💥 Housing-Related Pain is on the Rise💥

As interest rates rise, mortgage issuers and servicers are in trouble.

")

On November 30, 2022, NJ-based and Starwood Capital Group-backed Reverse Mortgage Investment Trust Inc. (“RMF”) and four affiliates (the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Walrath) — the latest company to suffer due to Fed action that’s sparked a devastatingly quick reversal in the housing space. PETITION readers will recall that First Guaranty Mortgage Corporation filed for bankruptcy back in late June when interest rate increases first started to really bite.

Before we get to RMF, let’s take a moment to review what happened in housing last week:

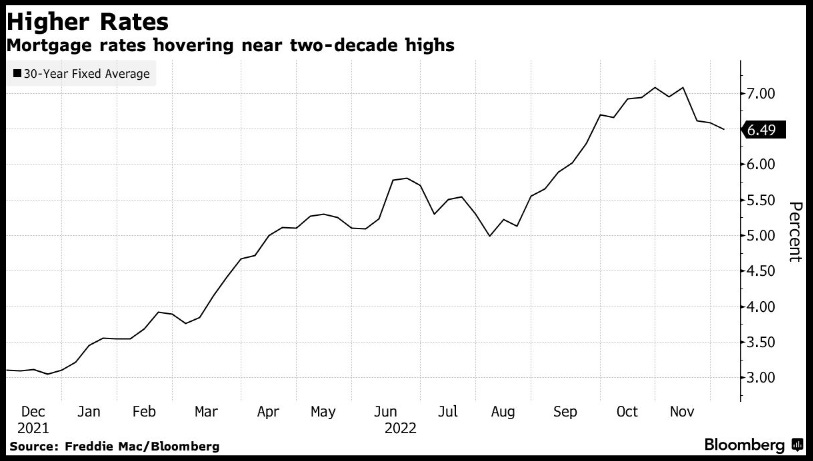

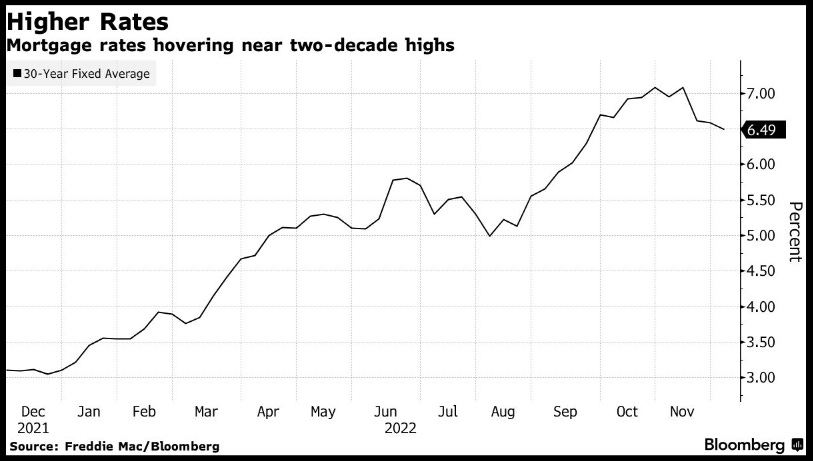

Higher interest rates and sky high prices have destroyed housing demand while supply remains considerably tight.

That said, prices are coming down. Last week the S&P CoreLogic Case Shiller national home price index showed a decline for the third straight month in September (down 0.80%). YOY price growth stood at 10.8% (which, believe it or not, reflects a slowdown).

Last week Fannie Mae and Freddie Mac agreed to raise the limits of government-backed loans — in some high-cost areas, the maximum loan limit will exceed $1mm, a record. It’s hard to say given the record home prices but, on the margins, this may mean that certain borrowers in a pricing sweet spot may avoid jumbo loans. It also might mean that people take on more debt for a stretch home.

For the ninth straight month, existing home sales fell at a clip of 5.8% month-over-month and 28.4% YOY. Pending sales figures look bleak AF:

Bank of America Inc. ($BA) CEO Bryan Moynihan predicted on CNN last week that “…there could be two years of pain in the housing market before activity returns to normal.”

Per Bloomberg, Wells Fargo & Co. ($WFC) “…cut hundreds more mortgage employees [last] Thursday, the latest in a series of reductions across the industry after higher interest rates brought the pandemic-era home-lending boom to halt.” Back in the early summer, JPMorgan Chase & Co. ($JPM) laid off hundreds in its home lending group while also reassigning hundreds more employees. Non-bank lenders have also — as the bankruptcies suggest — been taking it on the chin.

Blackstone Real Estate Income Trust Inc. (BREIT), a $69b non-traded real estate investment trust threw up its gates, preventing investor redemptions. The company focuses on rental housing and industrial properties in the Southern and Western US. In other words, its investments are highly illiquid and this presents a timing mismatch when investors want to pull their funds: it’s not like the REIT can just liquidate its holdings to satisfy redemptions at the flip of a dime. This all trickled over to Blackstone Inc’s ($BX) stock which got halted on Thursday after dropping like a stone. More here (from FT).

On Monday, Starwood Real Estate Income Trust (“SREIT) followed suit (Barron’s). The $14.6b non-traded real estate investment trust — which happens to be the second largest non-traded REIT behind you-know-who above — threw up its gates after elevated investor withdrawal requests exceeded the REIT’s 5% quarterly limit. SREIT’s investment profile is similar to BREIT: multi-family apartment complexes and warehouses. Investors are running for the hills after years of (inflated?) out-performance relative to publicly-traded peers (which tend to use less leverage). 🤔 This comment to the Barron’s article seems to be 100% on point: “It’s implied that these people have gotten out because this fund is up 10% while publicly traded REITs are down 30%. Does that mean they are moving funds to publicly traded REITs as a value play! Doubt it. Isn’t the thought process more like ‘I’m lucky I’m up 10% in an over priced real estate market considering interest rates, cap rates and a looming recession. I’m out!’”

Also on Monday, The Black Knight House Price Index (HPI) came out. It came chock full of interesting commentary:

“We’ve now seen four consecutive months of home price pullbacks at the national level,” said Graboske. “But after a couple of significant drops earlier in the summer, the pace of cooling has slowed considerably, with October’s non-seasonally adjusted drop of just 0.43% the smallest decline yet. Though seemingly counterintuitive, the much higher rate environment may be limiting the pace of price corrections due to its dampening effect on inventory inflow and subsequent gridlock in home sale activity. While the median home price is now 3.2% off its June peak – down 1.5% on a seasonally adjusted basis – in a world of interest rates 6.5% and higher, affordability remains perilously close to a 35-year low. Add in the effects of typical seasonality and one might expect a far steeper correction in prices than we have endured so far, but the never-ending inventory shortage has served to counterbalance these other factors. Indeed, the volume of new for-sale listings in October was 19% below the 2017-2019 pre-pandemic average. This marks the largest deficit in six years outside of March and April 2020 when much of the country was in lockdown – with the overall market still more than half a million listings short of what we’d consider ‘normal’ by historical measures.

“Though the home price correction has slowed, it has still exposed a meaningful pocket of equity risk. Make no mistake: negative equity rates continue to run far below historical averages, but a clear bifurcation of risk has emerged between mortgaged homes purchased relatively recently versus those bought early in or before the pandemic. Risk among earlier purchases is essentially nonexistent given the large equity cushions these mortgage holders are sitting on. More recent homebuyers don’t fare as well. Of the 450K underwater borrowers at the end of Q3, the mortgages of nearly 60% had been originated in the first nine months of 2022 – and these were overwhelmingly purchase loans. All in, 5% of purchase mortgages originated thus far in 2022 are now marginally underwater, with another 20% in low equity positions. Among FHA purchase mortgage holders specifically, more than 20% have slipped underwater and a full two-thirds have less than 10% equity. This is an illustrative and, unfortunately, potentially vulnerable cohort that we will continue to keep a close eye on in the months ahead.” (emphasis added)

Which gets us to RMF. We’re not gonna lie: this is a complicated business that the debtors “attempted to encapsulate” in this chart: