💥Another Failed Liability Management Exercise. Part II (Serta Simmons).💥

💥Another Failed Liability Management Exercise. Part II (Serta Simmons).💥

Also: Voyager Digital Crushes Spirits and Corner Bakery is baking some drama.

As we discussed in our previous coverage, Serta Simmons Bedding LLC (“SSB”) is well-known for a ‘20-vintage liability management exercise featuring a then-novel “uptier” exchange transaction that provided it with a $200mm new money infusion while providing certain (and only certain) participating lenders new super-priority status for the $200mm of new money (“FLFO”) plus super-priority status for a roll-up of existing first lien term loans into new first lien second out paper (“FLSO”). Impressively, SSB also got an appreciable discount on the roll-up exchange (26% for the legacy first lien and 61% for the second lien), all of which had the effect of providing SSB with additional liquidity while also deleveraging the balance sheet.

Of course, this transaction left behind first lien term lenders who held over $800mm of the paper who suddenly found themselves way down in priority. It also left them pissed off AF. But they were pissed off for different reasons than those who got J.Screwed in J.Crew, because the company didn’t do the whole “dropdown” dance wherein it moved certain intellectual property collateral into an unrestricted subsidiary for the purpose of issuing new, effectively super-priority, secured debt (see also Revlon Inc.). Rather, here the company — aided and abetted by certain lenders and its sponsor — just took an aggressive stance vis-a-vis the credit docs and unleashed some … ⚡️wait for it⚡️ violence!!

Ok, maybe not “them all,” just the non-participating lenders.

Here, courtesy of S&P Global Ratings, is what this drama looked like:

At the end of the day, however, SSB ended up filing for bankruptcy anyway — just like J.Crew and Revlon before it — and so all of that complex sh*t represented above merely, as we stated previously, “…had the effect of ‘managing’ the debtors’ ‘liability’ for all of two frikken years. The bankruptcy papers repeat over and over how, without this transaction, the debtors likely would have ended up in bankruptcy sooner, as if they’re proud of their zombie-like status over the last two years. Specifically, they highlight how the deal reduced the debtors’ debt by $400mm, lowered all-in interest expense, and increased cash to over $300mm. In other words, the debtors bought two years, the priority lenders who participated in the exclusionary deal (discussed more below) got super-priority status and additional collateral and the company’s sponsor, Advent International, got to play out an option!”

Back when SSB filed, we previewed some of the legal issues that were likely to dominate the debtors’ adversary proceeding concerning the legitimacy of the ‘20 uptier. One big issue: whether Judge Jones (of the Bankruptcy Court for the Southern District of Texas) would rule on the transaction or leave it to Judge Faila of the Southern District of New York who, following some speedy legal maneuvering by the non-participating lenders, found herself presiding over the creditor-on-creditor claims.1

(PETITION Note: we’re truncating this line of thought for space but, based on a not-so-scary DIP budget and $160mm initial cash balance, it’s not *immediately* clear that SSB was in imminent financial distress when it filed. It does seem, however, that SSB’s officers and advisors were imminently about to give depositions in the pending S.D.N.Y. action.).

Spoiler: it’s Judge Jones, who signed an order last week extending a temporary stay to the S.D.N.Y. action. That’s big news, and it means we might be on a fast track to a final uptier ruling. With SSB’s confirmation hearing already scheduled for May 8th (in what seems to be a relatively quiet chapter 11 case), we’d imagine the Court will want to get this wrapped up soon. The summary judgment hearing is today, March 28th!

See, going all the way back at a January 27th scheduling conference, Judge Jones signaled that he not only felt like the bankruptcy case was the proper venue to resolve the creditor-on-creditor claims, but also a view that the legality of the uptier is a “simple” contract issue which may be resolvable without significant discovery or trial.

“I know that one court has said that they thought there was an ambiguity. I’ve read that specific provision, and I’m going to respectfully disagree… I don’t find it ambiguous at all. I’ve lived in that world – I don’t find it difficult at all.”

(PETITION Note: Judge Jones appeared to reiterate this view in the March 13th hearing regarding extension of the automatic stay to the S.D.N.Y. action.).

This is a major departure from the New York courts, which have so far unanimously found the contract terms to be ambiguous. A finding of ambiguity at the summary judgment phase makes the legitimacy of the uptier a trial issue and, indeed, each of the uptier lawsuits, including the one against SSB, has languished for years pending trial in New York court.2 Nevertheless, Judge Jones appears comfortable drawing on his own professional experience (and presumably some Texas gumption) to chart his own course, a path which drew a mild rebuke from Reorg, of all sources:

We also can’t endorse Judge Jones’ casual rejection of Judge Failla’s prior decision on the open-market exchange issue, or his repeated insistence that the matter is ripe for summary judgment before anyone has filed a motion. Maybe Houston Judge Jones should take a hint from New York Judge Jones’ [sic] more even-handed handling of the Revlon unrestricted asset transfer transaction litigation.

Citing nonbankruptcy precedent for moving quickly in bankruptcy — we want New York Judge Jones to be our valentine. By pushing for a tough schedule without suggesting any prejudgment, the New York judge left the parties’ relative leverage unscathed, whereas Houston Judge Jones handed a gift to the Serta debtors that might discourage them from being more reasonable in negotiations. (emphasis in original).

(PETITION Note: But it might encourage more cases with a creditor-on-creditor feature to file in the SDTX!)

Assuming Judge Jones sticks to that line of thought, this would mark the first final ruling in an uptier case, and the precedent that Judge Jones sets could significantly influence market practice over the next several years. While a ruling in the Southern District of Texas is not binding with respect to New York contract law (and, of course, every credit agreement is different), the next uptier case in New York (Boardriders) is quite a ways away from resolution, assuming it doesn’t settle. If Judge Jones ratifies SSB’s actions, distressed borrowers and their advisors will be eager to exploit the newfound justification and engage in aggressive recapitalizations (and, it bears repeating, use the SDTX if things go south and bankruptcy occurs anyway). If Judge Jones instead decides that the transaction was an unambiguous violation of the credit agreement, we may see lenders and administrative agents hesitate to undertake similar transactions in the future.3

At this point, we’ve seen summary judgment briefs and supporting materials from each of the parties. As we noted in our initial coverage, the key issue is the “open market purchase” exception to the rule requiring pro-rata payments to each lender.4

Before we begin, here’s a great interview with Gibson, Dunn & Crutcher LLP’s Scott Greenberg and Steve Domanowski, the lawyers who helped engineer the transaction on behalf of the participating lender group and, back in April ’21, accurately forecasted where the fight would focus nearly two years later:

As to the $200 million super senior tranche of debt, I don’t think that’s controversial. We’ve been doing it for years. The part that I think made it a bit more adversarial was the non-pro rata portion of the transaction with the exchange offer, because effectively by flipping everyone up, you’re subordinating everyone else down the capital stack.

In the end, we analyzed the loan documents and pursued a transaction that was permissible between the lack of subordination protection and the open-market purchase language in the credit agreement. Now, whether or not people liked it was a very different thing. We weren’t tone deaf; we recognized the people that were sitting on the outside of this transaction would not be happy.

Now that’s an understatement. The two-hundred-and-fifty-ish-million-dollar question is this: what is an “open market purchase” in the context of SSB’s loans? The participating lenders offer some thoughts in their motion for summary judgment:

An open market purchase for a private company’s loans—unlike an open market purchase on the public stock exchange, which could hypothetically be open to any buyer or seller— necessarily involves direct and private dealings with the lender who owns those loans… Because syndicated loan debt is not traded through a public exchange, a purchase or sale of a private company’s debt will never be available to all market participants in the same way as a stock market trade.

SSB adds:

[I]t is undisputed that an open market purchase for loans, unlike those for registered trades on a public stock exchange, can only be consummated by those lenders who own the existing loans… In order for the Company to repurchase its debt through an open market purchase, it has to approach individual existing lenders in the open market and negotiate the terms of a repurchase, as it did here.5

On the other hand, in their oppositional brief, the non-participating lenders have offered a variety of legal arguments, plus two expert reports and a helpful introductory supporting declaration from Wharton Professor Vince Buccola, to argue that this transaction was not what the parties intended by the phrase “open market.”6

In an “open market” an issuer does not handpick certain favored lenders to participate in a transaction while simultaneously concealing the availability of the deal from the rest of the interested market. Still less does it actively exclude existing lenders that learn of the deal and seek to join. Yet that is precisely what Serta and its allies did. In a maneuver that would make Vice President Elbridge Gerry (progenitor of the term “gerrymander”) blush, plaintiffs structured the transaction to work only if other First Lien Lenders were excluded.7

Okay, first of all, LOL. You know it’s serious when the adversary complaint defendants are name-dropping Vice President Elbridge Gerry (in office 1813-14). More to the point:

As explained in the accompanying declarations… an “open market purchase” in the context of a credit agreement is a purchase of bank debt, typically for cash, in the secondary bank debt market conducted at arm’s length at or close to the prevailing market price. The secondary bank debt market is a well-developed market where buyers and sellers regularly come together to transact, through banks and broker-dealers that serve as intermediaries, in the purchase and sale of both par and distressed bank debt…

Accordingly, open market purchase provisions in credit agreements are intended to permit one-off purchases of term loans on a non-pro rata basis in a quick, cost-efficient manner in ways that do not resemble tender offers.

We’ll sum up the issue like this. It seems that one very viable interpretation is that the loan parties intended this provision to provide the borrower with some flexibility to repurchase its loans and capture trading discounts. On one hand, a repurchase through a broker at the lowest available secondary market trading price seems much more in line with the definition of “open market.” On the other, there probably isn’t enough secondary market liquidity to repurchase, like, half your $1.9b first lien term loan in one go, so you can understand why a borrower would need to engage in direct negotiations with its major creditors. Still, the agreement was written to include other options beyond an “open market purchase,” namely a pro-rata Dutch auction and an exchange offer, that would be capable of facilitating a large repurchase outside of the secondary markets. It may be the case that the debtors are trying to streeeeeetch the (non-pro-rata) open market purchase exception to validate a transaction that ought to have been accomplished through other (pro-rata) provisions.

We’re not bankruptcy judges, and our Texas gumption is sorely lacking, but this whole thing seems at least a little bit *ambiguous* to us. We’ll also note that the non-participating lenders decision to retain multiple experts and introduce witness testimony at the summary judgment phase seems designed to facilitate an almost certain appeal. They argue:

…if the Court finds the agreement to be ambiguous (which was the view of the court in LCM), discovery on the contract claim is appropriate. The parties have had no meaningful opportunity to conduct discovery regarding the intent of the parties and the interpretation of the agreement, and the Court should not resolve an ambiguity without that evidence. In this dispute, where the Excluded Lenders seek only a monetary recovery solely from the Favored Lenders – which have known all along of the Excluded Lenders’ claims – there is no legitimate reason for a rush to judgment. (emphasis added)

We’ll have to wait and see what Judge Jones decides on Tuesday. Mark your calendars, double check those cooperation agreements (we’re looking at you, Carvana lenders), and, if you’re a small-AUM lender holding distressed names, may G-d have mercy on your soul.

*****

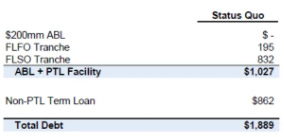

Despite all of this drama, the debtors’ chapter 11 cases are proceeding at a healthy clip. On Thursday March 23, Judge Jones approved the debtors’ revised disclosure statement in an uncontested hearing. Things are largely tracking the terms set forth in the original restructuring support agreement (with some minor changes, i.e., a slight increase in debt on balance sheet post-emergence, from $300mm to $315mm). Which just goes to show precisely why this creditor-on-creditor violence thing is such a big deal.

See, it just so happens that according to the debtors’ investment bankers at Evercore, the value “breaks” at the FLSO making it the “fulcrum security.” This means that the holders of FLSO claims will end up with, among other things, 100% of the post-reorg equity (subject to dilution, etc.). This amounts to an estimated recovery around 75%.

What is the projected recovery for the non-participating lenders? It’s max 2.4%, lol, provided they’ve voted to accept the plan, LOL.

⚡️Update: Voyager Digital Ltd.⚡️

Let’s take a brief break from our regularly scheduled programming to get a quick glimpse of Voyager Digital Ltd’s attorneys over at Kirkland & Ellis LLP, including Joshua Sussberg…

…Christopher Marcus…

…Christine Okike…

…and Allyson Smith:

On the heels of getting its plan or reorganization confirmed after a long and painful eight months that required these fine folks to learn far more about crypto than we reckon they ever f*cking wanted to in a thousand motherf*cking f*ck f*ck years … and after seeing their original deal with that fraudulent f*ckface Sam Bankman-Fried fall through … and after seeing the US government get napalmed by the bankruptcy court judge in their attempts to obstreperously obstruct the proposed sale to Binance … the plan is on hold. That’s right, it’s on hold. The US government sought a stay pending appeal and got it from US District Judge Jennifer Rearden yesterday.

The deal is a blow to Voyager, which has been trying to exit bankruptcy and repay its customers since filing for Chapter 11 protection last year. The proposed sale to Binance’s US arm is worth about $1 billion, a sum that primarily reflects the value of Voyager’s customer accounts.

Adding a bit of extra comedy to this is the fact that the appeal commenced before yesterday’s news that another division of the US government, the Commodity Futures Trading Commission, sued Voyager’s buyer, Binance, and its CEO Changpeng “CZ” Zhao over a bunch of shady-a$$ sh*t.

The bright side? Potentially more fees!! 😜

🧁New Chapter 11 Bankruptcy Filing - CBC Restaurant Corp.🧁

Sometimes the smaller cases have more fireworks than the large ones.

On February 22, 2023, Dallas-based CBC Restaurant Corp. and three affiliates (the “debtors) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Owens). The debtors are best known as “Corner Bakery,” a fast casual purveyor of “…kitchen-crafted, artisan-inspired food, made by real cooks, for breakfast, lunch & dinner” located primarily in the the heart of neighborhoods and urban markets across California, Texas, Pennsylvania, Illinois, Virginia, Maryland, and the District of Columbia. Real cooks, y’all!

The debtors — which had over 100 locations — apparently had been struggling even before the pandemic, with declining average unit volumes battering the business. These struggles were — not to state the obvious — compounded by the pandemic which decimated the debtors’ workplace catering business and its commuter traffic.

Interestingly, the debtors’ current sponsor, Pandya Restaurant Growth Brands, LLC ("PRGB"), one of the Rohan Group of Companies, purchased the debtors in April 2020 from Roark Capital Group. For its part, Roark acquired Corner Bakery in 2011 — right in the midst of, in case you forgot, a global pandemic. Terms of the Roark sale to PRGB were not disclosed which, from our vantage point, probably means that PRGB got a sweetheart deal and figured it would play out an option. Furthering that view is the fact that, around that time, Corner Bakery reportedly had already been working with DLA Piper and Stifel to restructure the company’s debt and evaluate strategic alternatives. It appears they found one in PRGB. Anyway, this was a boldly-timed transaction: we’d love to see that underwriting memo! PRGB subsequently introduced a new management team and a new business plan focused on improving the guest experience, menu development, and brand recognition. Clearly that didn’t go so well.

About the aforementioned debt. The debtors are party to a ‘17-vintage credit and guaranty agreement, initially with Goldman Sachs Specialty Lending Group L.P. as agent. The original debt amount was $177.5mm but the facility has been amended and/or extended nine times since September ‘19. The lenders have the benefit of a pledge and security agreement as well as a trademark security agreement. As of the petition date, the debtors state that they owe approximately $33.8mm. The debtors’ successor agent, SSCP Restaurant Investors LLC (“SSCP”), begs to differ: it alleges it is owed north of $40mm.

Let’s pause here to talk about SSCP for a second. According to its own website, “SSCP and/or its affiliates currently owns/operates 80 Applebee’s, 43 Sonic Drive-In’s, is the parent for the fine dining concept Roy’s, and owns various shopping centers, apartment buildings and other real estate holdings.” In a savage maneuver, SSCP swooped in during the 11th hour — as the debtors were discussing the maturity of their credit facility with their existing lenders and negotiating a potentially meaningful $20-$24mm loan paydown — and acquired the credit facility. Within 18 days SSCP was up the debtors’ a$$ about alleged events of default; indeed, shortly thereafter SSCP quickly demonstrated its intent to foreclose on the debtors’ assets and “…caused a Notice of Public Sale of Collateral to be issued, setting a sale of collateral to be held on February 23, 2023.” Note the filing date above! Coincidence, that is not. This was a crash chapter 11 filing.8 Per the debtors:

As a result of the discord with SSCP and the vulnerable state of its financial condition, the Debtors have determined that a substantial deleveraging combined with new capital investment is the best path forward for their business as a going concern and will serve as the foundation of a reorganization plan that will payoff the company's creditors while also preserving stakeholder value.

Clearly the crux of this case is the battle between the debtors and SSCP. The debtors intend to investigate the validity of SSCP’s pre-petition liens. In turn, SSCP is gonna start hurdling bombs over every Corner Bakery fence in America. Points of conflict include the debtors’ proposed (i) use of cash collateral and (ii) rejection of certain non-residential real property leases. But that’s just the starter course. On March 20, 2023, SSCP also filed a motion seeking the appointment of a Chapter 11 Trustee due to “the failures of the Debtors and existing management to keep even the most fundamental business records or operational information.” Let’s address each of these in turn.

📍Cash collateral. Back on February 24, 2023, SSCP agreed to the debtors’ use of their cash collateral for the limited purposes of funding (a) $2.4mm of overdue payroll and (b) approximately $1mm of essential food costs (read: together, “critical operating expenses”). It’s good to see that the parties could agree that workers and food are key to a restaurant business! Anyway, things didn’t stay constructive for very long. Shortly thereafter, SSCP demanded that the debtors provide direct, read-only access to the company’s “Rossnet” system, which houses financial software and data. CBC found this inappropriate and claimed it would hamper reorganization efforts and assured that SSCP is “adequately protected.” A subsequent agreement followed on March 15, 2023 regarding CBC’s use of cash collateral, and again on March 22, 2023. The next key date relating to the use of cash collateral is today, March 28, 2023.

📍Rejection of Non-residential real property leases. The debtors were parties to 113 nonresidential real property leases prior to the petition date. Wasting no time, the debtors filed a motion seeking the rejection of certain of these real property leases within a week of the bankruptcy filing. Why? A number of the cited locations had been closed and vacated pre-petition; some were never even opened (which became the subject of lawsuits); and, finally, 11 locations were with one particularly litigious landlord who was none-too-pleased that the debtors had designs to gtfu of their lease obligations early.

The debtors had plenty of data to back-up their decision. Their “performance analysis” indicated that all of the 11 recently vacated premises operating in ‘22 either had negative EBITDA or would have if the rental/operating expenses were paid. The debtors said that monthly sales averages for the 6 months preceding the petition date indicated a rent to sales ratio of 25% or higher, with some stores exceeding 35%(!), and that a rent to sales over 20% indicates a very low probability of ever being profitable (which begs the question why they were opened in the first place). All the personal property left behind on the premises was deemed immaterial by CBC. Read: there’s plenty of unused cutlery up for grabs!

SSCP was pissed. It claims that the debtors didn’t bother to consult with them about either the closed locations or the abandoned property (read: collateral). In a response, the debtors call BS on that, providing emails as support. Not a great look for SSCP. Also, they may get a rude introduction to “business judgment.”

📍The Chapter 11 Trustee motion. Whoa boy. Per SSCP:

“The appointment of a Chapter 11 Trustee is necessary in these Chapter 11 Cases due to organizational and management failures at the highest levels. Simply put, the only true stakeholders here—creditors like SSCP and the debtors’ franchisees, given certainty of deep insolvency—have no faith in the debtors’ leadership and direction, and it has become clear that reorganization with the status quo in place is impossible.”

SSCP highlights the debtors’ alleged inability to explain numerous discrepancies in bank statements, financial records, etc. SSCP also notes its inability, despite repeated requests, to obtain management agreements or shared service agreements involving PRGB, the Rohan Companies, or other entities that may be controlled by Jay Pandya. They argue:

“It has become apparent that even the most basic financial information needed to operate a business of this size is mysteriously lacking. After repeated requests by SSCP, the debtors’ professionals have stated that the following financial and operational information simply does not exist: 2020-2022 audited or unaudited financial statements; 2020-2022 tax returns; Corporate personnel organizational chart; Monthly G&A detail statements for each debtor, including salaries by employee; Monthly statements of cash flows; and Historical store-by-store operating financials. Further, the debtors continue to resist providing other financial information that is standard in multi-store restaurant businesses. While the debtors are required to provide necessary information under the Cash Collateral Order the information provided has been limited, untimely, and insufficient.”

It gets nastier:

“Mr. Pandya and PRGB used the debtors as a piggy bank – taking over $21 million of funds out of the debtors’ business for the benefit of entities owned and/or controlled by Mr. Pandya. Mr. Pandya’s self-dealing in the business of the debtors knows no bounds. His actions leading up to and since the filing of the debtors’ bankruptcy proceedings have reinforced SSCP’s position that Mr. Pandya is incapable of acting in the best interest of the debtors.”

SSCP drove the hammer home by describing Jay Pandya’s further mismanagement, citing Pandya Brands’ earlier default under obligations to Pizza Hut and the subsequent litigation.

“Since 2020, Mr. Pandya and various entities he owns and/or controls have been named defendants in at least 58 cases involving a number of matters related to, among other things, franchise disagreements, landlord disputes, and breach of contract claims. A list of these lawsuits is attached hereto as Exhibit A. This is in addition to the at least 84 cases filed against the debtors since 2020”.

Apparently Mr. Pandya could not “Out-Pizza-The-Hut” lol.

The question now is whether his management team will survive SSCP’s vote of no confidence….9

Stay tuned.

The debtors are represented by Culhane Meadows PLLC (Lynnette Warman, Sharon Lewonski, Mette Kurth) as legal counsel, CR3 Partners LLC (Greg Baracato) as CRO, and Hilco Trading LLC d/b/a Hilco Global (Teri Stratton) as investment banker. SSCP Restaurant Investors LLC is represented by Foley & Lardner LLP (Holland O’Neil, Mark Moore, Stephen Jones, Timothy Mohan, Andrew Howell, Steven Lockhart) and Ashby & Geddes PA (Ricard Palacio). Finally, the UCC is represented by Tucker Ellis LLP (Jason Torf, Thomas Fawkes, Brian Jackiw) and Potter Anderson & Corroon LLP (Christopher Samis, Aaron Stulman, Levi Akkerman).

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.

The non-participating lender group structured their S.D.N.Y. lawsuit to only press claims against the participating lenders (thus trying to avoid the automatic stay). However, the debtors and participating lenders have an indemnification agreement, through which SSB is apparently liable for any damages resulting from the uptier transaction. SSB claimed that the indemnification obligation could drive them back into insolvency after exit, and therefore the litigation needed to be resolved as part of the Chapter 11 cases.

Those cases are the LCM case against SSB, Boardriders, and Trimark.

We’ve already seen at least three administrative agents resign their role rather than sign off on an uptier (Trimark, Boardriders, Incora), though their successors were happy to ratify the transactions. It’s worth noting that many new agreements have new “technology” with blockers designed to prevent a lot of these creditor-on-creditor episodes in the future.

The other issue is breach of the implied covenant of good faith and fair dealing, but that’s been more of a background claim.

SSB also raises an fun point, highlighted by this FT article, that some of the non-participating lenders were actively negotiating a rival dropdown transaction which (similarly to Revlon) also would have included a roll-up under the open market purchase exception.

Of course, just because Angelo Gordon is performing some legal gymnastics, doesn’t mean that the arguments here should be dismissed out of hand. Indeed, one of the key plaintiffs from the past two years (and now a defendant under SSB’s adversary complaint in bankruptcy court), LCM Asset Management LLC, was not part of the dropdown group, was not invited to participate in either liability management transaction, and, for all intents and purposes, was an innocent bystander throughout the process. It is NO FUN to be a small lender in the current distressed environment.

Interpreting the parties’ intent is the fundamental question in a contract lawsuit. In some circumstances where the meaning of the contract is clear (unambiguous), a judge may rule on the lawsuit at the summary judgment phase. If a contract term is unclear (ambiguous), the court holds a full trial and each party may present facts to support their view of what the parties intended the term to mean.

For example, Ryan Mollett, head of distressed at Angelo Gordon, noted in his declaration that SSB offered to let AG participate if it agreed to ditch Gamut and Apollo (the other lenders it had formed a bloc with). AG refused.

Indeed, in their response to SSCP’s objection to their motion to extend the time to file their schedules and SOFAs, the debtors noted the following:

…the Debtors commenced these cases with virtually no advance planning. A substantial amount of work that would ordinarily be done by the Debtors and their professionals prior to the Petition Date—such as preparing "first-day" motions for the chapter 11 filings, negotiating cash collateral usage and financing with their lender, preparing the business to transition into chapter 11, negotiating with their significant creditor constituencies, and preparing creditor matrixes—did not occur until after the Petition Date.

You don’t see that every day.

A status conference was held on March 23, 2023 but its unclear from the docket what, if anything, was achieved.