💥Another Retailer Bites the Dust💥

Stock+Field, Peabody Energy Corp., NYC Chains, & Neiman Marcus Feedback

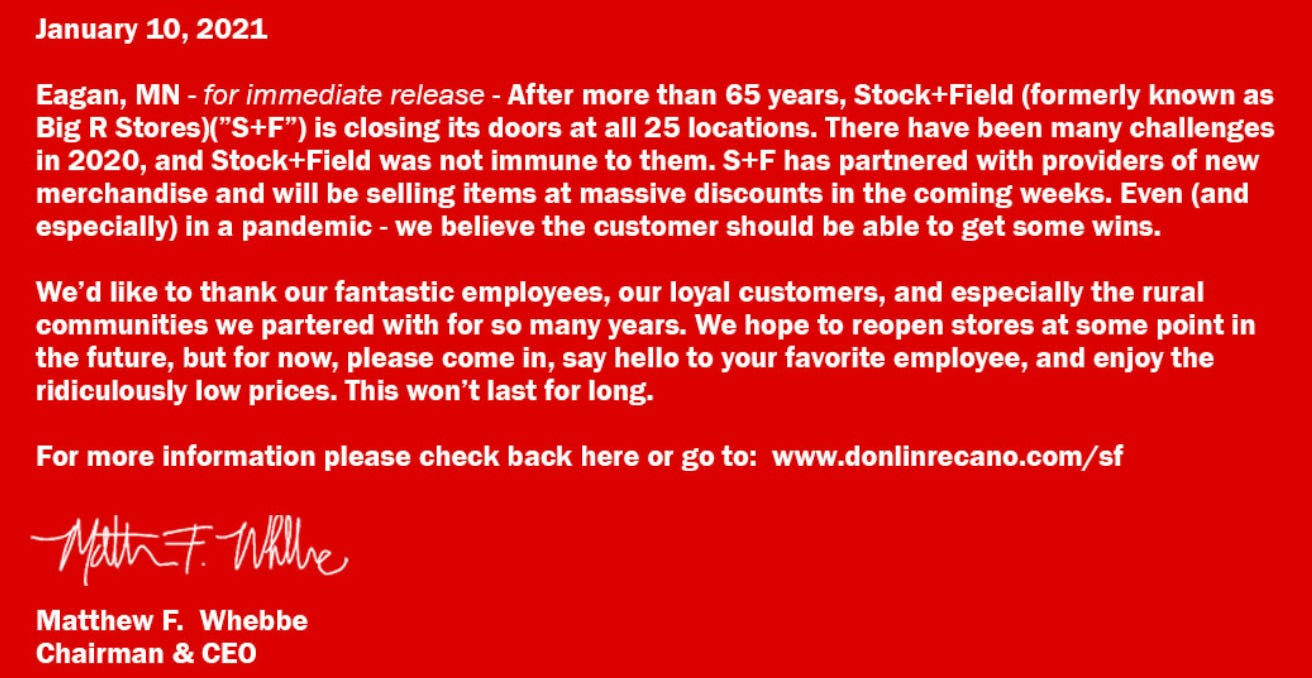

🚜New Chapter 11 Bankruptcy Filing - Tea Olive I LLC (d/b/a Stock+Field)🚜

The #retailapocalypse is indiscriminate. Sometimes it likes to take down big prey like J.C. Penney or J. Crew but other times it just wants to take the path of least resistance and snag some low hanging fruit. That means that a number of retailers those of us in our bubbles in maj…