (Ropes & Gray LLP)($3.1b).

If we wanted to be generous, we could throw in these two also:

📍Wellpath Holdings Inc. (McDermott Will & Emery LLP)($644mm); and

📍CareMax Inc. (Sidley Austin LLP)($423mm).

Note, also, the firm coverage. Given the big personnel moves this week, it’s notable that Latham & Watkins LLP, Weil Gotshal & Manges LLP and Paul Weiss Rifkind Wharton & Garrison LLP are absent from this list, 🤷♀️.

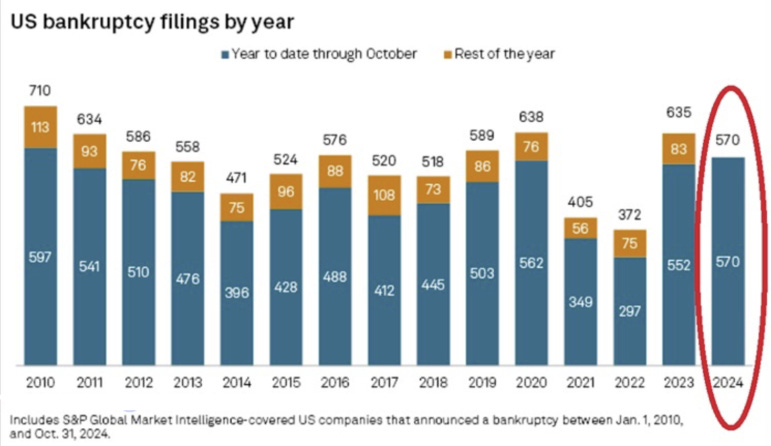

Still, even a robust November ain’t going to change our general assessment that ‘24 has, by and large, been a year chock full of dogsh*t cases. Sure, the YTD numbers show robust filing activity but read the fine print folks:

Greater than or equal to $2 million. Get the f*ck out of here, S&P.

*Of the 10 defaults, Moody’s notes that seven were in the leveraged loan space and the remaining three in high yield. The issuer-weighted US loan default rate as of the end of October is 6.9% and high yield is 2.8%, both down from September.

✈️That's the Spirit. Part II.✈️

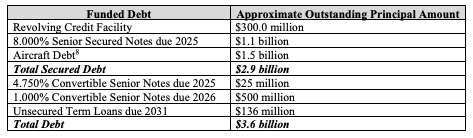

On November 18, 2024, FL-based Spirit Airlines Inc. ($SAVE) filed a prearranged chapter 11 case in the Southern District of New York (Judge Lane) to address its $3.6b of aggregate funded debt:

The downfall of this beloved carrier (🖕) sparked cries across the internet:

Hell, there’s even a letter sent to the court bemoaning the Spirit experience:

“The debtor is very well known to have a years long practice of offering the worst customer service in the nation. Now, they want to use the courts to get relief from their debts and obligations that are a direct result of management and its employees treating the American traveling public with less dignity and respect. Cattle in 19th Century Chicago Stockyards were treated better.”This emergency landing in chapter 11 stings just a little more when looking at the debtors’ previous suitors, JetBlue Airways Corporation ($JBLU) and Frontier Group Holdings Inc ($ULCC), both of whom are up YoY:

We went over the merger struggles and operational issues in our previous coverage here…

… so let’s dive straight into what this deal is and what it isn’t ⬇️.