Happy Sunday, y’all! Let’s get you warmed up with some distressing numbers for those focused on distressed.

As of the end of February, despite the Fed funds rate sticking “higher for longer,” there was only ~$76.8b of distressed loans (trading at or below 80c). This represents a ⬇️ of nearly $7b from January and a $37b ⬇️ from just three months ago. Repeat: a $37b dip from just three months ago. The pool of distressed loans hasn’t been this shallow in a year and a half. Take the rest of the year off, folks! 😜

Source: GIPHY

For the lawyers among you whose eyes roll into the back of your heads when you see numbers, we’ll give you some context. The amount of stressed/distressed loans was $140b at the end of ‘22 and $323b at the height of the pandemic in March ‘20. As things stand currently, the pool of loans is set to dip below the $67b mark from just before the pandemic in February ‘20.

But at least things are dicier in the high yield bond world, right?

Nope.

As of the end of February, the universe of distressed bonds fell by $6.6b to $80.5b, a nearly two year low. Juxtapose this against $149b in June ‘22 and … wait for it … $418b in March ‘20 and, well, things sure are looking bright for golf season.

Source: GIPHY.

*****

Unless you’re down in Texas. Sh*t looks bleak AF down there.

Particularly if you’re Jackson Walker LLP.

Source: PETITION Meme Department

The Office of the United States Trustee (“UST”) is on a crusade and recently moved to vacate orders that approved Jackson Walker’s retentions and fees (clawbacks!) in a whole menu of cases and added a request for sanctions as the cherry on top. Why? Do we really need to ask? Ok, fine, we’ll answer our own question. There was a Judge down there who made a habit of napalming, from the high ground of his high horse, a number of restructuring professionals for all manner of sins — most small and blown out of proportion and one (arguably) large — in the name of protecting “the integrity of the bankruptcy system,” 😂, only to then blow himself up by engaging in a (consensual) relationship with a local practicing attorney (and former Jackson Walker partner) and committing the most egregious of unforced errors, i.e., failing to disclose the potential conflict of interest during, among other occasions, the times when Jackson Walker was before him or the times when his “partner” had fee requests before him when disclosure is one of the hallmarks of “the integrity of the bankruptcy system.” He’s now off the bench, a formerly-retired Judge had to come back to pick up the disgraced Judges’ full slate of existing cases (at least until a recently retired Weil partner joins his former colleague on the “complex panel”…? 🤔), and new cases are now filing left and right in Delaware or in New Jersey rather than Texas, much to the chagrin of everyone who worked so hard to manufacture Texas jurisdiction into a “thing.” Jackson Walker is trying to deflect arguments that it, too, failed to make necessary disclosures about its former partner, especially during a period where it apparently “knew” of the relationship. This all obviously looks bad and Norton Rose & Fulbright LLP is in the trenches defending Jackson Walker — there are some more buses on sale, guys, that you can use to throw said former Jackson Walker partner under — even though, ironically, it might actually be to Norton Rose’s benefit to see Jackson Walker go down in the flamiest way imaginable (we see a lot of local counsel gigs in your future, guys!). We’re eager to see how this plays out. We are reminded, however, that, once upon a time, the UST made a big stink in the Northeast about certain claims and noticing agents failing to disclose that they had entered into exclusive data sharing agreements with a certain tech company angling to facilitate e-trading of general unsecured claims via a new tech platform. The whole industry was on the edge of their seats waiting to see how that would play out. We admit: we had a ton of fun with it at the time (Littlefinger!), but, in the end, it turned out to be a giant nothingburger (with the largest fine being $500k, a drop in the bucket for a company supposedly worth $3b). Will this war march end with anticlimax too? We can’t wait to find out.

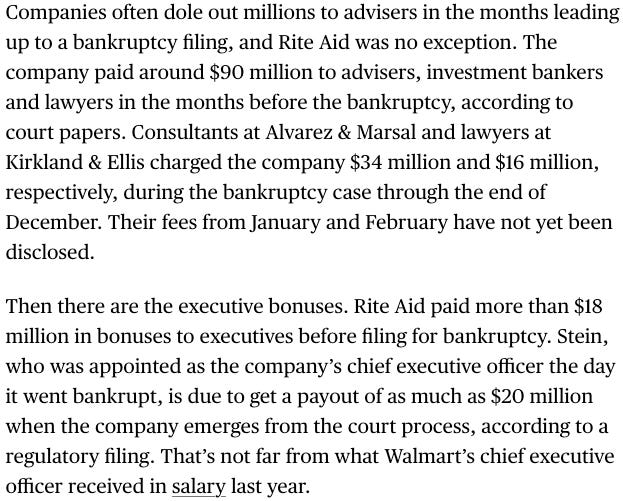

⚡️Update: Rite Aid Corporation⚡️

Source: PETITION Meme Department

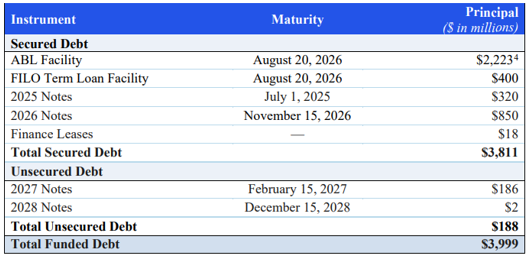

Rite-Aid Corporation and 119 affiliates (the “debtors”) filed their chapter 11 bankruptcy cases in the District of New Jersey (Judge Kaplan) way back on October 15, 2023. In our initial post-petition coverage, we noted the laundry list of reasons for the debtors’ collapse — chief among them, an over-levered capital structure featuring $3.8b of total secured debt. Here’s what that looked like:

Source: FDD

You’ll recall that the debtors rolled up $3.25b of debt and obtained access to $200mm of new money in connection with their DIP facility. You’ll also recall that the debtors sold their PBM business, Elixir, to stalking horse bidder, MedImpact Healthcare Systems Inc., placing the focus for the rest of the cases on the debtors’ retail business. And, there was no question about it, the Ad Hoc Secured Noteholder Group has been very focused on that business. In our initial coverage*…

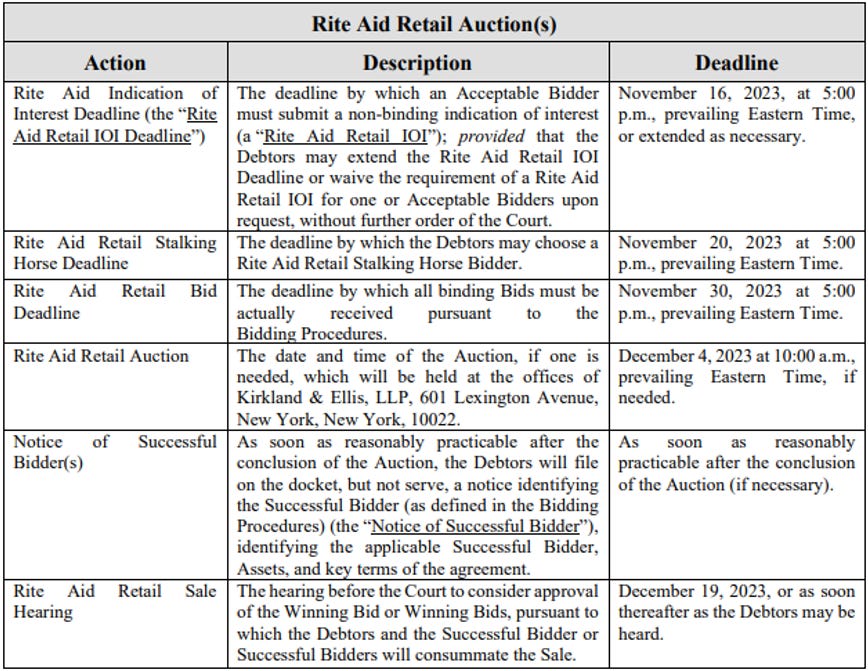

For its part, the Ad Hoc Secured Noteholder Group (which makes up 66.7% of the aggregate principal amount of secured notes outstanding) has agreed in an as-of-yet-unfiled RSA to either exchange their debt in exchange for equity in the reorganized Rite-Aid or, if certain confirmation milestones aren’t satisfied, support a 363 alternative for the debtors’ retail business that would feature either a third-party bid or a credit bid by the Ad Hoc Secured Noteholder Group. The debtors swiftly moved to get bidding procedures approved at the first day hearing and succeeded — with the Ad Hoc Secured Noteholder Group indicating that the “timeline is critical” with so little cash available and a business that operates on an “economically thin margin.” The procedures included $11.5mm in break-up fees. The proposed sale timeline looks as follows:

Source: Docket 33

That “critical timeline” has been left in the dust. It turns out marketing a third-rate dilapidated pharmacy business while also contending with 2k+ stores (and rejecting leases for scores of them) and fending off two committees (yes, two, there’s also the Official Committee of Tort Claimants (“TCC”)) is quite a heavy lift.

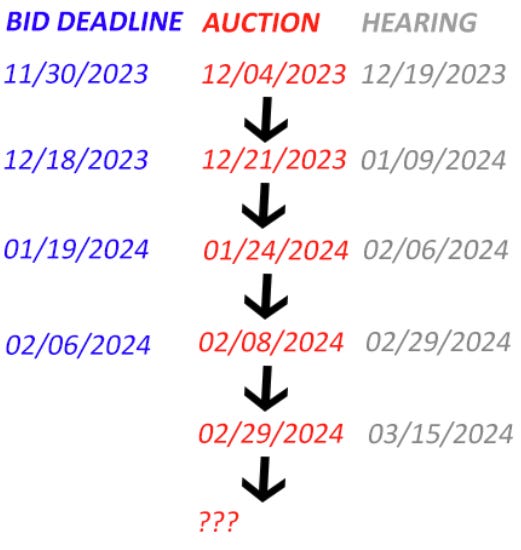

Unable to meet those original deadlines, an extension hit the docket on November 29, 2023 that moved the bid deadline to December 18, 2023, the auction to December 21, 2023, and the sale hearing to January 9, 2024. This extension happened after the second day hearing at which the committees were insistent on a more accommodating timeline. Per Arik Preis from Akin Gump Strauss Hauer & Feld LLP on behalf of the TCC during that second day hearing:

“We have concerns that [the processes] are being run in a fashion that predetermines the outcome. We are focused on the marketing process and making sure that the sale processes are not set up to fail in favor of the company's preferred re-org path … [w]e've provided the company with new timelines and proposals and we've seen the company already reject some of them.”

On the other hand, Mr. Preis also seemed acutely aware of the admin burn:

“I just want to point out that between dip financing fees, dip financing approved interest, debtor professionals and the CRO, the company is projected to pay about $400mm in a six to nine month case. That's without any fees or anything going to the committees and it's without any recovery to any unsecured creditors.”

We’re at month five and counting. 😳

As it turned out, the first extensions proved to be inadequate, and consequently, Judge Kaplan entered an amended bid procedures order on January 9, 2024 that further postponed the bid deadline to January 19, 2024, the auction to January 24, 2024, and the sale hearing to February 6, 2024.

And of course those dates came and went too.

Source: PETITION Meme Department

The debtors needed another extension on January 22, 2024 that moved the bid deadline to February 6, 2024, the auction to February 8, 2024, and the sale hearing to February 29, 2024.

Did these new dates work? No, of course not, otherwise we’d be covering an “announcement of successful bidder.”

Instead, the debtors rescheduled the auction to February 29, 2024 and the sale hearing to March 15, 2024 … only to file a notice of adjournment of the auction eight days later that adjourned the auction “to a date to be determined.”

Here’s a handy chart of all the delays:

Source: PETITION LLC

But wait, aren’t there milestones or something under the DIP?

Correct! But, don’t worry the DIP has already been amended twice to push the milestones out.

Source: GIPHY, the debtors trying to catch up to their milestones

“The Ad Hoc Secured Noteholder Group either supports or has no objection to the modifications reflected in the Amended Final DIP Order.”

This sale process has literally rendered the Ad Hoc Secured Noteholder Group speechless.

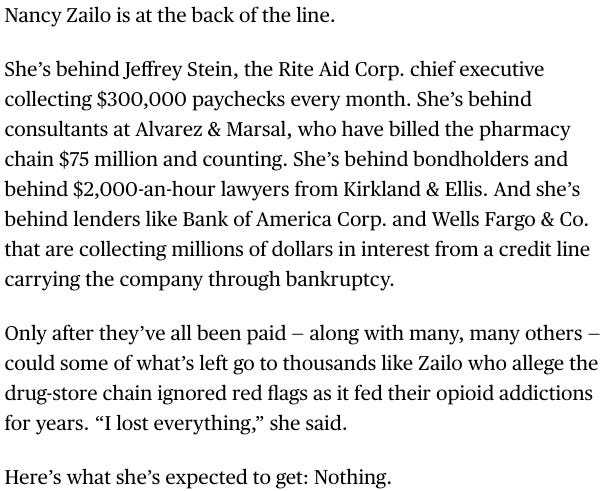

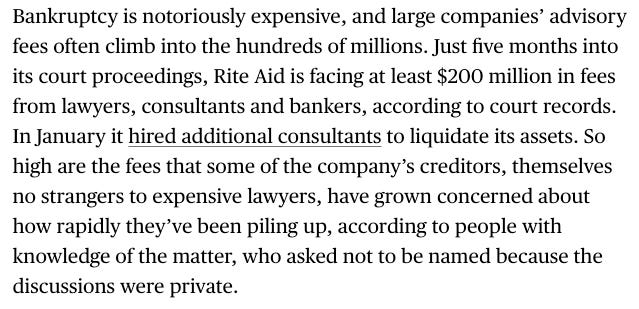

So what is going on here? What happened to Sullivan & Cromwell LLP’s potential mystery bidder? Has the sale process for the retail business completely stalled out? If so, is anybody — in addition to Mr. Preis (who we’re sure is all to happy to clip his fees) — concerned that a prolonged schedule will lead to astronomical admin costs (or is it just us)? Clearly yes. Here is Bloomberg:

Don’t worry tort claimants! There’s about to be a fee examiner who will scrutinize all of the professional fees and keep things under control (for $525/hour plus any fees incurred by professionals he needs to “discharge his duties”))! 🙄

All of which leaves us with some questions. Is the Ad Hoc Secured Noteholder Group spending considerable time in therapy addressing the fact that they may end up owning this fecal matter against their will (a dramatic misread by Mr. Preis at the onset of the cases)? What kind of negotiations are transpiring between the DIP lender banks and the Ad Hoc Secured Noteholder Group about the future of this melting ice cube?

From the outside looking in, it’s hard to tell for sure what the hell is going on here but we’re beginning to get, at best, the Ad-Hoc-Secured-Noteholder-Group-truly-doesn’t-want-these-assets vibes and, at worst, some Toys-R-Us-style-there’s-a-non-zero-chance-this-f*cker-liquidates-vibes, 🤷♀️. Might we be overly dramatic here? Perhaps. Though this sure seems … odd (if true):

Say what now?! Per ABC27 News:

Rite Aid suddenly withdrew biweekly severance payments it had already made to the accounts of laid-off employees Thursday, according to several employees who spoke with abc27 News and provided similar accounts of their experiences.

An e-mail message from the company to employees confirmed the sudden payment reversals weren’t an oversight. “We must now take another difficult action to further preserve cash in the short-term,” the message said. “This is necessary in order to best position Rite Aid to emerge from this process as a more financially stable company. As part of these cash-preservation efforts, severance payments due to be distributed on March 7 have been delayed. It remains our intention to make these payments to you. Given the fluid nature of the situation, we are not able to provide a definitive timeline for distribution at this time.”

Yet another timeline that’s FUBAR. Daaaaaaaamn that’s harsh. Damn…

Source: GIPHY

We can only imagine how hard Rite-Aid’s counsel, Kirkland & Ellis LLP — which already has Toys’ liquidation on its record — is pushing to keep this thing on track and avoid another major retail liquidation.

Source: PETITION Meme Department

We certainly hope this dumpster fire isn’t as dire as it seems.

We’ll find out soon enough.

*You can find our other post-petition coverage of the case here:

1. The Container Store Inc. ($TCS). The hits just keep on coming for Johnny’s favorite storage solutions retailer. S&P Global Ratingsslapped an issuer level and term loan level downgrade (both to B-) on the struggling company after it reported dogsh*t earnings.