💥Not Much to Smile About. Part II.💥

SmileDirectClub Inc. $SDC Files, an AppHarvest Update, and Mitchell Gold + Bob Williams

On September 29, 2023, SmileDirectClub Inc. ($SDC) and eight affiliates (collectively, the "debtors") filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez) — joining other distinguished companies like the Chicago Cubs, Marvel, Revlon and Delta Airlines Inc. ($DAL) that have leveraged the bankruptcy process to become bigger, badder and stronger (lol, totally on par guys, sure).

Or as @drwhitneyortho amusingly put it on Insta earlier this week, “Smile direct club got smoked out 😂 (I had to).”

That’s right. That’s ⬆️ an SDC retail location replaced by a smoke shop! Her caption stated:

“Extra extra! I noticed yesterday, by chance, that the smile direct club by my office got “smoked out” 😂

I must say that I am excited to see this turning point in the DIY orthodontic movement. I’ve seen too many unhappy endings there. I am hopeful that there is a renewed value and trust in dental professionals to provide quality care and treatment.

With gratitude, your fellow smile-loving orthodontist 🦷.”

Suffice it to say, real dentists f*cking hate this company.

We wonder how equity investors feel about it. Well, this is how the stock reacted on Friday after the filing:

And this is what’s happened since:

No meme stonk frenzy here, folks! Toilet seat pads from BBBY, sure. Teeth from SDC, no way!!

Anyway, we’ve written extensively about this one before …

… so what’s new that we can learn from the debtors’ bankruptcy filing? Let’s dive in ⬇️:

We’ll start with debtors’ counsel and New York Law Journal’s “Dealmaker of the Year,” Kirkland & Ellis LLP’s Joshua Sussberg. At the first day hearing on Monday, Mr. Sussberg made quite the opening statement, showing off his SmileDirect aligner and explaining how “it certainly works.” We love the anecdotal review, even if it might be slightly biased (and, for what it’s worth, we thought your pearly whites looked great already, Josh).

Despite the glowing review from Mr. Sussberg (an influencer outside of BK circles, he is not), the company has seen revenues drop dramatically partly due to accusations of “false advertising,” “common law fraud” and violations of “various state consumer protection statutes.” Not everyone was as satisfied with their SmileDirect experience as Mr. Sussberg, it seems. 🤷♀️

Pair customer complaints with the “bankruptcy basis bonanza” of (i) COVID-19, (ii) inflationary pressures, and (iii) the Ukraine-Russia War, and you end up with a highly levered company facing liquidity challenges.

By June 2023, the company engaged FTI Consulting Inc. (“FTI”), Centerview Partners LLC (“Centerview”), and Kirkland. Centerview started a financing process in July by reaching out to the company’s existing creditors, including HPS Investment Partners LLC (“HPS”), who were the lenders under the company’s credit facility, as well as third-party lenders and investors. Despite Centerview’s marketing efforts, no actionable proposals were received.

In the aftermath of the failed financing attempt the company decided to prep for a chapter 11 filing.

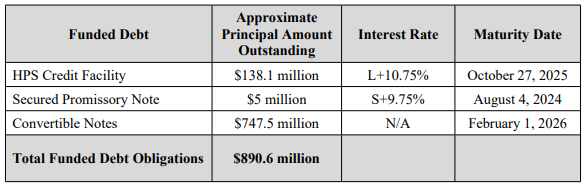

Here’s the company’s pre-petition cap structure:

We think the unsecured claimants list is worth looking at as well since the company has seemingly kicked a lot of professional services firms in the teeth (see what we did there?) in the run-up to chapter 11. Over 20% of the top 30 GUC list are advisers (pour one out for PJT Partners LP ($PJT), Skadden Arps Slate Meagher & Flom LLP, King & Spalding LLP, Troutman Pepper Hamilton Sanders LLP, Ernst & Young US LLP, Sullivan & Cromwell LLP, and Foley & Lardner LLP). There’s also a who’s who of tech companies on the top 30 list including Salesforce Inc. ($CRM), Alphabet Inc. ($GOOGL), Coupa Software and Amazon Inc. ($AMZN). And, most importantly, the second largest unsecured claimant is Align Technology Inc ($ALGN) to the tune of $63mm from an arbitration judgement against the debtors. We wrote about that in more detail here. All of which is to say that — even assuming none of the advisers sit on it — the official committee of unsecured creditors ought to have an interesting constitution here.

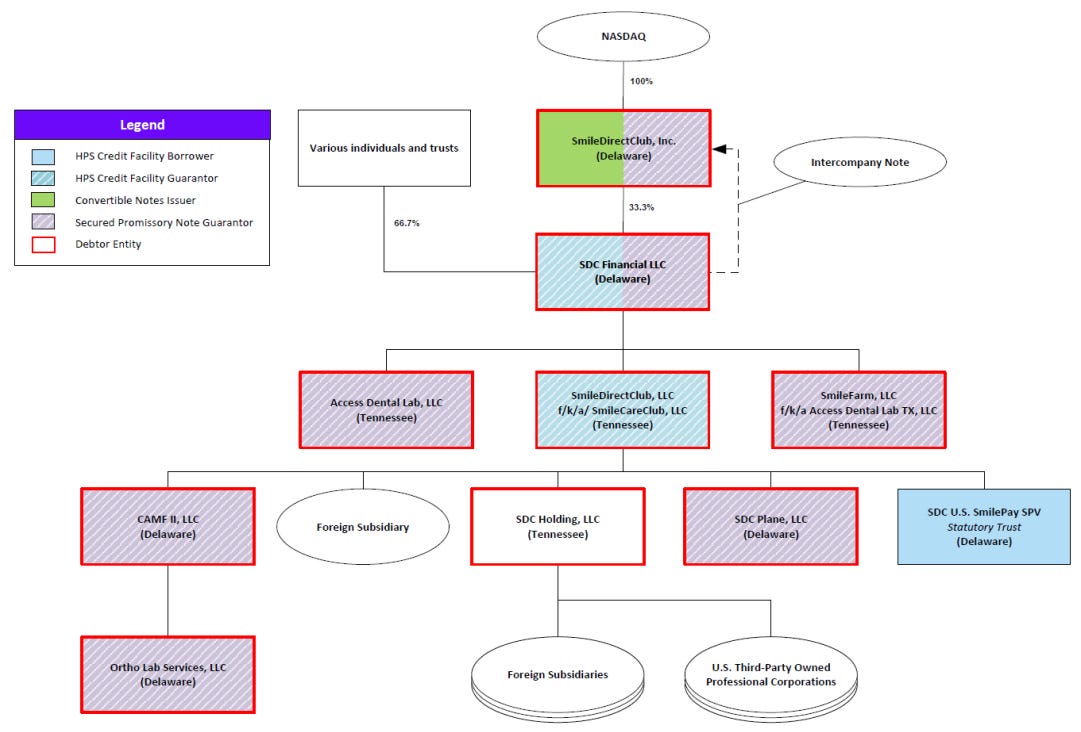

Prior to the filing, the company’s advisors were then tasked with the tough job of obtaining post-petition financing. We say tough here because the previously mentioned HPS credit facility sits at the company’s non-debtor subsidiary, SDC U.S. SmilePay SPV (the “SPV”). It also happens that almost all the company’s accounts receivables and intellectual property sits at the SPV level. This means that while the HPS credit facility was, and still is, happily secured by all these assets, any post-petition financing would not have a lien, thus, effectively, making them junior to HPS.

See below for the company’s org chart:

Absent any interest from third parties or HPS to provide any post-petition financing, the company turned to its founders to obtain an up to $80mm DIP and here are the highlights:

There’s a $20mm initial draw upon the entry an interim DIP order;

There’s a $30mm delayed draw on the 60th day after the petition date conditional on (i) a successful bid having been received and (ii) there has been no greater than a $7mm reduction in net cash flow over the first 60 days of the chapter 11 cases as compared to the DIP budget;

There’s a $5mm roll up of the founders’ secured bridge loan to the company;

There’s a $25mm accordion feature open to all holders of the convertible notes at the same terms as the DIP lenders ($10mm upon the interim draw and $15mm upon the delayed draw);

It carries a 17.5% PIK interest rate, a 5.0% draw fee, and a 5.0% exit fee; and

It features 90-day maturity unless the liquidation plan has become effective, then the DIP will remain outstanding for an additional 90 days.

Wait, liquidation plan? Yep, if the company fails to secure a successful bid in 60 days (aka the delayed draw conditions have not been met) then a liquidation plan comes in full force. There’s even a minimum liquidity covenant of $2.5mm on the DIP to be used as a wind-down budget just in case.

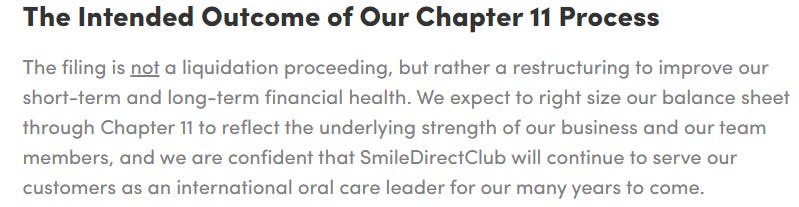

The company’s press release emphasizes that this is “not a liquidation proceeding”… yet.

Of course, the company also had to get permission from HPS with regards to the DIP. And so we get to the HPS Forbearance Agreement. The agreement has HPS waive a variety of default conditions and covenants prohibiting the incurrence of the DIP. In exchange, the debtors agree to true up the borrowing base securing the HPS credit facility through cash payments to a restricted account at the SPV.

So, does a white knight come in to pay for a company whose reputation and financials have been dragged through the mud? Or does this thing go to liquidation and we end up seeing pennies on the dollar for plastic teeth molds… stay tuned.

The debtors are represented by Kirkland & Ellis LLP (Joshua Sussberg, Rachael Bentley, Spencer Winters, Maddison Levine, Charles Sterrett, Patricia Lane, Michael Esser, Mark McKane) and Jackson Walker LLP (Matthew Cavenaugh, Rebecca Blake Chaikin, Emily Meraia, Genevieve Graham) as legal counsel, FTI (Daniel Wikel) as financial advisor, and Centerview (Ryan Kielty) as investment banker. HPS is represented by Latham & Watkins LLP (David Hammerman, Andrew Sorkin) and Porter Hedges LLP (John Higgins, M. Shane Johnson, Megan Young-John). An ad hoc committee of convertible noteholders is represented by Paul Weiss Rifkind Wharton & Garrison LLP (Jacob Adlerstein, Brian Bolin, Douglas Keeton, Tyler Zelinger) and Gray Reed (Jason Brookner, Lydia Webb) while the notes trustee, Wilmington Trust NA, is represented by Seward & Kissel LLP (John Ashmead, Andrew Matott). Finally, ALGN is represented by Saul Ewing LLP (Lucian Murley, Jorge Garcia) and Sherrard Roe Voigt & Harbison PLC (Michael Abelow).

💥Harvesting an Epic Beatdown. Part II.💥

Welcome back to the circus that is AppHarvest Inc. ($APPH now $APPHQ) and if you’re wondering why you’re reading about this sh*t stain case yet again, take comfort in the fact that we’re wondering why we’re writing about this sh*t stain case yet again. It is what it is.