🛢️New Chapter 22 Bankruptcy Filing - PetroQuest Energy Inc.🛢️

Louisiana-based E&P files to deleverage for a second time in six years.

On November 13, 2024, Louisiana-based PetroQuest Energy Inc. and three affiliates (collectively, the “debtors”) filed chapter 22 bankruptcy cases in the District of Delaware (Judge Goldblatt). Like most others in the oil patch, these debtors are intimate with boom and bust. They first filed in ‘18,* one of 28 North American E&Ps to do so that year. The debtors’ operating assets currently consist of leasehold interests and producing properties in Panola County, Texas, part of the Cotton Valley shale gas play (the “East Texas Assets”), according to the first-day declaration of CFO Angelle Perret.

The debtors attributed their November ‘18 bankruptcy filing to the horrific downturn in natural gas prices, which left the debtors unable to fund their drilling programs. Cash flow in the first nine months of ‘18 was $1.9mm, then-CFO J. Bond Clement wrote in his first-day declaration. Judge Jones confirmed their plan of reorganization on February 11, 2019. That plan had the effect of equitizing the then-second lien secured notes and providing those claimants with 100% equity in the reorganized company (subject to dilution) plus 10% $80mm ‘24 senior secured PIK notes (the “PIKs”). In addition to the PIKs, the company emerged with a $50mm L+750bps term loan. In total, therefore, the company delevered by more than half.

Talk about a false dawn.

Things went wrong almost damn near the minute the debtors left Judge Jones’ courtroom. The debtors’ last filing with the Securities and Exchange Commission (“SEC”) is for the June quarter of ‘19. “Ugly” is an understatement. Among its disclosures: the debtors had tapped out the exit facility. Unrestricted cash was down to $16.3mm and poised to diminish as natgas prices went down, down, down. The debtors suspended their drilling program and deferred completion of two drilled but uncompleted wells. They warned of the hits to cash flow and proved reserves, which boded nothing but ill. “If natural gas prices remain depressed, we will likely be out of compliance with the Coverage Ratio as of September 30, 2019 unless we receive a waiver from the lenders under the Exit Facility. As a result, there is substantial doubt about our ability to continue as a going concern.” LOL, that sure as f*ck didn’t take long, now, did it?

And that was all they wrote, for public consumption at least. A lonely press release lingering on their web site explains: thanks to an amendment to their 10% senior secured PIK notes due ‘24, the debtors were no longer required to file financials with the SEC. Nor, we reckon, did the company have to contend with the PIKs any longer: there’s no mention of them in the first day papers. Did they get equitized along the way?

We do learn from the first-day filing, however, that the credit facility has been amended six times since the debtors emerged from their first bankruptcy, with the outstanding balance more than doubling to $104.5mm. The last amendment was in September ‘24, and provided the debtors with a $2mm bridge loan. Unsecured debt is around $11mm.

Perhaps removing themselves from public scrutiny saved the debtors considerable embarrassment; everything they touched seemed to go wrong. Their acquisition and divestiture (“A&D”) efforts seemed jinxed. In ‘18, prior to the first filing, the debtors sold their offshore Gulf of Mexico assets to Sanare Energy Partners LLC (“Sanare”). Sanare claimed the debtors failed to obtain consent for certain lease transfers from the Bureau of Ocean Energy Management (“BOEM”), which oversees drilling in Federal waters. Therefore, Sanare claimed, it was not the owner of those assets and thus not liable for any required plugging and abandonment (“P&A”) and decommissioning. Guess who got stuck with the tab? Yes, the debtors. The debtors subsequently sued Sanare for damages and won; the Texas Bankruptcy Court awarded them $8mm in May ‘24. A moral triumph but not much more: “As of the Petition Date, despite efforts by the Debtors to collect from Sanare, the amounts due and owing under the Sanare Judgment remain outstanding,” Perret writes.

Ouch. But that wasn’t the worst A&D disaster. In ‘22, Patriot Natural Gas LLC (“Patriot”) agreed to acquire the debtors’ East Texas Assets, only to discover after signing the purchase and sale agreement (“PSA”) that the wells had “significant casing pressure issues.” The debtors disagreed and refused to cure, according to Gibbs & Bruns LLP, Patriot’s litigation counsel. Patriot terminated the PSA and demanded its $11.5mm deposit back. The debtors accused Patriot of “willfully breaching” the agreement. Patriot sued the debtors, and the debtors counterclaimed back (the “Patriot Litigation”). “Following extensive discovery, motion practice and a bench trial,” the Texas State Court entered its decision on July 4, 2024. The court found in favor of the debtors with respect to a claim of fraud. A consolation prize, more or less. The Court found in favor of Patriot regarding the breach of contract. Patriot kept the $11.5mm deposit; the debtors got stuck with Patriot’s attorneys’ fees (“Patriot Decision”). The parties reached a settlement that fixed the size of the bill (Perret doesn’t specify other than “millions of dollars of liabilities”) and prevented Patriot from coming after the debtors’ assets until October 31. That’s like a thug telling you on Monday that he’ll be back on Friday to deliver a righteous a$$-kicking.

The board engaged in “careful consideration.” It didn’t take an abacus to determine there was no way out of the liquidity hole. It decided to put itself on the block again. On August 1, the entire board resigned, replacing itself with Jeremy Stillings as sole independent director to oversee restructuring efforts and “maintain the integrity of the sale process.” The debtors subsequently retained Cole Schotz LLC (Daniel F.X. Geoghan, Jacob S. Frumkin, Daniel J. Harris, Patrick J. Reilley, Melissa M. Hartlipp)(“lawyering is our art”) as legal counsel (“a curated collection of legal talent”)** and Eisner Advisory Group LLC (Allen Wilen) as financial advisor.

But wait – another sale process? Yes: for those troublesome East Texas Assets. Back in February, the board hired Detring & Associates LLC (“Detring”), a highly-regarded A&D shop founded by former Merrill Lynch backer Derek Detring, to run a “competitive auction process.” Detring assembled a list of 90 potential buyers and got busy. They secured sixty-five NDAs; sixty potential buyers viewed management’s presentation in the virtual data room.

Detring set an initial bid deadline of August 30. Eight submitted offers. Detring asked for a “second and best” by September 4. Three of the initial bidders and one brand-new bidder participated. The debtors negotiated with one party about serving as the stalking horse, but given the increasingly dire liquidity picture and the millions owed Patriot loomed ever larger, the debtors elected to file first and then finalize the stalking horse post-petition. “The Debtors anticipate seeking approval of appropriate bidding and sale procedures within the first two (2) weeks of these Chapter 11 Cases.”

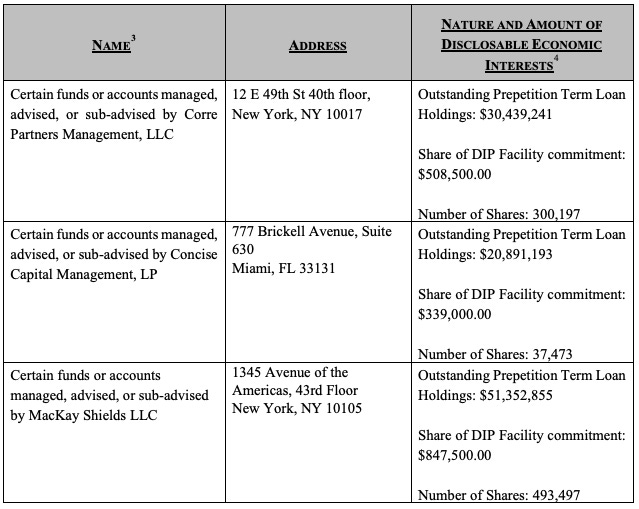

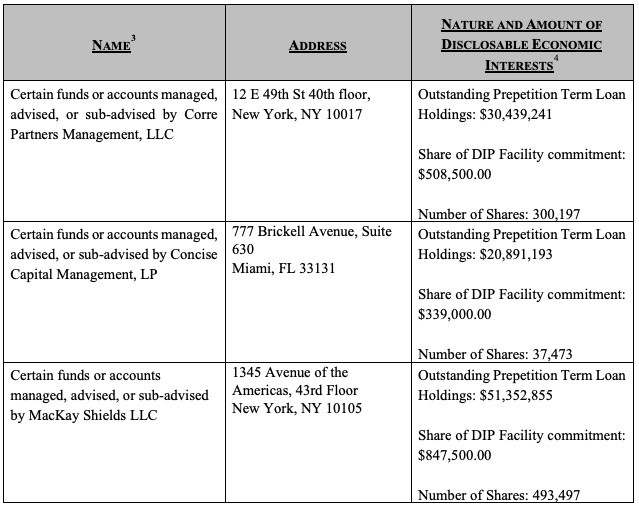

The debtors plan to fund the cases with cash collateral and a $14.2mm DIP provided by pre-petition lenders MacKay Shields, Corre Partners, Concise Capital Management and Mercer Investments, represented by Faegre Drinker Biddle & Reath LLP (Patrick A. Jackson, Sarah E. Silveira, James H. Millar, Laura E. Appleby, Drew M. Magee). The DIP facility comprises $1.695mm of new money, with $875mm on an interim basis; and a $12.5mm rollup of pre-petition obligations, with $2mm rolled on an interim basis and $10.4mm on a final basis. The facility bears interest of 8%, with a default rate of 10%. There is a 2% upfront fee and a 2% exit fee – both on the total amount of the DIP, including the roll-up portion, and a fee of 0.5% on the average daily unused amount.

Milestones call for the filing of the bid procedures motion no later than 10 days after the petition date (and approval no later than 28 days after), with a sale order and sale closing due within 79 and 85 days of the petition date, respectively.

The debtors obtained all requested relief at the first-day hearing on November 15, 2024, including the cash collateral/DIP motion. “I'm pleased to report, Your Honor, that we have a fully consensual interim DIP order” that incorporated and resolved comments from the U.S. Trustee, said Jacob Frumkin, one of the “legal artists” at Cole Schotz.*** A final hearing for the motions is set for December 12, 2024.

*In the Southern District of Texas. Judge David Jones presided over the cases.

**C’mon people, who the hell came up with this?

***Fire your marketing people, please.

Company Professionals:

Legal: Cole Scholtz (Daniel F.X. Geoghan, Jacob S. Frumkin, Daniel J. Harris, Patrick J. Reilley, Melissa M. Hartlipp)

Financial Advisor: Eisner Advisory Group LLC (Allen Wilen)

A&D Advisor: Detring & Associates LLC

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

PIK Notes Trustee: Computershare Trust Company NA

Legal: Emmet Marvin & Martin LLP (Thomas Pitta)

Ad Hoc Lender Group: MacKay Shields, Corre Partners, Concise Capital Management, Mercer Investments.

Source: Docket 39 Legal: Faegre Drinker Biddle & Reath LLP (Patrick A. Jackson, Sarah E. Silveira, James H. Millar, Laura E. Appleby, Drew M. Magee)