💥RX Pros Weigh In. Part II.💥

With '24 nearly done, our panel of RX pros looks ahead to '25.

In Wednesday’s a$$-kicking briefing, our panel of highly-accomplished restructuring professionals gave us their take on ‘24. You can find that here:

Today, our panel looks to ‘25. Let’s dig in ⬇️.

PETITION: Put your prediction cap on: what do you think the biggest restructuring theme of ‘25 will be?

Damian Schaible (Partner and Co-Head of Restructuring at Davis Polk & Wardwell LLP): “Post liability management restructurings — I am working on 6 of them right now in various stages and expect more to come. It turns out when you effectively just add leverage and interest expense it doesn’t always help.”

Scott Greenberg (Partner and Global Chair of Business Restructuring and Reorganization at Gibson Dunn & Crutcher LLP): “LMEs and failed LMEs. As we all know — they don’t all “stick.” So while the LME train will continue to chug along, some of these will go off the track and those will be a source of more traditional restructurings in 2025.”

Rachel Albanese (Partner and Co-Chair of US Restructuring at DLA Piper LLP): “Liability mismanagement — that is to say, the subsequent workouts.”

Sean O’Neal (Partner at Cleary Gottlieb Steen & Hamilton LLP): “Continued focus on LME transactions and the litigation it brings, both inside and outside of bankruptcy, until the pendulum swings.”

Erica Weisgerber (Partner at Debevoise & Plimpton LLP): “I mean ... can I say liability management again? Seems like a safe prediction.”

Sanjeev Khemlani (Chairman of Senior Lending Advisory at Lazard): “More of the same: liability management transactions for companies with a maturity runway and loose credit documents and harder restructurings for those without.”

Brett Miller (Partner and Co-Chair of Restructuring at Willkie Farr & Gallagher LLP): “Boring but more of the same. Perhaps at some point we will get around to doing some operational fixes.”

Joshua Sussberg (Partner and Member of the Firm’s Executive Committee at Kirkland & Ellis LLP): “I think ‘25 will be similar to ‘24. A desire to avoid court or otherwise go through the process on an expedited basis only when absolutely necessary. Everyone wants to keep the time (and expense) in chapter 11 to a minimum. All of which is made complicated by the fact that before a filing you do not even know the identity of the stakeholders that will likely challenge the restructuring, all of which is paid for by the company and the ultimate owners of the business. Out of court restructurings and liability management transactions (which have been around forever by the way), will continue. All of which is a good thing.”

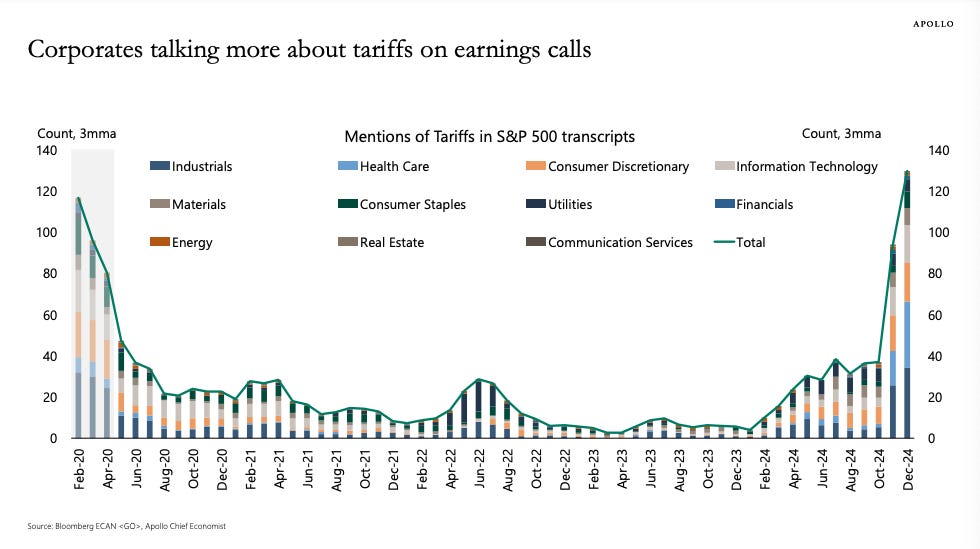

Michael Eisenband (Global Segment Leader of FTI Consulting’s Corporate Finance & Restructuring Group): “Is a Trump presidency good or bad for our business — not in a direct sense but the impact of his policies on corporate distress and restructurings — and how will it unfold? This is a wildcard that can’t really be gamed because he tends to change his mind or backtrack on things he says he’ll do. At least that was true in his first term. There is no reliably predictable pattern of behavior that makes this knowable or estimable. Will the Trump presidency ultimately deport hundreds of thousands of migrants or several million? Will import tariffs really be 25% and will other countries retaliate? Who the heck knows! But the status quo will be shattered, and some things will break.”

PETITION: On the topic of tariffs, btw:

Michael Handler (Partner at King & Spalding LLP): “Difficulty in negotiating restructuring terms due to unpredictable operating/financial forecast because of unknown regulatory/policy changes by new presidential admin and Republican-controlled House and Senate.”

Ryan Preston Dahl (Partner and Chair of Business Restructuring at Ropes & Gray LLP): “This is not a “restructuring” theme, but I believe the principal theme in 2025 will be the accelerating instability among both domestic and international systems. On the former, we have an incoming administration with the stated goal of a near-complete overhaul of accepted governmental practices, coupled with a demonstrated tendency to embrace inflationary (not to say “populist”) fiscal policy. Whether you think this is the right approach or the wrong approach, there cannot be any real question that it will impact markets and, by extension, restructuring practitioners.

On the international level, the continued theme seems to be more instability — not less — in an increasing number of regions and at an accelerating rate throughout the world. Again, not necessarily a “restructuring” theme per se. But it is equally hard to see how market activity and restructuring activity is not also impacted by the geopolitical risks that grow by the day.”

Andy Dietderich (Partner and Co-Head of Global Finance & Restructuring at Sullivan & Cromwell LLP): “Consolidation of creditor funds and advisors.”

David Meyer (Partner, Head of Restructuring and Reorganization, and Member of Management Committee at Vinson & Elkins LLP): “2024 trends continue. I anticipate you will be able to cut and paste my answer about restructuring trends in 2024 next year. When will this trend change? That’s a better question.”

Brian Resnick (Partner and Head of Liability Management & Special Opportunities at Davis Polk & Wardwell LLP): “Lower interest rates and less regulatory oversight leads to increased distressed M&A activity and 363 sales.”

PETITION: Outside of the US, where do you expect to see distress in ‘25?

Cullen Speckhart (Partner and Chair of Business Restructuring at Cooley LLP): “In cross border cases, addressing questions about releases. In cross-border cases, there may be significant debate about whether (or how) Purdue Pharma applies to the question of whether nonconsensual third-party releases can (or should) be approved. Several cases hold that non-consensual third-party releases may be permissible under Chapter 15, but there may be avenues for creditors and other stakeholders to argue that such releases are categorically prohibited under Purdue or barred by the public policy exception under section 1506. However, (i) as made explicit in the Supreme Court’s opinion, the holding in Purdue is narrowly tailored to its own facts, (ii) the Court in Purdue was clear that its decision was a textual one not based on public policy; and (iii) though not binding precedent, some bankruptcy courts that have approved non-consensual third-party releases in recent Chapter 15 cases prior to Purdue Pharma have stated that even if non-consensual third-party releases are categorically prohibited under Chapter 11 by subsequent binding case law, that relief may nevertheless be appropriate under Chapter 15. Without express statutory authority under the Bankruptcy Code for approval of non-consensual third-party releases in Chapter 15 cases, however, stakeholders may use the Purdue Pharma decision to argue against such releases in Chapter 15 cases, and lower courts may reach differing conclusions on the issue.”

Brett Miller: “South America. Plenty of work to be done across South America.”

Erica Weisgerber: “China.”

Sanjeev Khemlani: “The tariffs discussed by the incoming administration could negatively impact the Chinese economy. Combined with the six straight quarters of deflationary prices, a weaker consumer, and a challenging real estate market, distressed activity could pick up in Asia.”

Scott Greenberg: “EUROPE: it’s already coming. If you look at matters like Altice, Ardagh, and others — the wave seems to have hit Europe and that doesn’t seem to be slowing down.”

Josh Sussberg: “Europe.”

Brian Resnick: “Europe.”

Michael Handler: “Western Europe.”

Damian Schaible: “Europe. I keep feeling like we are playing piano on the deck of the Titanic over here in the US while the world very unfortunately burns around us (how is that for mixed metaphors?). Ukraine, Israel, energy transition issues, inflation, costs, China, Korea, tariffs to come, it goes on and on and presumably starts to really impact Europe even as it all starts to come for us.”

Andy Dietderich: “Continental Europe.”

Rachel Albanese: “Europe, Canada, Mexico, China… Will depend largely upon US tariffs and geopolitical events.”

Michael Eisenband: “Economic prospects for Western Europe in 2025 are weaker than they are here. Major political and business news stories coming from most EU countries certainly leave the impression that Europe overall remains highly challenged on many fronts. So are we, but business interests prevail more often here, and certainly that would be the expectation for 2025.”

PETITION Rapid Fire #1: Do cooperation agreements get challenged as an antitrust violation in ‘25?

Damian Schaible: “No. Silly noise from sponsor lawyers talking their own book and trying to brush creditors back from something that — in the right circumstances — can and should provide a hedge of protection to the LM mania.”

Michael Handler: “No, but they might be challenged on another legal basis.”

David Meyer: “Challenged? Likely yes, but among professionals and saber rattling. Litigated? Someone may shoot their shot one day. I don’t know that it is in 2025.”

Andy Dietderich: “Briefly. There are better challenges here if they go too far, as well as a real question about remedies in the event of a sensible breach in the best interest of the debtor.”

Erica Weisgerber: “Possibly. The initial question is who will tee up such a challenge and why. A challenge from a borrower seems unlikely because if the alleged “harm” caused by the cooperation agreement is that a borrower is not able to achieve as favorable a financing as it would otherwise, a distressed borrower seems unlikely to take the time to file a (regular, slow-moving) litigation challenging the co-op; to the contrary, a distressed borrower is more likely to seek out whatever financing is available to it and move on. By contrast, a challenge from an excluded lender seems somewhat more likely — possibly as an add-on claim in an excluded lender’s lawsuit following an LME.”

Joshua Feltman (Partner and Chair of Restructuring & Finance at Wachtell Lipton Rosen & Katz LLP): “I don’t thiiiiiink so? My gut is the time it would take to litigate is too long for it to be an effective tactic for the borrowers and the out of pocket costs to the lenders could be reasonably socialized among the co-op members in the short run (including leading lawfirms in the LM world bearing some risk) with a reasonable expectation of future reimbursement from the borrower in the long run. But definitely maybe … I don’t view it as a real argument, but you can imagine it as a real tactic that could affect lender willingness to compromise on the margin.”

Ryan Preston Dahl: “Great question!”

Sean O’Neal: “I doubt it.”

Cullen Speckhart: “Perhaps.”

Michael Eisenband: “Hopefully not. Lenders gotta be able to fight back or sponsors will continue to punch hard.”

Sanjeev Khemlani: “No, it’s not ripe. Also, if the case is brought and won, it should result in credit investors insisting on greater protections at original issuance which is antithetical to the desires of the issuers.”

Brian Resnick: “No.”

Scott Greenberg: “NO — and if so (see next answer).”

PETITION Rapid Fire #2: If so, does the challenge prevail?

Scott Greenberg: “No.”

Brian Resnick: “No.”

David Meyer: “Good cocktail conversation.”

Michael Handler: “Not on an antitrust basis.”

Damian Schaible: “No. Creditors are understood to be allowed to cooperate on account of their existing debt and the market for new financing is rarely if ever impacted — see private credit being the foil in every single LM transaction.”

Joshua Feltman: “Robert Bork just rolled over in his grave. No.”

Erica Weisgerber: “Perhaps an unsatisfying answer: it depends. Primarily depends on who is bringing the challenge, the terms of the co-op, the context in which the co-op was used, the articulated harm, and the venue for the challenge.”

Cullen Speckhart: “No. At least, not as a final matter in 2024.”

Andy Dietderich: “Not fundamentally, but if the club is exclusionary I wouldn’t be surprised to see a rule of reason applied to any compensation not shared pro rata with other lenders.”

Ryan Preston Dahl: “Even better question!”

Sean O’Neal: “No.”

PETITION Rapid Fire #3: Does the rate of LM increase or decrease in ‘25? In what way will the ‘25 version be an evolution from prior deals?

Brian Bolin (Partner at Paul Weiss Rifkind Wharton & Garrison LLP): “Increase. We will see private equity sponsors increasingly engage in LMEs opportunistically to trade covenant flexibility for debt discount, even in the absence of a catalyst (liquidity need, maturity, etc.) requiring a transaction. We will see lenders organize and sign cooperation agreements earlier and earlier to protect against potential LMEs, or at least ensure they are in the majority group. And we may see public companies start to become more comfortable engaging in LMEs.”

Scott Greenberg: “Yes — it’s not slowing down at all. And I think the move has been to make them more inclusive but tiered. Everyone participates — biggest folks at the best exchanges, and so on and so forth.”

Erica Weisgerber: “Liability management exercises will increase in 2025. Certain businesses — particularly those that rely on imports — will feel the impact of any forthcoming tariffs, which will increase the rate of restructurings generally — and from the company perspective, liability management transactions are typically a better way to deal with distress if possible. As for an evolution: after the initial wave of LMEs, we had started seeing a “kinder, gentler” LME, where excluded lenders were offered the opportunity to participate in the transaction on somewhat less favorable economics. I think what we’re starting to see is a growing disparity between the economics for the participating lenders and the economics for the excluded lenders. As that disparity gets larger and larger, it is likely to reignite another wave of litigation.”

Josh Sussberg: “Increase. While everyone likes to say we follow a play-book, there really is none. Professionals will continue to be creative and utilize the assets that exist in the underlying credit agreements to come up with new and novel ways to extend runway, access cash and potentially even discount. Every single time the industry is able to do that, it is a success. The narrative that 90+% of liability management transactions fail and result in a bankruptcy is exhausting. And simply wrong. If cash is accessed and runway is extended, by definition this is a success. Restructuring professionals do not control operational performance. We can simply create the opportunity and pathway for companies to breathe and have the opportunity to live to fight another day.”

Damian Schaible: “Increase or remain steady. Technology and deal dynamics will continue to evolve to permit even greater differential spreads between majority and minority creditors until (hopefully) creditors just get tired of it and coop up broadly and dare the sponsors to light money on fire with the deal away.”

Joshua Feltman: “Increase. The market will be hot in the first part of the new (old) administration, which will counterintuitively lead to more LM. Long-term rates ain’t coming down and budget blowouts and tariff risks are going to inspire people to get while the getting’s good: look out for “pre-distress LM” where highly- (but not obviously over-) levered companies agree to tighten covenants in exchange for relatively little discount but a whole lotta cash to the balance sheet at reasonable spreads.”

David Meyer: “LME continues to increase taken as a whole. Continued extension of pro rata deals but with exceptions that will arise based on unique facts and circumstances.”

Rachel Albanese: “Increase in frequency; hopefully, decrease in gamesmanship.”

Cullen Speckhart: “It increases, but more double dipping in 2025.”

Brian Resnick: “Similar levels, but with expanding creativity and complexity, and an increasing amount of ‘dips’.”

Michael Handler: “LMs may increase slightly. Third party financings may become more attractive if loans trade up and opportunity to capture discount declines.”

Michael Eisenband: “For all the talk about tightening up loan documents and incorporating various blockers in new deals since 2022, our sources indicate that lender protections in more recent deals are only modestly stronger at best, so there’s little reason to believe that LME transactions will moderate going forward. This is a cat-and-mouse game with sponsors, who often seem to figure out a workaround and have the negotiating upper hand in a borrower-friendly lending market.”

Sanjeev Khemlani: “Increases. The technology continues to evolve due to a combination of competition and creativity. Furthermore adoption will increase in the more insulated markets around the global.”

Brett Miller: “It stays constant as professionals are out there are shopping them every day. Perhaps there will be minor changes based upon the reported decisions. Do we ever really learn?”

Andy Dietderich: “The larger lenders are going to continue to group up and increasingly control outcomes.”

Ryan Preston Dahl: “Increase, but the thrust of the thesis/antithesis/synthesis will be focused on how co-ops impact deal making, particularly the “co-op for life” structure that is out there in the market.”

Sean O’Neal: “Stays about the same.”

PETITION Rapid Fire #4: Do proposed DIP roll-ups get more or less aggressive in ‘25?

Michael Handler: “Thanks to the excellent legal representation of the minority lenders in the American Tire Distributors chapter 11 cases from yours truly, I would say less to the extent there are prepetition contractual sacred rights that prohibit roll ups if the underlying DIP is not offered on a pro rata basis.”

Erica Weisgerber: “I am inclined to say more aggressive, but in reality the answer will likely depend on whether more bankruptcy courts adopt the approach taken in American Tire. Judge Goldblatt’s approach of basically saying, ‘you can close the DIP, but I’m not going to give you protection on it and everyone can reserve their rights’ seemed to manage to get folks to go back out in the hallway and work out a deal.”

Sanjeev Khemlani: “DIP providers are going to remain motivated to push on roll-ups. As the bankruptcies get more challenging or hit companies in out-of-favor sectors (e.g., retail), the roll-up ask will likely get more aggressive.”

Rachel Albanese: “More aggressive. 🚀”

Josh Sussberg: “More aggressive.”

Brian Resnick: “More.”

Brett Miller: “Definitely more aggressive. By 2026, a 4-1 roll-up will seem normal.”

David Meyer: “Proposed DIP roll-ups continue to get more aggressive; Companies and other non-participating stakeholders continue to try and blunt roll-up but TBD on how successful (or not) they will be. Expect more guidance in first half of 2025 on this topic that will help inform/instruct behavior, including from judges who will have their first opportunities to meaningfully weigh in.”

Jeffrey Cohen: “More aggressive. Given recent rulings, why would lenders stop now?”

Damian Schaible: “Hard to get more aggressive, but they will in certain circumstances — read: tough retail restructurings to come.”

Ryan Preston Dahl: “Plus ça change.”

Andy Dietderich: “About the same.”

Sean O’Neal: “Stays about the same. I think we’ve hit equilibrium.”

Scott Greenberg: “This doesn’t appear to be getting more aggressive. The boundaries have been pushed — there is precedent — so I think everyone now understands just how far you can push this envelope.”

Michael Eisenband: “They can’t get much more aggressive without becoming a parody. New money is kind of important too.”

PETITION Rapid Fire #5: Is the default rate higher or lower in ‘25?

Joshua Feltman: “Lower for at least 9 months … fourth quarter’s a toss-up. ’26 > much higher….”

Rachel Albanese: “Lower in ’25 (higher in ’27). It will be a repeat of the ’21 / ’23 cycle, with lots of M&A, crypto and de-SPAC activity. When those businesses flame out due to the lack of fundamentals, the restructuring industry will be there to pick up the pieces again.”

Brian Resnick: “Higher.”

Michael Eisenband: “The abundance of distressed exchanges (DDEs) done since 2022 practically assures that defaults and restructuring activity won’t tank in 2025, as a fair portion of those DDEs eventually will have to restructure. On the other hand, leveraged credit markets remain hot and will provide rescue financing that wasn’t there a year ago. I’ll play it safe and say these opposing forces will be mostly offsetting and so the default rate will remain rangebound in 2025 compared to 2024.”

Erica Weisgerber: “Higher. Based on some of the proposed tariffs and related measures that we might see in early 2025, companies will pay more for imported goods, whether raw materials, parts, components or finished goods. Freight costs will go up as companies try to beat imposition of new tariffs. Higher costs will impact pricing. And even export markets could be impacted by retaliatory duties in foreign countries. With that perfect storm, increased defaults seem likely.”

Sean O’Neal: “Probably higher. Is that wishful thinking?”

Cullen Speckhart: “It is higher.”

Michael Handler: “Higher.”

Damian Schaible: “Higher but not significantly so.”

Sanjeev Khemlani: “Higher as elevated interest rates continue to consume a greater proportion of cash flow and liability management transactions get rated as selective defaults by the agencies.”

Scott Greenberg: “Higher — and mainly because of “selective default” ratings that come with most consummated LMEs.”

Josh Sussberg: “The same.”

David Meyer: “Close to same.”

Ryan Preston Dahl: “About the same in ’25.”

Andy Dietderich: “No clue.”

Brett Miller: “Depends on what President Trump does to the economy.”

PETITION Rapid Fire #6: The Fed lowers the fed funds rate by 100 bps in ‘25? Yes or no and if more/less, why?

Michael Eisenband: “Assuming inflation stays in check (a riskier assumption than most think), then 100 bps sounds about right. Credit market expectations is for a neutral Fed Funds rate ending 2025 near 3.5%, which is consistent with historical norms in non-recessionary/non-inflationary environments. President-elect Trump seems to be making nice with Fed Chair Powell lately, but if the Fed needs to pause expected rate cuts for whatever reason, expect a confrontation with the president.”

Joshua Feltman: “No. Not consistent with the fiscal outlook … extending the 2017 tax cuts, doubling the SALT deduction, probably eliminating tax on tips and more or less eviscerating the IRS, in addition to tariff-induced supply chain dislocation… you know, not not inflationary. Not to mention impossible to fund that deficit without attractive rates for savers. Technically independent but higher deficits will eventually affect even the FFR.”

David Meyer: “I am out on further predictions on what the Fed will do.”

Erica Weisgerber: “A bit too soon to tell, so I’m going to say “roughly 100 bps or thereabouts, 😉.”

Scott Greenberg: “No — too drastic. I think there will be a cut or 2 under trump but I’m guessing in much smaller increments.”

Brian Resnick: “No; too much too soon with inflation still elevated and unpredictable.”

Michael Handler: “No. Inflation is more likely to go up than down.”

Brett Miller: “I assume it will go down but let’s see if the Trump plan is working before we can guess how low.”

Ryan Preston Dahl: “Hoo boy. Pressure will be on Powell from the beginning, and I think Powell is the only one who knows what he’ll do.”

Damian Schaible: “Yes. And then tariffs and increased government spending brings us back to trouble.”

Rachel Albanese: “Yes, and more. Because the incoming president is likely to eliminate the Fed’s independence, and he will crave the temporary market boost a lower interest rate offers.”

PETITION Rapid Fire #7: In the US, the industry that sees the most amount of distress in ‘25 will be … which? … and why?

Andy Dietderich: “Life Sciences – experienced 2nd most distress in 2023 and 2024 (behind retail/consumer discretionary) as a result of among other things higher for longer interest rates. Industry faces growing fixed costs and volatile and uncertain outcomes.”

Ryan Preston Dahl: “Healthcare services.”

Brett Miller: “Healthcare because there are operational problems that have to be fixed and the can has been kicked down the road for too long.”

Cullen Speckhart: “The Services industry – primarily as relates to healthcare and education. Both are dealing with increased operational costs, regulatory considerations, lingering pandemic impacts, and challenges sourcing staff.”

Michael Eisenband: “Can’t go wrong with healthcare facilities & services given that wage spikes, labor shortages and reimbursement challenges that have driven high distress and restructuring since COVID won’t change much in 2025. Activity in the TMT sector (which comprises several industries) has come on strong since 2022, as the combination of tech disruption and high leverage continues to take a toll. And, of course, the retail sector, once a perennial leader in restructurings, is bubbling up again as consumer spending slows and shifts.”

Scott Greenberg: “Healthcare and retail.”

Damian Schaible: “Retailers. A lot of them have scraped through but are getting weaker and consumer sentiment and spending will fail to support them as things feel choppier by second half of 2025.”

Erica Weisgerber: “Retail. Inflation, high operational costs, reduced consumer spending, and competition from e-commerce giants have challenged brick-and-mortar and online retailers alike. These headwinds contributed to increased retail bankruptcy filings in 2024 — including repeat filings for retailers that had already used chapter 11. To survive this evolving landscape, retailers will need to embrace technology, enhance online offerings, and provide customers with a seamless omnichannel experience. Without successful innovation on those fronts, chapter 11 may (again) offer retailers the best opportunity to reshape their storefront footprints, streamline their supply chains, reduce costs, and negotiate better contract terms. A couple of others: commercial real estate is still feeling the effects of post-pandemic move to hybrid and/or remote work models and the reduced demand for office spaces. And with anticipated favorable policies for oil and gas, rollback of EV tax incentives and environmental regulations under the new administration, we can expect electric car makers to experience continued challenges — some of which are endemic to the automotive industry as a whole, where we also might expect to see more action.”

Brian Resnick: “Retail woes continue; potential supply chain disruption and tariffs will lead to some net losers.”

Sanjeev Khemlani: “Retail, because consumer patterns are constantly evolving and the preference for online convenience continues to grow.”

David Meyer: “Difficult to predict what policies the new administration will implement (or not). But eyes broadly on traditional retail, electric vehicles, energy transition, and TMT.”

Sean O’Neal: “Retail and renewables (including electric vehicles). The reasons for retail’s demise are well known and highlighted in boilerplate first-day declarations for the past few years. This thing called the internet seems like it is here to stay. For renewables, it seems like the driving force will be legal and regulatory changes, costs of innovation and lack of continued innovation.”

Michael Handler: “Restaurants — costs will increase (e.g., labor, food), sales will remain stagnant.”

PETITION Rapid Fire #8: What’s your prediction for what comes out of the Judge Jones drama in Texas? Whose head rolls, in the end (if anyone’s)?

Jeffrey Cohen: “I think we’ve all had enough with the Judge Jones drama. Calm has been restored in the Southern District of Texas and that should be all we care about as restructuring professionals. Can’t we satisfy our soap opera cravings by seeing what’s next for Taylor Swift now that the Eras Tour is over?”

Scott Greenberg: “Unclear. Candidly stopped following it, personally.”

Michael Eisenband: “Haven’t those heads rolled, more or less? As for legally determined outcomes, I don’t care to guess. I can only look back on this episode and wonder what the heck these brilliant legal minds were thinking to believe this relationship didn’t need to be disclosed.”

Erica Weisgerber: “It’s been an active year since the news first broke, but my prediction is that it goes away quietly with a whimper. Case in point: just [recently], the SDTX District Court dismissed the lawsuit of the litigant (Michael Van Deelen) who initially lit the fuse on the drama, due to his failure to file an amended complaint after the court dismissed his initial RICO claim. So it seems that Van Deelen himself decided to abandon further pursuit of his claims arising out of the situation.”

Andy Dietderich: “If you can’t say anything nice….”

Ryan Preston Dahl: “No idea.”

David Meyer: “No predictions on this one. Everyone has already lost and loses. It’s sad for all involved and directly and indirectly impacted. But I will predict that SDTX continues to be a popular venue for complex chapter 11 cases.”

Sean O’Neal: “My prediction is that in the future judges will be less likely to not disclose they are living with former clerks who appear before them.”

Rachel Albanese: “Without getting into specifics, the saga is useful to reinforce the critical role disclosure and transparency play in bankruptcy proceedings.”

Brett Miller: “Someone goes to jail. A firm gets the “death penalty” (no more restructuring practice). It will be ugly.”

Michael Handler: “I think Serta gets reversed on appeal. Does that count?”

PETITION Rapid Fire #9: The biggest controversy in RX circles in ‘25 will be _________?

Brian Resnick: “International restructuring systems capturing market share of multinational company restructurings from the US due to cheaper, faster, and ‘non-bankruptcy’ alternatives.”

Michael Eisenband: “Are leveraged credit markets in bubble territory? Credit spreads are near historic lows, yet torrents of money are chasing leveraged credit, and many investors are rationalizing the excess. Hard to believe this can go on indefinitely but the money seems to be there. How much risk and spread compression will lenders tolerate to put money to work?”

David Meyer: “That’s a great question. I'm not sure it's a controversy, but mindful of how the continued advance of AI will have impacts on RX circles and professionals broadly that we will all continue to consider and evaluate in 2025.”

Brett Miller: “Judges being presented with Chapter 22’s asking how the previous plan was ever feasible.”

Sean O’Neal: “I would expect more litigation on LME. There will be outlier situations where majority groups overreach, resulting in litigation and potentially pushback from the courts. Courts decisions on these outlier situations could have effects on more traditional and less aggressive LME approaches.”

Scott Greenberg: “LMEs and the in group/out group dynamic. I think so long as LMEs stay inclusive litigation should be tempered but it feels like each situation presents a new opportunity for folks to test the bounds and if it happens too much, I could see a spike in litigation.”

Michael Handler: “Controversy with respect to Cooperation Agreements will continue, and I think you will see litigation related to same.”

Erica Weisgerber: “By its nature, you can’t predict a controversy before it happens! But we’ll all be watching to see what happens in the shakeout of the recent high-profile lateral moves.”

Cullen Speckhart: “Lateral movement among partners in biglaw restructuring practices.”

Josh Sussberg: “No controversy in ‘25. Everyone in the industry is going to take a step back and be grateful to be part of such a dynamic and impactful community. No one will get lost in the competition, the cases and the positions we take in our matters. Or the daily grind. Instead, everyone will appreciate and be supportive of one another in an effort to leave the community in a better place for generations to come. We will have each other’s backs. Continue to get stronger, more sophisticated and creative. Be incredibly charitable. And along the way we will continue saving thousands of businesses, millions of jobs and develop life-long relationships that will far extend our restructuring careers. Not wishful thinking — it is the truth that we all need some reminding of every once in a while.”

Ryan Preston Dahl: “One topic that’s been a huge feature of recent conversations in Rx-land is whether in fact Houses of the Holy is Led Zeppelin’s strongest album. I’m not sure a consensus has emerged on this point, but there’s a strong case to be made that Houses uniquely showcases the breadth and depth of peak Zeppelin. You have anthems like The Song Remains the Same (which is the title for Zeppelin’s only concert film for good reason) and Over the Hills, balanced on the other end of the spectrum with Rain Song, as well as Zeppelin’s nod to world music with tracks like D’yer Mak’er. Huge range. That being said, there’s a strong counterargument that Houses really cannot compare to IV. Clearly some of the chattering classes may try to underplay just how strong that album really is. But what more can you say about an album where When the Levee Breaks isn’t even close to its best song? More work clearly needs to be done here.”

PETITION: And, finally, what is the one question we SHOULD be asking?

Brett Miller: “Is doing an LME and then having a contested bankruptcy really cheaper and more effective than doing it the old fashioned way and actually fixing the business (operations and capital structure) in Chapter 11?”

Sanjeev Khemlani: “What percentage of LME transactions will be successful?”

Scott Greenberg: “Why don’t borrowers just file anymore when it’s clear they need to?”

Michael Handler: “Will continued consolidation/M&A in the asset management space affect restructurings?”

Brian Resnick: “Could the US implement legislation for a parallel restructuring system for light touch pre-packaged in or out of court reorganizations analogous to U.K. schemes or Brazilian EJs?”

Michael Eisenband: “Is Gen AI having any noticeable impact so far on the way restructuring firms conduct their business, and if not, when can we expect that?”

Erica Weisgerber: “Which industry player hosted the best holiday party in 2024? What’s the best gift for the restructuring advisor who has everything? Where is everyone going for winter break? What was the best destination for a restructuring advisor-hosted trip in 2024? Who do you think is the true author of PETITION? 👀”

Cullen Speckhart: “We should all continue in our curiosity about who is PETITION? Regardless, I’ve had a fun time with this! Thank you!”

David Meyer: “Will anyone figure out who authors Petition before 2026?”

Damian Schaible: “Who writes PETITION? How many big, group changing moves will there be in 2025 with seemingly everyone chasing the money…?”

Andy Dietderich: “How big can US law firms get before they collapse from the core and become black holes?”

PETITION: Or said another way, when does the levee break?

📈Xs + Charts of the Week 📈

An interesting assessment of progress in the world of self-driving cars:

The USPS has been practically bankrupt for years. We wrote about it back in November ‘17 here:

Anyway, this news broke earlier this week:

Given recent news surrounding the liquidation of a pair of retailers, we found this chart interesting:

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

PETITION is looking for one MBA and one JD candidate to work with us as paid interns. This is primarily a research and writing position for up to 10-20 hours a week that will give awesome exposure to the worlds of distressed investing, bankruptcy and restructuring. Work is remote. If interested, email us your resume at petition@petition11.com with the subject line “Internship” and we’ll be happy to answer questions. Cheers.