⚡️Solar Coaster⚡️

⚡️Solar Coaster⚡️

Solar companies have been keeping bankruptcy courts busy.

⚡️Update: SunPower Corporation⚡️

You’ll recall that Richmond, CA-based SunPower Corp. ($SPWR) and 9 affiliates (collectively, the “debtors”) filed chapter 11 cases in the District of Delaware (Judge Goldblatt) back on August 5, 2024. We covered the filing here:

In a nutshell, accounting irregularities + a downturn in the solar industry = sh*tco solar company in bankruptcy. The debtors were relying on $18.2mm of cash collateral (as well as the sale of $11.9mm of solar loans) to finance the cases that featured an opening $45mm stalking horse bid from Complete Solaria Inc. ($CSLR).

On September 6, 2024, the debtors filed the first draft of a disclosure statement. Then, on September 16, 2024, the debtors announced Complete Solaria’s stalking horse bid as the winner. Complete Solaria will be paying $45mm in cash and assume ~$51mm of liabilities.* Additionally, on September 17, the debtors announced the sale of its membership interest in the debtors’ financing business, SunStrong Capital Holdings, LLC, and certain loans and leases to HA Sustainable Infrastructure Capital Inc. ($HASI) and GoodFinch LLC for $11.5mm in cash.**

But, there were issues. First, the Securities and Exchange Commission (the “SEC”), the United States Trustee (the “UST”), and the lead plaintiff in a securities class action against the debtors all objected to the disclosure statement.*** The objections all shared a common theme: third party releases! The Purdue Pharma decision still weighs on us heavily.

Second, Maxeon Solar Technologies, Ltd. ($MAXN) objected to the Complete Solaria sale. Who? Maxeon is a designer and manufacturer of solar panels that was spun off from the debtors in ‘20. As part of that spin-off, the parties agreed to divide ownership of the “SUNPOWER” brand. This was done through a "Brand Framework Agreement” (see Exhibit A here). Under the agreement, there were several provisions that restricted each parties ability to sell, abandon, or discontinue the SunPower trademarks. Here’s an example of the restriction of sale provision:

And here’s Maxeon in their objection:

“Consistent with general principles of federal trademark law, the Debtors’ and Maxeon’s respective rights to the SunPower Marks (defined herein) were governed by the principle of “use it or lose it.” Each party agreed to “take commercially reasonable actions to avoid an event or circumstance that would be reasonably foreseen to result in a meaningful loss of rights” with respect to the SunPower Marks, and upon either party’s discontinuation or abandonment of the marks, the other would have a right of first refusal to acquire the brand for no additional consideration.”

So when the Complete Solaria sale included the debtors’ IP and trademarks, Maxeon was like:

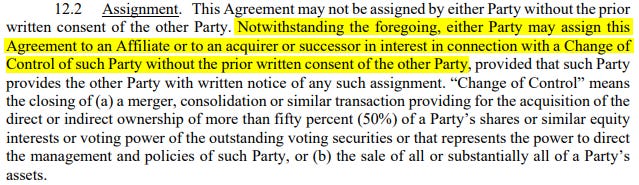

But here’s section 12.2 of that same Brand Framework Agreement:

Aha, change of control! A stalking horse sale surely qualifies, right?

We got our answer during a September 23 hearing on provisional interim approval of the disclosure statement, approval of the SunStrong sale, and approval of the Complete Solaria sale.

The hearing lasted close to four hours but he third party releases were dealt with within the first forty minutes. Here’s Judge Goldblatt:

“Look, the safest thing to do if one - because this is expressly interim approval, and no one is saying that the approval of the procedures should have preclusive effect - if the parties want to go forward in the face of uncertainty with an opt-out form, I’m not stopping you but nor is the approval going to preclude someone from coming in later and saying that form of release is inappropriate.”

“All I can tell you is that the safest thing to do would be an opt-in form.”

Basically the issue is kicked to confirmation but the post-Purdue writing is on the wall.

As for the remaining three+ hours? The parties spent that time debating Maxeon’s objection, touching on section 365 of the bankruptcy code (adequate assurance), property interests, executory obligations, and more. Exciting stuff!

Not so much, 😴. Thankfully Judge Kaplan put an end to the misery. Relying on the previously highlighted section 12.2 of the Brand Framework Agreement, he sided with the debtors and overruled Maxeon’s objection. And thus the path to confirmation is clear(er); a hearing is scheduled for October 18 at 2:30pm ET.

*The assumed liabilities number comes from the declaration of Moelis & Company LLC’s Rick Polhemus.

**SunStrong was formed as a joint venture between SunPower and HASI with interests in several non-debtor affiliates that hold solar leases/loans.

***The securities class action is Piotr Jaszczyszyn, Individually and on Behalf of All Others Similarly Situated v. SunPower Corp. et al., Case No. 3:22-cv-00956-AMO in the United States District Court for the Northern District of California.

⚡️Update: iSun Inc.⚡️

You’ll recall that back in early June, VT-based iSun Inc. ($ISUN) and eleven affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Horan). The “solar energy services and infrastructure deployment company” was a money incinerator and after pre-petition strategic alternatives failed, the debtors ended up in bankruptcy with a $4mm consensual priming DIP ($3mm new money, $1mm roll-up of a bridge; later upsized to $5mm) and a stalking horse bid, both from a company called Clean Royalties LLC (“CR”). We covered the filing here:

Unfortunately the actual bid wasn’t disclosed at the time of the filing but we learned shortly thereafter that CR’s bid consisted of a $10mm credit bid plus the assumption of certain assumed liabilities. No other bidders emerged to challenge CR and the debtors therefore designated CR the “successful bidder” in late July. The sale closed in late August.

This unfortunate sale result left the primed pre-petition secured lender, Decathlon Growth Credit LLC, with a $9.5mm claim. That (deficiency) claim is dealt with pursuant to a recently proposed/filed plan of liquidation in which a trust will be funded with a $350k carveout from sale proceeds (unless expended pre-confirmation on plan-related pro fees, lol). The trust’s assets include certain litigation claims, certain remaining Article 5 causes of actions, some dirty tissues and used toilet paper. Decathlon will get the first 25% of any trust distributions up until the $350k is repaid to Decathlon and from there it will share pro rata with other trust beneficiaries, including general unsecured creditors. As you might’ve guessed, holders of the public equity — equity issued in connection with a ‘20-era deSPAC — will get a big fat 🍩.

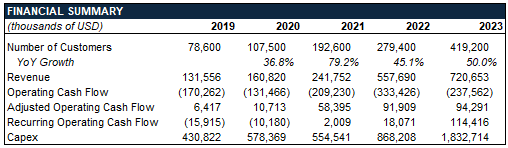

Someone ought to put this chart on iSun’s tombstone:

⏩One To Watch: Sunnova Energy International Inc ($NOVA)⏩

Concepts like “energy independence,” “energy security,” and “energy transition” have been quite topical these days when it comes to national news — in the context of, among other things, geopolitics and global warming. Yes, this is serious stuff. How might you do your part at home?

Well, you, like our very own Johnny, might’ve already had the pleasure of dealing with a door-to-door solar salesman from the likes of Houston-based Sunnova Energy International Inc. ($NOVA), an energy services company that specializes in residential solar. NOVA generates revenue by entering into purchase power agreements (“PPA”), lease agreements, and loans with its customers — though, NOVA would be just as happy to take that hard-earned cash if you wanted to fork it over.

The company partners with local dealers and contractors who sell and perform installation of NOVA roof solar panels. Because NOVA does not have a large direct sales force, this model should lower its SG&A costs.

Before we go any further, you might be wondering: “what the h*ll is a purchase power agreement?”

Great, let’s dive into some solar panel economics.

By all accounts, residential solar is cheaper to install than say 10 years ago:

But, that doesn’t mean it’s not a significant capital investment. At a cost of $4/watt, an 8k kW system would run you $32k — almost the same price as a new Tesla Inc. ($TSLA) car. And you can’t really show off a solar panel as much as you can a Tesla.

The solar companies, however, know this. They’ve figured out ways of reducing the upfront costs shouldered by the customer through PPAs, leasing agreements, and loans.

Under a PPA, the customer pays NOVA for the energy generated from the solar system ($/kWh) and a lease is a fixed monthly payment for the privilege of using the system. Both have terms that typically last 20-25 years and since both leave ownership of the system with NOVA, the customer does not get the tax credit benefits associated with the installation.

If a customer is keen on owning the system, they can choose to pay cash or enter into a 10/15/25 years loan with the company instead. Approximately 24% of customers had lease agreements, 24% had PPAs, 37% had loan agreements and 12% had service plan agreements as of December 31, 2023.

And so through these offerings, the initial capital burden gets shifted from the customer to NOVA. Great, but where does this capital come from?

The company funds these installations through two main avenues: tax equity funds and non-recourse solar asset/loan-backed notes.

The company co-invests alongside tax equity investors through partnership flips to fund new installations. Tax equity investors can then benefit from the investment tax credits (“ITCs”) associated with the installation.

NOVA also securitizes customer agreements (loans), as well as the associated assets, and issues secured non-recourse notes.

So if you’re reading all this and thinking “long term leases/loans financed by co-invest and loans. Is this just a spread business?” then ding ding ding, bingo!

It’s a spread business that also webs in all the intricacies of renewable energy credits/incentives:

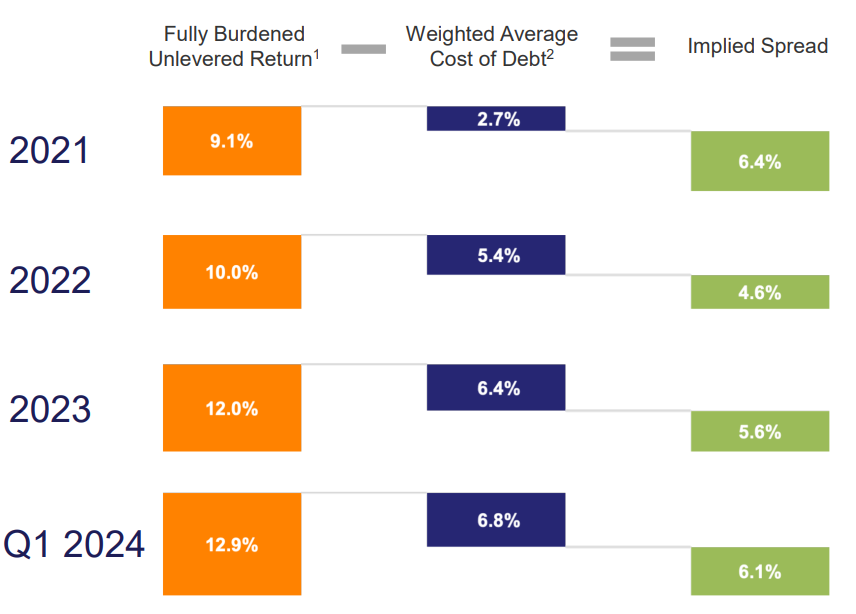

You can see from the above that a rising interest rate environment has significantly impacted the company’s spread.

As of March 31, 2024, the company had an estimated gross contracted customer value of $9.5b at a 6% discount rate.

And credit where credit is due, the company has seen consistent growth:

But cash flow is the issue here given the large capital outlay required to fund the projects and the rising cost of debt.

Which brings us to the rather grotesque capital structure due to all the special purpose entities and asset-backed notes. There’s ~$7.8b of debt on the BS including ~$1b due ‘26.* The 0.25% $575mm convertibles due ‘26 were last trading at ~75c on the dollar and a 14.2% yield according to FINRA (both improvements in recent weeks, btw). The stock is down 32% YTD:

The company has already reportedly brought on Moelis & Co ($MC) to pursue potential transactions given the distressed trading levels. Can you say “liability management”?

And 1Q’24 results didn’t leave much room for optimism. The company missed on revenue while also lowering FY’24 guidance for customer additions from a midpoint of 190k to 145k. Makes sense as a “higher for longer” rate environment kills a lot of demand from customers who have to look to rely on more expensive financing options to purchase their solar system. Residential solar is expected to decline by 13% in ‘24 according to the Solar Energy Industries Association.

Buuut 2Q’24 results were released on July 31, and well … the stock is up 42.9% since then. The company significantly adjusted their cash generation forecast upwards due to higher than expected impact from ITC adders (thank you IRA).** However, customer additions guidance for FY’24 was, once again, revised downwards to a midpoint of 115k from 145k.

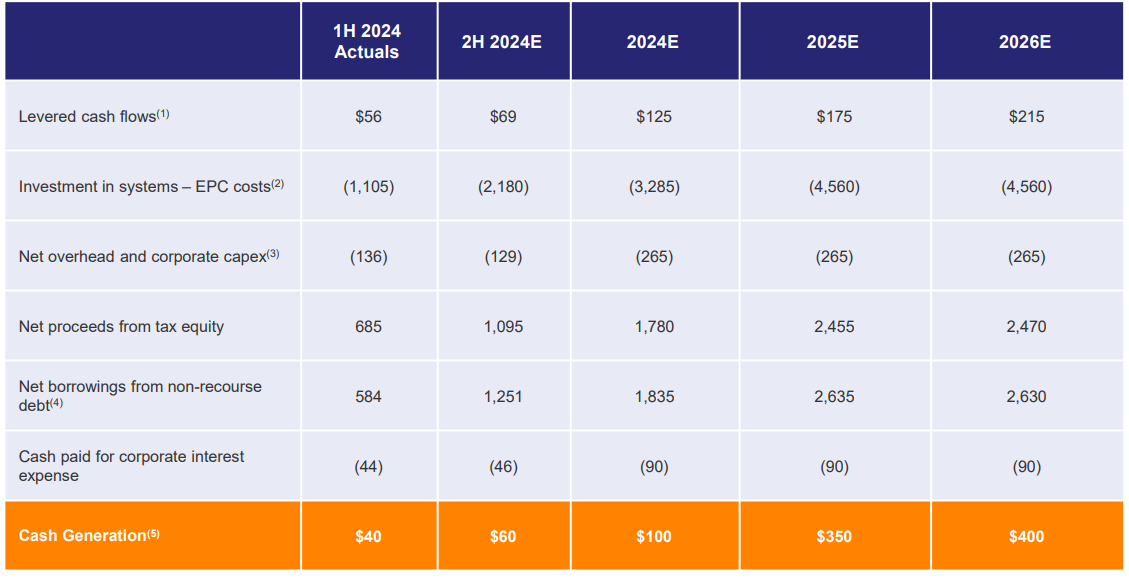

But cash is king and the company had $630.4mm in greenback, of which $253.2mm was unrestricted, and $1b in borrowing capacity as of June 30, 2024. And future liquidity is expected to look like this:

Aka, as always, cash is heavily dependent on access to tax equity investments and non-recourse debt.

The company also secured a $3b loan guarantee with the US Department of Energy (“DOE”) back in September ‘23, of which $168.9mm appears to have been put to use. Unfortunately, this was quickly followed by a probe from Congressional Republicans who accused the company of “troubling sales practices” and favorable treatment from the DOE.

Those “troubling sales practices” allegedly included scamming dementia patients into signing 6 figure leases. Because nobody needs a 25 year solar panel lease more than an 86 year old on their deathbed, 😬.

We’ll keep y’all updated on whether NOVA also ends up on its own deathbed.

*****

Speaking of reeling solar companies, back in July, SolarEdge Technologies Inc. ($SEDG) — an Israeli solar company with a meaningful presence in the United States — announced that it was laying off 400 people, about 7% of its workforce (half of which would affect Israelis already reeling from a war-depressed economy). The company indicated that while things look relatively promising in North America versus Europe, it is nevertheless contending with “excess inventory.” The company was also affected by the chapter 7 bankruptcy filing of a a major customer, PM&M Electric, a solar panel installer in Arizona, which left the company with a $11.4mm claim. All told, SEDG has had a whopper of a year: its stock is down nearly 77% YTD.

*The company also issued an additional $230.9mm in loan backed notes on June 28, 2024. We’re still waiting for that LME Moelis….

**ITC adders are essentially additional credits that can be “added” by meeting certain criteria like using domestic material.

💥New Chapter 11 Bankruptcy - Lumio Holdings Inc.💥

Okay, maybe not so “new” but cut us some slack.

On September 3, 2024, Utah-based Lumio Holdings Inc. and one affiliate (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Stickles) — the second residential solar company of the year (see also Sunpower Corp.)!

As you can imagine, in a world of higher interest rates, people just aren’t willing to shell out tens of thousands of dollars on solar panels — a situation we also just covered above with respect to Sunnova Energy International Inc. ($NOVA). Pair all of the macro headwinds with $300mm of prepetition debt and …

After failed efforts for an out-of-court transaction — efforts that were bogged down by a pesky requirement that any potential purchaser of the business be already licensed for solar panel installation — the debtors commenced preparations for a chapter 11 process in early August. It took a month but ultimately the debtors landed in bankruptcy court with their prepetition secured term loan lender, White Oak Global Advisors LLC (“White Oak”), committed to a $8mm DIP that is roll-up free! Wow, when was the last time we got a DIP without a roll-up???

The DIP is also interest free!

Haha, no, we’re just joking. Keep dreaming.

The DIP carries an interest rate of SOFR+900bps and a 4% upfront premium fee. $4mm of the $8mm new money will be available upon entry of an interim order.

The DIP milestones include a bid deadline of October 7, 2024, an auction date of October 9, 2024, and a sale hearing date by October 14, 2024.

Additionally, White Oak is also acting as stalking horse purchaser for substantially all of the debtors assets with a $100mm credit bid plus the assumption of certain liabilities.*

Interestingly, in a great example of how interconnected the solar industry seems to be, the debtors also owe Sunnova $2.1b in obligations related to prebates. Wait, what? Prebates? What are these prebates?

If a residential customer of the debtors required financing services, Sunnova stepped in and provided them, acting as a financing partner (“FinCo”). In exchange for doing all the installation work and the general operating expenses of the debtors, the FinCos would advance prebates to the debtors, as an incentive for Lumio to herd them more customers in need of financing. However, if certain volume requirements were not met, the FinCos (in this case, Sunnova), were entitled to repayment of these prebates.

Outside of Sunnova, the debtors also owe $2.5mm to Solar Mosaic LLC and $4.8mm to Palmetto Solar LLC due to repayment on prebates. These prebates are all treated as unsecured obligations, but we do wonder, as one domino falls, does this ripple through the rest of the residential solar industry? The answer to that question remains open but we do know that Solar Mosaic LLC and Sunnova aren’t going quietly into the night: the United States Trustee (“UST”) appointed both to the official committee of unsecured creditors (“UCC”) in the cases.

So what’s next for these cases? The debtors hope to get authority to enter into the White Oak stalking horse agreement and approval of their proposed bidding procedures. The hearing on that motion was originally scheduled for September 17, 2024 but it kicked to later today, September 25, 2024, at 2:30pm ET after the UST filed an objection expressing some concerns:

First, the U.S. Trustee objects to the Debtors’ request to provide an uncapped Expense Reimbursement to the Stalking Horse Bidder, an entity affiliated with the Pre-Petition Lender Representative, the Pre-Petition Agent (as successor) and the DIP Agent/Lender, White Oak Global Advisors LLC (“White Oak”), because the proposed bid protection is not an “actual, necessary cost [or] expense of preserving the estate” under 11 U.S.C. § 503(b)(1)(A). Second, if allowed, payment of an expense reimbursement to a qualified bidder in connection with a bankruptcy sale process upon the occurrence of conditions other than the closing of a superior alternative transaction is not permitted. Third, White Oak should not be permitted to serve as a Consultation Party while their affiliated Stalking Horse Bidder is still actively bidding.

We will keep you updated if anything of particular note transpires at the hearing.

The debtors are represented by Morris, Nichols, Arsht & Tunnell LLP (Robert Dehney Sr., Matthew Harvey, Matthew Talmo, Scott Jones, Erin Williamson) as legal counsel, Houlihan Lokey Capital Inc as investment banker, and VRS Restructuring Services LLC (Jeffrey Varsalone) as financial advisor. White Oak is represented by Davis Polk & Wardell LLP (Darren Klein, Joanna McDonald) and Richards, Layton & Finger, P.A. (Mark Collins, Amanda Steele, James McCauley) as legal counsel. The UCC is represented by Porzio Bromberg & Newman PC (Cheryl Santaniello, Warren Martin Jr., Kelly Curtin, Rachel Parisi, Christopher Mazza).

*White Oaks is the sole secured lender and holds ~$248mm of prepetition secured term loans.

📤 Notice📤

Charles Persons (Partner) joined the ever-expanding Paul Hastings LLP from Sidley Austin LLP.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.