✈️New Chapter 11 BK - Spirit Airlines Inc. ($SAVE)✈️

Emergency landing in chapter 11 with a comprehensive balance sheet restructuring.

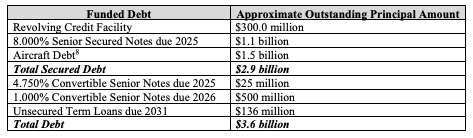

On November 18, 2024, FL-based Spirit Airlines Inc. ($SAVE) filed a prearranged chapter 11 case in the Southern District of New York (Judge Lane) to address its $3.6b of aggregate funded debt:

The downfall of this beloved carrier (🖕) sparked cries across the internet:

Hell, there’s even a letter sent to the court bemoaning the Spirit experience:

“The debtor is very well known to have a years long practice of offering the worst customer service in the nation. Now, they want to use the courts to get relief from their debts and obligations that are a direct result of management and its employees treating the American traveling public with less dignity and respect. Cattle in 19th Century Chicago Stockyards were treated better.”This emergency landing in chapter 11 stings just a little more when looking at the debtors’ previous suitors, JetBlue Airways Corporation ($JBLU) and Frontier Group Holdings Inc ($ULCC), both of whom are up YoY:

We went over the merger struggles and operational issues in our previous coverage here…

… so let’s dive straight into what this deal is and what it isn’t ⬇️.

We’ll go in reverse order. This is NOT a major operational restructuring. While SAVE is going forward with a sale of 23 aircraft to rationalize its fleet and better position its go-forward business plan for success, priority claimants and general unsecured claimants will be, if all goes according to plan, paid in full or remain unimpaired.

Debtors’ counsel, Davis Polk & Wardwell LLP (“Davis Polk”), would also have you believe, this is NOT a bankruptcy proceeding. Lol no seriously.

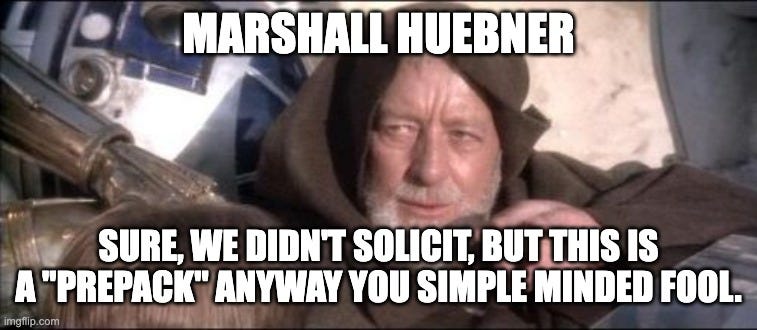

Here’s Marshall Huebner in his opening remarks:

“Your honor, obviously obviously I am aware that Spirit is in chapter 11. I actually signed the petition, but it is also true that in some ways Spirit is not really in chapter 11. As you'll hear in a few minutes, many foreign systems would actually allow the effectuation of what we filed these proceedings to undertake without proceedings that are known as or called bankruptcy proceedings.”He continues throughout the hearing:

“This is a very streamlined, very simplified bankruptcy case that we expect to move on very quickly. As I noted before, Your Honor, in many countries in Europe, for example, this would not be a bankruptcy.”“Apparently, it's unfortunate that at least as of now, although the law continues to develop, the word bankruptcy really has to be anywhere in spirits of storyline.”

Lol, for someone trying to convince the masses (creditors/customers) this “isn’t a bankruptcy” Mr. Huebner sure used the word “bankruptcy” a lot.

Anyway, there was a “bankruptcy petition” that got filed so verbal gymnastics aside, this is a bankruptcy, and it comes in the form of a major balance sheet restructuring.

And further, this IS (kinda) a prepack! Again, here’s Mr. Huebner:

“Candidly, this is analytically a prepack. It is technically true that we did not solicit under applicable non-bankruptcy law, so we will need to do a plan and disclosure statement. When you look at all the ethoses that underlie the prepack guidelines, I think we actually satisfy all of them in spades.”LOL, what the actual f*ck?

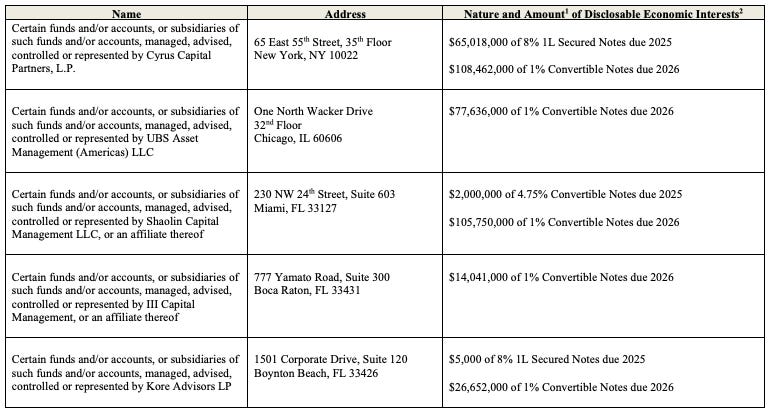

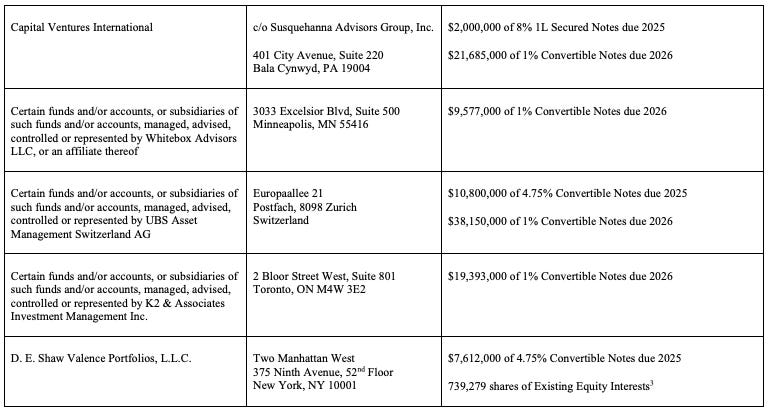

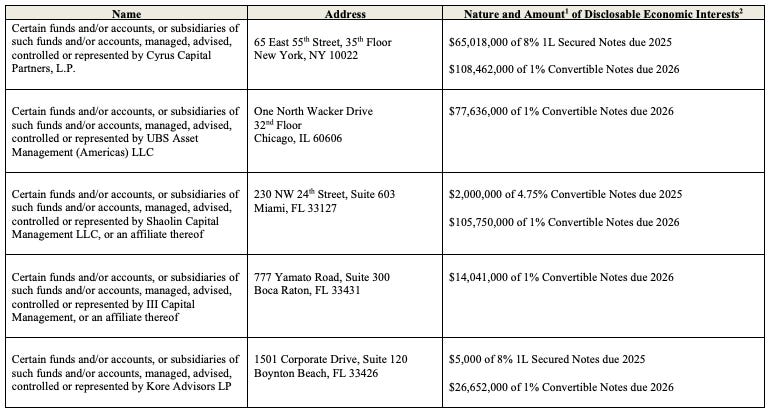

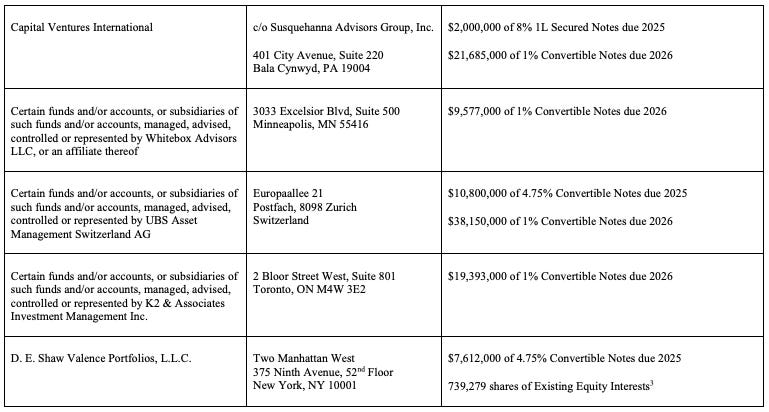

The debtors secured the support of two ad hoc groups via a restructuring support agreement (the “RSA”). Ad hoc group number 1 consists of holders of ~72.6% of the $1.1b of senior secured notes. Ad hoc group number 2 includes holders of ~81.3% of the ‘25 convertible notes and ~84.3% of the ‘26 convertible notes (together totaling $525mm).

Okay so what’s this yet-to-be solicited plan?

First, the new equity interests. Who are the proud new owners of revamped Spirit?

In short: the prepetition senior secured noteholders. They’ll be receiving 76% of the new equity interests with the remaining 24% going to the convertible noteholders. This is subject to dilution from a $350mm equity rights offering (the “ERO”)(and a management incentive plan).

Secured noteholders are being allocated 78.75% of the new equity interests issued via the ERO while convertible noteholders will be given the remaining 21.25%. The ERO is fully backstopped by the two ad hoc groups and in exchange for their support, the backstop parties will be granted holdbacks on the ERO and a backstop premium.*

Reorganized Spirit will also be emerging with $840mm in exit secured notes. The notes carry a 11%/12% interest rate and are due 2030.** $700mm of these notes will be distributed to the senior secured noteholders with the remaining $140mm going to the convertible noteholders.

If you crunch the numbers, that’s a $795mm debt reduction.

And to accomplish all of this the debtors will rely on its $800mm cash balance. Now that might look like a massive cash balance and more than enough to get the debtors to emergence. BUT, we once again direct your attention — as we did in our prior coverage —to the debtors’ credit card processor. Here are the debtors in their DIP motion:

“[T]he Debtors’ agreement with its largest credit card processor results in hundreds of millions of dollars of chargeback exposure at any given time and requires significant minimum liquidity reserves in the ordinary course of business.”So good you have to say it twice. Further down in the same paragraph:

“For example, the Debtors’ agreement with its largest credit card processor results in hundreds of millions of dollars of chargeback exposure at any given time and requires significant minimum liquidity reserves in the ordinary course of business.”Repeat sentence guys …

So yes, there is a DIP. It’s $300mm large, extended by certain creditors party to the RSA, and fronted by Barclays Bank PLC ($BARC). The DIP carries a S+7% (or ABR+6%) interest rate and while there isn’t a commitment fee, there is a 3% ($9mm) put option premium payable on closing.***

The debtors don’t need immediate access to the new money so only the debtors only pushed through the commitment letter (and adequate protection) during the first day hearing (this includes the put option premium).

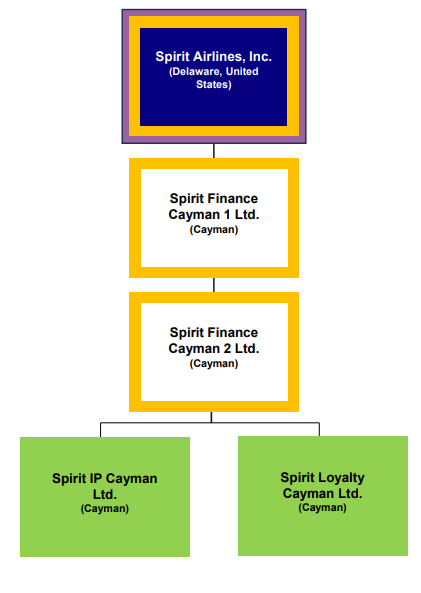

At this point maybe you’ve noticed that we’ve used “debtors” (note the plural) instead of “debtor” even though, currently, there’s just one debtor entity. That’s because there are four remaining entities that have not yet filed — but will soon, if all goes well.

The four subsidiaries you see in the org chart above were created in ‘20 for the purpose of raising new capital. That new capital ended up being the senior secured notes, which are collateralized by the only assets of (likely) any real value here: the debtors’ loyalty programs and IP.**** All four subsidiaries are structured as bankruptcy-remote SPVs and well, apparently it’s very hard to un-SPV an SPV.

Here’s Mr. Huebner during the first day hearing:

“So it turns out, live and learn, that even with the consent of virtually every single party, an overwhelming majority that has the authority to direct a trustee, it actually takes a whole bunch of time and work to un-SPV an SPV.”The delay in solicitation — and the projected emergence in late Q1’25 — are driven by the need to un-SPV these critical entities.

And so, indeed, you live and you learn. You liven and learn not to treat your customers worse than “cattle in 19th century Chicago stockyards” and maybe you’ll have heaps of revenue, the ability to service your debt, and no need to “un-SPV an SPV” in …

… DON’T … YOU … DARE … SAY … IT …

The debtors are represented by the aforementioned Davis Polk (Marshall Huebner, Darren Klein, Christopher Robertson, Moshe Melcer, Kayleigh Yerdon, Sihui Ma) as lead counsel, and Debevoise & Plimpton LLP (Jasmine Ball, Elie Worenklein), O’Melveny & Myers LLP and Morris Nichols Arsht & Tunnell LLP as various supporting legal counsel, Alvarez & Marsal LLC is SAVE’s financial advisor, and Perella Weinberg Partners LP (Bruce Mendelsohn) is its investment banker. Ad hoc group 1 is represented by Akin Gump Strauss Hauer & Feld LLP (Michael Stamer, Abid Qureshi, Jason Rubin, Kevin Zuzolo, Blaine Scott) as legal counsel and Evercore Group LLC ($EVR) as financial advisor. And ad hoc group 2 is represented by Paul Hastings LLP (Matthew Warren, Geoffrey King, William Reily, Valerie Eliasen) as legal counsel and Ducera Partners LLC as financial advisor.

*Holdback amounts are subject to an RSA participation threshold (90%). If the threshold is met, the senior secured holdback amount would be $27.6mm and the convertible holdback amount would be $7.4mm. If the threshold is not met, the senior secured holdback amount would be $137.8mm and the convertible holdback amount would be $37.2mm. Backstop parties will be able to purchase their backstop commitment at a 30% discount to plan equity value. There’s also a backstop premium equal to 4.9% of the total shares outstanding for senior secured backstop parties and 1.3% of the total shares outstanding for convertible backstop parties.

**At issuer’s option, payable either at 11% fully in cash or 8% cash and 4% PIK.

***Economics here, economics there, economics everywhere. Management might as well get in on the party. Per CFODive:

Just days ahead of its bankruptcy filing Monday, Spirit Airlines’ board approved $5.4 million in total one-time cash retention awards to five named executive officers, according to a Securities and Exchange filing. The Nov. 12 agreement stipulated the executives must pay the money back if they are no longer employed by Spirit in “good standing” one year after the effective date.

The highest-value retention bonuses are teed up for CEO and President Edward Christie III, at $3.8 million; COO John Bendoraitis at $850,000, and CIO Rocky Wiggins, who is to receive $300,000, according to the filing. CFO Frederick Cromer will get $175,000, the smallest sum of the group.

LOL, the poor CFO getting trolled by a pub called CFODive … harsh!

****The issuers subsequently redeemed $340mm of the senior secured notes in ‘21 and issued an additional $600mm in ‘22.

Company Professionals:

Legal: Davis Polk & Wardwell LLP (Marshall Huebner, Darren Klein, Christopher Robertson, Moshe Melcer, Kayleigh Yerdon, Sihui Ma)

Fleet Legal: Debevoise & Plimpton LLP (Jasmine Ball, Elie Worenklein)

Labor Legal: O’Melveny & Myers LLP

Conflicts Legal: Morris Nichols Arsht & Tunnell LLP

Financial Advisor: Alvarez & Marsal LLC

Investment Banker: Perella Weinberg Partners LP (Bruce Mendelsohn)

Claims Agent: Epiq (Click here for free docket access)

Other Parties in Interest:

RCF Administrative Agent: Citibank NA

DIP Agent: Wilmington Savings Fund Society FSB

Legal: Schulte Roth & Zabel LLP (Adam Harris, Reuben Dizengoff, Douglas Mintz)

Ad Hoc Group of Certain 8% ‘25 Senior Secured Noteholders

Legal: Akin Gump Strauss Hauer & Feld LLP (Michael Stamer, Abid Qureshi, Jason Rubin, Kevin Zuzolo, Blaine Scott)

Financial Advisor: Evercore Group LLC

Ad Hoc Group of 4.75% ‘25 + 1% ‘26 Convertible Noteholders

Source: Docket 36 Legal: Paul Hastings LLP (Matthew Warren, Geoffrey King, William Reily, Valerie Eliasen)

Financial Advisor: Ducera Partners LLC