💥Another Failed Liability Management Exercise. Part III (Serta Simmons).💥

Tupperware Brands Corporation ($TUP), PLx Pharma Inc. ($PLXP), Nielsen & Bainbridge LLC, AmeriMark, Cano Health ($CANO) & More.

As some of you may have heard, there was a ruling in the Serta Simmons Bedding case (filing coverage here, subsequent pre-ruling coverage here). Before we dive in, we want to take a moment to talk about the financial stakes here.

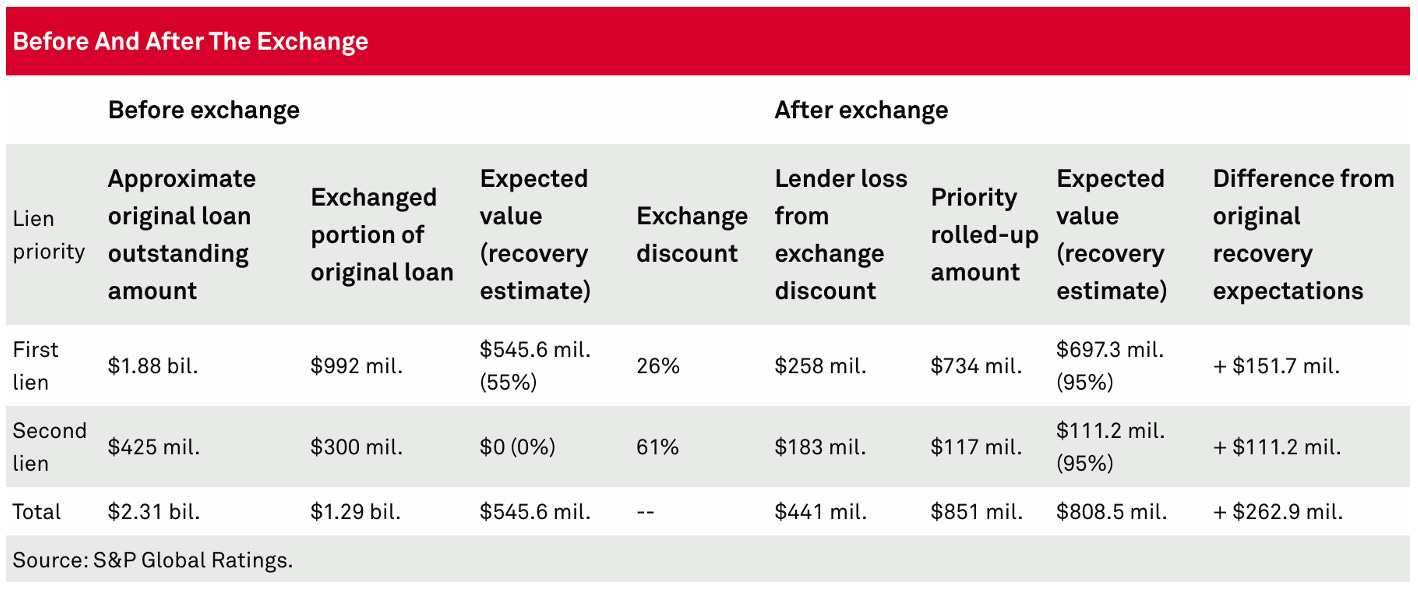

We used this ⬇️ S&P Global Ratings chart in prior coverage to indicate the economics of the exchange:

We should note, out of the gate, that the reflected discounts (to par value) still appear to price the debt well above the pre-transaction secondary market value, which the non-participating lenders peg at ~43c for the 1L and 8c for the 2Ls. The value of the non-exchanged 1Ls apparently fell to approximately 31c on news of the uptier exchange which, based on the above figures, shakes out to an approximately $105mm immediate loss for the non-participating lenders.

It only got worse from there.

The debtors’ disclosure statement, approved a few weeks ago, projects a 73.7% base recovery for the first-lien, second out (“FLSO,” which is the exchanged debt)1 versus a 2.4% recovery for non-participating lender claims, subject to a death trap that reduces recovery to 1% in the event of a ‘no’ vote. Using some napkin-math, we can estimate an approximately 43% blended recovery when collapsing the FLSO and non-participating debt (after applying the 26% first lien exchange discount), representing an approximately $265mm loss for the non-participating lenders compared against their potential recovery had the debtors used a pro-rata exchange offer with full participation.2 😬

Not following why this is worth highlighting? Unclear why this is such a big deal?

Let’s put it plainly:

‘Liability management transactions,’ despite their benign branding, are devastating blows for the folks who get left behind.

*****

Against that backdrop, let’s talk about the ruling. The big news: Judge Jones (i) found that the “open market purchase” language in the credit doc was unambiguous and (ii) allowed Serta’s uptier transaction.