💥Will Regis' Lenders Take a Haircut?💥

Plus: A Carvana Update ($CVNA). And One to Watch: Armstrong Flooring ($AFI).

You may not be so familiar with the name Regis Corporation ($RGS) but there’s no doubt that you’ve seen one of their brands: Supercuts, SmartStyle, Cost Cutters, First Choice Haircutters or Roosters. Founded in 1922, the MN-based company franchises, owns and operates hair salons that — let’s be honest — have been a bit of a punchline for quite some time. Johnny remembers back in the day when his school bully Biff used to riff, “Where’d you get that haircut, Johnny…Supercuts?” to uproarious laughter. Johnny is still in therapy.

You know what else sparks uproarious laughter? This stock chart⬇️:

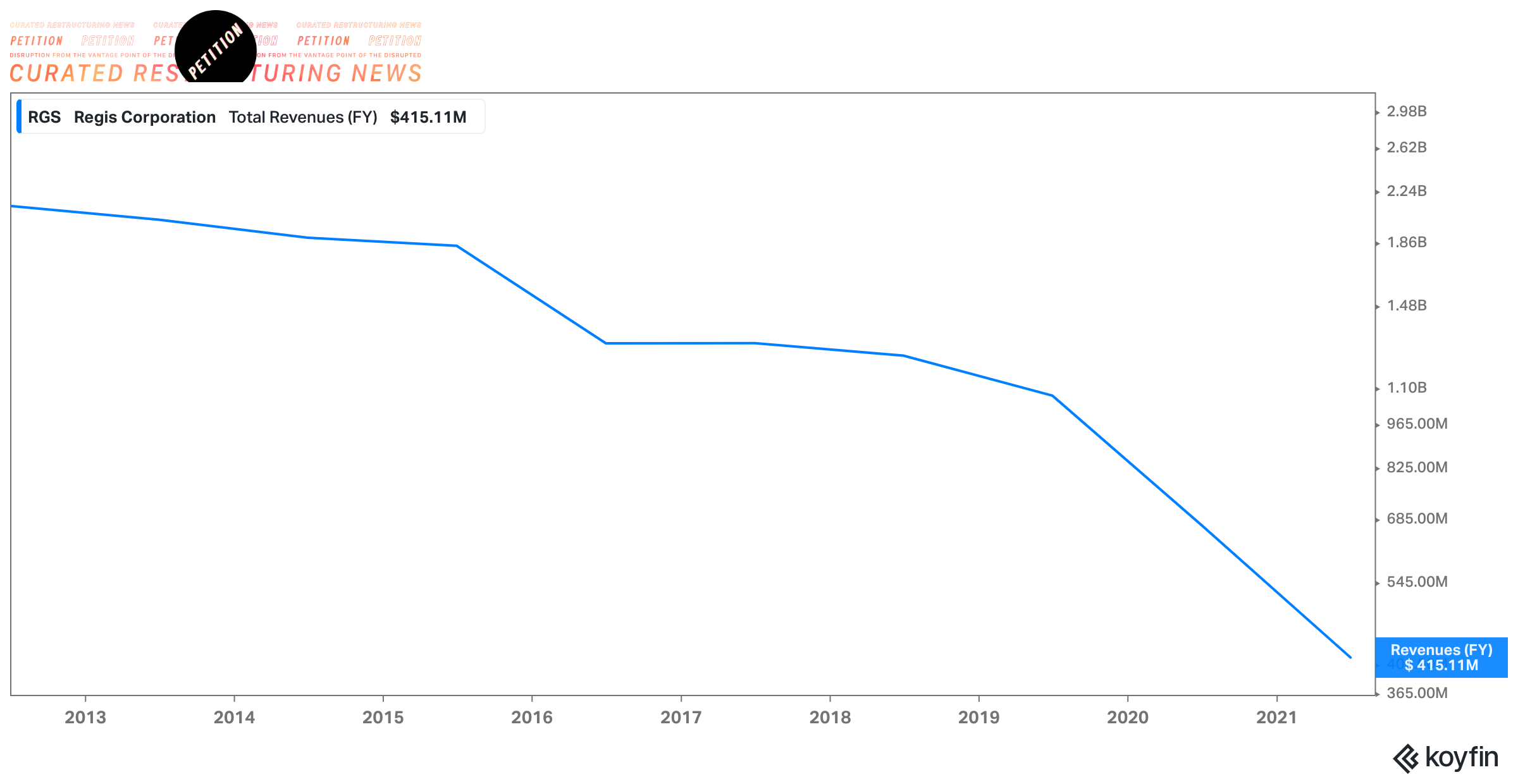

Why the precipitous drop? Having a penchant for losing gobs of money will do that. Take a look at the company’s revenue over the last ten years:

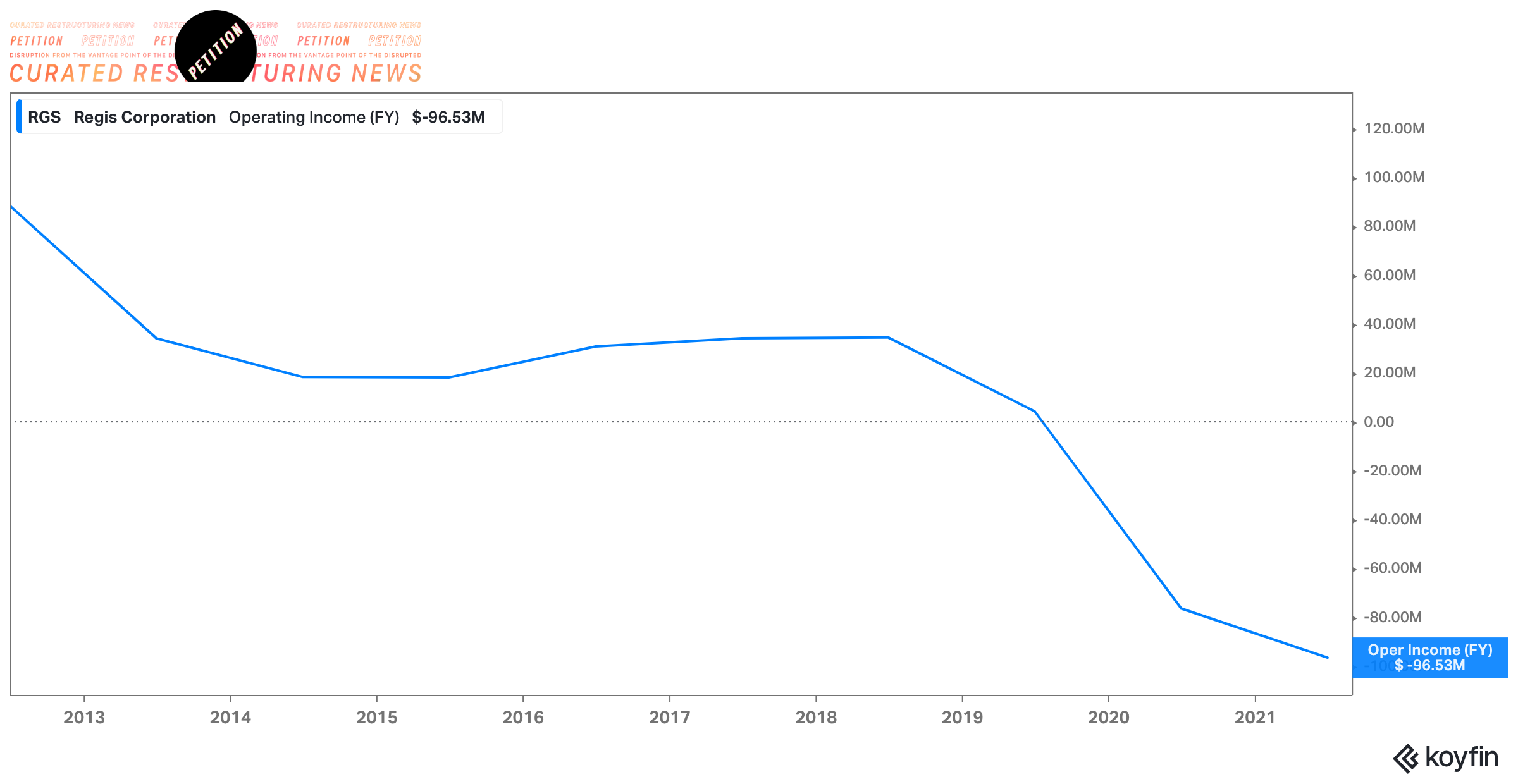

And here is the company’s operating income over the same time frame:

Sh*t is ugly. The company has only turned a profit in two years over the last decade due to a number of unprofitable salons.

Consequently, prior to the pandemic, management decided to take action and transition the business to a full franchise model. The company had 12.7k worldwide locations in 2010 of which ~16% were franchised. Today, the total number of worldwide locations is down to approximately 5.8k of which 97% are franchises.

There’s still work to do. Regis posted a net loss of $113mm for FY21 (ended June) driven by store closures. That trend has continued into FY22 with the company posting a net loss of $10.4mm in Q122 and $4.9mm in Q222. Overall Q222 revenue dropped by ~33% against the same quarter in 2020 to $70mm. This was driven by Regis exiting company-owned salons that generated significant revenue but even greater losses.

According to the Q2 earnings call, company-owned stores lost RGS ~$43mm of EBITDA in FY21. In addition to rolling off company-owned stores, management implemented cost saving measures such as (i) exiting a product distribution business, which was a logistical nightmare, and (ii) launching a new CRM technology called “Opensalon PRO.” These efforts led to over $15mm of EBITDA savings in FY21.

There were some other positives — though you may need to spin your head a few times to grasp them:

On a two-year basis, a comparison to pre-COVID, systemwide comps were down 17% in the quarter. We reported an operating loss of $1 million during the quarter, which is a significant improvement from an operating loss of $27 million in the prior year quarter. The improvement results from an increase in systemwide sales, our G&A savings initiatives, wind down of our company-owned salons, and a few onetime non-cash benefits. On an adjusted basis, second quarter consolidated adjusted EBITDA was $2 million, compared to a loss of $18 million in the prior year's quarter.

And:

Our core franchise business achieved adjusted EBITDA of $5.5 million, compared to a loss of $6.8 million in the prior year. We are pleased to see positively EBITDA results, which reflects the cost savings initiatives we have undertaken.

Interim CEO Matt Doctor said “Our Q2 results reflect our shift to a fully franchised business model, as we are nearing profitability amid the continued impact of the pandemic in terms of labor availability and customer traffic.” He added that management’s six key priorities are:

Addressing the company’s capital structure,

Continuing to exit remaining corporate-owned salons,

Strengthening its franchisee relationships,

Driving and increasing customer traffic,

Furthering the adoption of technology, specifically the Opensalon PRO platform, and

Reassessing the company’s salon brands to ensure that they’re relevant to today's consumer.

Management hopes that the combination of these initiatives — coupled with liability management and a return to pre-pandemic sales levels — will drive a $38mm EBITDA business.

The question is whether the company’s lenders are convinced.

Like, say, the lenders behind the company’s 5.125% March ‘23 revolving credit facility (“RCF”).

Back in late March, the Wall Street Journal reported that the company had hired Jefferies Financial Group Inc. ($JEF) to help it address the maturity of the RCF. As of December 31, ‘21, total liquidity was $117mm — consisting of $35.4mm in cash and $81mm available under the $291.7mm RCF. The RCF has a minimum liquidity covenant of $75.0mm which means that net available liquidity as of December 31 was $63mm. The company was able to bolster its cash position through an incremental at-the-money equity raise, which resulted in $37mm of additional capital. Still, with performance this bad, there’s clearly work for some smart bankers to do here.

So what do we suspect that Jefferies is doing here? Well, we have to assume that the lenders want no part of owning this piece of sh*t. They know that. The company knows that. Jefferies knows that. So that means that a bankruptcy wherein they swap the paper for equity in a reorganized company isn’t exactly super-appealing. It doesn’t mean it’s not possible, though.

So what do liability management options look like? Jefferies could try and find someone to take out the lenders — likely at a discount. First lien lenders generally don’t like discounts, however, and so they may be more amenable to rolling the dice with a continued relationship; they can roll into a new piece of paper at what would undoubtedly be more favorable economics for them but more crippling economics for the company. Rates are rising, after all. If things completely go to sh*t on either of these options, a bankruptcy sale process is another potential avenue.

We reckon that, as always, everyone’s acting to try and avoid that scenario.

Luckily, the company reports earnings on May 10, 2022 so we should have some updates then.

🚩One to Watch: Armstrong Flooring Inc. ($AFI)🚩

Back on New Year’s Eve, PA-based Armstrong Flooring Inc. ($AFI), a designer and manufacturer of “innovative” flooring solutions, news dumped that it had successfully amended its ABL credit facility (Bank of America NA) and term loan facility. The amendments provided covenant relief under both facilities through June 30, 2022. In tandem with the amendments, pre-existing term loan lender, Pathlight Capital LP, provided the company with $35mm in incremental term loans. The company intended to use that financing to, among other things, buy some time for its investment banker, Houlihan Lokey Capital Inc., ($HLI) to find a buyer. Internally within PETITION, a note circulated at the time that said, “[m]ight be worth a quick peek to see how long $35mm might carry these guys….” Well, we never got around to researching and publishing anything on the name but we’ve nevertheless gotten our answer: not long, apparently.