💥They Choose Violence💥

As chapter 11 activity increases, violence is erupting in bankruptcy court.

💊New Chapter 11 Filing - Endo International plc💊

“Our read of the tea leaves is that other parties will show up to bid.” — Scott Greenberg, Partner at Gibson Dunn & Crutcher, counsel to the ad hoc first lien group.

On August 16, 2022, Ireland-based pharma company, Endo International plc ENDP 0.00%↑and a whole bunch of affiliates (collectively, the “debtors”) filed “prearranged” (LOL) chapter 11 cases in the U.S. Bankruptcy Court for the Southern District of New York (Judge Garrity Jr.).

This, ladies and gentlemen, was a long…time…coming.

So long, in fact, that debtors’ counsel, Skadden, and the debtors’ investment banker, PJT Partners LP PJT 0.00%↑, have been feeing up this motherf*cker since the beginning of 2018.1 😎🤑

That said, things have definitely evolved since then. What started out as an opioid-driven distress story — you know, the usual tale involving a big pharma company (i) getting sued out the a$$ for, among other things, deceptive marketing practices, and therefore (ii) doling out hundreds of millions of dollars in legal defense fees and still having zero handle on disparate processes in disparate jurisdictions and zero visibility into how much potential liability remains outstanding, even after hundreds of millions of dollars of settlements — morphed into a full-fledged distress story.

This distress story is layered but, when boiled down to its simplest form, its awfully hard for a pharma business to grow when it faces a number of stiff challenges like (a) the loss, via court decision, of patent protection over its “crown jewell” sterile injectable, VASOSTRICT ($902mm of revenue in FY21), and the ensuing onslaught of generic production/competition and race-to-the-bottom pricing, (b) hundreds of millions of dollars of legal defense costs, the opportunity cost of which is the inability to invest in research and development — the critical lifeblood of any viable pharma company given the always-ticking clock of patent viability, (c) the effects of the global pandemic including, among other things, stunted growth of the debtors’ branded pharma product, XIAFLEX ($432mm of revenue in FY21) due to the precipitous decline in non-covid hospitalization rate, and (d) an unsustainably large capital structure.

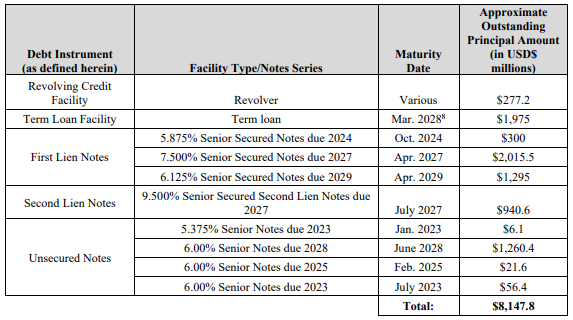

…look at this monstrosity ⬇️:

Per the debtors:

As of June 30, 2022, the Company had approximately $8.15 billion of funded debt outstanding, which is approximately 7x its last twelve months of adjusted EBITDA (approximately $1.22 billion) and greater than 10x its anticipated 2022 EBITDA (approximately $775 million), excluding capitalization of contingent liabilities that could potentially significantly increase such leverage figures. The Company’s expected decline in profitability will further exacerbate the leverage issues facing the Company.

Wait. There’s more:

Additionally, the cost to service the Company’s existing debt balance has constrained its ability to reinvest in its business. The Company currently spends over $550 million per year on cash interest expense, and an additional $20 million on mandatory debt amortization (excluding maturities). The cost of servicing such debt has limited the Company’s free-cash flow available for operations and capital expenditures.

And things may only get worse:

In addition to the Company’s already prohibitive debt service costs, approximately 28% of its debt is tied to floating interest rates. In an increasing interest rate environment, these floating interest rates further add to the Company’s already elevated cash interest expense.

Now, this behemoth of a capital structure may be one thing if say, everyone stayed in their clearly marked lanes but it’s wholly another when you have crossholders of various tranches of debt like you do here. Indeed, the Ad Hoc Cross-Holder Group with which the debtors had been negotiating with exclusively prior to April ‘22 is comprised of holders of all sorts of debt — first lien, second lien, unsecured notes. It’s no wonder that — especially with the opioid overhang and, even with settlements with various states, no mechanism with which to bind all litigants — the debtors struggled to find an out-of-court solution let alone a restructuring support agreement (RSA) that revolves around a plan of reorganization. Rather, the debtors appear to have landed on the path of least resistance given recent financial performance: a sale process with an ad hoc group of first lien creditors holding ~54% of the debtors’ first lien debt (yes, term loans + first lien notes, among other things) intending to credit bid approximately $6b to own this thing on the backend of bankruptcy. Talk about a trial balloon, folks. Let the market determine where the “fulcrum security” is, right? RIGHT?