💥Telecom!💥

We’re back y’all! We spent the weekend murdering pink and yellow-dyed marshmellow peeps and cadbury eggs and holy f*ck we’ve got a ton of sugar in our systems so hold on to your butts, we’re about to do a Q1’24 review before we merely skim the surface of the absolute sh*t show that was the first 24 hours of Q2’24. Warning: if this comes off as mildly disjointed, don’t @ us, consider it a public service announcement that ingesting 42,322,666 grams of sugar over a weekend is probably not a great idea. You heard it here first.

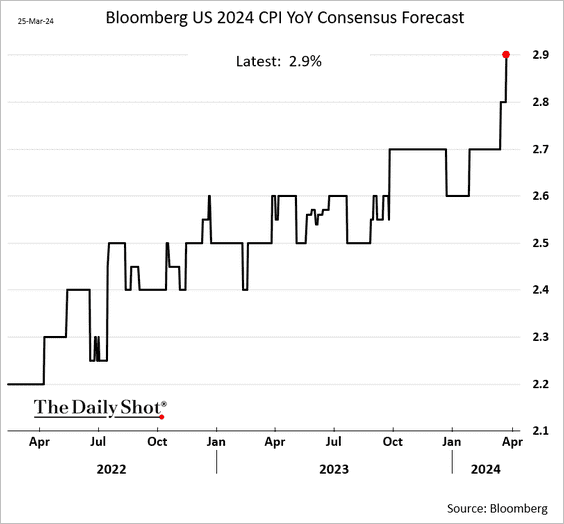

Let’s lead off with the MVP of the quarter, Fed Chair Jerome POW-ell. Here is Mr. POW-ell speaking at the San Francisco Federal Reserve Bank’s Macroeconomics and Monetary Policy Conference on Friday, March 29, 2024 — after PCE figures came in at 2.5% headline (higher, bad!) and 2.8% on a core twelve-month basis (lower, good!). Zoom in just a bit and over the last three months, core inflation clipped at a 3.5% annual rate, up from 1.6% in December and the highest in nearly a year. That’s … uh … not necessarily bullish for the rate cut crowd.

When challenged on Friday about whether it’s time to start lowering the Fed funds rate, Mr. POW-ell urged restraint saying, “We don’t need to be in a hurry … the fact that the US economy is growing at such a solid pace, the fact that the labor market is still very, very strong, gives us the chance to just be a little more confident about inflation coming down before we take the important step of cutting rates.” Indeed, as of March 28, 2024, the US Bureau of Economic Analysis indicated that Q4’23 GDP chugged along at a 3.4% annual clip, as labor and consumer spending remain strong.

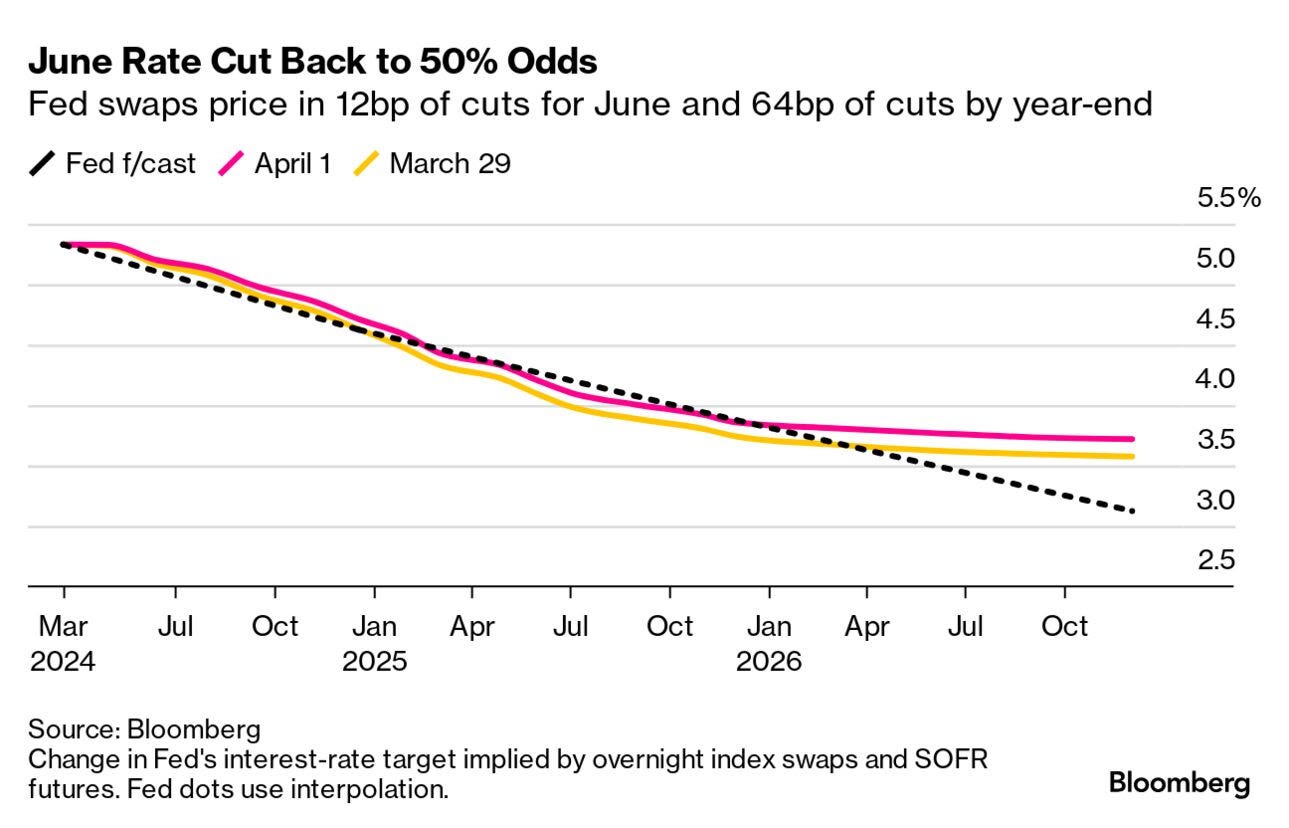

POW-ell’s sentiment is one of the major stories of Q1’24: after some elevated inflation numbers in January, the Fed held steady at current rates, forcing the market to come to terms with the fact that interest rates would, in fact, stay “higher for longer.” Indeed, all of those market predictions of six rate cuts in ‘24 be like:

Wonky numbers in February validated that stance. "Our hand is a steady hand in this," Powell said. "We didn't overreact to the good data we had in the second half of last year ... and you won't hear us overreacting to these two months that are higher." Notably, Federal Reserve Governor Christopher Waller commented on Wednesday March 27, 2024, before the Economic Club of New York, “In my view, it is appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data…,” and that was before the PCE figures came out. 🤔

The market is reacting. Many appear to think that inflation will continue getting worse, not better.

On Monday, April 1, 2024, we got an ISM manufacturing report for March that surprised people, showing expansion for the first time since July ‘22, and further feeding the narrative that rates may not be going anywhere anytime soon.

Markets appear to be betting on it, a major reversal of where overnight swaps and futures were mere months ago.

Powering this growth continues to be the consumer — yes, the very same people we’ve been told for a year now were running out of their pandemic-era cash stash and getting increasingly spend-cautious. Apparently there is some real bifurcation happening here, with some legitimate pain in the subprime and lower income echelons — a point we highlighted on Sunday, March 24, 2024. The numbers don’t particularly reflect the dichotomy. Here is a good paper diving into some of the weeds on this subject:

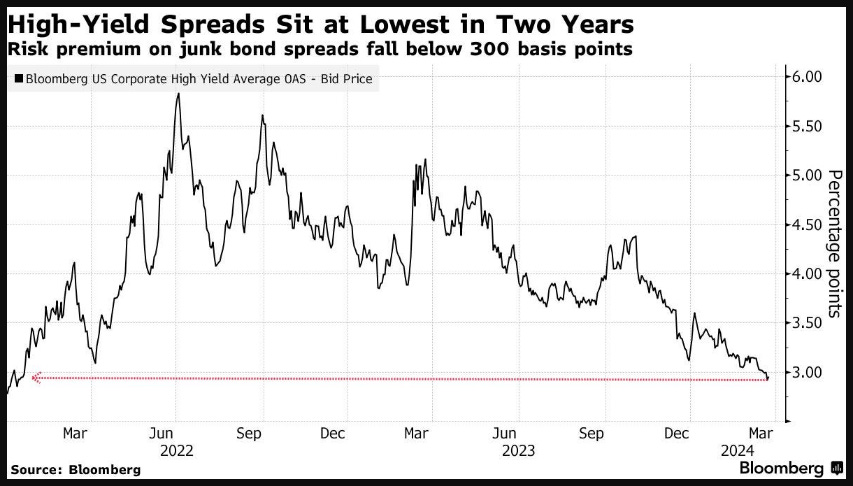

Of course, as we’ve discussed quite a bit over the quarter, neither the capital markets nor the equity markets1 seem to give a flying f*ck about “higher for longer.” Spreads are tight…

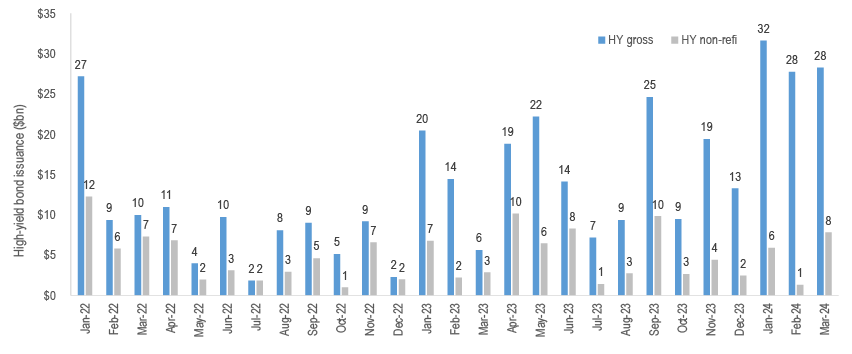

…and corporates are borrowing:

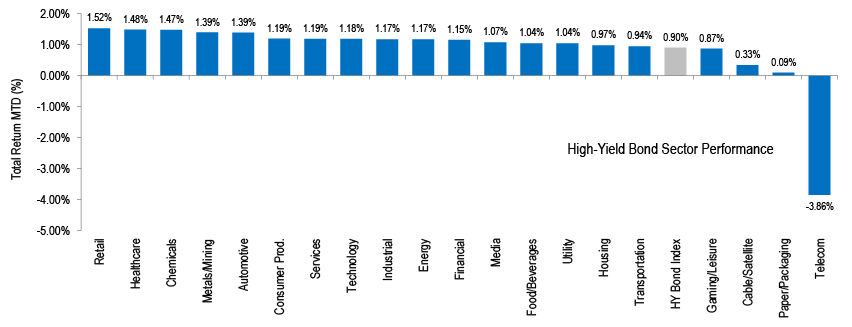

That’s right. Q1’24 high-yield issuance is ripping with quarterly new issue volume the best it’s been in years. Generally, high-yield sector has performed well with one very notable exception:

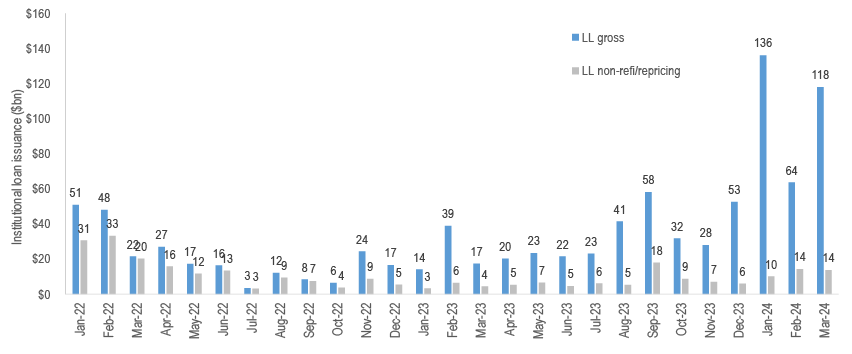

Similarly, leveraged loan issuance is almost literally off the charts:

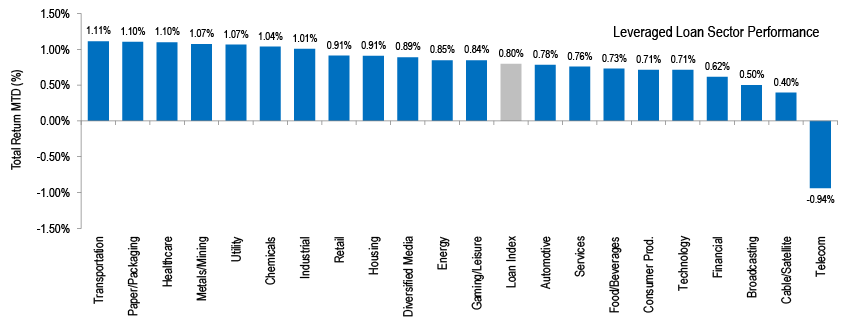

Q1’24 was the second most active quarter EVER and performance was almost universally positive with … wait for it … one notable exception:

Surely a number of you LME folks are very well aware of this outlier (cough, cough Lumen Technologies, Dish Network, Sinclair, etc.).

Issuers are taking advantage of tight spreads and tapping capital markets, effectively pushing out the always-dreaded-and-almost-never-really-relevant maturity wall.

Still, there are some defaults. Per Fitch Ratings:

The leveraged loan TTM default rate ended February at 3.7%, up from 3.4% in January, in the fifth consecutive month of rising loan default rates, while the high-yield (HY) TTM default rate was 3.04%, up from 2.79% at the end of January, according to Fitch Ratings.

Eight leveraged loan issuers defaulted in February for a total volume of $8.52 billion, the highest monthly total since May 2023, as issuers continued to struggle with high leverage, looming debt maturities and depressed operating performance that frequently manifested in extended and ongoing periods of negative FCF. Four of the eight defaults were distressed debt exchanges (DDEs). (emphasis added)

Note that the default rate does not necessarily equate to in-court bankruptcy activity due to, among other things, excessive amounts of LME processes working their way through the system and the rise of private credit. Fitch added:

Fitch’s Market Concern Loan and Bond lists added seven unique issuers this month due to significantly deteriorating credit profile, including Weight Watchers, Radiate Holdco and Rackspace Technology, all of whom hold leveraged loan and HY debt. Companies on Fitch’s Market Concern lists continue to face serious challenges around sizable near-term debt maturities placing them at refinancing risk, and/or continued declining operating performance leading to depressed revenue generation without a clear path to recovery. Issuers are frequently left with few options but to engage in DDEs or file Chapter 11, which has driven default volume higher.

Startups, however, are going belly-up at an impressive clip:

Good for those of you who make some decent coin doing assignments for the benefit of creditors!

As for the rest of you? Well, you can read our assessments of January here…

…and February here…

In March we saw the continuation of a number of chapter 11 trends:

📍Delaware remains the resurgent venue of ‘24 as filers largely shun the Southern District of Texas.

📍But New Jersey continues to draw interest as a venue too. While Kirkland & Ellis LLP picked up where it left off ‘23 with multiple filings in NJ in Q1’24, what’s interesting is that others are now beginning to follow. Sidley Austin LLP filed BowFlex Inc. in NJ in the beginning of March.

📍Prepacks and 363 sales continue to dominate the filing landscape. Charge Enterprises Inc.? Prepack. JOANN Inc.? Prepack. CURO Group Holdings Corp.? Post-LME prepack. Airspan Networks Holdings Inc.? Prepack.

📍Nearly all of the notable filings in March were public companies. See $BFX, $CRGE, $EVA, $JOAN, $CURO and $MIMO.

📍GOL Linhas Aéreas Inteligentes S.A. remains the only case thus far in ‘24 with over $2b in funded debt. In March, three more companies in the $1b-$2b range filed for bankruptcy: Enviva Inc., JOANN Inc., and CURO Group Holdings Corp. Sub $2b of funded debt seems to be where all the action is these days.

As far as accolades go, there was nothing really compelling about March as deal flow was generally scattered (though, on the creditor side, it just seems like Gibson Dunn & Crutcher LLP is rolling right now). A number of firms had good quarters: Kirkland & Ellis LLP, PJT Partners LP, AlixPartners LLP, Alvarez & Marsal LLC, and Guggenheim Securities LLC stand out in terms of the relatively bigger deals. Still, other firms seem to have their tentacles in a lot of places, including Sullivan & Cromwell LLP, Oppenheimer & Co., and SSG Advisors LLC.

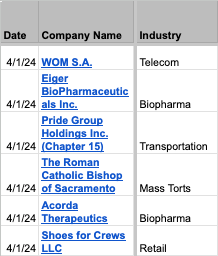

Apropos of the aforementioned charts underscoring pain in the telecom sector, Q1’24 closed with the telecom filing of Airspan Networks Holdings Inc. (discussed below). And, curiously, Q2’24 opened with the telecom filing of WOM S.A. (also discussed below). WOM was just one of six — ⚡️yes, SIX ⚡️— filings on April 1, 2024, a blockbuster start to a new quarter.

Does the explosion of (relatively small and disparate) cases over 24 hours portend things to come in the quarter? Or is this just some sort of April Fool’s joke to get RX pros’ hopes up?

Stay tuned to your friends at PETITION to find out.

💥New Chapter 11 Bankruptcy - Airspan Networks Holdings Inc. ($MIMO)💥

On March 31, 2024, FL-based Airspan Networks Holdings Inc. ($MIMO)(“Airspan,” and, collectively with three of its affiliates, the “debtors”) filed straddle prepackaged chapter 11 bankruptcy cases in the District of Delaware (Judge Horan). The provider of software and hardware for 4G and 5G networks for both public telecom service providers and private network implementations felt compelled to end (i) our Q1 as a rare busted-deSPAC-sh*tco (see New Beginnings Acquisition Corp.) to hit the bankruptcy bin in ‘24 and (ii) Softbank Group’s quarter2 with another busted equity investment. Good frikken times.

What does Airspan do? F*ck if we know. Read this and see if you can make heads or tails of it:

The Company offers a broad range of software defined radios, broadband access products and network management software to enable cost-effective deployment and efficient management of mobile, fixed and hybrid wireless networks. The Company’s customers include leading mobile communications service providers (“CSPs”), large enterprises, military communications integrators and internet service providers (“ISPs”) working to deliver high-capability broadband access to numerous markets. The Company’s mission is to disrupt and modernize network total cost of ownership (“TCO”) models. The Company aims to lower costs for customers throughout the product lifecycle, from procurement through commissioning and ongoing operating costs.

Yeah, we still don’t know. As a practical matter, your gawd-awful in-flight Gogo wifi experience appears to be powered by an Airspan enterprise private network. Similarly, Airspan tech helps IT-company Thales provide coverage in the New York City subway system. Which, for Johnny at least, never seems to f*cking work. 🤷♀️

Anyway, it doesn’t matter. There was enough razzle dazzle in there to attract a SPAC sponsor (lulz) and go public — despite the fact that this thing basically hemorrhages cash, having “incurred significant operating losses in part due to its commitment of significant resources to research and development….” PS, attracting a SPAC sponsor in the beginning of ‘21 is a pretty low bar and most investors saw this thing for the turd it is even back then. The deSPAC transaction closed in August ‘21 (lol, of course) and, after taking into account heaps upon heaps of redemptions, only raised $115.5mm of which $75mm was a PIPE and $50mm was convertible notes issued to Fortress Investment Group (“Fortress”). Per the debtors’ disclosure statement, “The De-SPAC Transaction and the PIPE Financing did not result in sufficient capital for the Company and, as a result, the Company had to rely on further financing from senior secured lenders. The Company was thus left in an over-leveraged position given its subsequent revenue performance.” Basically this 💩 was in “strategic alternatives” mode the second it hit the tape. Like, seriously, folks. Per the debtors’ disclosure statement, “Beginning in September 2021, Airspan began exploring a strategic transaction to maximize the value of the enterprise for its stakeholders.” LITERALLY A MONTH AFTER THE DESPAC DEAL CLOSED, LOLOLOLOL.

About that “further financing.” There was a lot of it over time such that the petition date capital structure looks like this:

And that’s after the debtors sold the common stock of a business associated with Airspan’s affiliate Mimosa Network for $60mm in March ‘23 and used $45mm of the proceeds to pay down senior secured debt.

The “further financing” and asset sale weren’t enough to ward of continuing liquidity problems brought on — in addition to the leverage out of the gate — by pandemic-induced supply chain disruptions and inflation. Consequently, the debtors formed a special committee of three independent directors and, once again, evaluated strategic alternatives including a (failed) sale and marketing process. To pursue this process and, once it failed, pivot towards a balance sheet restructuring, the debtors’ lenders (read: Fortress) funded $37.4mm of the above-noted debt between December ‘23 and March ‘24. Ultimately this money bought everyone a restructuring support agreement (“RSA”) — supported by 95% of the senior secured lenders and 100% of the subordinated term lenders — and the proposed plan filed on the petition date.3**

So what does this proposed plan accomplish? A number of things:

📍It fully equitizes the $205mm of total funded debt with (a) the senior secured creditors getting 94.375% of the post-reorg equity subject to dilution by (i) the MIP, (ii) the new money infusion (see immediately below), (iii) the warrants (see lower down), and (iv) the backstop premium (also see lower down) and (b) subordinated creditors — both term lenders and convertible noteholders alike — getting 5.625% of the post-reorg equity (subject to same dilution as senior secureds);

📍It infuses $20mm of new money into the post-reorg company as part of an overall $95mm pre-petition-senior-secured-creditor-backstopped “equity investment opportunity” (that otherwise pays down the proposed DIP, discussed below, and of which $90mm of the “opportunity” is available to the senior secured creditors and the remaining $5mm offered ratably to the subordinated term creditors);4

📍It pays general unsecured creditors in full (the DS notes ~$2mm of trade);

📍It contains an equity death trap that provides ratable sharing of a $450k cash distribution available to equityholders who do not opt out of proposed plan releases or, in lieu of cash, an opportunity to elect to receive warrants that, if the company were to basically triple its implied enterprise value, be worth up to 3% of the post-reorg equity.

The debtors intend to fund the bankruptcy process via a $55.5mm DIP credit facility ($7.5mm interim) within which the debtors and the senior secured lenders intend to roll-up the aforementioned $37.4mm. The DIP will accrue PIK interest and carry a 3% commitment fee (of all DIP obligations, earned upon entry of the interim order) and a 3% exit premium payable at maturity (if not earlier under the plan).

The debtors’ first day hearing is later today, April 2, 2024 at 11am ET.

The debtors are represented by Dorsey & Whitney LLP (Eric Lopez Schnabel, Samuel Kohn, Alessandra Glorioso, Michael Galen, Rachel Stoian) as legal counsel, VRS Restructuring Services LLC (Jeffrey Varsalone) as financial advisor, and Intrepid Investment Bankers (Lorie Beers, Carl Comstock) as investment bankers. The senior secured creditors are represented by Davis Polk & Wardwell LLP (Damian Schaible, David Schiff, Amber Leary) and the consenting subordinated lenders are represented by Sidley Austin LLP (Stephen Hessler, Anthony Grossi, Jason Hufendick).

💥New Chapter 11 Bankruptcy Filing - WOM S.A.💥

We’re kicking of Q2’24 with a trip to South America!

On April 1, 2024, Santiago Chile-based WOM S.A. (“WOM” f/k/a Nextel Chile S.A.) and five affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge ). WOM is a telecom provider, providing mobile voice, data, and broadband services (including 5G) plus its “Fiber to the Home” broadband offering to Chilean consumers and businesses; it claims it’s the second largest mobile network operator in Chile with a total customer base of 8.5mm customers, of which 1mm are 5G wireless broadband customers; it also purports to have four-band spectrum that blankets approximately 26% of Chile.

Despite the millions of customers and expansive coverage, the debtors have had liquidity issues, many of which stem from a March ‘23 Fitch Ratings downgrade of the debtors’ US-dollar-denominated ‘24 and ‘28 unsecured notes (issued by Kenbourne Invest S.A. and collectively totaling $649mm). The downgrade brewed a perfect storm; it (i) triggered a margin call on certain derivative contracts that cost the company tens of millions of dollars between Q2’23 and Q4’23, and (ii) sparked a $50mm credit reduction of a $100mm credit facility provided by the Inter-American Investment Corporation, an affiliate of Inter-American Development Bank (the “IDB”)(which had further financing implications for the debtors). A Moody’s Investors Service downgrade in November ‘23 (following an earlier one in April ‘23) resulted in the IDB closing the credit facility altogether, diminishing access to credit and creating a repayment obligation.

As if the loss of tens of millions of dollars due to above wasn’t enough, the debtors have been battling with the Chilean government — the parties are in an international arbitration — over the construction of cellular towers necessary for the rollout of the debtors’ 5G network.5 The debtors intended to enter into sale-leaseback transactions vis-a-vis the towers (a global tower infrastructure operator called Phoenix Tower International): the delay obviously got in the way of that plan, costing the debtors ~$25mm that they’d modeled for liquidity purposes. Yes, tens of millions (IDB) + tens of millions (margin call) + tens of millions (sale-leaseback) = heaps of liquidity gone! 😳

Which gets us back to those 24s: there’s $356mm-worth and they mature in November! These ⬆️ developments no doubt created some refinancing risk. The debtors hired Rothschild & Co. US Inc. (Marcelo Messer) to scour the markets but it became abundantly clear that an out-of-court financing was not gonna happen. Rothschild, therefore, pivoted to DIP financing to address the debtors’ increasingly dire liquidity needs.

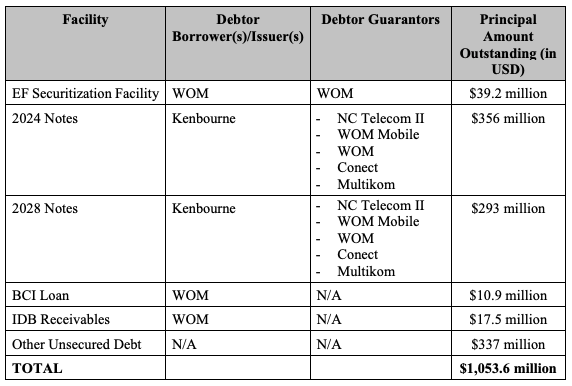

Before we get to the DIP it probably makes sense to outline what the overall cap stack looks like. So here it is:

As you can see, in addition to the 24s and the 28s, the debtors also owe approximately $39mm on account of a securitization facility and $10.9mm on a loan from Banco Scotiabank. Furthermore, the debtors owe IDB approximately $17.5mm on account of a receivables transfer agreement. Behind all of that is approximately $337mm of unsecured debt owed to vendors, taxing authorities, employees, and other contract counterparties.

The debtors’ proposed DIP financing is a $210mm multi-draw 10% cash pay term loan facility (the “DIP”) agented by JPMorgan Chase & Co. ($JPM). The DIP here is very different from what we’ve become accustomed to seeing in bankruptcy these days: there’s no priming liens, no roll-ups, and no harsh milestones forcing an expedited case. The proceeds will be used to repay the ~$39mm owed under the EF Securitization Facility and for working capital. The debtors seek $100mm on an interim basis. Fees include (i) a 1% exit fee, (ii) a 3% unused commitment fee, (iii) a 1% maturity extension fee, and (iv) other fees that total approximately $6.4mm. The outside maturity date is July 1, 2025 with a 90-day extension built in (subject to the 1% maturity extension fee) so … uh … yeah … these guys seem to think that some of the issues with the Chilean government will take some time to sort out and seemingly plan to hibernate under US bankruptcy protection for a while. This is not something you see everyday:

In addition to Rothschild as investment banker, the debtors are represented by an army of lawyers at White & Case LLP (John Cunningham, Richard Kebrdle, Philip Abelson, Samuel Hershey, Andrew Zatz, Andrea Amulic, Lilian Marques, Claire Tuffey, Peter Strom, Doah Kim) and Richards Layton & Finger PA (John Knight, Amanda Steele, Brendan Schlauch) and Riveron Consulting LLC (Robert Wagstaff) as financial advisor. JPM is represented by Latham & Watkins LLP (James Ktsanes, Andrew Sorkin, Jeffrey Mispagel, Amy Quartarolo) and Potter Anderson & Corroon LLP (Jeremy Ryan, Brett Haywood) while an ad hoc group of WOM bondholders is represented by Dechert LLP (Allan Brilliant, Stephen Wolpert, Isaac Stevens) as legal counsel and Ducera Partners LLC as investment banker.

The debtors’ first day hearing is later today, April 2, 2024 at 11am ET.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥. We’ve added, “The Credit Investor's Handbook: Leveraged Loans, High Yield Bonds, and Distressed Debt,” by Michael Gatto and have high hopes for its arrival.

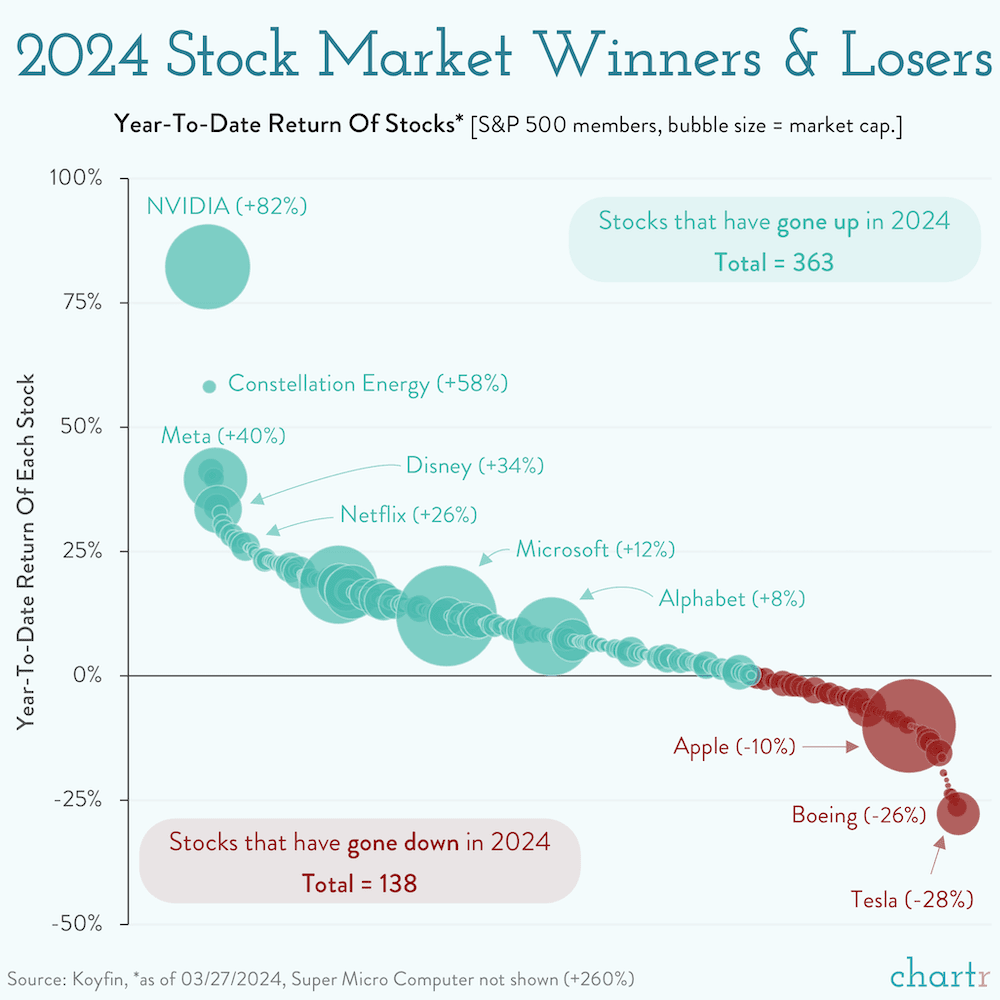

The equity market absolutely crushed in Q1’24. The S&P 500 closed Q1’24 with its 22nd record close of the year at 5,254.35, an all-time high. The Dow Jones Industrial Average also closed at a record high of 39,807.37. For the quarter, the S&P 500 gained 10.56% inclusive of dividends, the best Q1 since ‘19. And the rally was broad. Every sector other than REITs was up for the quarter and there were some clear winners (cough, everything AI!)…

…and some clear losers, including a number of companies in the electric vehicle space (as we discussed at length here). Believe it or not, Tesla Inc. ($TSLA) was the worst performing stock in the entire S&P 500, shedding ~$240b in market cap. This is a brutal chart:

We can only imagine what the chart looks like for privately-held (by Musk), X. Fidelity can’t seem to cute the value of its stake in X fast enough!

One notable point about the equity rally? Insiders appear to be running for the hills.

According to the petition, Softbank owns a 21% interest in the debtor, ranking second to Oak Investment Partners’ 43%.

The RSA authorizes the debtors to pursue a post-petition sale and marketing process subject to the consent of the debtors’ required consenting senior secured creditors. Any sale proposal must come in by April 26, 2024 and must cover all or substantially all of the debtors’ assets and include enough cash to satisfy the DIP and senior secured claims and leave subordinated creditors, equity and GUCs better off than they’d be under the proposed plan. It would need to close by the end of May. So, yeah, this is very unlikely to happen.

The equity backstop premium is 10% of $20mm, payable as new money common equity. Price per share is based on $86mm EV.

To add insult to injury, there are various creditors in Chile who are moving for “forced liquidation proceedings” against the company. Per the debtors first day declaration:

Chilean law permits any creditor to seek a forced liquidation proceeding against the Company if the company has failed to comply with its obligations to that creditor and the creditor has an “executive document” that evidences this obligation for the Chilean court. For example, overdue invoices can be converted to “executive documents” that allow the Company’s creditor to initiate an executive proceeding against the company and request liquidation to the Chilean court following a short ancillary proceeding that usually takes only a few weeks. Furthermore, if there are more than two ongoing executive proceedings (juicios ejecutivos) against the Company, at any given time, any creditor of the Company can request a forced liquidation, even those who do not hold executive documents.

As of the date hereof, certain of the Company’s Chilean unpaid creditors have initiated at least six ongoing executive proceedings and made at least two attempts to force the Debtors into liquidation proceedings in Chile. The Company was able to negotiate and consensually resolve such proceedings from moving forward, but the threat remains and the number of such actions against the Company may grow in the near term if the Company’s liquidity position is not immediately stabilized.