💥More Failed LME (Wheel Pros)💥

💥More Failed LME (Wheel Pros)💥

All it took was one year for the company's hyped "double dip" LME to fail.

PETITION Note: we recommend pairing this reading with a classic:

So that sure didn’t take long.

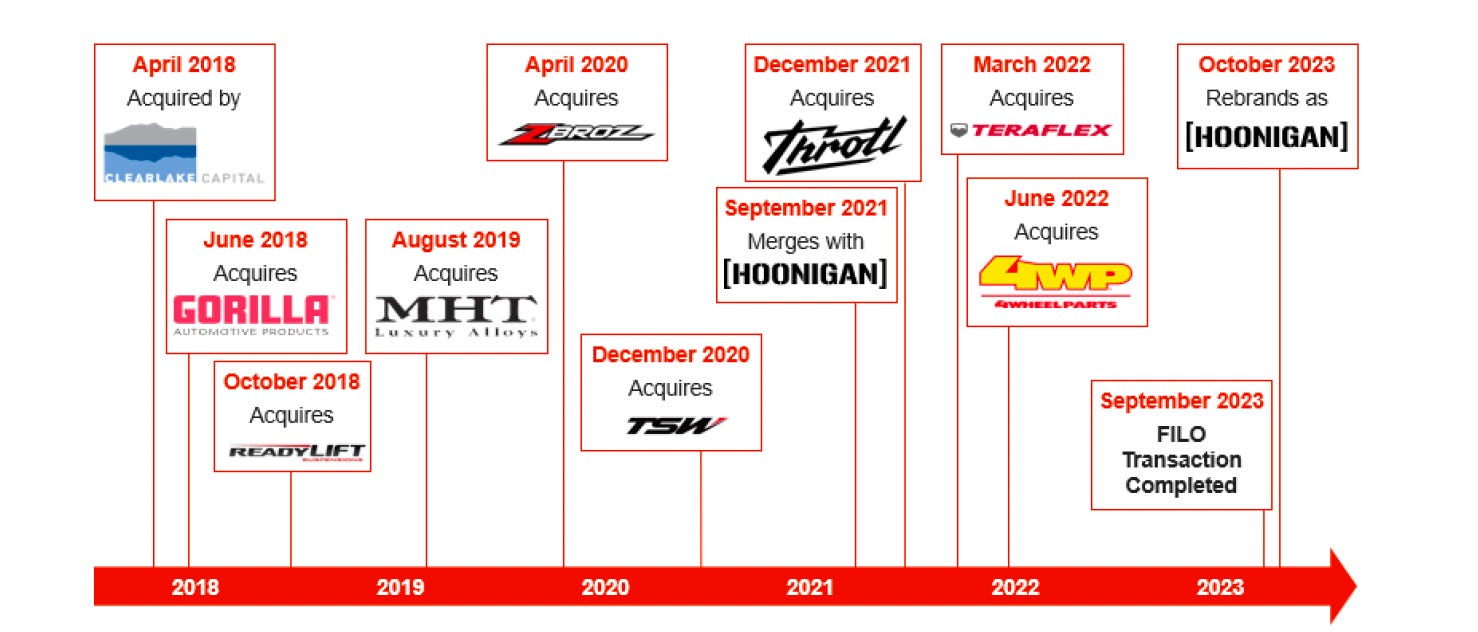

On September 8, 2024, Wheel Pros LLC (d/b/a Hoonigan), a Colorado-based designer, marketer, and seller of aftermarket automotive wheels backed by Clearlake Capital Group (“Clearlake”), along with 26 affiliates (collectively, the “debtors”), filed prepackaged chapter 11 bankruptcy cases in the District of Delaware (Judge Dorsey). This filing comes just a year — ⚡️yes, only a year, 🙄⚡️— after completing a much-publicized “double dip” liability management exercise (“LME”). That’s right, folks: you can add this one to the growing list of busted LMEs, see also J.Crew, Serta Simmons, RobertShaw, Incora, etc., 🥱. Unfortunately, this not-so-exclusive club is sure to expand.

We first wrote about the company back in September ‘23…

… after it announced its LME deal.

We detailed how the company had been struggling operationally and that the market reflected the piss poor performance in the form of a distressed-priced $1.175b ‘28 L+450 term loan and even deeper-distressed-priced issuance of 6.5% ‘29 senior unsecured notes. Both pieces of debt whipsawed throughout ‘23, culminating in the LME announcement on the rather ominous date of September 11, 2023. Happy anniversary, guys!

Significantly, the press release indicated:

Wheel Pros, Inc. ("Wheel Pros" or the "Company") today announced that it reached an agreement with a majority of its lenders for a comprehensive transaction that includes a "new money" term loan, a refinancing and/or exchange of existing debt and a maturity extension of its ABL facility, the result of which will provide the Company with liquidity and reduce total debt. All existing lenders will be offered the opportunity to participate in the transaction. (emphasis added)

Note the bits about “majority of its lenders” and “offered the opportunity to participate.” How did that play out? Well, 11 days later the company dropped this:

You’ll recall that back in February …

… and then in Part II in April …

… King & Spalding LLP’s Michael Handler made a guest appearance with PETITION, offering a primer of sorts on “Double Dip” deals, the then-latest-and-greatest LME technology. In Part II, he discussed the now-debtors at length — it’s worth a revisit because it discusses, in some detail, the mechanics of the deal. Which is great because Mr. Handler literally spilled more ink on the deal in a PETITION newsletter (an a$$-kicking one, we might add) than CEO Vance Johnston does in the entirety of his first day declaration (“FDD”). He writes in the introduction to the FDD:

The Company initially sought to improve its liquidity through balance sheet initiatives. In September 2023, after arm’s-length negotiations, the Company entered into a financing transaction (the “FILO Transaction”) with 99.7% of its existing secured term lenders, which provided a $235 million new money FILO credit facility and a $1.4 billion discounted debt exchange, allowing the Company to capture $140 million of discount on its funded debt obligations. The FILO Transaction extended the Company’s liquidity runway, providing some breathing room for the Company to address legacy SG&A and operational challenges directly. While the additional liquidity supported the Company’s balance sheet, the Company continued to miss near term projections, requiring the Company to consider broader initiatives.

And later in the FDD:

In September 2023, after months of arm’s-length negotiations, the Company entered into the FILO Transaction. This involved both a discounted exchange of $1.4 billion of existing funded debt obligations and $235 million of new-money financing in the form of the FILO Loans. The FILO Transaction provided the Company with both maturity relief and significant incremental liquidity.

That’s literally all he had to say about the LME LOL.

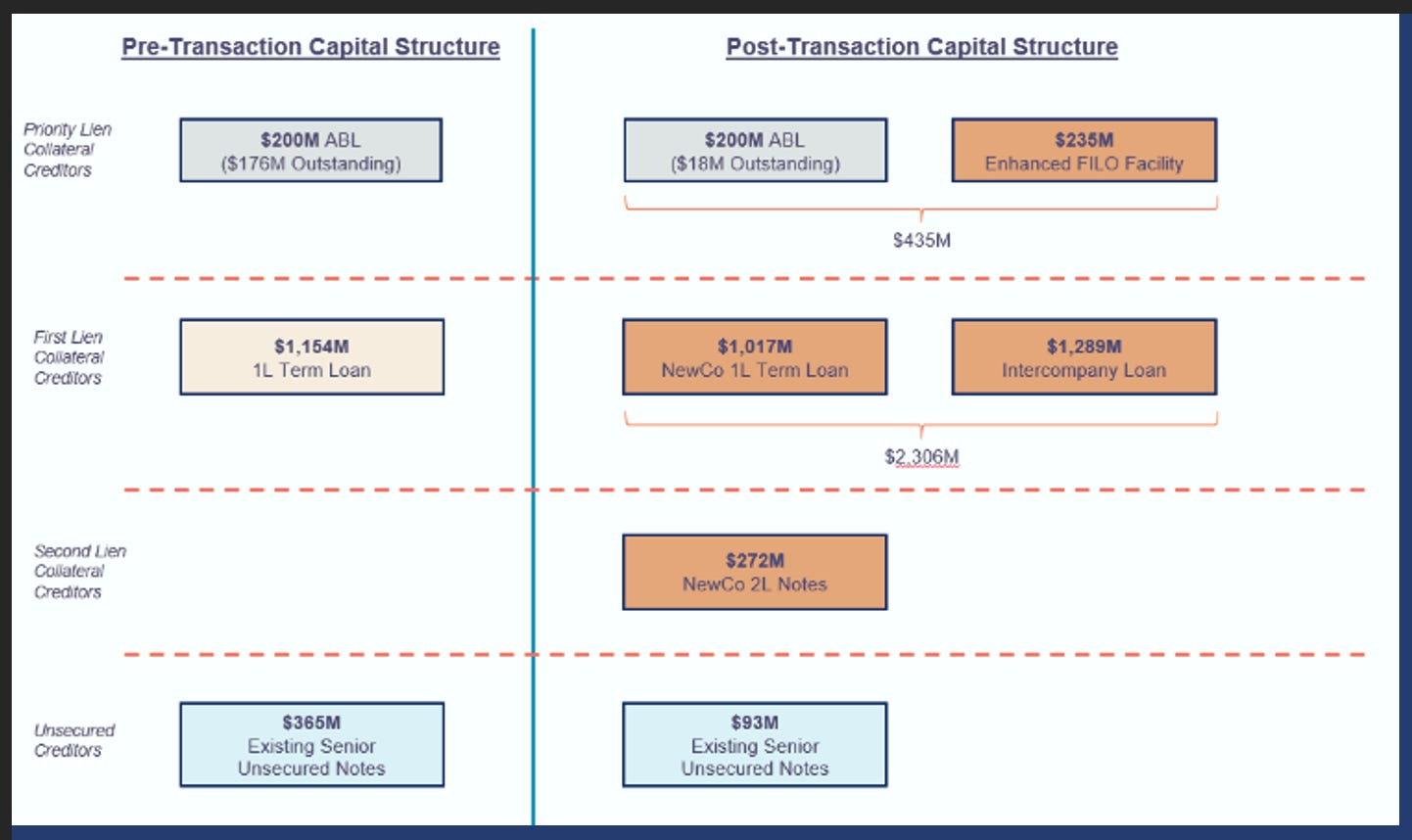

They couldn’t even do us the favor of supplying this handy chart so the more visual-oriented among us can see exactly what that LME translated into:

Instead all we get is this:

What does it show? The FILO referenced by Johnston, for starters. The “almost” 100% participation out of the “Legacy First Lien Loan” into the “NewCo First Lien Loan.” And the uptier of the Legacy Notes into the NewCo Notes. You’ll recall that the debtors and Wells Fargo Bank NA ($WFC), as agent, contemporaneously extended the ABL Facility too.

Ultimately, as we now know, all of the balance sheet chicanery in the world couldn’t blunt the debtors’ operational challenges.* Per the debtors:

The COVID-19 pandemic led to sharp increases in product demand, largely due to increased outdoor leisure time and governmental stimulus support provided to customers. Indeed, heightened demand, coupled with a series of acquisitions in the automotive space, resulted in the Company’s revenue almost doubling between 2019 and 2022. During this period, the Company also acquired companies that expanded the Company’s sales channels outside of the scope of its historic core business and distribution model, including retail locations and e-commerce platforms, with the intention of keeping up with consumer purchasing preferences and expanding the availability of Hoonigan’s products.

Turns out, as we’ve seen time and time again, the debtors over-indexed to a “post-pandemic new paradigm” thesis.

However, macroeconomic issues, including a rapid and dramatic rise in interest rates, persistent inflation, burdensome supply chain disruptions, a decline in customer demand well below the historical trendline, and unsustainable debt service obligations all placed significant pressure on the Company’s revenue and cost structure.

Also, it turns out that integration of acquisitions isn’t so easy:

These factors, together with the inherent challenges of integrating the new products, brands, and operations of acquired companies resulted in significant liquidity challenges for Hoonigan in 2023.

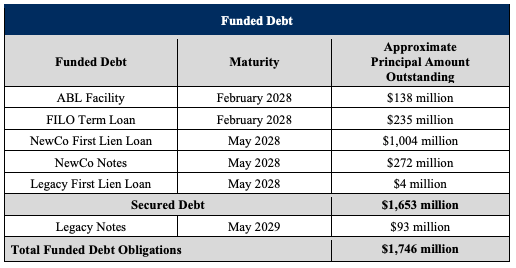

This is, in total, what that looks like:

Indeed, after the LME, “…the Company continued to miss near term projections, requiring the Company to consider broader initiatives.” Heads rolled. The company brought in a new exec team and launched a variety of operational initiatives designed to cut costs. And cut costs they did: they company realized “…an annualized run-rate EBITDA improvement of $39 million in FY 2023….”Alas, it still wasn’t enough and the debtors’ liquidity picture got uglier and uglier. In early July, the $1.1b TL due in May ‘28 priced around 77c on the dollar. A few weeks later, the company missed an interest payment.

And so here we are. A (proposed 40-90 day) prepackaged bankruptcy** to effectuate a restructuring support agreement (“RSA”) supported by holders of 74% of the obligations under the FILO Loans, 99% of the obligations under the NewCo First Lien Loans, 100% of the obligations under the NewCo Notes, and 7% of the obligations under the Legacy Notes. The debtors also intend to use that swift period to negotiate an exit ABL and sell certain non-core assets (e.g., 4WP, acquired in June ‘22 for a “retail footprint” and expanded e-commerce presence, and Poison Spyder Customs Inc.) for plan distribution purposes. Ultimately, the proposed plan of reorganization will eliminate $1.2b of funded pre-petition. The question is how that gets done.

First, you need some that good ol’ American greenback.

The RSA contemplates a $175mm senior secured superpriority SOFR+4% DIP ABL (subject to a “creeping” roll-up) and a $110mm SOFR+8.5% new money senior secured superpriority term loan ($85mm on an interim basis). The debtors also get the consensual use of their lenders’ cash collateral.

And, second, there’s the plan. The “fulcrum security” is at the First Lien Claims level — which includes both NewCo First Lien Claims and the $4mm of Legacy First Lien Loans. That means two things: (i) the FILO Term Loan will get paid in full (note, at $280mm); and (ii) the First Lien Claims will get 85% of the post-reorg equity (subject to a management incentive plan), an amount that the debtors indicate represents a 52% recovery.

The remaining 15% of equity will go to those First Lien Claimants that backstop a proposed $570mm exit term loan facility.

You see that Class 6? That class includes the NewCo Notes, the $93mm of Legacy Notes, and the First Lien lenders’ deficiency claims. If the class approves the plan, the very large deficiency claims will be disregarded and the class will get to share in a whopping $500k cash recovery or as the debtors put it in the chart above, roughly 🍩.1%, lol. Notably, general unsecured claimants will get repaid in full or reinstated. Don’t want a committee here!

So, in the end, the LME appears to have achieved little for anyone — well, other than the professionals getting a second bite at the fee apple.*** The new money didn’t last long. The “discount capture” in the exchange didn’t impact much. And the maturity extensions bought literally only a year. At least Clearlake got to play out that one-year call option!

Summed up more succinctly: what a f*cking joke.

And what of the double dip component? What’s it’s significance under this construct? Take a look at the “Intercompany Claims” entry in the table ⬆️. And let’s turn back to Mr. Handler, the beneficiary here of a “double-dip” appearance with PETITION, for comment:****

“The proposed plan treats the intercompany claim component of the double dip term loan (totaling $1.26b) as part of the Class 8 “Intercompany Claims” and discharges it without any distribution on account thereof. In other words, after all of that “double dip” hype (including devoting a significant portion of my terrific Petition piece to the transaction), the intercompany claim component was disregarded for plan distribution purposes. But before everyone starts singing in unison “in the end, it didn’t even matter,” the Intercompany Term Loans are included in the disclosure statement’s liquidation analysis for purposes of showing that the proposed plan satisfies the “best interests” test or Section 1129(a)(7) of the Bankruptcy Code (which requires a non-accepting holder receive or retain under a plan what such holder would receive or retain if the debtors liquidated under chapter 7). Thus, the liquidation analysis includes the Intercompany Term Loans in the “Total Deficiency Claims of $2.843.8 billion to $2.947.2 billion.” The Legacy Notes Claims — which is the only funded debt tranche not a party to the RSA in an amount sufficient to carry the class if it was separately classified for plan voting purposes — is $110.2mm or 4% of the deficiency claim total. If a group of holders of Legacy Notes organized to object to the proposed plan for purposes of meaningfully improving their treatment thereunder, they would have to fight a two-front war of establishing (i) that there is significant unencumbered value that should be shared pro rata by the general unsecured creditors and (ii) that the Intercompany Term Loans and other components of the term loan deficiency claim should be disallowed or otherwise waived. In sum, whereas the Intercompany Term Loans do not affect distributions under the proposed plan, they could become relevant if a group of holders of Legacy Notes objected to the plan.”

Could.***** We’ll see whether they do.

A confirmation hearing has already been set for October 15, 2024.

The debtors are represented by Kirkland & Ellis LLP (Anup Sathy, Steven Serajeddini, Yusuf Salloum, Erica Clark, Casey McGushin, Lindsay Wasserman, Ashley Surinak) and Pachulski Stang Ziehl & Jones LLP (Laura Davis Jones, Timothy Cairns, Edward Corma) as legal counsel, Alvarez & Marsal LLC (Cari Turner) as financial advisor and Houlihan Lokey Capital Inc. (Matthew Braun) as investment banker. A special committee helmed by Jonathan Foster is represented by Cole Schotz PC. The ad hoc group of lenders is represented by Akin Gump Strauss Hauer & Feld LLP (Philip Dublin, Daniel Fisher, Zachary Lanier, Omid Rahnama) and Potter Anderson & Corroon LLP (M. Blake Cleary, Gregory Flasser, Maria Kotsiras) as legal counsel and PJT Partners LP ($PJT) as investment banker. Strategic Value Partners LLC is the largest holder of the NewCo First Lien Loans and NewCo Notes; it is represented by Davis Polk & Wardwell LLP (Damian Schaible, Adam Shpeen, David Kratzer) as legal counsel and Lazard Freres & Co. as investment banker. Morgan Lewis & Bockius LLP (Christopher Carter, Stephan Hornung, David Shim) and Morris Nichols Arsht & Tunnell LLP (Derek Abbott, Matthew Harvey, Sophie Rogers Churchill) represent Wells Fargo as pre-petition and DIP ABL Agent. Finally, Clearlake has Katten Muchin Roseman LLP (Steven Reisman, Cindi Giglio, Lucy Kweskin) and Polsinelli PC (Christopher Ward, Michael DiPietro) in its corner.

*One can only wonder whether Clearlake “PE Bro’d” the hell out of this company with a rollup of hobbyist sh*t:

**Technically this is a “straddle” prepack in that solicitation commenced but didn’t finish pre-petition.

***Notably, the consenting lenders to the deal have already agreed that they will “not object to or otherwise seek to hinder” payment of Houlihan’s fees and expenses.

****Technically triple DIP since we broke the primer up into two parts but whatever.

*****There was no indication at the 41-minute long first day hearing that this might happen so it’s entirely possible and, in fact, highly likely, that the “double dip” aspect of this particular LME will prove academic and nothing more. Indeed, there was no mention of the concept “double dip” whatsoever.

🔗What We’re Reading (11 Reads)🔗

We spent some time clearing out our inboxes over the Labor Day holiday and here are a few things the team found interesting:

1. Bankruptcy Talk (Short Retirement). There’s something about bankruptcy professionals having an aversion to retirement. Here is James Sprayragen — formerly of Kirkland & Ellis LLP and now at Hilco — talking bankruptcy stuff with Bloomberg Intelligence:

Want more restructuring porn? Here’s another podcast featuring Jimmy Levin, CIO of Sculptor Capital Management:

Yes, these podcasts and not something we’re “reading,” but let’s not get nitpicky.

2. Blockchain Technology (Long Overdue Usefulness). Hallelujah! A blockchain use case that may actually apply to the simpletons of the world like Johnny. California’s Department of Motor Vehicles digitized 42mm car titles using the Avalanche blockchain “…in a bid to detect fraud and smoothen the title transfer process…,” according to Reuters in an exclusive piece published at the end of July. Per Reuters:

Digitizing car titles will reduce the need for in-person DMV visits and the blockchain technology will also function as a deterrent against lien fraud.

Blockchain technology can help detect lien fraud by creating a transparent and unalterable record of property ownership, making it difficult for fraudulent activity to go unnoticed.

Reduce DMV visits?!? One of the presidential hopefuls should campaign on this sh*t and they may find themselves breaking a popular vote record.

3. Busted Tech (Long ABCs). Per Inc:

In the first quarter of 2024, 254 venture-backed clients of Carta shut down, according to data from the equity management company. That's a 58 percent increase over the prior year--and a seven-fold jump over the 2019 numbers, when Carta first began tracking failures.

The number of VC-backed company collapses was the highest this decade, but Carta says it wasn't an outlier.

"The number of company closures has been steadily rising for the past two years," the company wrote. "Between Q1 2022 and Q1 2023, the number of shutdowns experienced a 124 percent year-over-year increase. Between Q1 2023 and Q1 2024, the count grew by another 58 percent."

The author blames a sharp pullback in venture funding as a “…chief reason[] for the growing failure rate…” though another chief reason could just be that a lot of the companies funded in the ‘20-’22 timeframe were just really f*cking dumb ZIRP-juiced companies with no real reason to exist.

Speaking of “f*cking dumb ZIRP-juiced companies,” the pain continues in the Amazon aggregator space (see Thrasio Holdings’ chapter 11 filing earlier this year). Here CNBC reported on a potential merger between two aggregators, Branded and Heyday:

Amazon seller aggregators. Companies in the space took advantage of low interest rates and pandemic-driven growth in e-commerce to collectively raise more than $16 billion from top names on Wall Street and in Silicon Valley with the intent of rolling up independent sellers on Amazon’s marketplace. Aggregators caught the attention of high-profile investors like L Catterton, BlackRock, and even Jared Kushner’s Affinity Partners.

Cracks began to appear in 2022 as venture funding dried up for cash-burning startups and e-commerce demand cooled with consumers returning to physical stores. Aggregators were suddenly struggling to profitably operate the brands they acquired.

Former highflier Thrasio, an early leader in the aggregator space, filed for bankruptcy in February and lost several key executives.

Hahaha, lost several key executives? Um, they weren’t lost; they were sh*tcanned and left hung out to dry when the time came for plan releases to be doled out, lol.

4. DAOs in Bankruptcy (Long DeFi BK). In this abysmally written piece, we learn that a decentralized autonomous organization called Hector DAO obtained recognition of a BVI foreign main proceeding in a Chapter 15 filing in New Jersey! This is not exactly what we had in mind back in early ‘22 when we pondered how/when bankruptcy pros would encounter the DAO bros but, 🤷♀️.

5. Drones (Long Crowded Skies?). Maybe some of our Dallas-based readers can chime in here but there’ve been some big developments in the drone delivery space: the US Federal Aviation Administration (“FAA”) has now give multiple drone delivery operators license to fly autonomously in the same airspace simultaneously. This is doable via what’s called the Unmanned Aircraft System Traffic Management system and here is a company called Zipline showing how it works:

Google is also a beneficiary of the FAA’s recent gradual acceptance of drones in our skies.

6. Hotel Robots (Short Human Masseuses). New York City hotels are introducing 30-minute $75 robotic massages and this Bloomberg piece runs through the pros and cons — of which there are many. While phallic AF, apparently it cannot pierce back knots and so Johnny ain’t interested. He’s also concerned about a rogue robot deciding it might be fun to snap his back and neck so, yeah, there’s both a health and psychological component to trying this. Frankly, it lost him at the point he’d have to put on special clothes. Hard pass. $75 massage in midtown, though, 🤔. If adopted — and it likely will be — this is credit negative for the masseuses of the world.

7. Media (Long AI). There’s something wholly unsettling about the fact that a media company that’s widely been considered “successful” — here, Axios — had to sh*tcan 50+ people because of, among other things, artificial intelligence. One silver lining: Axios founder Jim VandeHei, while putting the writing on the wall back in April, suggested that “high-end subscription newsletters” will survive. We certainly hope so!

8. Reef Technology (Long Retrenchment). We’ve previously referenced this Softbank-backed Miami-based “startup” — if you can even call it that anymore — here and here. It’s basic premise is to utilize under-used parking lots for mobile kitchens. Before this genius business idea spewed out of the bee’s nest that is Masa’s brain, they also had software to help passersby reserve unused or underused parking spaces. It was called ParkJockey back then. Then Masa dumped $1b into it, said “think bigger,” and, well, we all know what that means after seeing it play out in WeWork, lol. Per Commercial Observer:

The SoftBank (SFTBY)-backed company that grew out of the pandemic providing restaurant services out of trailers on a delivery-only basis is continuing its closure of locations in major cities by laying off 53 workers and shuttering its locations in the Bronx, Manhattan and Long Island, according to disclosures with the New York State Department of Labor.

That doesn’t sound promising. At least you should be able to find parking against on W. 24th Street between 5th and 6th Avenues.

9. Road Taxes (Long EV-based Disruption). What happens when governments depend upon gasoline taxes for infrastructure maintenance and yet EVs gain adoption? People are worried about this issue.

10. Solar (Long Homely Green Revolution). Plug-in solar panels are all the rage in Germany and the European country may be on the forefront of something big for the sustainability movement. And for China’s solar manufacturing industry.

11. The Future of Hospitality (Long Marriott Bonvoy Points). Sonder Holdings Inc. ($SOND), which we’ve written about here and here, has secured additional liquidity at the cost of selling its soul to Marriott International Inc. ($MAR). Through a 20-year licensing agreement, the company’s properties will now be available through Marriott’s website and you’ll be able to use your sweet sweet Bonvoy points to book them. Here’s co-founder and CEO, Francis Davidson:

“The importance of large, recognized brands can’t be overstated in our industry. In fact, the last few decades have been the story of hospitality brands joining forces under groups that now house numerous brands under a single platform. A diverse array of brands means more selection for loyal guests, driving increased share of wallet.”

The market seems to view this very favorably. The company’s stock is up nearly 104% YTD. Not too shabby for a company that, based on poor operational performance, appeared to be getting closer and closer to bankruptcy court footsteps.

Selina Hospitality Inc. ($SLNA) on the other hand, well, 🤷♀️. We initially covered the name here, but, in short, the company is a hostel operator with the added schtick of also providing coworking spaces (yeah, we were confused as well — digital nomads or something). Nearly a year after our initiation, the company entered administration in the UK with FTI Consulting Inc. acting as administrator. The stock has been wiped. The “future of hospitality” ladies and gentlemen.

📤 Notice📤

Joe Zujkowski (Partner) joined Latham & Watkins LLP from Gibson Dunn & Crutcher LLP.

Rebecca Marston (Associate) joined Perkins Coie from Kirkland & Ellis LLP.

Timothy Walsh (Partner) joined Steptoe from Winston & Strawn LLP.

Vinod Chandiramani (Partner, head of Capital Advisory) joined Solomon Partners from Greenhill & Co. Inc.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.