💥Rate Cuts Coming?!💥

Plus: a(nother!) Rite-Aid Update & a rash of new filings (2U, Mobileum, Conn's).

Ruh roh guys. If you think your “new restructuring matter” pipelines are looking bare now, the macroeconomic data ain’t exactly working in your favor.

Consumer prices fell 0.1% in June, their first decline since May ‘20, slowing the annual rate of inflation to 3% in June from 3.3%; both were “better” than consensus. The Bureau of Labor Statistics, responsible for the report’s creation, cited falling gas prices, “more than offsetting” an increase in shelter costs. The core rate, which excludes fuel, rose 0.1% in June, bringing the annual rate to 3.3%. The BLS says this is the smallest 12-month increase since April ‘21.

The Federal Reserve is indifferent to CPI, or so they say. How the market reacts to CPI is another matter entirely. The Fed does care about the Personal Consumption Expenditures Price Index, aka PCE, often called “the Fed’s preferred inflation gauge.” The measure rose 0.1% in June from May, and to 2.5% on an annual basis, the Bureau of Economic Analysis disclosed on Friday. PCE ex-food and energy rose 0.2% for a year-over-year increase of 2.6%. The data was in line with expectations; the commentariat observed that inflation is creeping steadily toward the Fed’s 2% target.

You know what that means? No longer this high for much longer?!?

That’s right, market expectations shifted quickly, pricing in a 94% probability of a Fed rate cut in September.

More amazing, the market expects two more cuts before year end (during the election cycle, no less, 😬, former President Trump is sure to love that!) and four cuts in ‘25.

In other words, the market is finally admitting that Goldman Sachs Group Inc. ($GS) was right all along: the so-called “vampire squid” notorious for planting alumni at central banks around the world (Mario Draghi at the ECBi, Mark Carney at the Bank of England) has been bucking the market and holding to its call for two rate cuts this year;* and it’s been saying for some time now that September is where the action is at.

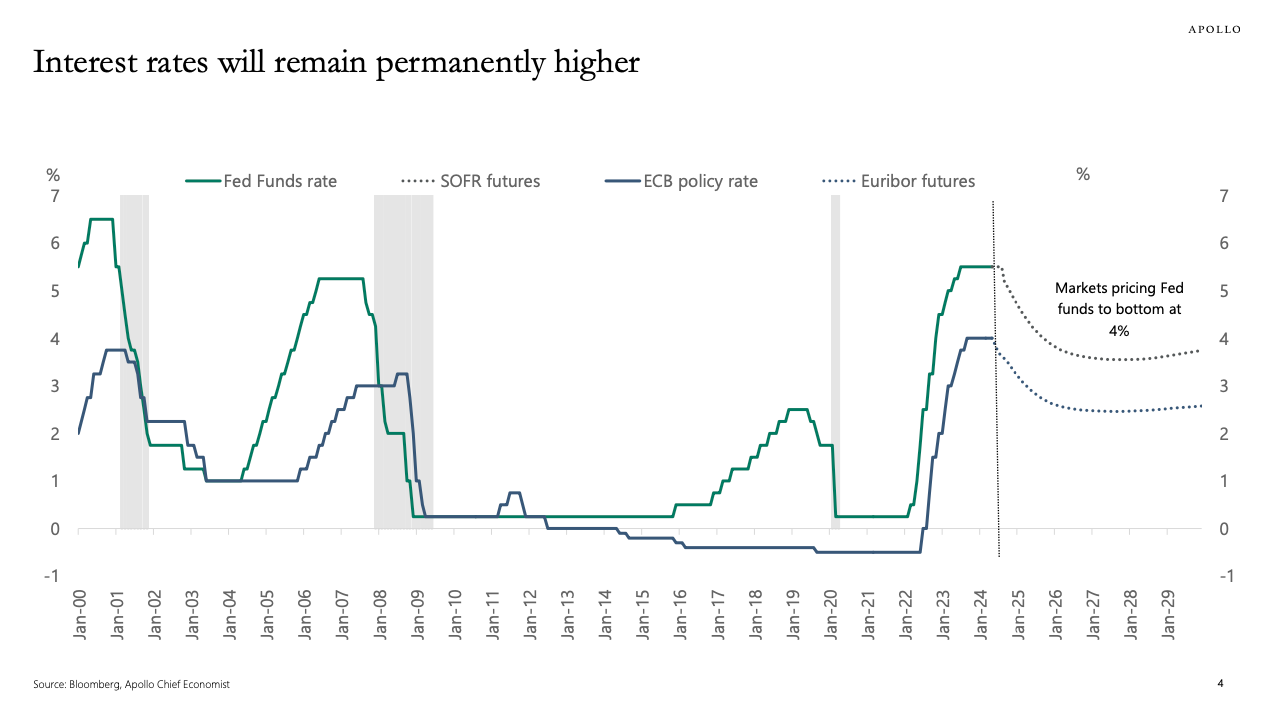

How low can it go? Some have their doubts, most notably, Dr. Torsten Sløk, chief economist at Apollo Global Management, who recently released his midyear chart book, chock full of some of the most graceful charts in the business. Each and every one of Dr Sløk’s slides will give you something to worry about. Top of mind is — no surprise! — interest rates. Higher for longer, said Dr Sløk (as we recall he was among the first to forecast NO rate cuts this year), adding “strong near-term growth, deglobalization, the energy transition, increased defense spending, rising Treasury issuance, and US fiscal deficits.” (Maybe double-check the “energy transition” thing, though.). This one was our favorite:

Not just “higher for longer,” but permanently higher. A terminal rate of 4%. Oh dear! Is that where the Fed will land? His forecast for no cuts ain’t looking so hot but will things “remain permanently higher”?

Anyway, couple lower rates with all of that darn cash out there ripe for investment …

… per Institutional Investor …

Record dry powder is not a proxy for the health of the private equity and VC industries. A short list of the largest managers accounts for a disproportionate share of the cash. The 25 firms with the largest war chests collectively have $556.19 billion of uncommitted capital, more than 21 percent of all dry powder globally, according to S&P Global Market Intelligence. Topping the list of managers are KKR (which has had a celebratory five-years stretch) and Apollo Global Management, which each have more than $40 billion in dry powder. Ten others have at least $20 billion and the rest have at least $12 billion.

… and ripe for lending …

… and we may be looking at a back half of ‘24 and ‘25 that look like ‘22 for (especially large cap) chapter 11 bankruptcy. Oh, sorry, for those of you suffering from memory lapses: ‘22 was not good.