💥Decidely Poor Prospect(s)💥

Prospect Medical Holdings Inc. is an early candidate for dumpster fire of '25. Also: Mondee Holdings Inc. is this year's first deSPAC sh*tco to file BK.

😷New Chapter 11 Bankruptcy - Prospect Medical Holdings Inc.😷

Back on January 11, 2025, SoCal-based and formerly-Leonard Green & Partners, L.P. (“LGP”)-owned* Prospect Medical Holdings, Inc. (“PMH”) and 66 of its direct and indirect subsidiaries (collectively and together with PMH, the “debtors” and together with their non-debtor affiliates, the “company”) filed chapter 11 bankruptcy cases in the Northern District of Texas (Judge Jernigan), with an embarrassingly low ~$3.3mm of cash on hand against an average of One-Hundred-and-Twenty-One Million dollars in payroll costs per month. That’s just PAYROLL. This is a company that’s “close to $2.5 billion in revenue” for ‘24.

Give us a minute.

Okay, that’s better. Good. G-d. It’s only January, and we already have a contender for the sloppiest bankruptcy of the year. It would be more efficient to cover what’s gone right with this company, but that’s not the kind of shop we run so let’s dive in ⬇️.

With humble beginnings in mid-to-late ‘90s Los Angeles, the company is “a significant provider of healthcare services” and “experienced remarkable growth … evolving into a multi-billion-dollar healthcare system dedicated to serving underserved communities.” Clearly, in addition to serving, they were dedicated to billing. After being acquired by LGP in a ‘10 LBO, and straight out of PE-playbook, the company set its sights beyond the Golden State and went on an debt-fueled acquisition spree, buying up facilities in Texas, Rhode Island, New Jersey, Pennsylvania, and Connecticut from ‘12 through ‘16. It currently operates 16 hospitals across four states, which, for those keeping count, is two fewer than the total mentioned in the prior sentence.

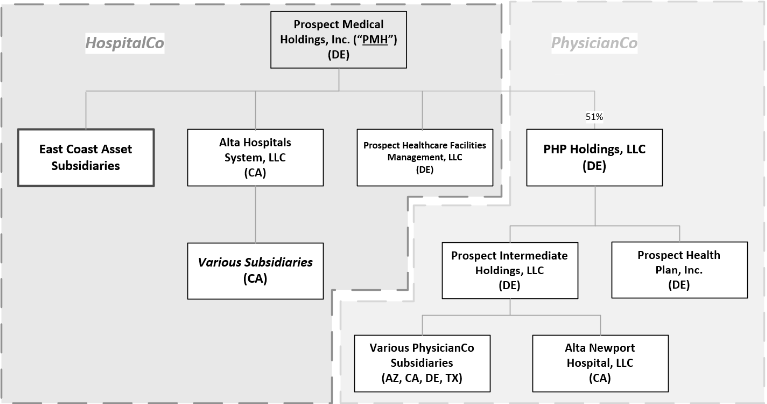

The company operates its business in two “distinct, but interrelated” silos: (i) HospitalCo, which is composed of PMH and its hospital subsidiaries, all of which are debtors other than Prospect Healthcare Facilities Management, LLC (“PHFM”), and (ii) PhysicianCo, which are non-debtors PHP Holdings, LLC (“PHP Holdings”) and its subsidiaries. PHFM is the “member-manager” of PHP Holdings,** and as their names suggest, HospitalCo owns and operates the hospitals, while PhysicianCo houses mostly-services-based operations: healthcare plans, medical groups, management services, and a pharmacy. We say “mostly” because, for some reason, PhysicianCo also has one hospital under its purview, 🤷♀️.

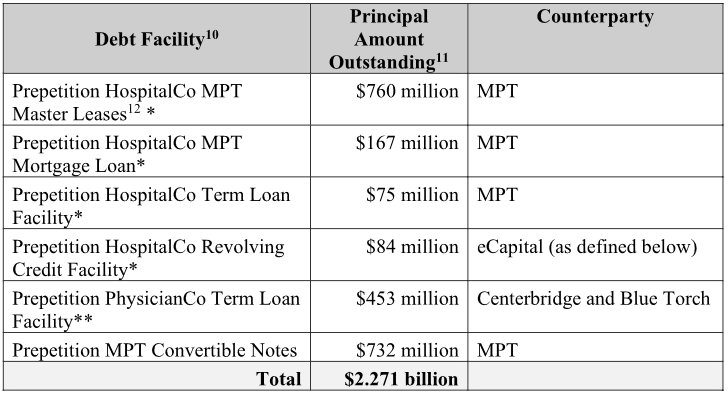

To fund that transcontinental growth and related CapEx,*** the company, naturally, levered up and, as of the petition date, had ~$2.3 billion in funded debt, for which the debtors were directly on the hook for ~$1.1b and, after including guaranties, ~$1.5b.**** Here’s the cap stack:

That elegant two-silo structure 👆 there was born in ‘23 out of the company’s most recent, non-bankruptcy financing: a “comprehensive” liability management transaction (the “LMT”) with Centerbridge Credit CS, L.P. (“Centerbridge”), Blue Torch Capital L.P. (“Blue Torch”), and Medical Properties Trust, Inc. ($MPW) (“MPT”). The company entered into the LMT because, and this will be a persistent theme, it is a bottomless cash pit and needed more to keep the doors open and, when not busy gutting services, patients tended to. Under the LMT, (i) MPT agreed to reduce obligations owed to it by $646mm for a 49% ownership stake in PHP Holdings (PMH owns the other 51%) and convertible notes, which, if exercised, would increase its stake to ~83%, and (ii) Centerbridge and Blue Torch, true to its name, torched $375mm of new money, used to pay off the company’s then-existing debt and transaction costs, fulfill regulatory capital requirements, and “allow PMH to catch up on certain outstanding accounts payables amounts” — not a penny went to the company’s coffers.

Are you waiting with bated breath to find out whether the LMT worked?