🍔New Chapter 11 Bankruptcy - TGI Friday's Inc.🍔

Casual dining restaurant chain succumbs to the long-arm of COVID-19, sheds meaningful footprint.

Friday doesn’t mean what it used to.

On November 2, 2024, Dallas-based casual dining chain TGI Friday’s Inc. and 22 affiliates (collectively, the “debtors”)* — purveyors of beer, cheese and “beer cheese” — filed chapter 11 bankruptcy cases in the Northern District of Texas (Judge Jernigan), blaming financial challenges that resulted “…from COVID-19 and [their] capital structure.” Founded in ‘65 in NYC, the debtors currently offer, across their 39 owned/operated restaurants, classic American food (like “beer cheese,” a true classic) and bevvies with a vibe meant to “…celebrate the liberating spirit of ‘Friday’.”** LOL, looks like WFH stole some thunder there, y’all.

These debtors are going to do more harm to the commercial real estate sector than they did to your arteries. Pre-petition, the debtors ceased operations at 79 locations,*** surrendering possession of the premises to their landlords; they now seek to reject those leases pursuant to section 365 of the bankruptcy code, a strategy that will result in nearly $1.4mm of savings — per month. The debtors also seek to reject the lease of the corporate office in Dallas. There’s just one problem: they need to get some valuable property out first and their landlord has refused the debtors access to the office, lol. The debtors, as part of their lease rejection motion, are asking the bankruptcy court for authorization to enter, collect, and remove their remaining property from the office.

At the time of this writing, the filing is incomplete. We’ll update our readers in due time.

The debtors are represented by Ropes & Gray LLP (Chris Dickerson, Rahmon Brown, Alexys Ogorek, Michael Wheat, Nyle Hussain) and Foley & Lardner LLP (Holland O’Neil, Mark Moore, Zachary Zahn) as legal counsel, and Berkeley Research Group LLC (Kyle Richter, Michael Brown) as CRO and financial advisor. Proposed DIP lender Texas Partners Bank is represented by Norton Rose Fulbright US LLP (Toby Gerber, Kristian Gluck, Jason Blanchard, Michael Berthiaume).

*The TGI Fridays brand and IP are owned by non-debtor TGI Fridays Franchisor LLC (“Franchisor”) “…as a result of a securitization agreement with a separate investor group.” Franchisor has negotiated a transition services agreement with the debtors — which includes interim funding — to maintain support services for franchisees.

**The debtors also have a large international presence due to a robust franchise program. By large we mean 422 franchised restaurants spread out among 56 franchisees in 41 countries. None of the franchised locations are debtors.

***Among the proposed rejected leases is the TGI Friday’s located in Times Square, NYC. You know you’ve been there, don’t front.

⚡️Update: TGI Friday's Inc.⚡️

On November 2, 2024, Dallas-based casual dining chain TGI Friday’s Inc. and 22 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the Northern District of Texas (Judge Jernigan). For some reason it took nearly a full 48 hours for the debtors to complete the filing of their “first day” papers, so our initial coverage only skimmed the surface. Now that the filing is complete, let’s take a look — in as lazy a fashion imaginable given that we’re drinking while watching election results pour in — to see if there’s anything particularly interesting to note ⬇️.

📍Footprint. Other places around the globe cherish Fridays more than we do here in the US:

“For the 52 weeks ending on December 25, 2023, the Company generated global restaurant sales of $1.4 billion. In the same time, the Company generated $62 million in revenue from its asset-light operations in the U.S. and internationally.” We kid, we kid: this is obviously a function of scale.

📍Post-pandemic Operations. The debtors shifted their business considerably in response to the COVID-19 experience. Off-premises sales went from 8% to 25% as the debtors diversified their business towards online and mobile ordering, pick-up, and white-label delivery. The debtors have also been putting franchisees out of their misery, snapping up underperforming or retiring franchisees and, in many cases, closing or assigning them to others. Supply chain issues and inflation also both bit into performance.

📍Gift Cards. This company has … wait for it … nearly $50mm(!) in outstanding customer gift card obligations out there because the cards NEVER expire. Franchisees are concerned that they’re going to be left holding the bag if there’s a rush to restaurants in coming weeks to spend those cards. Per Reuters:

"After hearing the franchisees' concerns at a Monday court hearing in Dallas, U.S. Bankruptcy Judge Stacey Jernigan allowed TGI Fridays to continue its gift card program on an interim basis. The decision allows more time for franchisees to review the gift card program and TGI Fridays' finances before the program is approved for the remainder of the bankruptcy."📍The Franchise Agreements. How much will a TGIF franchise run you in the US? It’s a $50k initial fee followed by a monthly royalty fee of 4% of gross sales plus “a percentage of … net sales to fund marketing and advertising campaigns.”

That 4% sounds rough in an inflationary environment.

As is the mandatory ten year term (with options to renew for two successive five year terms, subject to various terms and conditions).

📍Securitizations. In ‘17, TGI Friday’s Inc. and Citibank NA ($C) entered into a base indenture and management agreement governing a securitization transaction, which included the issuance of two series of notes collateralized by, among other things, the company’s existing and future franchise agreements and existing and future intellectual property. TGI Friday’s Inc. was the manager under the agreements. The securitization entities, including TGI Fridays Franchisor LLC, sacked TGI Friday’s Inc. as manager in early September, due to, among other things, reporting failures. FTI Consulting Inc. ($FCN) has been the back-up manager since.** The company and the securitization entities are now operating pursuant to a transition services agreement which has a number of extensions built in to it which could take it through the end of Q1’25. This termination, however, was impactful. Per the debtors, “As a result of the termination of TGI Friday’s Inc. as Manager, the Company lost a significant portion of its revenue stream as the Company would no longer receive the benefit of the restaurant royalty payments.”

There’s more. The debtors may actually owe up to $30mm to the securitization entities on account of nonpayment of royalties related to both the franchise agreements and IP licenses. This would make the securitization entities the largest unsecured creditors in the cases.

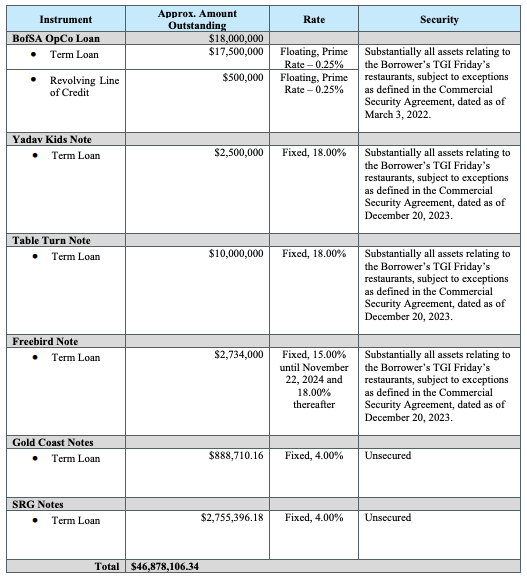

📍Pre-petition Cap Stack. Compounding the lingering effects of the pandemic and the sacking of TGI Friday’s Inc. as manager under the franchise agreements is a dangerous mix of floating rate debt plus insanely high-rate fixed debt. See ⬇️. But much of it, once you get below the Texas Partners Bank (d/b/a The Bank of San Antonio, “BofSA”) component, involves equity sponsor Mr. Anil Yadav, a businessman known in the franchisee space.*

The Yadav Kids Note, the Table Turn Note, and the Freebird Note are all subordinated in right of payment to the BofSA loan.

The debtors cite approximately $51.8mm due to trade creditors, exclusive of employee obligations and customer programs. The top 50 largest general unsecured creditors include a good mix of digital marketing companies and landlords but very few vendors (since many went COD pre-petition).

📍Financing. The debtors have a commitment from Texas Partners Bank for a $23.9mm 10%-interest DIP, comprised of $5.9mm in new money and an $18mm roll-up ($3.3mm of new money and $6.6mm total interim, representing a 1:1 roll-up to new money); they’ll also get to use their lenders’ cash collateral. There’s a 2% commitment fee (1% upfront, 1% at maturity) on the new money portion. The DIP matures in 90 days, subject to certain milestones. At the first day hearing, the UST expressed some concern over the DIP lenders “materially improving” their position by getting super-priority over the assets of certain entities that weren’t original borrowers but those concerns were — despite the restaurants still having “lovely … Tiffany-style lamps” and “buttons and pins” and “flair” — summarily dismissed (Per Judge Jernigan, “I'm not sure any of that is like tremendous new collateral as opposed to the bank already having a lien in the equity.”).

📍Go-forward? The TL;DR is that this is yet another sh*tty sale case and, as of the petition date, there’s no stalking horse purchaser to anchor the process. That said, there were some encouraging signs. Per debtors’ counsel Chris Dickerson of Ropes & Gray LLP:

"...it's envisioned that it will be an approximately 60-day process. As you will note, we do not yet have an investment banker, but we are actively interviewing them and hope to have one in place here this week. That's required, that's a necessary part of our meeting the milestone that requires us to have filed the sale procedures motion within eight days of the petition date, as well as to identify a stalking horse. We have had numerous pre-petition indications of interest in purchasing some or all of the debtors' assets, including one in which we are pretty far down the road and are working to try to bring to the table as a stocking horse bidder. It is our hope that when we do file the sale procedures motion that it will include a stalking horse bidder. As you would expect, in addition to the handful of parties that we had been dealing with prior to the petition date, we have received numerous indications of interest in participating in that process since the filing, and we will, of course, in conjunction with the investment banker that will be hired by the company, subject to your honor's approval, of course, look to involve as many parties as possible so that we can, again, have a value-maximizing process."Man. Hats off to whomever the banker is that jumps into this pressure cooker!

We will update this situation as facts merit.

*Per LinkedIn, Yadav Enterprises is a restaurant franchisee company with 343 restaurants covering six brands; Jack in the Box, Denny’s, El Pollo Loco, Corner Bakery Cafe, Sizzler and TGI Friday’s. These restaurants are operated throughout Northern California, Texas and six Midwest states.

**FTI is represented by Kramer Levin Naftalis & Frankel LLP (Alexander Woolverton, Andrew Pollack, Kelly Porcelli) and Munsch Hardt Kopf & Harr PC (Deborah Perry).

Company Professionals:

Legal: Ropes & Gray LLP (Chris Dickerson, Rahmon Brown, Alexys Ogorek, Michael Wheat, Nyle Hussain) and Foley & Lardner LLP (Holland O’Neil, Mark Moore, Zachary Zahn)

Independent Manager: Alexander Matina

Financial Advisor/CRO: Berkeley Research Group LLC (Kyle Richter, Michael Brown)

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

Servicer + Control Party: Midland Loan Services, a division of PNC Bank NA

Legal: Sheppard Mullin Richter & Hampton LLP (Dwight Francis, Alexandria Lattner, Alan Feld, Ted Cohen, Shadi Farzan, Caroline Sischo) and Eversheds Sutherland US LLP (David Wender)

DIP Lender: Texas Partners Bank

Legal: Norton Rose Fulbright US LLP (Toby Gerber, Kristian Gluck, Jason Blanchard, Michael Berthiaume)

Financial Advisor: CR3 Partners

Backup Manager for TGIF SPV Guarantor LLC, TGIF Funding LLC, TGI Fridays Franchisor LLC: FTI Consulting Inc.

Legal: Kramer Levin Naftalis & Frankel LLP (Alexander Woolverton, Andrew Pollack, Kelly Porcelli) and Munsch Hardt Kopf & Harr PC (Deborah Perry)

Official Committee of Unsecured Creditors

Legal: Pachulski Stang Ziehl & Jones LLP (Michael Warner, Theodore Heckel, Bradford Sandler, Robert Feinstein)