💥Special Double Edition: Where's the Auto Distress?💥

EV Adoption Slows. Charge, Lordstown, Proterra, and Fisker.

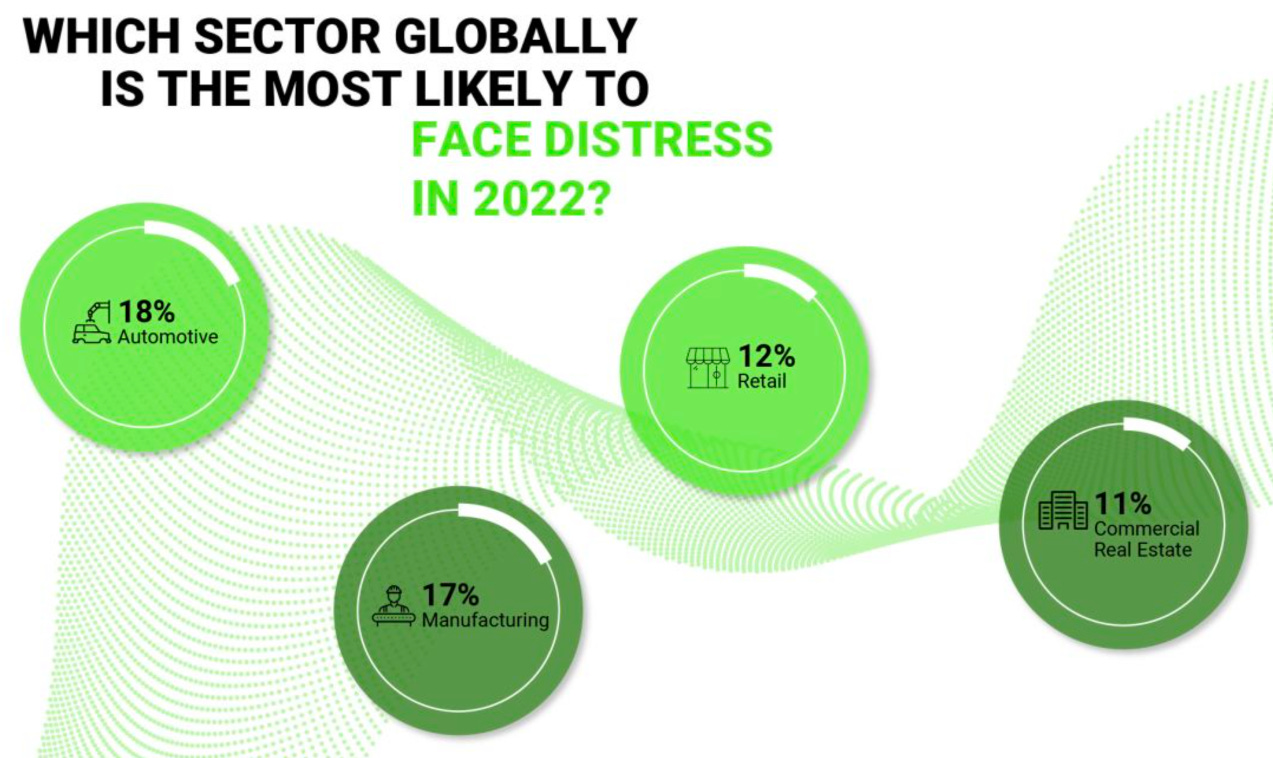

Callback to AlixPartners LLP’s 17th Annual Turnaround and Transformation Survey circa 2022 in which “…more than 600 of the world’s leading restructuring experts — the professionals most experienced in responding to the downside of economic volatility…” were asked “…how they view the current climate.” Therein, respondents singled out the automotive industry as the global sector most likely to face distress in 2022.

Jim Mesterharm, Alix’s Global Co-Head of Turnaround & Restructuring Services wrote:

In automotive specifically, I see two critical issues. Firstly, the ongoing conflict and pandemic have had an extreme regional and global impact on this industry’s supply chains, such as access to wiring harnesses and other vital raw materials. We also see the enduring impact of chip shortages, which is really impacting auto production globally.

Secondly, the longer-term challenges of electrification will continue to create huge disruption, driven by broader environmental concerns and a concerted shift towards hybrid and full electrification resulting from governments' push for higher fuel efficiency and lower emissions. The big question will be when will we reach that tipping point – the true moment of convergence – when more battery electric and fuel cell electric vehicles are sold than internal combustion or hybrid? Along the way there also will be challenges with new technology upstarts trying to enter the market and scale to production, and a shakeout down the road of legacy suppliers in the internal combustion engine space as demand decreases for their products.

By the time Alix published its 18th Annual Turnaround and Transformation Survey in the summer of ‘23 (featuring the views of now-700 people), one conclusion was that “industry distress shifts focus,” with commercial real estate coming in first as the standout industry to face distress in ‘23 — ranked first by 34% of respondents, more than double that of the second industry, retail, and triple that of the third industry, financial services. So what happened to all of that feared automotive distress? Per Alix:

“Automotive distress was significantly signaled by German (23%) and Italian (20%) respondents, failing to register as highly in other regions.”

Indeed, Mr. Mesterharm, despite a full page “perspective,” doesn’t even mention the automotive industry in the ‘23 edition. That's likely because, in the Americas, it came in fifth place behind the three aforementioned hot spots and consumer goods.

Fast forward to today and note how the automotive industry has been fairly quiet as far as bankruptcy activity goes. The narrative has continued to shift. To the extent there is distress, it’s less in traditional pockets of the auto sector and, ironically, more in the EV space. And that may only get worse.

Consider some of the recent earnings, news and commentary: