💥More Rite Aid Drama!💥

💥More Rite Aid Drama!💥

Plus: Basic Fun is about to find out how horrible and un-fun bankruptcy is.

Goddamn it.

Every time we think we’re close to being done with Rite Aid Corp, it just keeps rearing its ugly head. We literally covered its confirmation a week ago…*

… but once again there are issues.

And not even particularly original issues.

Remember MedImpact Healthcare Systems Inc. (“MedImpact”)? It’s back! We last discussed these guys two weeks ago in the run up to the confirmation hearing:

MedImpact disputed ~$225mm of assumed liabilities associated with the debtors’ Elixir sale. The debtors thought MedImpact’s position was ridiculous and Judge Kaplan agreed. During a June 24, 2024 hearing, Judge Kaplan ordered MedImpact to perform under the original asset purchase agreement and sale order.

By the time of the confirmation hearing on June 27, 2024, MedImpact had already appealed in district court, and, apparently, also refused to actually perform and pay a liability due to McKesson Corp ($MCK).**

So the debtors, obviously a bit concerned at the lack of cooperation, filed a motion seeking an order holding MedImpact in civil contempt. LOL!

Per the motion:

“MedImpact has not complied with the Sale Order or Enforcement Order. On July 1 and July 3, the Debtors specifically gave MedImpact two chances to confirm that MedImpact will pay one of the six Disputed Liability Types that were teed up in the First Motion to Enforce: the $35 million “McKesson Liabilities” that have been due since Closing and that MedImpact must satisfy for the now confirmed Plan to go effective.” (emphasis added)

But MedImpact apparently indicated to the debtors that they had “no information on the composition of this alleged liability to McKesson.” MedImpact be like “compel”…

The debtors aren’t buying it. In fact, they highlighted how (i) during the previous dispute, one of MedImpact’s witnesses mentioned the liability, (ii) the liability is on the closing working capital list verified by MedImpact, (iii) the invoice is on Elixir’s subledger which MedImpact controls, and (iv) the individual invoices were listed in a file that MedImpact sent to the debtors back in May. In other words, per the debtors:

“MedImpact knows exactly what the McKesson Liabilities are, why they must be paid, how much must be paid, and when they were due to be paid by MedImpact.”

“MedImpact had its day in Court and lost. MedImpact’s continued play for self-help must end. MedImpact is slow walking payment—perhaps in an effort to use the Debtors’ tight liquidity situation to try to renegotiate aspects of the Court’s orders. But anything short of full compliance is unacceptable to the Debtors and a disservice to their customers, creditors, and employees. MedImpact knows full well the import of its actions and who will be harmed by them.”

After all the debtors have gone through in this case, they’ve got to be feeling like this:

We know we are. And we reckon Judge Kaplan is too. Something tells us this won’t bode well for MedImpact.

A hearing is set for July 29, 2024 at 11am ET.

*You can refer to our other prior RAD coverage here, here, here, here, here, and here.

**To be clear there also hasn’t been any proposed stay pending appeal from MedImpact.

💥New Chapter 11 Bankruptcy - Basic Fun Inc.💥

Damn it! Can’t we at least have our f*cking toys!!

On June 28, 2024, FL-based Basic Fun Inc. (“Basic Fun”) and four affiliates (collectively, the “debtors” or the “company”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Goldblatt). The debtors are purveyors of fun — a “global children’s entertainment company,” founded in 2009 by Jay Foreman.

Jay’s got a passion for toys and a penchant for horrible TikToks like this ⬇️ one:

“Meet Frank”… the CFO of a toy company … really, guys?!? With “content” like this, it’s no wonder you’re bankrupt. (The post got 26 “likes,” lol).

Since ‘13, Jay has been busy rolling up toy brands. “Well-known, steady” toys please, the better to build a “consistent profit base,” according to the first-day declaration of … wait for it … CFO Frank!* At least eight toybox-stuffing transactions since ‘13, including M&A, 363 purchases and licensing deals.** And why not? Tots are always going to love Lincoln Logs. And Tonka Trucks. Tinker Toys! Care Bears! Lite-Brite! With all new templates! My Little Pony! Johnny’s aged grandpa remembers them all: back in the day, he says, before you kids with your smartphones, “fun” was lobbing firecrackers at Lincoln Log cities and reveling in the conflagration. Is there any asset more capable of delivering annuity-like cash flows than hoary toys for nostalgic boomers? 🙄

Much to our surprise, apparently nostalgia — the success of the Barbie movie notwithstanding — isn’t a guarantee of business success. Per our boy Frank-of-26-Likes:

“Despite the Company’s successful acquisition of many major toy companies and products over 10 years, in fiscal year 2023, the Company recognized total net sales of approximately $144.1 million, representing a decrease of $15.3 million, or 9.6%, compared to fiscal year 2022.” (emphasis added)

How do we define success these days, 🤔? Sales only down 9.6%, 🤔? So Time Warner’s buyout of America Online was a successful exercise of sound business judgment?

To be fair, the debtors suffered from more than their share of exogenous hits. The Toys R Us (“TRU”) bankruptcy, for instance: TRU was the debtors’ largest customer, with some $35mm of annual sales. TRU’s chapter 11 filing and liquidation left the debtors with $6mm in uncollected receivables; they also faced “struggles” to shift the TRU volume to Amazon Inc. ($AMZN). Hmmm, maybe they should have partnered with Thrasio Holdings LLC, 😜?

And, of course, Covid-19. Demand from stay-at-homes surged, but the good news was shot through with shards of awfulness. As “a result of a shortage in container boxes and ships, the goods being produced were not being shipped on time to meet demand.” And when they were shipped, costs were some seven to ten times higher than before. At the same time, amusement parks were shuttered by social distancing mandates; the debtors’ amusement division lost $10mm in sales in ‘20. But when the restrictions lifted, consumers fat with stimulus money decided to blow it on (other) “experiences” like travel and dining. This came as the supply chain issues were resolved; suddenly the debtors were loaded with excess inventory, meaning margin-busting markdowns and persistently inflated shipping costs.

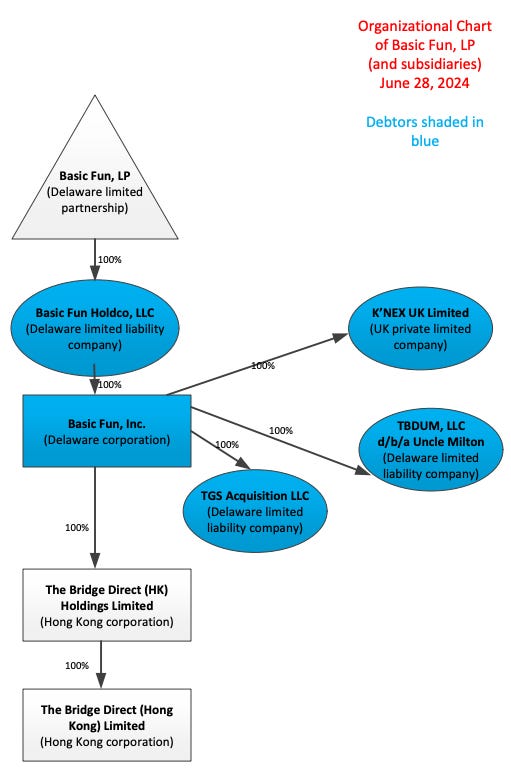

You’ve heard variations on this for quite some time, have you not? All excruciatingly, painfully familiar, is it not? Bid it farewell as we venture into the unknown of the debtors’ capital structure. First, Frank whipped up this nifty org chart:***

BF GP Inc., a Delaware corporation, is the general partner of Basic Fun LP, the non-debtor parent. Our boy Jay owns 100% of BF GP Inc. The debt sits below.

Let’s get into that debt shall we? Don’t let those TikToks fool you: we reckon that Frank was thinking “why the f*ck am I making TikToks, Jay, when I’ve got a bunch of liabilities on balance sheet to contend with?” A fair sentiment, we think.

On Aug. 3, 2017, the debtors obtained $40mm in senior secured loans, $15mm in mezzanine debt and access to a $20mm accordion via Royal Bank of Canada (“RBC”) as part of the debtors’ acquisition of Tech 4 Kids. The mezzanine facility has a PIK component. Frank-of-26-likes-and-tens-of-millions-of-debt dubs these the “Initial Loans.” In December of that year, the senior lenders advanced $5mm through the accordion to support the debtors’ acquisition of K’Nex; the advance was matched by a former investor in K’Nex, CCNAS Investment Holdings, Jay and John MacDonald, a member of the board and presumably Jay’s buddy.

“Growth” on their minds, meaning new acquisitions, the company sought a private equity partner to “invest in the business.” Jay engaged BMO Capital Markets to assist. “Though there were initially several interested parties, due to factors including the Toys R Us Bankruptcy . . . only one party, Falcon Structured Equity Partners, LP (“Falcon”), committed to an investment that the Non-Debtor Parent and its existing equity holders deemed to be acceptable.” Falcon invested $40mm, for which it got 400k units of 10% Series C Preferred Partnership Interests and 178,533.48 Class A-4 Limited Partnership Interests, which together represent 14% of the “common equity” of the non-debtor parent.

And what did the company do with that $40mm? Well, they first loaned the debtors $10mm on a subordinated basis. As for the rest, well, there was that $5mm match to contend with:

The Non-Debtor Parent had borrowed the $5,000,000 from Messrs. Foreman and MacDonald pursuant to notes issued by Non-Debtor Parent, which notes to Messrs. Foreman and MacDonald were repaid by Non-Debtor Parent from the proceeds of the Falcon Investment. The K’Nex Note is subordinated in payment to all of the current and past secured debt obligations of the Company.

But why stop there:

The remainder of the $40,000,000 equity investment repaid Foreman and MacDonald and a former unit holder $17,000,000 for his 26% interest in the company, senior employee distributions and transaction fees.

A lot ended up with our boy Jay and his boy MacDonald, unless we misread it somehow. “The anticipated benefits of a business partner with $3 billion of assets to deploy to grow the Company have not materialized,” Frank says. Oh? “Letters of intent requiring equity were not available and additional equity contributions from Foreman and MacDonald could not be invested with priority to the Falcon Investment.” Huh? Bit of a head-scratcher, but per Frank, there hasn’t been much on the M&A front since ‘18 due to the constraints the Falcon capital put on the company.

By ‘19, events spiraled somewhat out of the company’s control. RBC, rattled by the TRU bankruptcy and the pandemic, took a look at the Sept. ’20 maturity of that two-year old $20mm senior secured term and told the company that there was absolutely no way it would extend one second longer. “RBC moved the account to their Special Loan’s Group and hired A&M to monitor cashflow and report on the company’s performance. A Term Sheet negotiated with PNC was ultimately withdrawn as a result of Covid-19 impact uncertainty.” Certainly not an ideal time to hit the debt capital markets, but capital availability is often a function of price and so in marched Crystal Financial, d/b/a SLR Credit Solutions (“SLR”) with what Frank-of-26-likes-and-26-private-credit-battle-scars refers to, somewhat ominously, as The 2020 Refinancing Transaction.

SLR provided a $20mm revolver, subject to a traditional ABL borrowing base, and a $20mm term loan. RBC got some relief. As of the petition date, the debtors owed “not less than $20,000,000” to SLR with respect to the term loan, and $326,164.74 on the revolver.

RBC still had mezzanine piece. On July 15, 2020, RBC loaned the company another $2.5mm from the facility. Our boy Jay and his boy MacDonald promptly purchased “100% participation interest in RBC’s right, title and interest” in and to that loan (MacMahon calls it the “First Out Loan”). And if that’s not enough, on Oct. 20 of the same year, the mezz lenders advanced another $2.5mm to the company. Frank says it’s been repaid in full. Outstanding principal on the mezzanine piece is “not less than $[16,436,335.00]” as of the petition date.

Our boy Jay and his boy McDonald themselves loaned the company a total of $18mm in ’19. Frank says that the company “needed liquidity” as it was in talks with a jumpy RBC “to obtain forbearance from certain defaults pursuant to the 2017 RBC Senior Credit Agreement and the 2017 Mezzanine Credit Agreement.” (We’ll get to that.)

What’s left? $900k owed to shippers and warehousemen**** and $11.6mm in unsecured obligations to suppliers, vendors and the like. In terms of other major obligations, the debtors have their HQ lease in Boca, their storage lease in Boca, and showrooms in LA and Hong Kong.

The 2020 Refinancing Transaction with SLR bought some time. But in Oct. ’23, trailing twelve-month financials fell below levels required by the SLR facility. The company’s forecasts for ’24 looked worse. In December ’23, Frank-of-26-likes-and-26-sh*t-bricks-in-his-pants says, the “default” under the 2020 credit agreement with SLR caused “(i) the Company to accrue contractual fees and default interest to SLR, (ii) the amortization under the First Out Loans to end after only one month, and (iii) interest payments to RBC to end, resulting in a PIK 18% rate.”

These credit agreement defaults were still outstanding in June ’24. SLR chose not to exercise its right to implement cash dominion over the company’s accounts. However, the springing covenant clause meant that the facility matured on July 2 or 90 days prior to the Sept. 30 maturity of the mezz piece. The company asked for a revolver advance. Nope, SLR said. The company “…voluntarily complied with SLR’s request to transfer daily receipts to SLR’s collection account, with funds being re-advanced to the Company upon request.”

Back to the mezz piece. The company is in a covenant-based default. And, because we know Frank like we do (thanks TikTok!), we reckon he found RBC relentlessly annoying:

“As a condition to renewing the mezzanine loans, RBC signaled its desire to see (i) the Company’s access to capital to support operations, including through an acquisition strategy as a means to grow EBITDA, and (ii) re- alignment of management and equity interests in order to ensure that management was properly incentivized, and their interests were aligned with those of the Company.”

So RBC hadn’t thought to bring sort of thing up before? Then there’s this odd nugget:

In April 2024, the Company’s CFO and John MacDonald, the Chair of the Debtors’ governing boards (the “Boards”), held rounds of discussion with SLR, RBC, and Falcon. Following multiple calls with RBC and Falcon, the Company received a response from Falcon that did not adequately provide for access to capital or management alignment. RBC recommended that the Company retain an investment banker to provide valuation and strategic assistance in moving past the impasse with SLR, RBC, and Falcon.

The company says it urgently needs “liquidity” to “begin making acquisitions as a path to growing EBITDA.” SLR and RBC seem to be taking a dim view of the company’s ability to do that very thing. Who loses money on Lincoln Logs? At any rate, the company retained Oppenheimer & Co. (“Oppenheimer”) as investment banker; Oppenheimer presented two options and in June the company chose Great Rock Capital Partners (“Great Rock”). Great Rock sent its people to Florida and “commenced its borrowing base audit. At the same time, Oppenheimer had further conversations with RBC, SLR, and Falcon … Also in June 2024, SLR tightened oversight over the Company. Disbursements were strictly limited to deposits which is constraining during June, a busy month in the cycle of a toy company.”

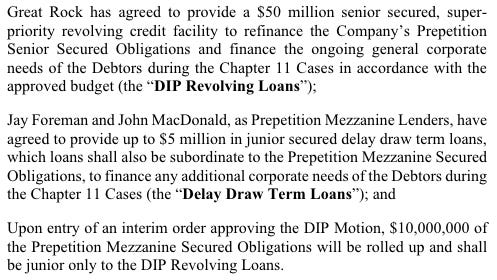

June may be busy, but July will be memorable. At the first day hearing on July 2, 2024, the debtors’ motions were approved on an interim basis, including a $22.5mm out of a proposed $50mm DIP RCF from Great Rock. Judge Goldblatt also approved a $10mm DIP term facility as a roll-up of RBC’s mezz piece and a $5mm junior secured delay draw term loan from our boy Jay and his boy John. The RBC roll-up was a requirement to priming. SLR’s debt remains senior to RBC until paid off (which is contemplated).

The first day hearing was surprisingly congenial (and short, clocking in just over an hour), given the intimations of strife in the filings. Mark Joachim of Polsinelli PC, counsel for the debtors, stated that the parties to the cases, including RBC, SLR and Falcon, have worked “feverishly” to come to an agreement on a “fully consensual debt financing,” but a “restructuring of the overall capital structure” is still in process as the parties put “the finishing touches” on. But an “agreement in principle” is close!

For its part, Falcon, noting that the company is founder-owned and subject to “corporate darkness,” insisted on the appointment of a “mutually acceptable” independent director familiar with restructuring. There may yet be some drama!

The debtors are represented by the aforementioned Polsinelli (Shanti Katona, Mark Joachim, Caryn Wang, Tanya Behnam, Michael Schuster) as counsel — part of a nice string of cases including ProSomnus Inc. and Delta Apparel Inc. — and Oppenheimer as financial advisor (Bruce Buchanan, Matthew Haasch, Geoffrey Weiss, Isaac Weinstock). RBC is represented by Orrick, Herrington & Sutcliffe LLP (Raniero D’Aversa, Nicholas Sabatino) and Klehr Harrison Harvey Branzburg LLP (Domenic Pacitti, Richard Beck, Sally Veghte), SLR by Morgan Lewis & Bockius LLP (Christopher Carter, Sandra Vrejan, David Shim, Jody Barillare), Falcon by Paul Weiss Rifkind Wharton & Garrison LLP (Paul Basta, Sean Mitchell, Paul Paterson, Nicholas Krislov) and Landis Rath & Cobb LLP (Richard Cobb, Joshua Brooks), and Great Rock by Paul Hastings LLP (Justin Rawlins, Matthew Friedrick, Xue Yu, Jennifer Hildebrandt) and Young Conaway Stargatt & Taylor LLP (Edmon Morton, Matthew Lunn).

*One name only for this legendary CFO. Okay, fine, McMahon is his last name.

**The company owns a variety of brands (e.g., K’nex, Mash’ems, Misfittens, Cutetitos, Playhut, and Uncle Milton) acquired over the aforementioned 10-year acquisition bonanza and licenses others (e.g., “iconic brands” like Care Bears, Lite Brite, Tonka, Nintendo Amusement, Lincoln Logs, and My Little Pony Retro), the latter making up ~70% of the company’s revenue. The debtors sell their toys in places like Target Inc. ($TGT), Walmart Inc. ($WMT), Macy’s Inc. ($M), Costco Inc. ($COST), online on Amazon Inc. ($AMZN), and at amusement parks.

***What? No “making of” vid on TikTok, guys, c’mon?

****Half of which may be taken care of via the interim order authorizing the debtors to pay prepetition claims of shippers, et al.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.