💥Rite-Aid Lives to See Another Day.💥

💥Rite-Aid Lives to See Another Day.💥

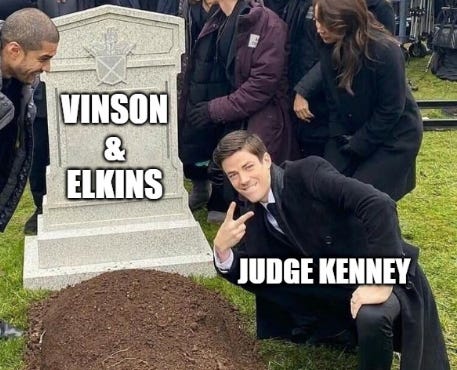

In Enviva Inc., Vinson & Elkins Does Not.

In our last Rite Aid Corp. update …*

… we discussed Judge Kaplan’s case-saving ruling against MedImpact Healthcare Systems Inc. (“MedImpact”), which had been arguing that Rite-Aid was on the hook for $200+ million of (unassumed) liabilities. So, with that out of the way, all good heading into the confirmation hearing, 👍?

👎! There were still some issues to hammer out at the hearings held on June 27 and June 28, 2024.**

One notable issue that remained included the State of Maryland’s (“Maryland”) adversary complaint filed on February 20, 2024. Basically, Maryland was looking to lock in its potential fraud claims as non-dischargeable. “Potential” being the key word here as there is no existing litigation from Maryland against Rite Aid, there’s only an ongoing investigation. And so the debtors filed a motion to dismiss the adversary complaint on April 9th, 2024.

At the confirmation hearing, Judge Kaplan completely agreed with the debtors:

“This court cannot and will not offer an advisory opinion on whether any specific claim or action that Maryland were to bring would qualify for non-dischargeability. Indeed, on several occasions, including yesterday, Maryland has repeated and acknowledged that there is no litigation, but there is merely an ongoing investigation.”

“This court is not the proper forum to pursue an investigation in lieu of litigation. The court can stop there and dismiss this adversary proceeding as baseless and premature.”

He continued the onslaught:

“In any event, Maryland's complaint constitutes little more than a vigorous effort to convert claims bottomed on negligence or malfeasance into fraud-based claims without including the specific facts required in this circuit under Rule 9(b) for fraud claims, specifically alleging falsity, reliance, and the resulting injury tied to the representations or the omission.”

And, finally, here’s Judge Kaplan’s long-winded conclusion, capturing his overall thoughts on Maryland’s pursuit of opioid claims:

“The complaint is being dismissed without prejudice. Notwithstanding, this court hopes and expects Maryland to take a step back and reconsider whether prioritizing such claims and pursuing such claims in the bankruptcy are truly in the best interest of the residents of Maryland. Maryland comes into court under the veneer of protecting its consumers and Maryland's opioid victims and survivors under its parens patriae authority, yet its actions and goals are in direct conflict with the rights and potential recoveries of these same Maryland opioid victims. Every dollar sought by Maryland for its coffers competes with the dollars available to those directly harmed. It has been explained repeatedly to Maryland by the estate fiduciaries working for the general unsecured creditors and tort victims, as well as the court and independent mediators, that continued prosecution of these claims imperil the reorganization and recoveries available under the plan for opioid victims. Unfortunately, we have seen similar parochial actions by other governmental authorities in other bankruptcies in the past. Not only are the anticipated recoveries threatened by such proceedings, but the interest of thousands of employees, poorly served communities, as well as trade creditors and landlords in nearly every state are prejudiced. The court urges Maryland to follow the path adopted after much thought and care by nearly two dozen other states as well as the Department of Justice.”

WOW. S.H.A.D.E.

In addition there were some compromises made regarding language (mainly with insurers). And several objections remained including, among others, those from the NAS claimants.***

Note that that the confirmation hearing also occurred immediately after the Purdue Pharma (“Purdue”) opinion dropped and nullified a massive multi-billion dollar settlement with nearly unanimous approval.**** Meaning, of course, there was an issue with non-consensual third party releases here. Yes, the repercussions of the Supreme Court’s Purdue decision didn’t take long to reverberate!

The United States Trustee (“UST”) previously raised concerns about the debtors’ proposed third party releases earlier in the case but got shot down by Judge Kaplan. Sensing, however, that the playing field had changed given the Purdue decision, the UST be like:

But the debtors were a step ahead; they’d already changed their third-party release mechanics to an opt-in format before the hearing. Per Kirkland & Ellis LLP’s Aparna Yenamandra:

“As we were finalizing issues with the various constituencies, we, the debtors, made the decision to pivot to an opt-in before Purdue came out.”

“We made that decision before Purdue. We did not make the decision as a result of Purdue. We do not think that's the result that Purdue requires. All that being said, now that it is an opt-in, I think it unquestionably is a consensual release. But I didn't want there to be any ambiguity that we were doing it in response to the Supreme Court ruling.”

No ambiguity here Ms. Yenamandra. Who needs a Supreme Court ruling when you’ve got initiative?! Kirkland be some prescient motherf*ckers.

Snark aside, there’s no question whatsoever that this case begged for some creativity after eight months — including, of course, soliciting the releases after voting on the plan, lol (“Just get this f*cker out of BK,” we reckon the lenders exclaimed while busting a lung).

The lenders may not share this view but, hey, perhaps we ought to take a step back and revel in the successes that we’ve seen through these cases. Indeed, all parties involved should get a well-deserved (albeit very self-congratulatory) pat on the back and maybe some time off (enjoy those July 4th Coronas guys!). Ms. Yenamandra summed it up best during her closing statement:

“But all that being said, it has been an extraordinary result, and one that was never guaranteed in these cases. We are a retail company. We face the liquidity constraints and the attrition of any other retail company and the 365(d)4 limits of any other retail company. We have a mass tort angle, but unlike many other companies with a mass tort angle, we don't have the - or we didn't have, at the time we filed - the benefit of being solvent. We are a highly regulated company with a key asset sitting at a non-debtor - that's the CMS receivable you've heard so much about. And we, when we filed the cases, had two businesses operating under one umbrella, the PBM business and the retail business. And so with all that said - and I know you'll hear a chorus of yeses confirming this when others speak up - while this is a monumental achievement, we're at a stage in the case where it's we achieve it now or we achieve it never. The case has gone on too long, and too many people have worked too hard that if we can't get it done now, we're simply never going to get it done.”

After that passionate speech, how could anyone not confirm the plan?

So, yes, of course the plan got confirmed. Did you think Judge Kaplan was just going to flush eight months — plus millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions upon millions in professional fees — down the drain? We think not!! 💰

Judge Kaplan gave a quick bench ruling and echoed Ms. Yenamandra’s praises while also making reference to — speaking of Coronas — Justice “I Like Beer” Brett Kavanaugh’s dissent in the Supreme Court ruling:

“Justice Kavanaugh's dissent in yesterday's released Purdue opinion commented that the Purdue plan was a shining example of the bankruptcy system at work. Some may argue or agree, some may disagree. However, I would certainly offer this chapter 11 case for consideration as an example of the strengths of the bankruptcy court as a viable centralized forum providing financially distressed companies with opportunities to address enterprise threatening litigation and wide ranging financial hurdles.”

We’re surprised that — while VA and TX hang by a thread — he didn’t just come out and say “…strengths of the [New Jersey] bankruptcy court….” But, hey, maybe that’s a little too on the nose.

*You can refer to our other prior RAD coverage here, here, here, here, here, and here.

**MedImpact has already filed an appeal in district court.

***The NAS claimants include plaintiffs who are seeking proceeds for damages involving neonatal abstinence syndrome allegedly caused by opioids dispensed by Rite Aid’s pharmacists.

****Of those who actually voted anyway.

🪦Update: Enviva Inc.🪦

Whoa boy.

We last left you guys with quite the cliff hanger in the Enviva Inc. chapter 11 bankruptcy cases …*

You may recall that at the last hearing on June 14, 2024, the still-dubbed-”proposed-debtors’-counsel”-three-months-after-the-filing Vinson & Elkins LLP filed a motion to reconsider in a last ditch attempt to salvage any hope of getting their retention application approved under section 327(a). That’s a motion to reconsider because Eastern District of Virginia Judge Kenney had already denied V&E’s employment in a memorandum of opinion dated May 30, 2024, denying V&E’s retention on account of its affiliation with Enviva’s 43% equity owner, Riverstone Holdings LLC (“Riverstone”).

Soooo, second time’s the charm, right? V&E’s proposal to impose an “ethical wall” was well-received, right?

Judge Kenney delivered a knockout punch with yet another memorandum of opinion denying the motion to reconsider and denying V&E’s 327(a) retention.

And he had fun doing it as well:

“Even with V&E’s volte-face on the issue of an ethical wall, the Court still finds that V&E is not disinterested.”

LOL, did Judge Kenney just call V&E flip-floppy?

Here’s a quick summary of the decision. Judge Kenney still believed the ethical wall was inadequate and amounted to a “partial wall.” After all, like we mentioned in our previous piece, only a grand total of TWO lawyers were walled off from the debtors. And on the company’s proposed Plan Evaluation Committee (the “PEC”), he had this to say:

“This, in the Court’s view, is only so much window dressing, an attempt to make it appear that V&E is disinterested.”

And, yet, after all of that, Judge Kenney actually tossed V&E a bone; he said the firm could have an “important role” as special counsel under section 327(e) of the bankruptcy code, potentially working on non-core legal matters such as tax and securities law compliance. “The Court anticipates that V&E would respect the limits of any employment under Section 327(e), and that V&E would not duplicate efforts by Section 327(a) counsel.”

Pretty safe to say this is a small consolation.**

*You can refer to our other Enviva coverage here, here, here, here, and here.

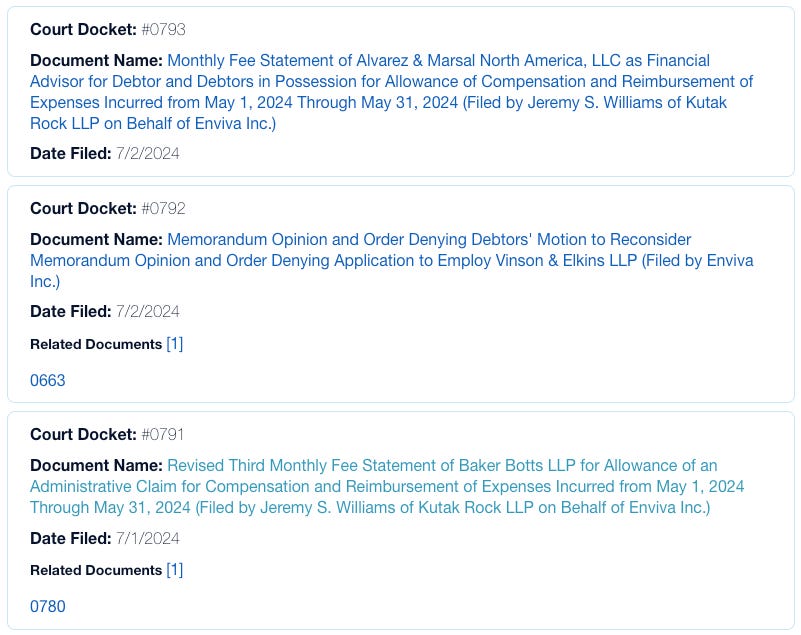

**We hear the company wasted no time taking pitches for new legal counsel. To add insult to injury, Alvarez & Marsal (“A&M”) and Baker Botts LLP sandwiched the V&E rejection with their monthly fee statements ⬇️, 😂😂😂😂😂.

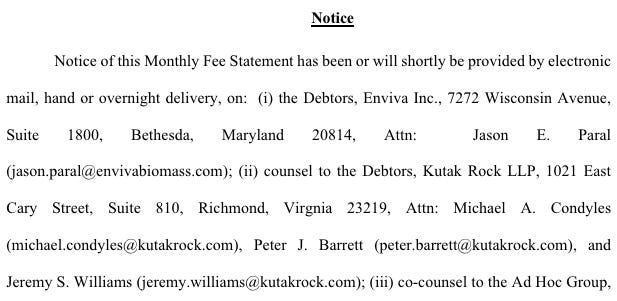

And we’re not sure which one is worse: A&M removing V&E from the notice provision so quickly…

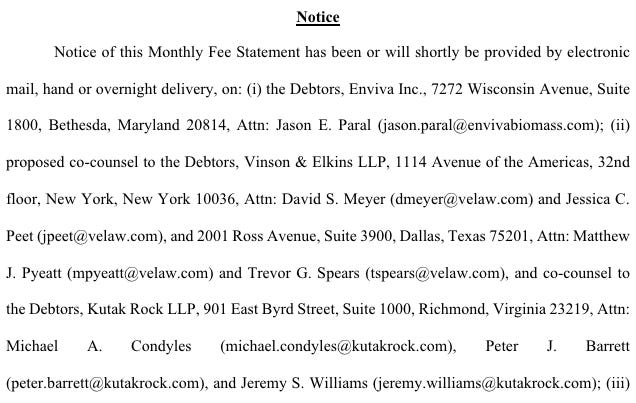

… or Baker Botts neglecting to do so and serving V&E with their fees. 😂😬

⚡️Update: LL Flooring Holdings Inc. ($LL)⚡️

And we’re back with an update on decrepit flooring company, LL Flooring Holdings Inc. ($LL). Here’s our initiation on the company:

In short, a harsh macro environment and a sprinkle of mismanagement have left the company with an impressive four consecutive quarters of same store sale declines. Terrible, yes, but that’s not the focus of today’s update. To understand the current “drama,” we need to make an introduction.

LL was originally founded by Tom Sullivan back in ‘94. Mr. Sullivan then left in ‘16 but returned last year in an attempt to take back the company through F9 Brands Inc. (“F9”) with a series of unsolicited offers. After those were thoroughly rebuked by LL’s board, Mr. Sullivan took it upon himself to start a proxy war in advance of a July 10, 2024 annual meeting, which we covered in our update:

Less than two weeks before this contentious annual meeting, on June 28th, LL filed an 8-K saying:

“Under the terms of the Company’s asset-backed revolving facility credit agreement (the ‘Credit Agreement’), the Company now believes that its projected levels of liquidity may not be sufficient to meet the minimum excess availability threshold in the third quarter of 2024. The Company is in discussions with representatives of the banks that are party to the Credit Agreement regarding an additional liquidity reserve requested by the banks and additional modifications to certain provisions of the Credit Agreement. There can be no assurance that the Company will reach an agreement with the banks regarding such matters.”

Okay, but, what does that mean (other than being a bright red flag screaming liquidity problems)? Well, if excess availability falls below 10% of the revolver cap ($17.5mm) then the fixed charge coverage ratio covenant test will trigger. What’s the fixed charge coverage ratio capped at you might ask? And to that we’d respond, “does it matter?” LL’s adjusted EBITDA has been negative for the last 6 quarters LOL.*

And so if you’re still wondering if the covenant will be tripped (absent any amendment), well…

Of course Mr. Sullivan took advantage of this opportunity to rally supporters to his cause. He issued a press release:

“LL Flooring’s shocking disclosure that its projected liquidity will not be sufficient to maintain compliance with its credit agreement months earlier than previously revealed only further hammers home that urgent change is needed in LL Flooring’s boardroom. It is preposterous for the Board to announce this dire development mere days after communicating to shareholders its strategic plan is working and positions the Company for long-term growth. This Board is burning through cash at a rate that could bankrupt the Company in the third quarter, yet it continues to waste valuable shareholder resources paying high-priced advisors to wage a proxy contest.”

“It should be clear that this Board cannot be left at the helm of LL Flooring if shareholders wish to protect the remaining value of their investments in the Company. F9’s three highly qualified director nominees bring the relevant flooring industry expertise, track records of value creation, shareholder alignment, and actionable plan necessary to stabilize LL Flooring’s business and put it on a path to long-term value creation for the benefit of all shareholders.”

And the list of “high-priced advisors” grows now that the company has reportedly brought on Houlihan Lokey Inc ($HLI) and AlixPartners LLP to help it through this liquidity crisis.

Some more choice words from Mr. Sullivan regarding the onboarding of these advisors:

“This report reinforces that LL Flooring is poorly run, desperate for cash, and teetering on the brink of going out of business as a result of the current Board’s failed leadership and sham sale process. It should be clear to shareholders now more than ever that urgent, meaningful change is needed in LL Flooring’s boardroom if the Company is to survive. F9’s director nominees bring significant flooring industry expertise, a strong track record of creating value for businesses, and an actionable plan to protect the value of shareholders’ dwindling investments in the Company before they are permanently destroyed.”

And no, we’re not done. Mr. Sullivan is also now a potential bidder in LL’s sale of its Sandston, Virginia distribution center (the “Sandston DC”):

“Although F9 Investments, LLC and its participants (“F9”) have been critical of a sale of the Sandston Distribution Center because of the additional lease expense LL would incur, this disclosure suggests that there may be no other option. As a result, on June 28, 2024, following such filing, Thomas D. Sullivan, in his capacity as a private investor and an owner of similar real estate around the country, sent an email to Charles Tyson, the President and Chief Executive Officer of LL, stating that Mr. Sullivan would be interested in looking at the Sandston Distribution Center and requesting the name of person handling this sale.”

The LL board is currently sitting in a corner fuming.

We’re looking forward to an exciting July 10th annual meeting, 🤣!

*If you’re still curious, the ratio is capped at 1:1 and the calculation is EBITDA less capex and taxes to debt service charges.

⚡️Update: Supply Source Enterprises Inc.⚡️

You’ll recall that, back on May 21, 2024, Supply Source Enterprises Inc. and four affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Shannon). We covered the filing here:

The TL;DR is that shortly before the bankruptcy filing, Tranzonic Companies, the parent company of Hopesco Brands Group (“Hopesco”), took out the pre-petition secured lender, committed to providing a DIP credit facility, and further committed to credit bid that facility (and the hefty rollup) for the debtors’ assets. We quipped:

So, for those of you keeping score at home, the stalking horse bidder, DIP lender, and prepetition lender are all the same party…Hopesco.

Judge Shannon expressed some concerns about the multiple hats worn by Hopesco but, ultimately, entered a bid procedures order on June 20, 2024, that authorized the debtors to designate Hopesco as stalking horse bidder. The order also established the deadline for interested parties to submit a “qualified bid.”

Well, enough with the foreplay, let’s just get to it already: nobody other than the stalking horse stepped up to the plate. No real surprise there. Accordingly, the debtors no longer required the scheduled auction and it was “canceled.”

The sale timeline is behind by a week from the debtors’ originally proposed schedule — a sale hearing is set for July 9, 2024 at 11am ET. The sale objection deadline is July 5, 2024 at 4pm ET.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.