🚨New Chapter 11 Bankruptcy - Wellpath Holdings Inc.🚨

Healthcare provider to correctional facilities files with $644mm of debt, plan to sell.

Back on November 11, 2024, Nashville-based and H.I.G. Capital LLC-owned Wellpath Holdings Inc. (“WHI”) and 38 affiliates (collectively, the “debtors” and, along with certain non-debtor affiliates, “Wellpath”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Perez). Wellpath is a “…provider of localized, high quality, compassionate care to vulnerable patients in challenging clinical environments” which is a super delicate way of saying that it is a medical and mental health services provider to people in correctional facilities, inpatient and residential treatment facilities, forensic treatment facilities, and civil commitment centers. The debtors operate three divisions (“Recovery Services,” “Local Government” and “State & Federal”)* in ~420 facilities across 39 states, serving ~200k patients daily. Just when Sam Bankman-Fried thought he could avoid the long-arm of the bankruptcy process, we imagine he’s sitting there in his prison cell getting dropped a “notice of commencement” leaflet between bars, lol. Perhaps his roomie Diddy can make bankruptcy the subject of his next jam, 😜.

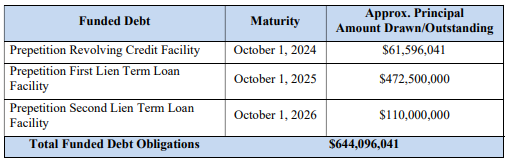

The debtors, like most of the others we’ve reviewed in ‘24, suffered from increases galore. Like, ⬆️ operating and labor expense, ⬆️ insurance expense, and ⬆️ interest expense. The debtors also struggled to either make money off of existing contracts or maintain contracts and the wheels basically came off in ‘23.** These were not favorable trends going into a debt maturity — specifically, an October ‘24 debt maturity on the debtors’ pre-petition RCF. Basically this situation was a perfect storm of 💩.

And so the debtors — with an army of restructuring professionals in tow — spent the entirety of ‘24 trying to source an out-of-court solution to address their growing liquidity problem and RCF maturity problem; they brought on Lazard Freres & Co. LLC ($LAZ)(Christian Tempke) and healthcare banking specialist MTS Health Partners (“MTS”)(Jason Schoenholtz) to conduct a marketing process of their behavioral health division, “Recovery Solutions,” with the hope that the proceeds could pay down the RCF and better situate the debtors for an extension of other debt.

That. Clearly. Did. Not. Happen.

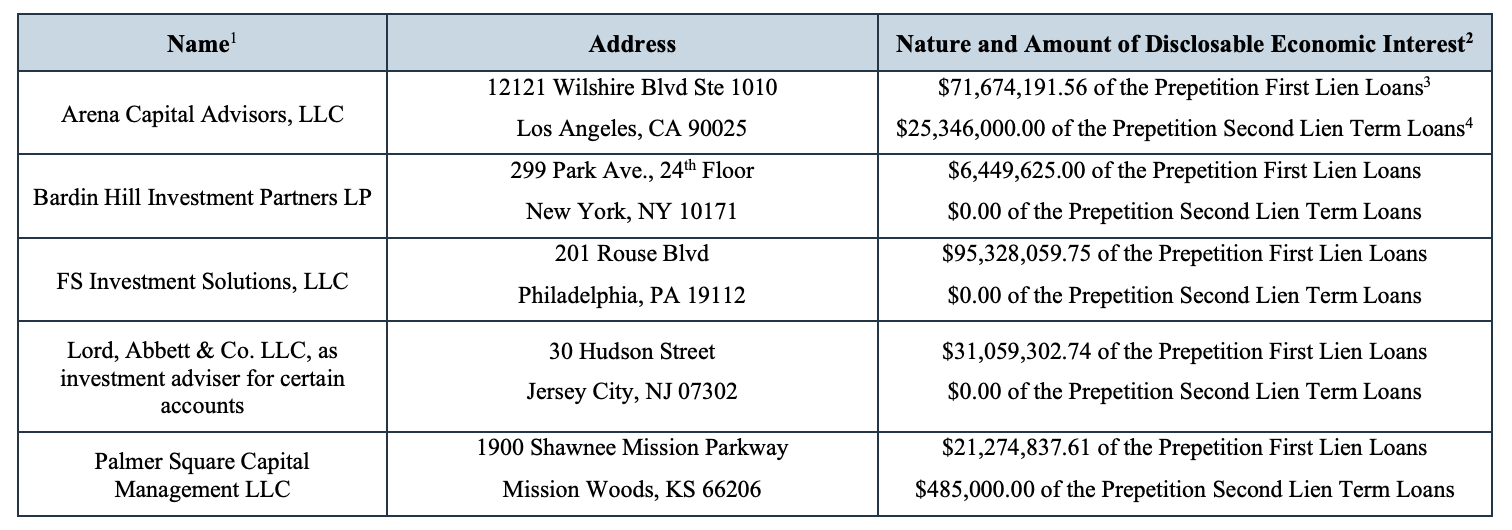

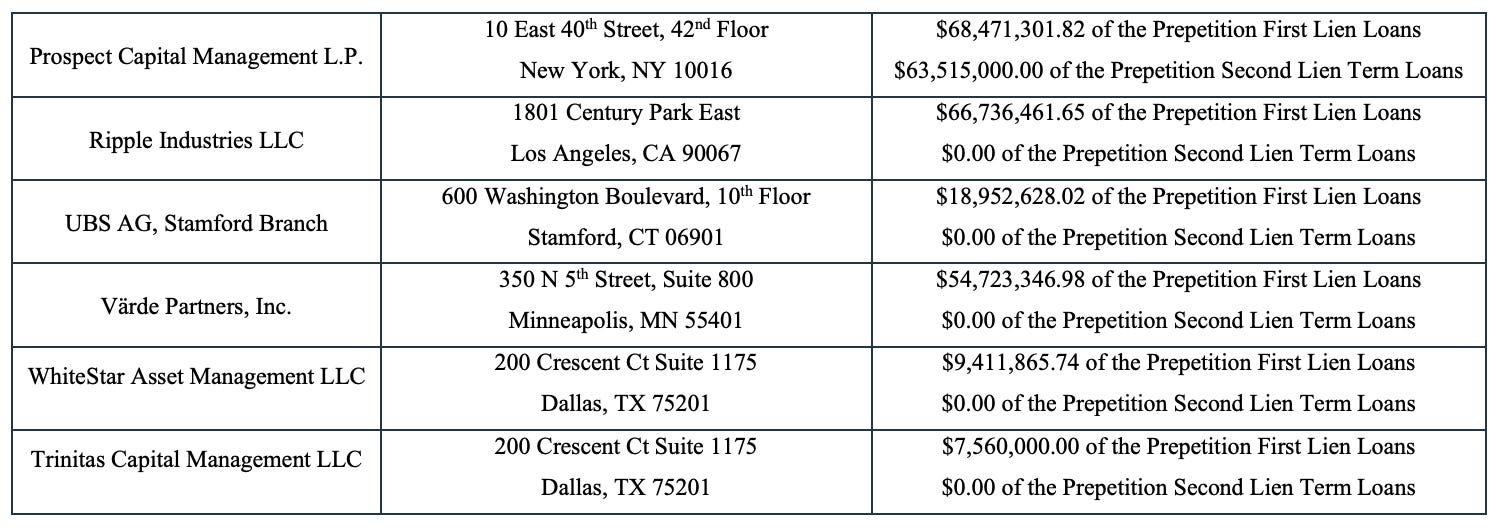

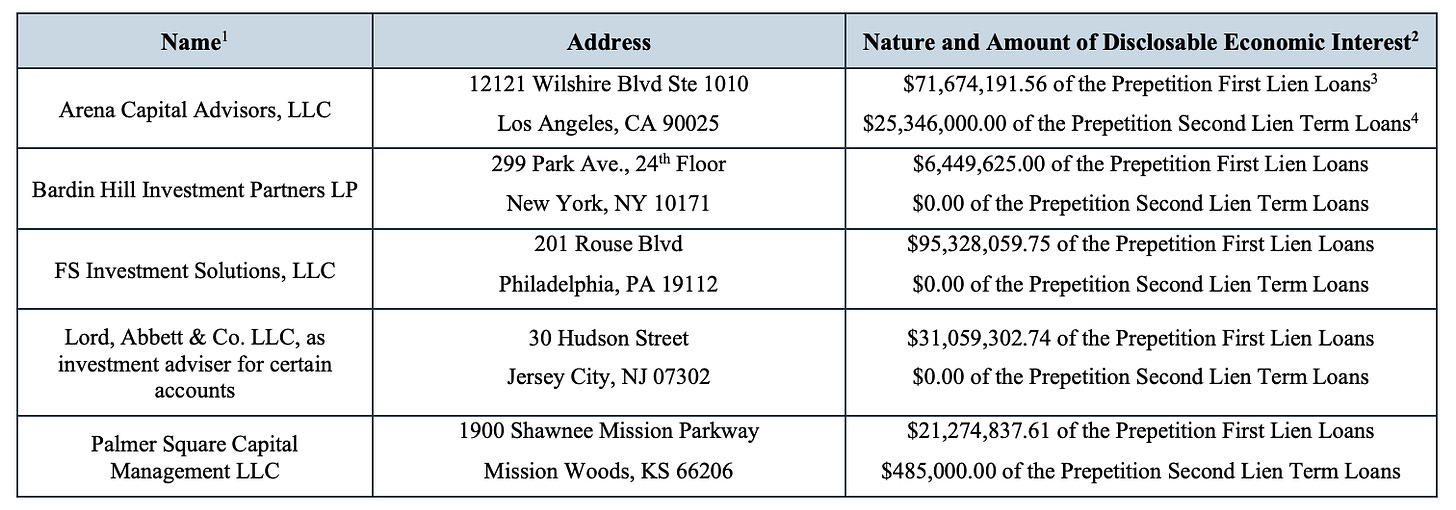

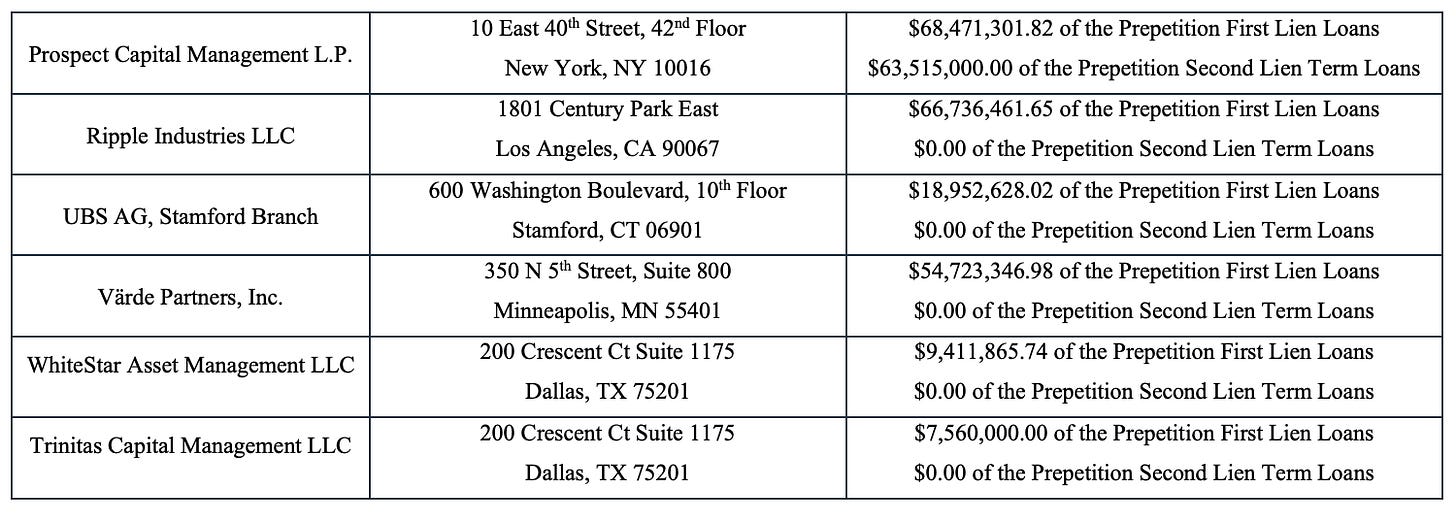

And so the debtors found their way into chapter 11 bankruptcy, with a restructuring support agreement (“RSA”) (i) agreed to by the debtors and an ad hoc group of lenders composed of eleven funds: Arena Capital Advisors LLC, Bardin Hill Investment Partners LP, FS Investment Solutions LLC, Lord Abbett & Co. LLC, Palmer Square Capital Management LLC, Prospect Capital Management LP, Ripple Industries LLC, UBS AG, Värde Partners Inc., WhiteStar Asset Management LLC, and Trinitas Capital Management LLC (the “ad hoc group”), and (ii) backed by about 85% of the debtors’ first lien lenders and over 80% of their second lien lenders.

Despite some bumps along the way, the debtors’ cases have progressed remarkably smoothly so far, in large part due to the apparent constructive approach taken by the debtors, the ad hoc group, and their professionals. Here are the highlights of the relief the debtors requested and subsequent developments:

📍DIP Facility. As contemplated by the RSA, the debtors sought approval of a $522,375,000 DIP facility composed of (i) a $105mm syndicated-to-all-lenders-postpetition-but-backstopped-by-the-ad-hoc-group new money component and (ii) a $417,375,000 prepetition secured loan roll-up (a 3.975:1 ratio). HOT DAMN, THAT’S AN AGGRESSIVE ROLL-UP. See, also, Franchise Group Inc. Significantly, the proposed roll-up would have subsumed a hefty portion of the total amount of the debtors’ prepetition funded debt:

But unfortunately for the ad hoc group, that roll-up didn’t sit so well with the US trustee (the “UST”), who lobbed in an objection at the first day hearing. The solution?

The debtors and the lenders punted on the issue, agreeing to a much less offensive interim roll-up of 2:1 on new money actually funded but reserving their rights to fight for the full, much more aggressive roll-up at the second day hearing. During that interim period, the UST appointed a 10-member official committee of unsecured creditors (the “UCC”),*** and rather than have a contested DIP hearing, the lenders agreed (and no one else objected) to a final roll-up of 2.45:1, bringing it down to a total of $257,250,000 – over $160mm less!

The final DIP order also limited the DIP lenders’ credit bid right to the Recovery Solutions division of the debtors’ business (subject to a cap to be agreed among the lenders, the debtors, and the UCC, in a last ditch effort to drum up a competing bid), leaving cold hard 💸💸💸 as the only option for a Local Government or State & Federal business bid and, following the closing of the sale of the Recovery Solutions business, the DIP will be deemed satisfied in full (after which the prepetition lenders step in as the relevant consenting parties with respect to cash collateral usage). Honestly, what a compromise by the lenders!

📍Bid Procedures Motion. Shortly after their cases filed and to comply with the RSA’s timeline, the debtors teed up an emergency motion for approval of (i) fast-track sale procedures for the Recovery Solutions business (culminating in a sale hearing a mere six weeks after filing) and (ii) a slightly elongated sale process for their Local Government and State & Federal divisions (with sale hearings to happen around February 4, 2025).

As suggested above, the DIP lenders are serving as a stalking horse for the Recovery Solutions business. As for the other two divisions, the lenders propose to purchase new equity interests in reorganized Wellpath via a direct private placement pursuant to a plan, subject, of course, to the aforementioned bid procedures and a 363 sale process and with respect to which the UCC reserved all rights.****

Notwithstanding the debtors’ aggressive timeline, the UST didn’t object, and the court quickly approved the motion on November 18, 2024. But shortly after being formed, the UCC petitioned the court to pump the brakes on the Recovery Solutions sale — as always, more time was needed and, after all, it’s the holidays, 🙄. But after some conversations among the parties, all was well once again — the court entered a new, consensual bidding procedures order kicking out the Recovery Solutions dates by about a week, subject to certain automatic extensions, which have since occurred.***** Bids for the Recovery Solutions business were due on January 6, 2025, with a sale hearing slated to take place later today, January 8, 2025.

📍Bar Date Motion. As most of our readers know, bar date motions are pretty routine and typically don’t get a lot of attention. That wasn’t the case here: given the unique situation in which many of the debtors’ creditors find themselves (you know, behind bars), the bar date motion received some unexpected commentary, namely, from the Center for Constitutional Rights, the Human Rights Defense Center, Public Justice, and Rights Behind Bars, who bandied together and filed an amicus brief. That brief noted what might be considered obvious on reflection: (i) mail service in prisons and jails sucks and requiring the incarcerated, who don’t have regular postal service access or any internet access, to return proofs of claim within 30 days was a bit much and (ii) documents full of legalese can be difficult to understand even for those out there who spent 3 years in law school.

To their credit though, the debtors and the UCC bent over backwards to address their concerns and revised the materials to generally make it easier for those individuals to understand what they need to do and get their claims on file, including by (i) kicking out the deadline to file from 30 to 100 days post-service, (ii) allowing claims to be filed English or Spanish, and (iii) streamlining the process by which relevant debtors are identified.

📍Stay Extension and Relief Motions. Oh boy, are these both messy and fun. Because Wellpath contracts with government entities and provides health services to individuals in — we’ll say — less than ideal environments, they and many of the folks they’ve ever been associated with, including their equity sponsor H.I.G., their D&Os, and doctors, have been on the receiving end of a variety of claims and lawsuits, including “1983 claims.” For those that don’t dabble in that area of the law, 42 U.S.C. § 1983 lets individuals sue for violations of their constitutional rights, such as, for example, denying them necessary medical services while incarcerated. What kind of violations have (allegedly) occurred? About as bad as you can imagine. Here’s what one court found in a prepetition lawsuit:

“[T]here was an avalanche of evidence presented to the jury that [one debtor’s] deliberate indifference [in addressing a patient’s medical needs] caused the constitutional violations inflicted on [her], resulting in her pain, suffering, and death.”

But because the lawsuits involve non-debtors and could result in debtor indemnity obligations, the erosion of insurance policies, and the like, the debtors endeavored to “extend” the automatic stay to certain of their non-debtor affiliates and equity sponsor during their chapter 11 cases.******

The court approved the relief on an interim basis without much fanfare, but understandably, not everyone is on board with this approach: the docket is littered with letters to the court (some, handwritten), objections, and even some motions to lift the automatic stay for lawsuits to proceed. The debtors have been scrambling to get ahold of the various parties, not all of whom have been quick to respond (see mail service point ⬆️), and the court will hold a hearing to figure all this out on January 14, 2025.

While these cases have undoubtedly presented some curveballs and been rockier than the debtors might have liked, it’s way less of a sh*t show than it could have been — kudos to the debtors, the ad hoc group, the UCC, and all of their professionals. We’ll keep you posted on any interesting updates as the cases progress.

The debtors are represented by McDermott Will & Emery LLP (Felicia Perlman, Bradley Giordano, Steven Szanzer, Marcus Helt) as legal counsel, FTI Consulting Inc. ($FCN) (Timothy Dragelin) as CRO and financial advisor, and the aforementioned LAZ and MTS as investment bankers. The UCC is represented by Proskauer Rose LLP (Brian Rosen, Ehud Barak, Daniel Desatnik, Paul Possinger) and Stinson LLP (Nicholas Zluticky, Zachary Hemenway, Lucas Schneider) as legal counsel and Huron Consulting Services LLC (Ryan Bouley) and Dundon Advisers LLC (Matthew Dundon) as financial advisor.******* UBS AG, as prepetition first lien agent, prepetition second lien agent, and DIP Agent, is represented by Cahill Gordon & Reindel LLP (Joel Levitin, Jordan Wishnew) and Norton Rose Fulbright LLP (Robert Bruner, Maria Mokrzycka) as legal counsel. The ad hoc group is represented by Akin Gump Strauss Hauer & Feld LLP (Scott Alberino, Kate Doorley, Marty Brimmage) as legal counsel, Ankura Consulting Group LLC as financial advisor and Houlihan Lokey Capital Inc. ($HLI) as investment banker. Finally, H.I.G. is represented by Akerman LLP (Eyal Berger, Evelina Gentry, Jason Oletsky) as legal counsel.

* In terms of size, the debtors’ Local Government division was the most lucrative in ‘23, followed by its State & Federal division and its Recovery Solutions division. All three, however, have suffered revenue setbacks in ‘24.

** It seems the debtors’ State & Federal division lost three contracts in ‘24 that accounted for over $440mm of annual revenue, 😬.

*** The UCC is composed of (i) Scott Allen for the estate of Brady Allen, (ii) Correct Rx Pharmacy Services, Inc., (iii) Ryan Curtis, (iv) Diamond Drugs, Inc., (v) Angela Hoyle, (vi) Elizabeth Naranjo for Estate of Cristo Canett, (vii) Teesha Ontiveros for the estate of Frankie Jacquez, (viii) Select Medical Corporation, (ix) Wellstar MCG Health, and (x) David Ryan Rood – that’s quite a bit of inmate representation!

**** This outcome is embodied in a plan filed by the debtors in late December ‘24 [Docket No. 564]. In many respects, it’s a placeholder while the sale process plays out and does not include information on projected recoveries or the specific assets to be distributed to unsecured creditors. A hearing to consider approval of the corresponding disclosure statement (Docket 566) is scheduled for January 28, 2025, so expect to see revisions in the coming weeks.

***** When and how these extensions are triggered is damn murky. The bidding procedures tie the extensions to updates on a fugly website maintained by COMMBUYS (Massachusetts’ official procurement record system), even though the debtors have operations in 38 other states. Luckily, the debtors filed a notice clearing up our confusion.

****** As the UST pointed out at the first day hearing, this relief is not so much an “extension” as a new injunction, which requires an adversary proceeding. The judge declined to rule on that issue until the final hearing.

******* It’s not clear why the UCC needs two financial advisors, although each swears up and down it won’t duplicate any efforts by the other. Notably, Dundon’s retention application includes services that appear legal in nature (e.g. “Analysis of … attachment and perfection of liens,” “Analysis of … bar date orders, claims solicitation and receipt procedures and their implementation”).

Company Professionals:

Legal: McDermott Will & Emery LLP (Felicia Perlman, Bradley Giordano, Steven Szanzer, Marcus Helt)

Board of Managers: Jorge Dominicis, Louis Hallman, Valerie Montgomery Rice, Justin Sapolsky, Rob Wolfson, Kevin Van Culin, Michael Kuritzky, Patrick Bartels, Carol Flaton

Legal: McDonald Hopkins LLP (David Agay)

Financial Advisor/CRO: FTI Consulting Inc. (Timothy Dragelin)

Investment Banker: Lazard Freres & Co. LLC (Christian Tempke, Daniel Klodor, Jennifer Wild) + MTS Health Partners (Jason Schoenholtz)

Claims Agent: Epiq (Click here for free docket access)

Other Parties in Interest:

Pre-petition First Lien & Second Lien & DIP Agent: UBS AG Stanford Branch

Legal: Cahill Gordon & Reindel LLP (Joel Levitin) and Norton Rose Fulbright LLP (Robert Bruner, Maria Mokrzycka)

Stalking Horse Purchaser: RS Purchaser LLC

Ad Hoc Group of Lenders

Source: Docket 54 Legal: Akin Gump Strauss Hauer & Feld LLP (Scott Alberino, Kate Doorley, Marty Brimmage)

Financial Advisor: Ankura Consulting Group LLC

Investment Banker: Houlihan Lokey Capital Inc.

Sponsor: HIG Capital LLC

Legal: Akerman LLP (Eyal Berger, Evelina Gentry, Jason Oletsky)

Statutory Unsecured Claimholders’ Committee

Legal: Proskauer LLP (Brian Rosen, Ehud Barak, Daniel Desatnik, Paul Possinger) and Stinson LLP (Nicholas Zluticky, Zachary Hemenway, Lucas Schneider)

Financial Advisors: Huron on Consulting Services LLC (Ryan Bouley) and Dundon Advisers LLC (Matthew Dundon)