💥Manufacturing Something Other than Cars💥

💥Manufacturing Something Other than Cars💥

Updates: Fisker Inc. ($FSR), The Children's Place Inc. ($PLCE) + An Exciting Offer.

We literally just covered Fisker Inc. ($FSR) in our last a$$-kicking paying-subscribers’-only edition on Sunday…

…in which we said “LOL, JK guys, there’s zero chance [further financing from the ‘25 noteholder] happens.”

The company promptly slammed down a March 18 press release that announced further financing from the ‘25 noteholder, LOL.

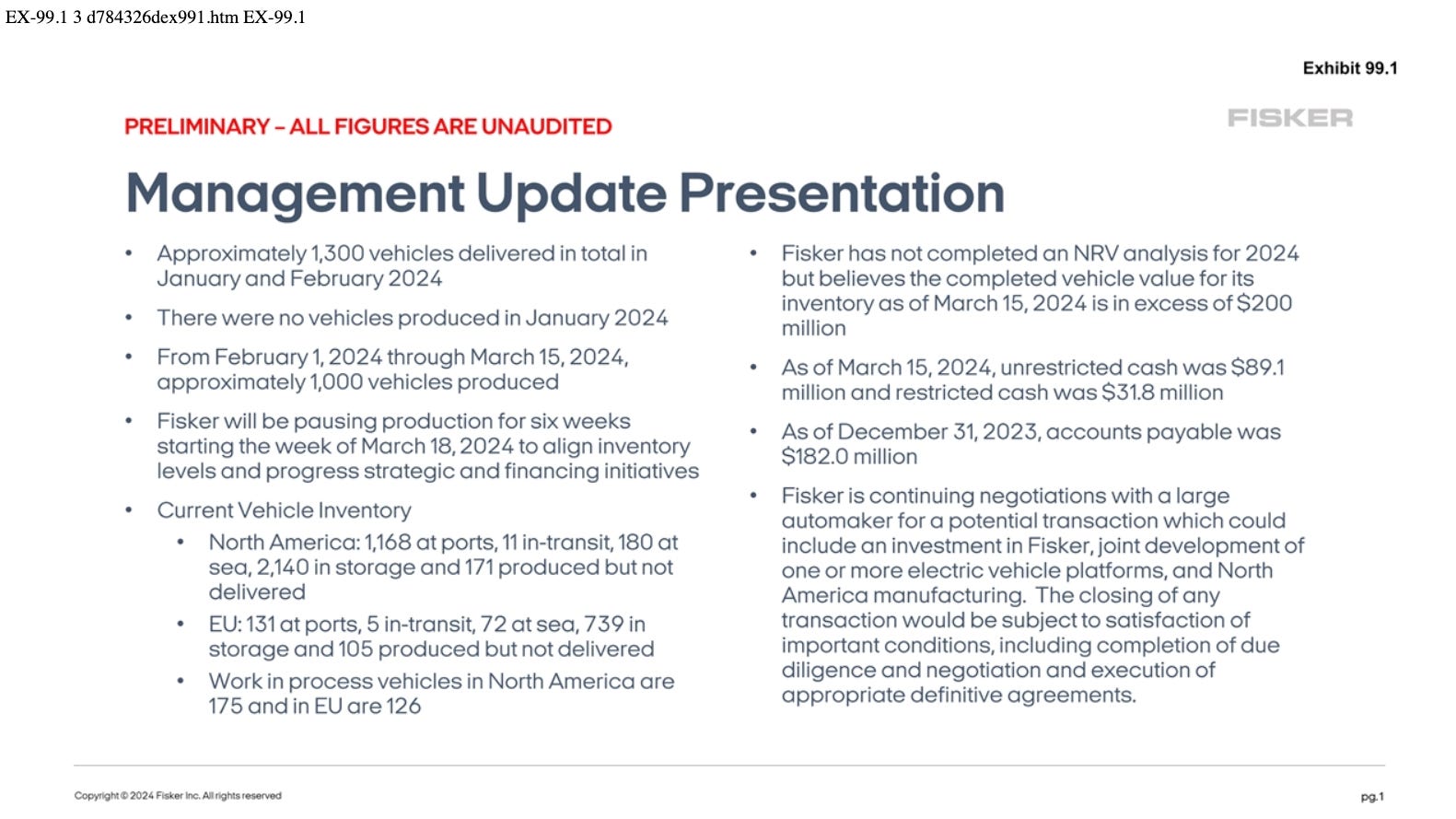

The release and related 8-K filing outline the proposed issuance of $166.67mm of new ‘24 senior secured convertible notes at 10% OID (the “2024 Notes”), meaning gross proceeds of $150mm to the company. The 2024 Notes — which remain subject to documentation — will be issued in four tranches, the first of which is $35mm, and carry a 3-month-SOFR+12% interest rate. In other words, we were more imprecise than incorrect; we meant there’s zero chance the ‘25 noteholder would finance under the terms of those particular converts. And they haven’t. This is an entirely different animal.

Of course, given the sh*tshowy nature of FSR, all of this begs a variety of questions. Who is the “investor” and what is its motive committing more cash to this dumpster fire at this late hour? Let’s dive into the 8-K ⬇️.

Well, we know from a corresponding Amendment and Waiver Agreement (relating to the 2025 notes) filed contemporaneously with the 8-K that the 2024 Notes “investor” is also the holder of 2025 Notes and is an entity called CVI Investments Inc., managed by Heights Capital Management Inc (“Heights”). Ok, great, but what are they looking to achieve here? Per the 8-K:

“All amounts due under the 2024 Notes will be convertible at any time, in whole or in part, at the Investor’s option, into shares of the Company’s Class A common stock, par value $0.00001 per share (the “Class A Common Stock”), at the then-applicable Conversion Price … plus all accrued and unpaid interest and Undrawn Investment Fees … with respect to such portion of such principal amount of Notes….”

This language suggests that Heights will be looking to instantly convert its notes into stock and puke said stock into the market. Why? How many shares will the new 2024 Notes convert into? Asked another way, how many shares will the 2024 Notes have to convert into with the stock trading at … gulp …

…$0.13/share for Heights to make a profit on the 2024 Notes (and potentially mitigate a loss on the 2025 Notes)? The 8-K references the potential issuance of two billion shares, lol. Note that “[t]he conversion price for the 2024 Notes (the “Conversion Price”) will be equal to the Market Price … on the [date the company enters into the securities purchase agreement with investor]” and “[f]or purposes of the 2024 Notes, “Market Price” will mean the lowest daily volume weighted average price (“VWAP”) for the Class A Common Stock on the New York Stock Exchange (the “NYSE”) during the five trading day period immediately preceding the applicable date, but in no event greater than the lowest daily VWAP of the Class A Common Stock on the applicable date.” The VWAP pricing methodology facilitates the dumping of large blocks of shares.

Of course, this really only works if there’s still a liquid market for said shares and that, currently, is at risk (hence, among other reasons, the multiple tranches). Indeed, the company’s NYSE listing is hanging by a thread due to non-compliance (see, again, the share price!). While the listing is theoretically valid for six months from February 15, 2024 (the date the SEC warned the company of non-compliance), there is always the possibility that the NYSE triggers an immediate suspension.

And so there’s some sort of financial chicanery going on here. Heights appears to be manufacturing some returns here. But, at the same time, Heights also appears to be bettering its position; that’s right, it is getting first in line in the event this thing goes belly up in bankruptcy. Per the 8-K:

“The 2024 Notes will be senior secured indebtedness of the Company, rank senior to the Company’s other indebtedness, and be secured by substantially all of the assets and properties of the Company and its subsidiaries (including without limitation, all vehicles, all equity interests of such subsidiaries, leasehold mortgages and all assets and property that currently secure the 2025 Notes, and with a security interest that will rank senior to the Company’s other indebtedness, subject to a consent by the Investor to subordinate the 2025 Notes (as defined below) held by the Investor), subject to exceptions (i) for certain intellectual property rights related to OEM commercial agreements and (ii) as otherwise mutually agreed. Any asset and property that are not collateral of the 2025 Notes will not be required to be pledged as collateral for the 2024 Notes until the closing of the first Additional Draw.”

So, Heights is getting collateral it didn’t have under the 2025 Notes and guarantees from subsidiaries — upon the closing of the first additional draw — that the 2025 Notes don’t have. Of course, Heights is bolstering its 2025 Notes as well. Back to the 8-K:

“As consideration for the holders of the 2025 Notes consenting to subordination of the liens on the collateral securing the obligations under the 2025 Notes to the 2024 Notes, the Company will provide the holders of the 2025 Notes with a perfected lien on any collateral that does not currently secure the 2025 Notes, which liens will rank junior to the first priority lien of the 2024 Notes.”

But what about that rumored OEM transaction previously reported on by Reuters? The 2024 Notes bake in all kinds of covenants and limitations including no ability by the company to undertake additional capital expenditure commitments until the execution of definitive documents surrounding “an OEM Transaction” — which is defined as “[O]ngoing negotiations between the Company and a large automaker for a potential investment and joint development partnership.” Note that subsequent tranches of 2024 Notes funding is inextricably tied to progress around an OEM Transaction. Back to the 8-K:

“The Investor’s obligation to fund each Additional Tranche will be subject to similar closing conditions, as well as (i) confirmation by the Investor of the completion of usual and customary due diligence (satisfactory to the Investor in its sole discretion), (ii)(A) for purposes of the first Additional Tranche, delivery by the Company of an executed indicative term sheet for an OEM Transaction effective as of such date, (B) for purposes of the second Additional Tranche, delivery by the Company of executed definitive documents for an OEM Transaction and (C)) for purposes of the third Additional Tranche, confirmation that such definitive documents remain effective; and (iii) the Company being in Compliance with the Approved Budget as of such date (subject to a 10% permitted aggregate budget variance tested on a cumulative bi-weekly basis).”

Query, then, how long that initial $35mm under the 2024 Notes will bridge the company…? Absent an executed indicative term sheet by the time that happens, it sounds like we’re looking at a potential bankruptcy filing whenever that bridge collapses…?

Which gets us to the next interesting bit in the 8-K. The company revealed that it is in default under the 2025 Notes due to its failure to timely file its FY’23 10-K. The company also skipped $8.4mm of cash interest payments on its 2026 Notes — despite having $89.1mm of unrestricted cash and cash equivalents as of March 15, 2024.

“The Company has elected to not make the Interest Payment (even though it currently has the liquidity to do so and may make the payment in the future) and take advantage of the grace period to allow time for discussions with certain stakeholders in the Company’s capital structure to continue, while also enhancing liquidity as the Company continues to take action to seek a partnership with an OEM partner.”

Hoarding that cash appears to make sense:

The company has ballooning A/P and inventory stuck all over the place. Production is now paused for the next six weeks. Consequently, there’s another going concern warning embedded in the 8-K:

“We need significant additional funding in the near term to execute our business plan and to continue our operations. We continue to seek and evaluate opportunities to raise additional funds through the issuance of our securities, through an arrangement with a potential strategic partner, and from the sale of vehicles. If capital is not available to us when, and in the amounts needed, we could be required to further curtail our operations. Moreover, we may not be able to satisfy our debt service obligations and could need to seek protection under applicable bankruptcy laws.”

This funding buys Fisker some time to find a deal with an OEM; it also serves Heights’ financial interests. But it’s just a band-aid.

The company needs an OEM Transaction to save the day here.

Pedal to the metal, guys.

🔥Meme of the (Mid)Week🔥

Reminder, PETITION has an admittedly under-utilized Insta account here.

👶Update: The Children's Place Inc. ($PLCE)👶

In our prior coverage of The Children’s Place Inc. ($PLCE), we discussed the serendipitous series of financing events that unfolded in February, powered by Saudi-Arabia-based Mithaq Capital (“Mithaq”):

Notably — seemingly out of nowhere — Mithaq committed $78.6mm in subordinated unsecured interest free term loans (😳) to the company, a lifeline of epic proportions. And Mithaq wasted no time following through; it funded the first $30mm tranche on February 29, 2024, and followed that up with the second $48.6mm tranche on March 8, 2024. Mithaq also precipitated the resignation of five board members and appointed a new independent, Douglas Edwards, an executive at Wells Fargo.

Mithaq’s CEO and Chairman, Turki Saleh A. AlRajhi had this to say:

“We are pleased to fulfill our commitment to all the Company’s shareholders by providing $78.6 million in funding, which is interest-free, unsecured, and subordinated. We believe that there is a strong alignment of interests between the Board and all shareholders that will help put the Company on a path to strong future free cash flow generation. We also look forward to the addition of Douglas Edwards to our Board as a new independent director, and we are confident that his expertise will be an asset to the Company as we seek to optimize the Company’s finances and operations. As custodians of the Company, with an equity stake representing over 54% of the Company’s common shares, we look forward to continuing to communicate with all fellow shareholders as we proceed down the path of value creation together.”

There’s going to have to be a lot of value creation for long time stockholders to feel some relief:

The stock has fallen down hard — down nearly 54% — since the initial spike following the announcement of the Mithaq funding.

The company also continues to work on the $130mm Gordon Brothers term loan which is expected to close this month.

We can’t wait to see whether the Saudis have any original solutions for longstanding retail problems.

⚡️Correction: 2U Inc. ($TWOU)⚡️

We love when our readers call us “morons” — especially when we actually deserve it. Last week, in our update on 2U Inc. ($TWOU), we wrote:

In connection with the going concern warning, the company pointed out the $900mm minimum recurring revenue covenant baked in its credit agreement. After seeing results for FY’23, this is getting tighter. Revenue for the past three quarters has been $222mm, $229mm, and $255mm, meaning they would need roughly $294mm of revenue in 1Q’24 to be above the minimum. (emphasis now added).

One of our astute readers pointed out that there was something a wee bit wrong with the math. So, let’s break out the calculator and redo that, shall we? 222+229+255 = 706. 900-706 = 194. So, the company needs $194mm of revenue in 1Q24 (NOT $294mm) to satisfy the covenant. Was this a typo? Or did we just flub the math? We’re going to be honest: it was the latter. Apologies for the impetuous calculation!

With guidance for the quarter being $195mm - $198mm, the company is still cutting it quite close, though the covenant is not as worrisome as we mistakenly pointed out prior. That being said, FY24 guidance is $805 - $815mm, so the covenant should still be on your radar.

📚Resources + AN EXCITING OFFER📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥. We recently added “These Are the Plunderers: How Private Equity Runs — and Wrecks — America” by Gretchen Morgenson.

🔥We also recently added, “The Credit Investor's Handbook: Leveraged Loans, High Yield Bonds, and Distressed Debt,” by Silver Point Capital’s Michael Gatto. Mr. Gatto has agreed to provide ten readers of PETITION with autographed copies of his book. Just send us an email with the subject line “Gatto Book” and indicate what it is you love most about the world of restructuring/bankruptcy/distressed-investing for an opportunity to win one of the books. We’ll select ten people at random and provide Mr. Gatto with your information 🔥

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 10,000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.