💥HNY! To Hope and Healing!!💥

Updates: Franchise Group Inc. + Wellpath Holdings Inc. + FOXO Technologies Inc ($FOXO)

Happy New Year, y’all! The PETITION team is back, baby. We’re a full eight days into the new year and we’ve already had our first big chapter 11 bankruptcy of ‘25 with Ligado Networks Corp. (“Ligado”) — a company that’s been swirling around the bankruptcy bin since the last time Donald J. Trump was President of the United States. Don’t worry, we’ll cover (i) Ligado, (ii) the fact that — in a throwback to Trump’s prior presidency — coal bankruptcies are back in vogue, and (iii) much much more — Serta! — in our a$$-kicking paying subscribers’-only Sunday edition. Before we get there, we still have some late-‘24-vintage trash to toss out.1 Let’s dig in.

⚡️Update: Franchise Group Inc.⚡️

You’ll recall that Franchise Group Inc. and 52 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Dorsey) back on November 3, 2024. We wrote about the cases here ⬇️ and a revisit is strongly encouraged:

It’s time we update what we’d dubbed “…the messiest BK case of the year.”

Because we weren’t wrong.

This thing is a total dumpster fire.

From the moment these cases filed, an hoc group of second lien and holdco lenders (the “Freedom Group”) represented by White & Case LLP (“W&C”) and Greenhill & Co. Inc. (“Greenhill”) …

… has been absolutely terrorizing the debtors, their lenders, their respective professionals and littering the bankruptcy docket with a metric f*ck ton of “paper.”

Folks, we’ve got it all in this one: (i) critical vendor and DIP objections;2 (ii) a bidding procedures objection; (iii) a motion to terminate exclusivity, lift the automatic stay, or appoint a chapter 11 trustee (the “termination motion”); (iv) a sh*tload of discovery notices; and (v) boy howdy, if all that wasn’t enough, four — COUNT ‘EM, FOUR — appeals to the district court.3 There’ve already been multiple seven+ hour long hearings: the bills in these cases are going to be absolutely astronomical.4

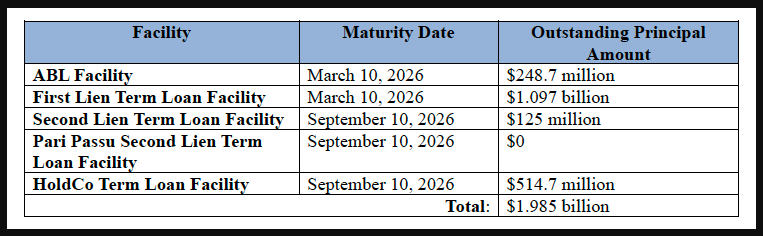

To recap, here is the debtors’ pre-petition capital structure:

At the interim stage, the debtors and the ad hoc group of first lien lenders and proposed DIP lenders (“Ad Hoc Group”) represented by Paul Hastings LLP and Lazard Frères & Co. ($LAZ) agreed to (i) lower the initial DIP draw to $100mm (from $125mm), (ii) limit a proposed roll-up to the interim funding amount, and (iii) reduce fees across the board (backstop from 10% to 9%, commitment from 2.5% to 1.5%, interest from SOFR + 10% to SOFR + 9%, and exit fee at 2.5% but only on new money). Basically, the initial roll-up was egregious AF, W&C’s Tom Lauria and Chris Shore called the Ad Hoc Group out on it, and, in the end, they were able to extract concessions from the Ad Hoc Group under duress. Between the first seven+ hour long hearing and the second seven+ hour long hearing, Mr. Lauria and Mr. Shore were able to extract even more concessions from the debtors and the Ad Hoc Group — although we think it’s fair to question whether the juice was worth the squeeze.

With respect to the proposed DIP credit facility, ahead of the second day hearing, the Ad Hoc Group further agreed to:

📍Limit the DIP guarantees at the holdco debtor level to the amount of proceeds used to fund those debtors’ administrative expenses (which will doubtlessly be huge since all of the litigation has focused on them – though we have no doubt W&C will take issue with any allocation);

📍A tiered-draw schedule that allows the debtors to delay borrowing the final $75mm under the DIP until a later date (saving some fees and interest);

📍Only roll up prepetition loans when funds are actually loaned (vs. rolling up against amounts committed);

📍Eliminate roll-up liens on commercial tort claims and avoidance action proceeds; and

📍Kick out some dates so that the unsecured creditors’ committee (the “UCC”)5 has more time to conduct an investigation.

On the bidding procedures, and also ahead of the hearing, the Ad Hoc Group agreed to:

📍Extend the sale process by about 1.5 weeks;

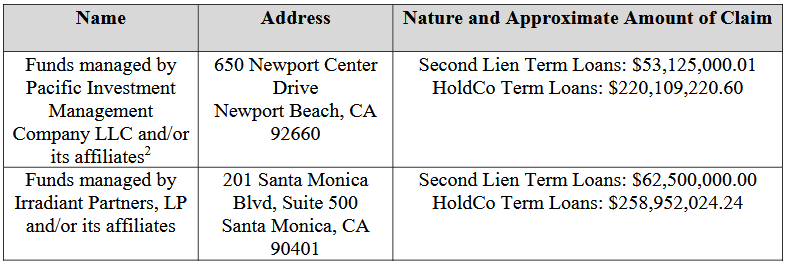

📍Establish minimum bid prices that guarantee a bidder a trip to any auction ($900mm for Pet Supplies Plus, $200mm for Vitamin Shoppe, and $60mm for Buddy’s, all against that hefty $1.985b pre-petition debt stack); and

📍Give the Freedom Group some super duper valuable consultation rights (and, lol, consent rights over changing those consultation rights).

Surely all of that flexibility avoided endless hours in bankruptcy court and ensured a smooth second hearing, right? RIGHT? RIIIIIGHT?

LOL, of course not. Remember this guy ⬇️?

The Ad Hoc Group’s concessions weren’t enough for the Freedom Group, which rained down objections over the course of the rest of the second day hearing (spanning December 10 and 11, 2024). A lot of the testimony was a rehash of what we already heard on the first day, so we can spare you (consider yourself #blessed), but we sat through the whole thing: all eight godforsaken hours of it. During that time, W&C (i) grilled the debtors’ investment banker from Ducera, Christopher Grubb, CRO David Orlofsky (of AlixPartners LLP), and CEO Andrew Laurence over basically each and every (reasonable) decision they made while negotiating the DIP and formulating the sale process and (ii) put on their own expert, Neil Augustine of Greenhill, to second guess each and every (reasonable) decision they made while formulating the sale process. What did we learn? Apparently there’s always some holiday to b*tch about — Mr. Augustine complained about pursuing a sale process over Christmas/Hanukkah/NY — and, of course, more time is always helpful (doubly so when it’s other people’s money being spent, 🙄).

While Mr. Lauria and Mr. Shore provided some entertainment along the way, it wasn’t lost on anyone that the Freedom Group was only there to stir up sh*t and make mountains out of molehills in an effort to create leverage for themselves (and maybe get some professional fees paid). In the end, Mr. Lauria had as much success as his Vols did in the CFB playoffs:

It wasn’t even a game. With a few tweaks to the orders, Judge Dorsey approved the DIP and bidding procedures.

But we still weren’t done! A few days later, on December 17, 2024, everyone got to haul their a$$es back to Delaware for the next fight with our favorite defenders of freedom.

Up this time was the Freedom Group’s termination motion, which sought one of the following totally reasonable outcomes (🙄 - in case you didn’t catch the sarcasm): (i) termination of the debtors’ exclusive period to file and solicit a chapter 11 plan; (ii) a lift of the automatic stay to allow the Freedom Group to foreclose on their collateral and “sweep” the holdco boards; or (iii) the appointment of a chapter 11 trustee — all within about 45 days of the debtors’ petition date, LOL.

Perhaps Mr. Lauria said it best when he described the termination motion to the court:

"Your Honor, I think there are two ways of looking at it. One, is it part of a scorched earth litigation strategy by out of the money creditors? To use the words of counsel to the [UCC], are we just trying to be sand in the gears? Or maybe we're just mad – mad angry, mad crazy? Or is this motion a proper response to a framework set in motion on day one of these cases at the behest of the senior creditors at the OpCos using their positional strength to wipe out the HoldCo estates and their creditors that presumes facts no one has even remotely tried to prove ... If the former, the motion should be summarily denied."To skip a few details, it was the former — it was never not the former — and if anyone reading this really believes otherwise, please reach out, we have some great investment options for you. Judge Dorsey denied the motion.

To demonstrate their constructive approach to the debtors’ cases, the Freedom Group appealed that denial, as well as the court’s critical vendors, DIP, and bidding procedures orders, the very next day because, like, of course they did.

Thankfully this turd is sure to provide some carryover entertainment into ‘25.

🚨Update: Wellpath Holdings Inc.🚨

Back on November 11, 2024, Nashville-based and H.I.G. Capital LLC-owned Wellpath Holdings Inc. (“WHI”) and 38 affiliates (collectively, the “debtors” and, along with certain non-debtor affiliates, “Wellpath”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Perez). Wellpath is a “…provider of localized, high quality, compassionate care to vulnerable patients in challenging clinical environments” which is a super delicate way of saying that it is a medical and mental health services provider to people in correctional facilities, inpatient and residential treatment facilities, forensic treatment facilities, and civil commitment centers. The debtors operate three divisions (“Recovery Services,” “Local Government” and “State & Federal”)6 in ~420 facilities across 39 states, serving ~200k patients daily. Just when Sam Bankman-Fried thought he could avoid the long-arm of the bankruptcy process, we imagine he’s sitting there in his prison cell getting dropped a “notice of commencement” leaflet between bars, lol. Perhaps his roomie Diddy can make bankruptcy the subject of his next jam, 😜.

The debtors, like most of the others we reviewed in ‘24, suffered from increases galore. Like, ⬆️ operating and labor expense, ⬆️ insurance expense, and ⬆️ interest expense. The debtors also struggled to either make money off of existing contracts or maintain contracts and the wheels basically came off in ‘23.7 These were not favorable trends going into a debt maturity — specifically, an October ‘24 debt maturity on the debtors’ pre-petition RCF. Basically this situation was a perfect storm of 💩.

And so the debtors — with an army of restructuring professionals in tow — spent the entirety of ‘24 trying to source an out-of-court solution to address their growing liquidity problem and RCF maturity problem; they brought on Lazard Freres & Co. LLC ($LAZ)(Christian Tempke) and healthcare banking specialist MTS Health Partners (“MTS”)(Jason Schoenholtz) to conduct a marketing process of their behavioral health division, “Recovery Solutions,” with the hope that the proceeds could pay down the RCF and better situate the debtors for an extension of other debt.

That. Clearly. Did. Not. Happen.

And so the debtors found their way into chapter 11 bankruptcy, with a restructuring support agreement (“RSA”) (i) agreed to by the debtors and an ad hoc group of lenders composed of eleven funds: Arena Capital Advisors LLC, Bardin Hill Investment Partners LP, FS Investment Solutions LLC, Lord Abbett & Co. LLC, Palmer Square Capital Management LLC, Prospect Capital Management LP, Ripple Industries LLC, UBS AG, Värde Partners Inc., WhiteStar Asset Management LLC, and Trinitas Capital Management LLC (the “ad hoc group”), and (ii) backed by about 85% of the debtors’ first lien lenders and over 80% of their second lien lenders.

Despite some bumps along the way, the debtors’ cases have progressed remarkably smoothly so far, in large part due to the apparent constructive approach taken by the debtors, the ad hoc group, and their professionals. Here are the highlights of the relief the debtors requested and subsequent developments:

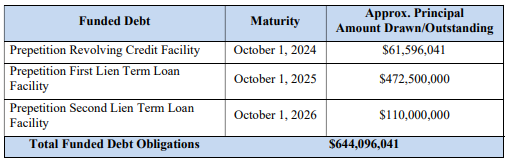

📍DIP Facility. As contemplated by the RSA, the debtors sought approval of a $522,375,000 DIP facility composed of (i) a $105mm syndicated-to-all-lenders-postpetition-but-backstopped-by-the-ad-hoc-group new money component and (ii) a $417,375,000 prepetition secured loan roll-up (a 3.975:1 ratio). HOT DAMN, THAT’S AN AGGRESSIVE ROLL-UP. See, also, Franchise Group Inc. Significantly, the proposed roll-up would have subsumed a hefty portion of the total amount of the debtors’ prepetition funded debt:

But unfortunately for the ad hoc group, that roll-up didn’t sit so well with the US trustee (the “UST”), who lobbed in an objection at the first day hearing. The solution?

The debtors and the lenders punted on the issue, agreeing to a much less offensive interim roll-up of 2:1 on new money actually funded but reserving their rights to fight for the full, much more aggressive roll-up at the second day hearing. During that interim period, the UST appointed a 10-member official committee of unsecured creditors (the “UCC”),8 and rather than have a contested DIP hearing, the lenders agreed (and no one else objected) to a final roll-up of 2.45:1, bringing it down to a total of $257,250,000 — over $160mm less!

The final DIP order also limited the DIP lenders’ credit bid right to the Recovery Solutions division of the debtors’ business (subject to a cap to be agreed among the lenders, the debtors, and the UCC, in a last ditch effort to drum up a competing bid), leaving cold hard 💸💸💸 as the only option for a Local Government or State & Federal business bid and, following the closing of the sale of the Recovery Solutions business, the DIP will be deemed satisfied in full (after which the prepetition lenders step in as the relevant consenting parties with respect to cash collateral usage). Honestly, what a compromise by the lenders!

📍Bid Procedures Motion. Shortly after their cases filed and to comply with the RSA’s timeline, the debtors teed up an emergency motion for approval of (i) fast-track sale procedures for the Recovery Solutions business (culminating in a sale hearing a mere six weeks after filing) and (ii) a slightly elongated sale process for their Local Government and State & Federal divisions (with sale hearings to happen around February 4, 2025).

As suggested above, the DIP lenders are serving as a stalking horse for the Recovery Solutions business. As for the other two divisions, the lenders propose to purchase new equity interests in reorganized Wellpath via a direct private placement pursuant to a plan, subject, of course, to the aforementioned bid procedures and a 363 sale process and with respect to which the UCC reserved all rights.9

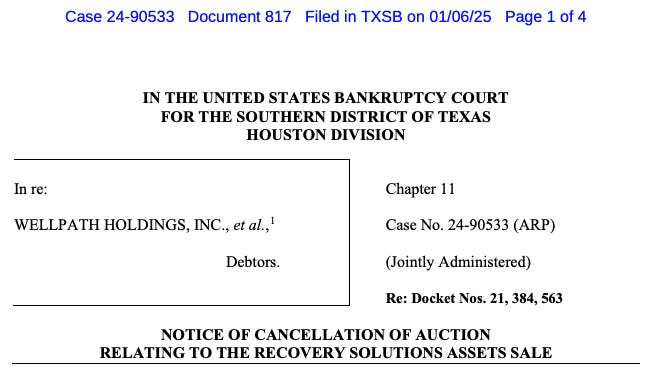

Notwithstanding the debtors’ aggressive timeline, the UST didn’t object, and the court quickly approved the motion on November 18, 2024. But shortly after being formed, the UCC petitioned the court to pump the brakes on the Recovery Solutions sale — as always, more time was needed and, after all, it’s the holidays, 🙄. But after some conversations among the parties, all was well once again — the court entered a new, consensual bidding procedures order kicking out the Recovery Solutions dates by about a week, subject to certain automatic extensions, which have since occurred.10 Bids for the Recovery Solutions business were due on January 6, 2025, and … well … this 👇.

A hearing is scheduled to take place later today, January 8, 2025, wherein the debtors will seek approval of the sale.

📍Bar Date Motion. As most of our readers know, bar date motions are pretty routine and typically don’t get a lot of attention. That wasn’t the case here: given the unique situation in which many of the debtors’ creditors find themselves (you know, behind bars), the bar date motion received some unexpected commentary, namely, from the Center for Constitutional Rights, the Human Rights Defense Center, Public Justice, and Rights Behind Bars, who bandied together and filed an amicus brief. That brief noted what might be considered obvious on reflection: (i) mail service in prisons and jails sucks and requiring the incarcerated, who don’t have regular postal service access or any internet access, to return proofs of claim within 30 days was a bit much and (ii) documents full of legalese can be difficult to understand even for those out there who spent 3 years in law school.

To their credit though, the debtors and the UCC bent over backwards to address their concerns and revised the materials to generally make it easier for those individuals to understand what they need to do and get their claims on file, including by (i) kicking out the deadline to file from 30 to 100 days post-service, (ii) allowing claims to be filed English or Spanish, and (iii) streamlining the process by which relevant debtors are identified.

📍Stay Extension and Relief Motions. Oh boy, are these both messy and fun. Because Wellpath contracts with government entities and provides health services to individuals in — we’ll say — less than ideal environments, they and many of the folks they’ve ever been associated with, including their equity sponsor H.I.G., their D&Os, and doctors, have been on the receiving end of a variety of claims and lawsuits, including “1983 claims.” For those that don’t dabble in that area of the law, 42 U.S.C. § 1983 lets individuals sue for violations of their constitutional rights, such as, for example, denying them necessary medical services while incarcerated. What kind of violations have (allegedly) occurred? About as bad as you can imagine. Here’s what one court found in a prepetition lawsuit:

“[T]here was an avalanche of evidence presented to the jury that [one debtor’s] deliberate indifference [in addressing a patient’s medical needs] caused the constitutional violations inflicted on [her], resulting in her pain, suffering, and death.”

But because the lawsuits involve non-debtors and could result in debtor indemnity obligations, the erosion of insurance policies, and the like, the debtors endeavored to “extend” the automatic stay to certain of their non-debtor affiliates and equity sponsor during their chapter 11 cases.11

The court approved the relief on an interim basis without much fanfare, but understandably, not everyone is on board with this approach: the docket is littered with letters to the court (some, handwritten), objections, and even some motions to lift the automatic stay for lawsuits to proceed. The debtors have been scrambling to get ahold of the various parties, not all of whom have been quick to respond (see mail service point ⬆️), and the court will hold a hearing to figure all this out on January 14, 2025.

While these cases have undoubtedly presented some curveballs and been rockier than the debtors might have liked, it’s way less of a sh*t show than it could have been — kudos to the debtors, the ad hoc group, the UCC, and all of their professionals. We’ll keep you posted on any interesting updates as the cases progress.

The debtors are represented by McDermott Will & Emery LLP (Felicia Perlman, Bradley Giordano, Steven Szanzer, Marcus Helt) as legal counsel, FTI Consulting Inc. ($FCN) (Timothy Dragelin) as CRO and financial advisor, and the aforementioned LAZ and MTS as investment bankers. The UCC is represented by Proskauer Rose LLP (Brian Rosen, Ehud Barak, Daniel Desatnik, Paul Possinger) and Stinson LLP (Nicholas Zluticky, Zachary Hemenway, Lucas Schneider) as legal counsel and Huron Consulting Services LLC (Ryan Bouley) and Dundon Advisers LLC (Matthew Dundon) as financial advisor.12 UBS AG, as prepetition first lien agent, prepetition second lien agent, and DIP Agent, is represented by Cahill Gordon & Reindel LLP (Joel Levitin, Jordan Wishnew) and Norton Rose Fulbright LLP (Robert Bruner, Maria Mokrzycka) as legal counsel. The ad hoc group is represented by Akin Gump Strauss Hauer & Feld LLP (Scott Alberino, Kate Doorley, Marty Brimmage) as legal counsel, Ankura Consulting Group LLC as financial advisor and Houlihan Lokey Capital Inc. ($HLI) as investment banker. Finally, H.I.G. is represented by Akerman LLP (Eyal Berger, Evelina Gentry, Jason Oletsky) as legal counsel.

⚡️Update: FOXO Technologies Inc ($FOXO)⚡️

HOT DAMN this one is a sh*tco. And while we tend to use that word liberally, this one is the real deal.

We took a look at Foxo Technologies Inc. ($FOXO) more than a year ago:

Surprise surprise, the epigenetics sh*tco is still up and running (kinda). Since our initial coverage, the company’s nose dive continued, posting total revenues of $145k for FY’23 vs $511k for FY’22. So what better way to fix the problem than with a couple of acquisitions, right? RIGHT? 🙄

The company entered into two transactions with Rennova Health Inc ($RNVA) between June ‘24 and September ‘24. The first was for an alcohol and drug treatment facility called Myrtle. FOXO paid $500k for Myrtle, split between a note payable ($265k) and stock ($235k). The second was for a critical access hospital, Rennova Community Health Inc (“RCHI,” d/b/a Big South Fork Medical Center). To pay for that transaction, the company planned to fork over $20mm in convertible preferred stock.

No seriously, like wtf is going on? The company has seemingly completely given up on the epigenetics angle and transitioned to a healthcare operator.

But it gets even messier. On September 10, 2024, the parties decided on a different form of consideration for RCHI. Instead of the $20mm in preferred stock, RCHI, as FOXO’s new subsidiary, would issue $22mm in senior secured notes to Rennova. But in another twist of events, on December 5, 2024, the parties backpedaled and agreed to exchange $21mm of the RCHI secured notes back into 21k shares of series A preferred stock that is fully convertible into common stock.

Why? Well the slimmer balance sheet looks better yes, but it might’ve been because the company realized they needed to satisfy the minimum stockholders’ equity requirements of the NYSE American exchange. Indeed, FOXO had already received a notice of noncompliance back in July ‘24. But the shenanigans worked and FOXO regained compliance on December 16.

That’s quite the charade you’ve got going on there guys.

But wait, there’s more f*ckery! At this point Rennova Health is basically just a shell. There is seemingly no operating businesses outside of RCHI and Myrtle as Rennova’s previous medical centers have all shut down. This includes CarePlus Clinic in Kentucky and Jamestown Regional in Tennessee. With these new developments, however, the long time CEO of Rennova, Seamus Lagan, has now found himself as the new CEO of FOXO.13 Further, in ‘20 Mr. Lagan held ~40% of Rennova’s common stock.

Meaning … FOXO is now, effectively, beholden to its new CEO who weaseled his operating businesses into a NYSE listed failing epigenetics company.

And look this is fun, we could spend hours diving into the new documents, but we think this sums up the transactions best, from the 3Q’24 10Q:

“The Company can provide no assurance that these actions will be successful or that additional sources of financing will be available on favorable terms, if at all. As such, until additional equity or debt capital is secured and the Company begins generating sufficient revenue and operating cash flows, there is substantial doubt about the Company’s ability to continue as a going concern for the one-year period following the issuance of these unaudited condensed consolidated financial statements. As a result of the Company’s acquisition of RCHI on September 10, 2024, the Company believes it will be able to fund its operations until the second quarter of 2025. In any event, if the Company is unable to fund its operations, it will be required to evaluate further alternatives, which could include further curtailing or suspending its operations, selling the Company, dissolving and liquidating its assets or seeking protection under the bankruptcy laws. A determination to take any of these actions could occur at a time that is earlier than when the Company would otherwise exhaust its cash resources.”Indeed, 3Q’24 was the first quarter that reflected the acquisitions and the company posted operating losses of $1mm and a CFO of negative $1.5mm. There’s currently $34k of cash on the balance sheet.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📤 Notice📤

Don Harer (Partner) joined Paladin Management from FTI Consulting Inc.

Robin Spigel (Partner) joined Willkie Farr & Gallagher LLP from A&O Shearman.

🍾Congratulations to…🍾

Agustina Berro on her promotion to Partner at Glenn Agre Bergman & Fuentes LLP.

Colleen Restel on her promotion to Partner at Lowenstein Sandler LLP.

Zachary Lanier on his promotion to Partner at Akin Gump Strauss Hauer & Feld LLP.

Turnarounds & Workouts Outstanding Restructuring Lawyers of 2024 including: Gregg Galardi (Ropes & Gray LLP), Timothy Graulich (Davis Polk & Wardwell LLP), Scott Greenberg (Gibson, Dunn & Crutcher LLP), David Hillman (Proskauer Rose LLP), Darren Klein (Davis Polk & Wardwell LLP), Paul Leake (Skadden, Arps, Slate, Meagher & Flom LLP), Lorenzo Marinuzzi (Morrison Foerster LLP), Brett Miller (Willkie Farr & Gallagher LLP), Curtis Miller (Morris, Nichols, Arsht & Tunnell LLP), Gabriel Morgan (Weil, Gotshal & Manges LLP), Joel Moss (Cahill Gordon & Reindel LLP), Sandeep Qusba (Simpson Thacher & Bartlett LLP), Adam Rogoff (Kramer Levin Naftalis & Frankel LLP), Steven Serajeddini (Kirkland & Ellis LLP), and John Sobolewski (Wachtell, Lipton, Rosen & Katz).

There’ll be more ‘24 “trash” to address on Sunday too, don’t worry. Looking at you Spirit Airlines Inc., Intrum AB, and CommScope Holding Company Inc.!

The debtors and the Freedom Group apparently resolved the critical vendors objection through the inclusion of some extremely tortured, over-lawyered language about reserving rights with respect to payments made under that order. The Freedom Group subsequently appealed the order, so it’s not clear what, if anything, was accomplished? The Freedom Group also (i) objected to the debtors’ motion to kick out the deadline to file SOFAs and schedules, which was resolved consensually by punting the DS hearing from December 17, 2024 to January 15, 2024, and (ii) filed a motion to adjourn the second day hearing, which was scheduled for December 10 (coincidentally, the same day as the second day hearing, which went forward, lol).

As if all of that wasn’t enough, a trust established for the victims of alleged fraud relating to the collapse of Prophecy Asset Management LP also objected to the debtors’ retention of Willkie Farr & Gallagher LLP because of “Willkie’s pre-petition relationship with and representation of the Debtors, [Brian] Kahn (the founder and former director and officer of certain of the Debtors) and his affiliated entities, and other parties [including B. Riley Financial] related to fundamental transactions preceding (and possibly causing) the financial collapse of the Debtors and the filing of [their] Chapter 11 Cases.” For a point of comparison, work for Kahn and his affiliates represented about 0.27% of Willkie’s revenue in ‘23, while Vinson & Elkins LLP got bounced from the Enviva cases because Enviva’s 43% equity owner, Riverstone, represented 0.8% of V&E’s billings and 1.4% of V&E’s collections for ‘23. A hearing on the retention is scheduled for January 15, 2025, so stay tuned — could history repeat itself?!

Jabbing a couple thumbs in the Freedom Group’s eyes, on January 3, 2025, the debtors revised their proposed plan and disclosure statement to adjust the strike price of the 2L’s plan recovery (warrants in the reorganized debtors) upwards by all costs and expenses incurred relating to the Freedom Group’s onslaught of litigation, as well as any delay of confirmation they cause — which, we’d be remiss not to acknowledge, is f*cking hilarious.

The UCC consists of Nestle, Solstice Sleep Company, Federal Warranty Service Corporation, NNN REIT, LP (f/k/a National Retail Properties), and Jennifer Walker, individually and in her capacity as a putative class representative; it is represented by Pachulski Stang Ziehl & Jones LLP (Brad Sandler, Colin Robinson, Robert Feinstein, Alan Kornfeld, Theodore Heckel) as legal counsel, Province LLC (Sanjuro Kietlinski) as financial advisor, and Perella Weinberg Partners LP ($PWP) (Bruce Mendelsohn) as proposed investment banker.

In terms of size, the debtors’ “Local Government” division was the most lucrative in ‘23, followed by their “State & Federal” division and their “Recovery Solutions” division. All three, however, suffered revenue setbacks in ‘24.

It seems the debtors’ State & Federal division lost three contracts in ‘24 that accounted for over $440mm of annual revenue, 😬.

The UCC is composed of (i) Scott Allen for the estate of Brady Allen, (ii) Correct Rx Pharmacy Services, Inc., (iii) Ryan Curtis, (iv) Diamond Drugs, Inc., (v) Angela Hoyle, (vi) Elizabeth Naranjo for Estate of Cristo Canett, (vii) Teesha Ontiveros for the estate of Frankie Jacquez, (viii) Select Medical Corporation, (ix) Wellstar MCG Health, and (x) David Ryan Rood – that’s quite a bit of inmate representation!

This outcome is embodied in a plan filed by the debtors in late December ‘24 (Docket 564). In many respects, it’s a placeholder while the sale process plays out and does not include information on projected recoveries or the specific assets to be distributed to unsecured creditors. A hearing to consider approval of the corresponding disclosure statement (Docket 566) is scheduled for January 28, 2025, so expect to see revisions in the coming weeks.

When and how these extensions are triggered is damn murky. The bidding procedures tie the extensions to updates on a fugly website maintained by COMMBUYS (Massachusetts’ official procurement record system), even though the debtors have operations in 38 other states. Luckily, the debtors filed a notice clearing up our confusion.

As the UST pointed out at the first day hearing, this relief is not so much an “extension” as a new injunction, which requires an adversary proceeding. The judge declined to rule on that issue until the final hearing.

It’s not clear why the UCC needs two financial advisors, although each swears up and down it won’t duplicate any efforts by the other. Notably, Dundon’s retention application includes services that appear legal in nature (e.g. “Analysis of … attachment and perfection of liens,” “Analysis of … bar date orders, claims solicitation and receipt procedures and their implementation”).