💥Inflated💥

A top '24 theme persists going into '25.

The holidays were R.O.U.G.H. We can’t wait to join the gym because we definitely overindulged. Johnny’s waistline, in particular, is inflated as f************ck.

Which is appropriately on theme.

Amidst all kinds of external pressures — multiple geopolitical and geostrategic headwinds gathering worldwide (e.g., Ukraine/Russia, Israel/Hamas/Hezbollah/Houthis/Iraqi militias/Iran, Syria, France, Germany, Canada, etc.), and a new (and seemingly angry) administration set to take office in the United States (threatening a spectrum of competency on the proposed cabinet, aggressive tariffs and tax cuts, and … gulp … “retribution”) — Jerome POW-ell and his team are getting trembling knees.

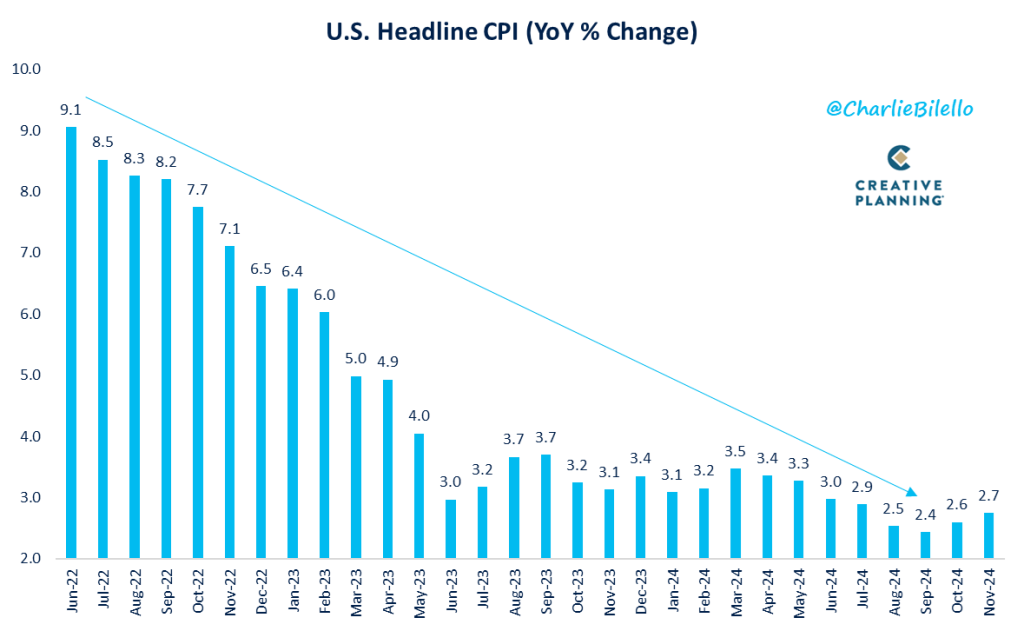

CPI moved up to 2.7% in November and the Cleveland Fed currently estimates that it will tick up further in December to 2.86%. This ⬇️ is NOT going in the right direction:

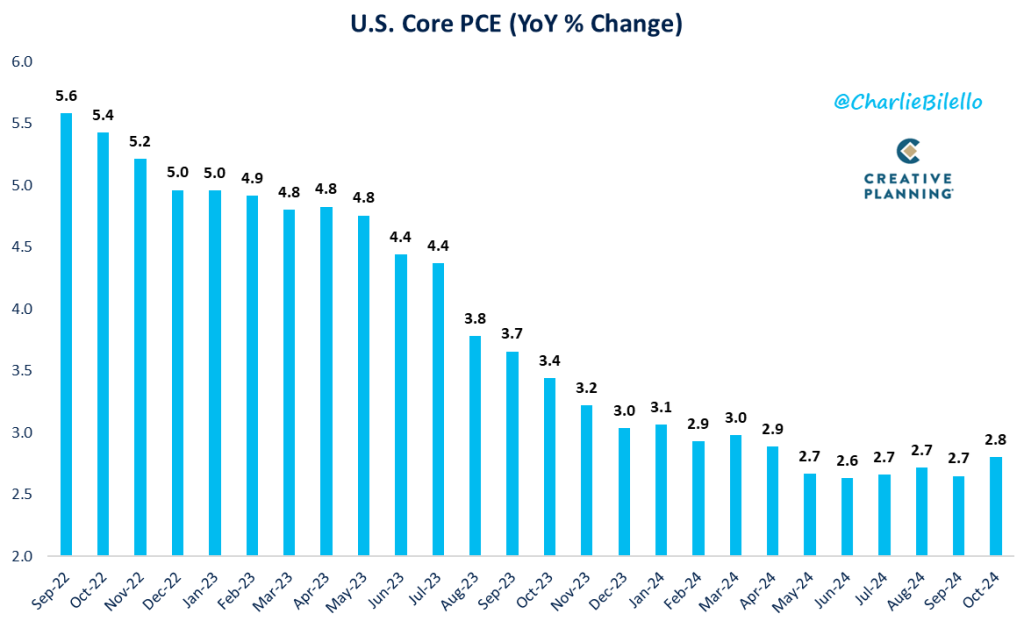

Of course, POW-ell & the Gang really only pay mind to its “preferred measure,” the Core PCE. Luckily that went dow … *checks notes* … uh oh … uh no … that moved up to 2.8% in October, a six month high:

Well, it was a six-month high until November core PCE came in a hair above October (up 0.11%, the 12-month rate held at 2.8%).

Despite these trends — not to mention the highest US Producer Price Index increase since February ‘23 — the Fed stayed on course and lowered the Fed funds rate by 25 bps right before the holiday break. In the process, however, it also ice bucket challenged the market with a hesitant (read: hawkish) take on future rate decreases. “We have lowered our policy rate by a full percentage point from its peak and our policy stance is now significantly less restrictive,” POW-ell said, adding, “We can therefore be more cautious as we consider further adjustments.”

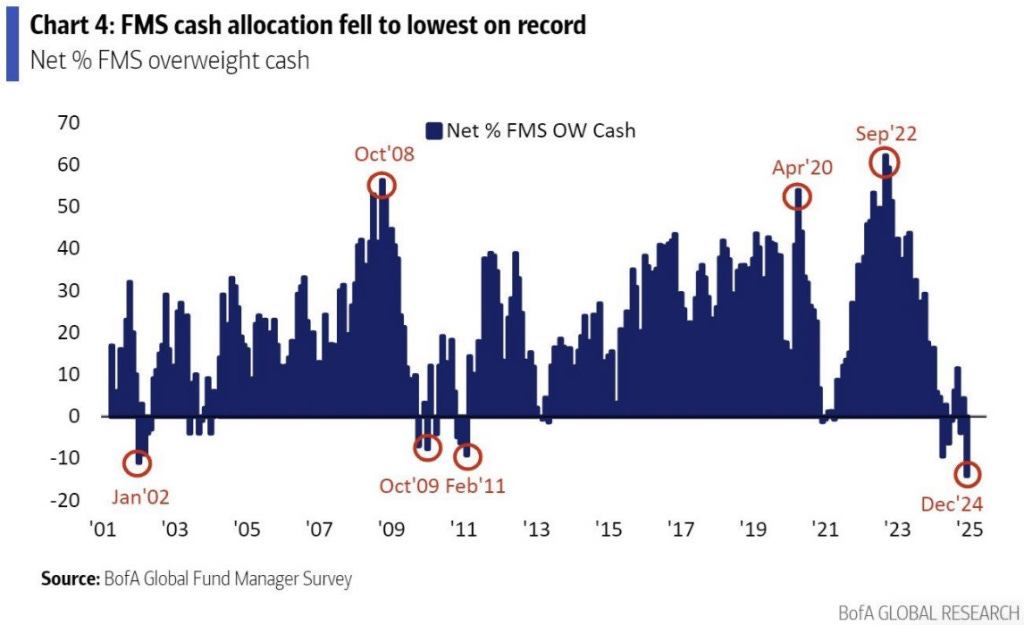

POW-ell likely already feels President Musk Trump 2.0 breathing down his neck. Tesla Inc. ($TSLA) stock is down 14.5% since the meeting. Fund managers had been chasing the rally with unbridled optimism; they’re 14% underweight cash according to BofA …

… which means there’s gonna be quite a lot of pain if the market corrects. The “smart money” investors have been buying into an S&P 500 that, as of Christmas, clocked in at a 26 P/E, a 30+% premium to the historical average. Multiple expansion baby! Risk on baby! President Musk Trump is already making people rich, lol!

Of course, nothing says “risk on” like the price of BTC. It, as of the time of this writing, is up 5% YTD (already, lol — but still off of the dramatic new highs reached on the day of the FOMC meeting).

Ok, fine, maybe high yield spreads say “risk on” just as effectively as BTC: investors stretched for most of ‘24 in what’s clearly been an issuer’s market.

Inflation, risk on, stretching for returns. These themes all apply to the restructuring world too.

First, inflation.

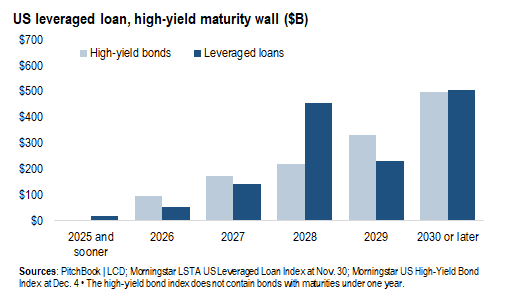

With the exception of the deflated near-term maturity wall …

… literally everything is inflated/up.

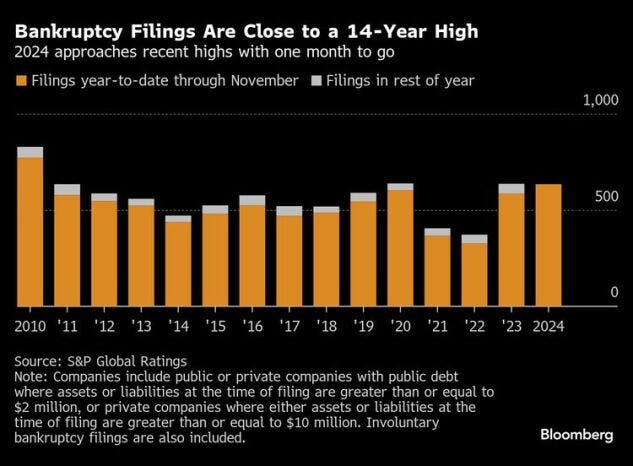

Case filings? Up, ✅. This is how things looked at the end of November:

And here is Epiq chiming in at year end:

“Commercial chapter 11 filings increased 20 percent in calendar year 2024 to 7,879 from 6,583 filings the previous year, according to data provided by Epiq AACER…. Overall commercial filings increased 17 percent to 30,009 from the 25,731 registered the previous year.”Liability management situations? Up, ✅ (though we’ll see what the recent Serta decision does on this front … commentary on that to come).

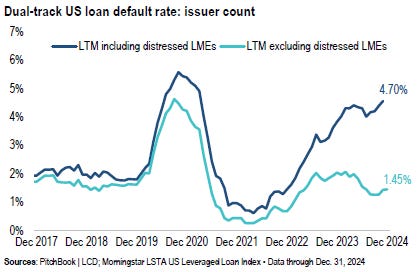

The default rate (mostly due to distressed exchanges)? Up, ✅. Here’s our fave leveraged loan chart reflecting the impact of LME:

“U.S. broadly syndicated loans (BSL) CLO portfolios have experienced 81 defaults year-to-date (YTD), the highest since the COVID-19 pandemic, compared to 96 in 2020. Of the YTD defaults, 65% were distressed debt exchanges (DDE) and/or restructurings.” Fitch, with its own default rate methodology, later added:

“Nine issuers across eight unique sectors defaulted on their leveraged loan (LL) debt in November 2024 bringing the LL default rate for the trailing twelve month (TTM) as of November 2024 to 5.2%, up from 4.7% in October. In the high-yield (HY) market, two additional issuers in different sectors defaulted, including Chapter 11 filings from Spirit Airiness and H-Food Holdings. The HY default rate for TTM November 2024 is 2.0%, up from 1.6% in October.”Billable rates? Up, ✅.

$2,675/hour. Repeat: $2,675/hour.

Really y’all?

And y’all wonder why liability management exercises have been all the rage? Who can afford actual bankruptcy these days? Or as one of our readers recently asked us:

"When does the market say no to exponentially increasing hourly rates? Why should a second year biglaw associate be charging more per hour than a senior suburban lawyer with forty years of experience? Why is anyone entitled to charge $2600/hour, other than maybe the Wizard of Oz?"Expect it to get worse.

We recently read this on ESPN:

“Every free market evolves differently, and this one -- led by [Juan] Soto, Max Fried's $218 million deal with the New York Yankees and a pair of $182 million contracts for Willy Adames (San Francisco) and Blake Snell (Los Angeles Dodgers) -- has already seen $2 billion committed to 43 major league free agents.”Now somebody do the New York biglaw RX tally, 😜! Between Latham & Watkins LLP (“Latham”), Fried Frank LLP (“Fried Frank”), Weil Gotshal & Manges LLP (“Weil”), and others, are we close to $2b yet this “offseason”? 🤑

What are these firms doing? How do they justify the massive multi-year 8-figure guaranteed pay packages that RX pros seemingly can’t stfu about these days?

📍Well, for starters, they’re hoping that the recipients are bringing over a legitimately portable book of business (spoiler alert: the book of business often isn’t as big as advertised).

📍Second, they’re praying that the new talent will be able to land fresh deals off platform.

📍Third, they’re counting on the fresh blood to serve as stoppers — plugging leakage from on the platform that, in the past few years, has generally benefitted the rapacious team at Kirkland & Ellis LLP (“Kirkland”). Kirkland is successful because the entire firm is bought in to symbiosis with the restructuring group. Leveraging a platform is much easier said than done; leave the door even slightly ajar and someone who maybe kinda sorta looks like this ⬇️ may just slither on through and steal your client. Just ask your friends at Latham, 😜.

📍And, fourth, titles drive business and so firms are handing out titles like candy on Halloween (aka title inflation, ✅!). If you’re looking right and you’re looking left and you see titles multiplying like Agent Smith in the second Matrix and you don’t have one, you may just want to do some introspection — or check your genitalia. Yes, we went there.

Weil isn’t alone in this. Willkie Farr & Gallagher LLP — in the wake of the Fried Frank move — has so many titles that it borders on the absurd. You’ve got “U.S. Chair of the Restructuring Department,” “Co-Chair of the Restructuring Department,” “Co-Chair of the Restructuring Department and Chair of the Company Restructuring & Reorganization practice” (a woman at least!), “Chair of the Distressed Company Governance” practice, and “Chair of the Creditor and Lender Rights” practice. We probably even missed one … or fifteen. We’re going to raise Lawdragon’s 500 Leading Global Bankruptcy & Restructuring Lawyers and announce PETITION’s 1000 Leading Global Bankruptcy & Restructuring Chairs in ‘25, stay tuned.

What’s a good hedge against those inflated paydays and ever-more-inflated titles? Increased billable rates (especially if your title is “Chair” of something, lol). Steadily rising for years, there’s no reason to think increases will slow in the face of these big attorney pay packages. Per Reuters:

“Heading into 2025, U.S. law firms are upbeat about growth opportunities … as this year shapes up to be a strong one, legal industry analysts said … Revenue increased an average 11.9% in the first three quarters of 2024 compared with last year, buoyed by 3.2% uptick in demand and a 9% increase in billing rates.”Sooooo … CPI and PCE increases at around 2.8% annnnnnnnd billing rate increases at around 9%. Got it. Makes perfect sense, 🙄.

*****

In case you missed it, we published our perennial end-of-year survey of leading RX pros before the holidays. You can find Part I here…

and Part II here:

To the extent you want more “hot takes” on ‘24, our friends over at Bloomberg, Reuters and The Wall Street Journal all recently featured commentary from industry pros too (click through links). Enjoy the flood of expertise … one our readers sure did:

😂🤷♀️.

*****

The team remains scattered due to the holidays but we’ll be back in force later this week. In the meantime, here are a few things that caught our eye(s) over the past week….

📈Charts, Tweets + Media of the Week 📈

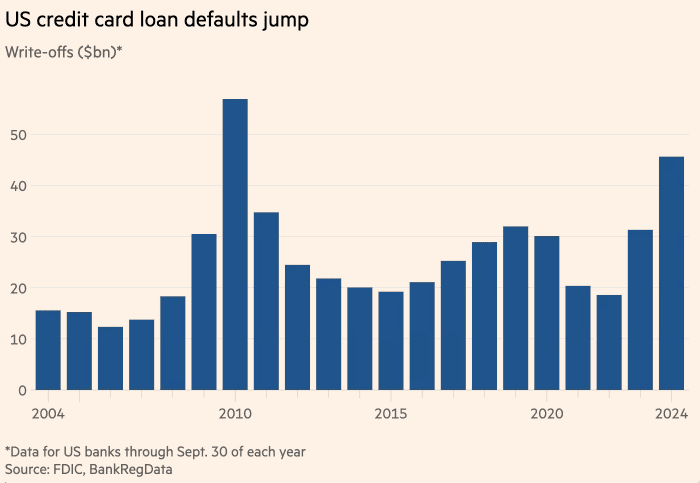

This can’t be good:

Nor this:

Or this:

Notably not one RX pro even mentioned real estate in this year’s survey. Last year if featured very prominently.

Meanwhile, call us crazy but this sounds disruptive (R.I.P. WeightWatchers):

And, finally, don’t RX pros know it:

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

PETITION is looking for one MBA and one JD candidate to work with us as paid interns. This is primarily a research and writing position for up to 10-20 hours a week that will give awesome exposure to the worlds of distressed investing, bankruptcy and restructuring. Work is remote. If interested, email us your resume at petition@petition11.com with the subject line “Internship” and we’ll be happy to answer questions. Cheers.