💥Not if, but how much💥

Updates Galore + Rhodium is the latest crypto sh*tshow to file.

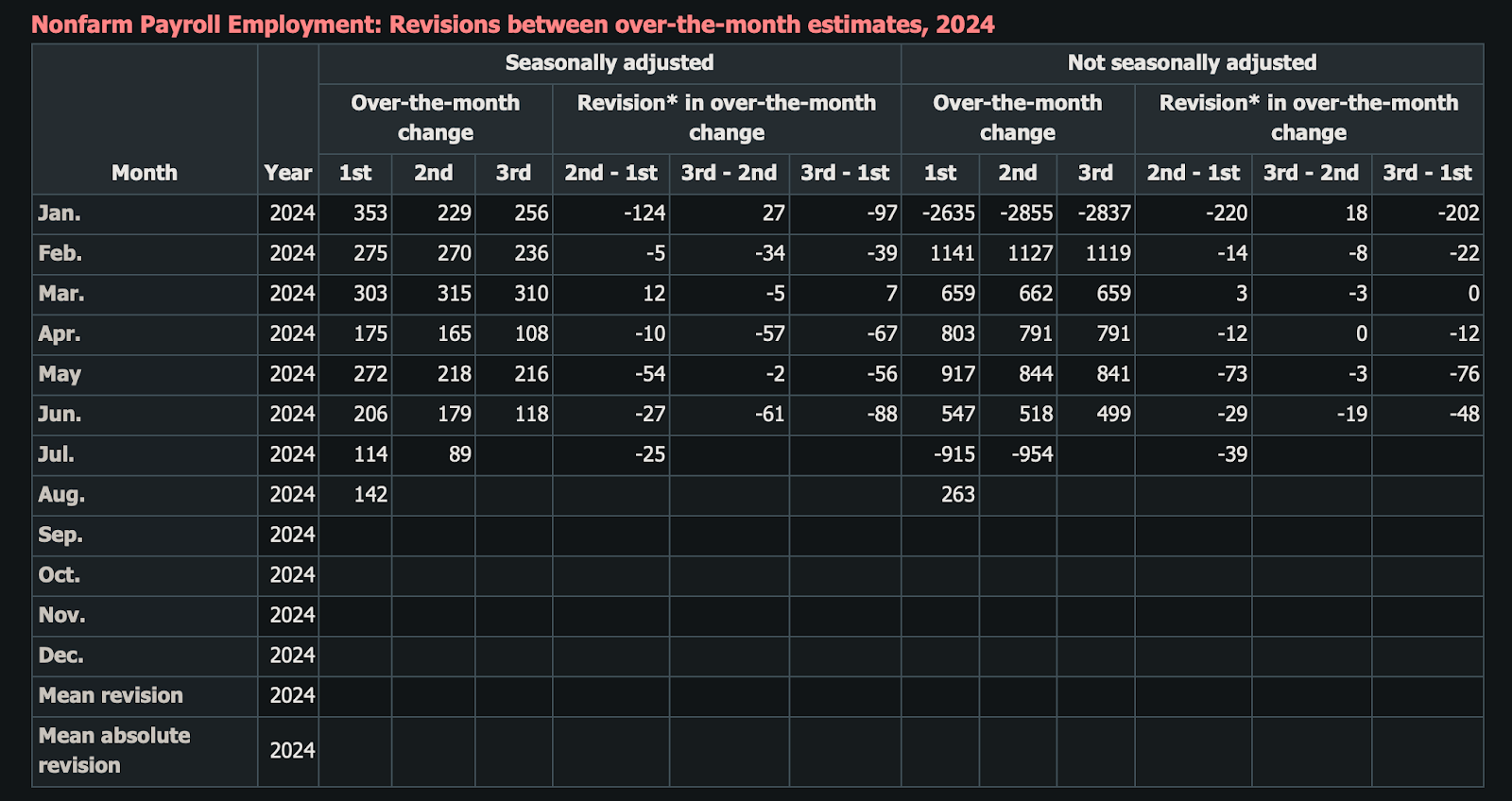

Answered prayers, it’s been said, are far worse than unanswered ones. Dubious theology, perhaps, but one wonders. For nearly a year the markets have been hoping, demanding, pleading, clicking its ruby slippers together and praying for the Fed to do something. And now, all signs and Fedspeak point to a rate cut in September. 25bps or 50bps? Payrolls were weaker than expected in August: a gain of +142k compared to 161k consensus. And as usually happens: more revisions, with July’s print “revised” to 89k, and June to 118k. And by “revised” we mean revised lower, of course:

We post this not simply to poke fun at our friends at the US Bureau of Labor Statistics (“BLS”), but because it supports the idea that the economy may very well be weaker than suggested by government statistics. In August, you’ll recall, the BLS completed its annual “benchmark revisions” of its payroll data; it discovered that the U.S. created 818k fewer jobs in the 12-month period ending in March than it, the BLS, had originally estimated. Whoopsies: just a small miscalculation, LOL.

So the labor market, this theory goes, isn’t simply softening, it’s weak and the all-important Great American Consumer, the driver of the debt-driven economy, is hurting. Need proof? Dollar General Corp. ($DG):

On August 29, DG’s shares plunged the most on record after the company reported horrific second-quarter earnings. On the subsequent call, CEO Todd Vasos said the chain’s core consumer was “less confident” in their financial position, which over the past six months worsened due to “higher prices, softer employment and increased borrowing costs.” The company also noted that “shrink” — aka shoplifting — was on the rise. It seems Johnny’s photo, which we originally shared back on August 24, 2024, was portentous. It seems, sadly, that the lower-income consumer’s Uber has arrived: