😎BK Pros Weigh In. Part I.😎

Updates: Troika + Digital Medial Solutions. PREIT & Ebix File.

We asked a panel of restructuring professionals to give us their take on ‘23 and their predictions for ‘24 (last year’s predictions here). And we’ll also be asking you — our dear PETITION readers — for your input on certain things too. Without further ado, let’s dig in with our first question ⬇️:

PETITION: What is the biggest restructuring theme to emerge out of 2023?

Eric Koza (Partner & Managing Director and Co-Head for the Turnaround & Restructuring Services Practice - Americas, AlixPartners LLP): Higher for longer. Elevated interest rates have started to expose the most distressed credits this year, but the trend of prolonged elevated interest rates will likely continue to be felt for the foreseeable future.

Ryan Preston Dahl (Co-Chair of Business Restructuring Practice Group & Parter, Ropes & Gray LLP): Interest rates and inflation (which obviously go hand-in-hand). Investors are trying to figure out how to make balance sheets work where Kd is no longer “zero.” Management teams are trying to figure out how to forecast where declining input costs are no longer a given and employment costs are going haywire. Where it stops, nobody knows.

By the way, you would look at the Silicon Valley / First Republic / Signature Bank failures as a symptom of this same theme. If you believe what you read, these institutions, at core, got caught on the wrong side of a relatively massive duration shift (note: “duration” in the technical sense, not in the “duration is a synonym for maturity” sense). But that’s just another way of saying rates are swinging in a way that we just haven’t seen in many of our professional lifetimes (myself included). Paul Volcker is undoubtedly so pleased, wherever he may be.

Jessica Peet (Partner, Vinson & Elkins LLP): Despite aggressive predictions of a near-term recession, the economy remained relatively steady this year. This resulted in an uneven year for restructuring. We saw a continuation of the existing trend of “lender-on-lender” activity. We saw potential for major disruption with the SVB filing, but it was quickly tempered by government intervention. And as the year progressed, we saw interest rate increases predictably push into court cases that likely would have found an out-of-court lifeline before the increases; this is likely the enduring theme.

Cullen Speckhart (Chair of Business Restructuring & Reorg Practice & Partner, Cooley LLP): Pressure on the banking system. In 2023, we saw two of the largest banking failures in our country’s experience with significant involvement by regulators to ensure stability for participants exposed to the challenges of SVB and Signature Bank. This year, we may learn whether these are aberrant examples of unexpected failure or signals of similar situations to come.

Rachel Albanese (Partner & Co-Chair, US Restructuring Practice, DLA Piper LLP): De-SPAC distress/bankruptcies.

J. Scott Victor (Founding Partner & Managing Director, SSG Capital Advisors LLC): In the dubious words of certain university presidents, “it’s a matter of context.” In mid to lower middle market special situations it’s the de-SPAC sh*tshow that created World War Z! Whether it’s life sciences, real estate, consumer, tech, retail or energy, many of the walking dead warranted a mercy double tap, and I don’t mean Chapter 22.

Evan Hengel (Managing Director, Berkeley Research Group): Zombie companies. In the wake of ZIRP and Covid-era cash stimulus lie a whole bunch of debtors who can’t exist in their current form. As debts come due, there isn’t enough corporate cost cutting available to offset the increase in interest payments that would reflect current market rates. So, we see the continued trend of forced M&A or lenders taking control.

Adam Meislik (Partner, Force 10 Partners LLC): I feel like you guys do such a great job of covering this: liability management exercises were tested, prevailed in BK court, and, as a result, will accelerate. I am sure first-year law associates and junior i-bankers will spend the holiday season scouring indentures for Uptiers, Drop-Downs, and Double Dip opportunities to infuse capital into tight collateral situations.

Damian Schaible (Co-Head of Restructuring & Partner, Davis Polk & Wardwell LLP): “The deal away” — We’ve gotten used to liability management being all the rage for overlevered sponsor portfolio companies. But we used to speak in terms of “lenders vs. lenders” in non-pro rata deals. Enter private credit funds, and we now have “lenders vs. the deal away” in more and more situations. Lenders grouping together to try to offer the sponsor a better deal in terms of cheap liquidity, maturity extensions and — increasingly — discount capture against the specter of a dropdown, double-dip private credit deal….

Michael Handler (Partner, King & Spalding LLP): Competitive special situation financings where sponsor, existing lenders, and/or opportunistic third-party financing sources “compete” to fund money to struggling companies. Runner up: coercive amend and extends.

Brian Resnick (Partner, Davis Polk & Wardwell LLP): Liability management transactions is the obvious call. For cases that do file for chapter 11, we’re seeing an increasing number of mid-market companies (often failed SPACs) filing with 363 sale credit bids instead of going concern reorganizations. With rates going “higher for longer,” and more companies that relied on cheap funding getting stressed, that trend seems likely to continue and even increase.

Dan Kamensky (Founder, Creditor Rights Coalition): Liability Management takes the prize with 21 liability management exercises during 2023 compared to 48 over the past 10 years.

Sachin Lulla (Managing Director, Head of Capital Solutions at Stephens): Liability management continues to dominate discussions with debtor and creditor clients and doesn’t seem to be slowing down.

Matt Warren (Partner, King & Spalding LLP): It is a lame and repetitive answer from 2022, but “liability management” is here to stay (even if we all change the name to something else). Despite numerous transactions, and many of which may only minimally extend runway before creating a more complicated restructuring than may have otherwise been the case, that runway can have value to the equityholders and the “priority enhancing” or other “tactical economics” to the creditors undertaking the transactions can have even more value. It is difficult to see a change in course on this front. Moreover, there is an anchoring and incremental feature with each transaction whereby it seems less aggressive to rinse and repeat or push on new elements for the next. I am sure there is a limit and that there will eventually be a court decision that in some respects stems or mitigates the tide, but when that will occur is anybody’s guess. And even when it does, I think it will be more of a tide mitigator than a tide reversal.

Larry Perkins (Founder & CEO, SierraConstellation Partners): The ZIRP era being over, and restructuring pros (and clients) having to deal with the new reality of where things sit. The 2009-2021 playbook is interesting, but maybe not relevant when it actually costs money to borrow, and valuations mirror that reality. For those of us that have been doing this for a while, it feels like some of the strategies and plays from the 90s and early 2000s are more relevant because there isn’t a buyer for every asset. Hung deals, financial stakeholders being whipsawed and grumpy related to recoveries, and sweating RX pros is the theme I’ve seen the most this year.

Greg Pesce (Partner, White & Case LLP): Winter is coming… but it is not here yet. Everybody entered 2023 thinking a full fledged recession would happen. That did not come to pass though we were all far busier than 2022 and are optimistic for an uptick for more fun to come in 2024.

💥Double Update: Troika Media Group Inc ($TRKA) + Digital Media Solutions ($DSML)💥

On December 7, 2024, Troika Media Group Inc ($TRKA or “Troika”) finally filed its very predictable chapter 11 bankruptcy cases in the Southern District of New York (Judge Jones). We’ve covered this sh*tco extensively before (subsuming links to all previous coverage)…

…so we needn’t give this company too much more of our attention at this juncture. Well, other than to highlight that the office of the United States Trustee appointed an official committee of unsecured creditors (“UCC”). While a UCC appointment in and of itself is hardly worthy of coverage from our perspective, we were amused by the composition of this one given the inclusion of PETITION fave:

That’s right. That’s the very same Digital Media Solutions ($DSML) we last discussed here when we concluded, “[w]e expect this company has a few more “L”s to come.”

Just one more step on DSML’s journey into a bankruptcy court of its own.

🎈Update 3: Anagram Holdings LLC🎈

We last left off our coverage of Anagram Holdings LLC — which, along with two affiliates (collectively, the “debtors”), filed chapter 11 bankruptcy cases on November 8, 2023, in the Southern District of Texas (Judge Isgur) — with a compromise reached between Silver Point Capital and the debtors vis-a-vis the debtors’ proposed sale deadline. At issue was the amount of time prospective bidders would have to diligence the debtors and challenge a stalking horse bid by an ad hoc group of first lien and second lien noteholders for an implied purchase price of somewhere between $180-$190mm. You can read all of our prior coverage here (which subsumes earlier coverage):

So what’s come of that compromise and the extra time? Literally nothing. The final bid deadline of December 15, 2023 came and went without any qualified bids to challenge the original stalking horse bid. The auction that was scheduled for December 19, 2023 is now cancelled and the debtors intend to move forward on December 22, 2023, with their sale hearing to gain approval of the proposed stalking horse APA.

Given Silver Point Capital’s reputation for making things interesting we really thought they might … uh … make … things … interesting.

Not so much.

🛒New Chapter 22 Bankruptcy Filing - Pennsylvania Real Estate Investment Trust ($PRET)🛒

On December 10, 2023, Pennsylvania Real Estate Trust ($PRET)(“PREIT” or the “company”) and 70 affiliates (together, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Owens) — PREIT’s second filing in three years. That’s right, waaaay back on December 11, 2020, the company patted itself on the back for a restructuring-well-done and boasted that it was now ready to “continue to stay ahead of the emerging concepts and uses across [the] portfolio.” CEO Joseph F. Coradino continued:

"We have significantly strengthened the Company … Having quickly and efficiently completed our financial restructuring, PREIT is now a more resilient company with additional resources and financial flexibility to continue delivering terrific experiences for consumers and outstanding service for our retail partners…”

Coradino was a bit more muted in the associated press release on December 11, 2023:

“…We look forward to quickly emerging from this process as a financially stronger company with the resources and support to continue creating diverse, multi-use property experiences throughout our portfolio."

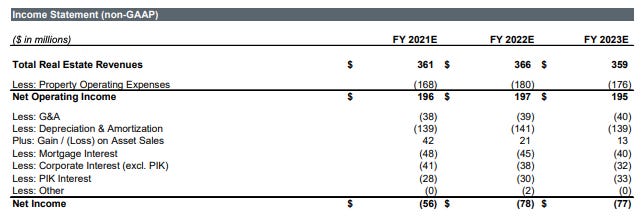

In our coverage of the first restructuring back in ‘20, we highlighted REIT’s overexposure to COVID-blighted commercial real estate (26 retail properties, of which 21 were shopping malls). Shuttered store fronts did not bode well for the $968mm of outstanding debt on balance sheet and so a financial restructuring provided some necessary relief. There’s one rub: it wasn’t much of a financial restructuring after all; it didn’t de-lever the balance sheet; it merely kicked the can. As noted above, the company was optimistic that, once things normalized, the business would spring back. Here are the company’s projections submitted during the initial filing back in 2020:

When compared to actual results, predicted real estate revenue & NOI were over-forecasted 22%/19% and 14%/16% for FY’21/FY’22, respectively. Most egregious was the error in bottom-line forecasts, with actual results around double expectations for both 2021 and 2022:

A lot of that performance is obviously attributable to the parade of horribles this dumpster fire once called “tenants”:

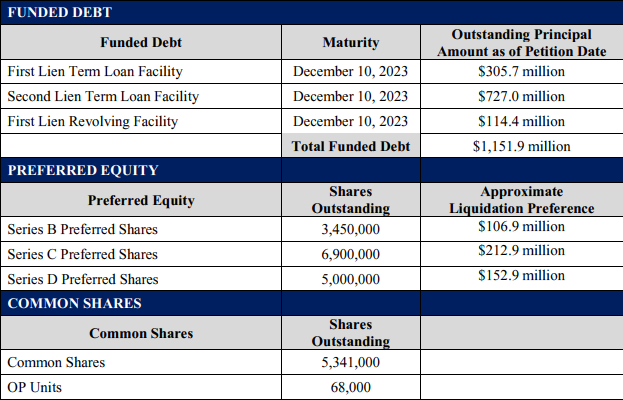

Compared to the $968mm in outstanding debt going into the first reorg, PREIT arrives at its Chapter 22 with $1.15b in funded (and matured) debt:

It also arrived at its Chapter 22 with very few alternatives to the proposed prepackaged plan. A pre-petition sale and marketing process yielded nothing but a metric f*ck ton of doubt about the go-forward prospects for certain, shall we say, lesser quality mall properties. You know … like … the sort that would depend upon JC Penney as an anchor tenant, for instance.

Which gets us to the filing and the prepackaged plan. Here are the highlights:

The plan eliminates $880mm of debt. It envisions the company emerging from chapter 11 bankruptcy with $135mm of debt in the form of (i) a $60mm DIP-to-exit term loan (SOFR+700; an initial $30mm followed by a final $30mm draw to extinguish property debt) and (ii) a $75mm new money exit revolver led by Redwood Capital Management and Nut Tree Capital Management at SOFR+550. Here is where SOFR currently sits. This is not cheap money.

The first lien lenders will be made whole or may choose to convert their claims to the new exit facility at 101%.

The second lien lenders with that massive $727mm nut ⬆️ will equitize into 65% of the new equity with those backstopping the exit facility clearing the additional 35% (subject to dilution from a MIP).

The company will be private at the end of the day with pref and common shares getting the jolly ol’ ax. Collectively, they’ll get a $10mmm payment net of costs with prefs getting 70% and common getting the remainder. They only get this, of course, if they support the debtors’ proposed course and don’t get all cute (seeking, for instance, an equity committee that might delay the debtors’ proposed timeline)(“Based on such advice from its financial advisors, the Board has concluded that the consideration provided to preferred and common shareholders is in effect a gift resulting from a voluntary agreement with the prepetition lenders to avoid the expense of protracted chapter 11 proceedings and shall only be available in the event that the Equity Distribution Conditions are satisfied”).

The debtors are (again) represented by DLA Piper LLP (Richard Chesley, Oksana Koltko Rosaluk, R. Craig Martin, Aaron Applebaum, David Riley, Malithi Fernando, Gregory Juell) as legal counsel and PJT Partners LP ($PJT)(Steven Zelin) as investment banker. The ad hoc group of lenders supporting the prepackaged transaction are represented by Paul Hastings LLP (Kristopher Hansen, Jonathan Canfield, Daniel Ginsberg, Sam Lawand, Jillian McMillan) and Young Conaway Stargatt & Taylor LLP (Matthew Lunn, Robert Poppiti Jr.) as legal counsel and Houlihan Lokey Capital Inc. as financial advisor. A notable early notice of appearance came from Chick-fil-A Inc., represented by Troutman Pepper Hamilton Sanders LLP (Tori Remington, Matthew Brooks), which may just explain PREIT’s troubles. If only it had tenants that were open seven days a week! 😜

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

🔥New Chapter 11 Bankruptcy Filing - Ebix Inc. ($EBIX)🔥

On December 17, 2023, GA-based Ebix, Inc. ($EBIX) and 11 affiliates (collectively, the "debtors") filed chapter 11 cases in the Northern District of Texas (Judge Everett) — something that should come as a surprise to absolutely no one given our previous coverage here and here.