☢️ New Chapter 11 Bankruptcy - Ultra Safe Nuclear Corporation ☢️

Another bankrupted company, another proposed asset sale.

On October 29, 2024, TN-based Ultra Safe Nuclear Corporation and three affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Owens). The debtors are “a global leader and vertical integrator of nuclear technologies and services, on Earth and in Space,” according to the first-day declaration of interim CEO Kurt A. Terrani. They have also, as we shall see, suffered a dramatic Chernobyl-style meltdown of liquidity after their anchor investor bid farewell to this vale of tears.

Which is odd, isn’t it? Nuclear is enjoying a renaissance: everybody’s talking nukes these days. There’s the ever-increasing possibility of a civilization-canceling nuclear conflagration, of course, but the bigger deal is the gargantuan, prodigious, mammoth supply of power demanded by Artificial Intelligence. Which comes at the worst possible moment, right when we’re shutting down the coal-fired plants and working to ban the sale of internal combustion engines because we’re still (right, guys?) dedicated to Zero-Carbon (let’s see some enthusiasm) by 2040 … and damn it, wind and solar just aren’t there yet. We wrote about this trend: Microsoft ($MSFT) reboots Three Mile Island; data centers are a Big Thing. Nukes are zero-carbon, so Larry Fink says it’s OK for you to deploy some dry powder there. It’s the Nuclear Moment, right?

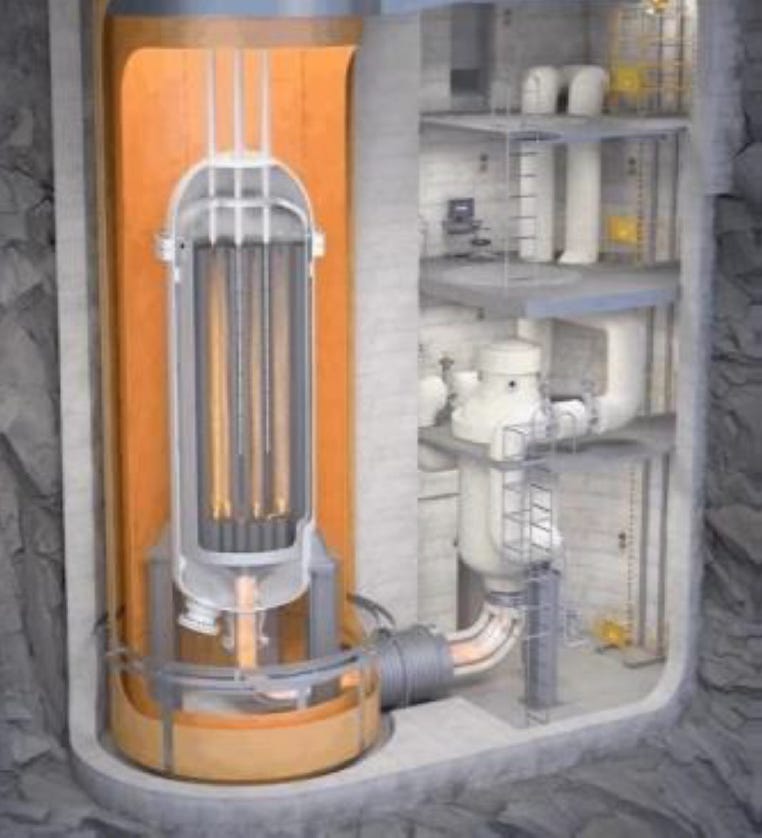

A moment tailor-made for the debtors, one would think. Founded in ‘11 by Dr Francesco Venneri, former CEO and current chief science officer, the debtors initially sought to commercialize the technology for Fully Ceramic Micro-encapsulated (FCM®) nuclear fuel (“FCM Fuel”), co-invented by Dr. Venneri. They are also developing the Micro Modular Reactor (MMR®) (the “MMR”) along with power and propulsion technologies for the defense industry and space exploration. FCM Fuel looms largest among these projects. “FCM Fuel consists of Tri-structural ISOtropic (“TRISO”) fuel particles embedded inside a silicon carbide matrix.” Just nod your heads, folks.

The debtors have “developed unique and proprietary commercial scale equipment” to produce these sinister yet Gaia-saving globules, much of it housed in their Pilot Fuel Manufacturing Facility in Oak Ridge, Tennessee. The facility was once used by the Manhattan Project, Terrani announces proudly, and is now the “largest commercial-scale TRISO production facility anywhere in the United States.”

Commercial scale? Are we really there yet? Anyway, FCM Fuel is the logical power source for the debtors’ MMR:

Now, just think about the MMR as a “‘nuclear battery,’” with 15.7 billion kilowatt- hours of thermal energy (kWth) during its lifetime,” Terrani writes. The MMR boasts any number of forward-looking features. It’s modular, you can build it with off-the-shelf parts, and it does not require water or an electrical grid or infrastructure. “The MMR’s ability to provide reliable but variable baseload power also makes it an ideal complement to other forms of renewable energy (such as wind and solar) to create new and more efficient renewable micro grids.” In other words: if you’re building a wind/solar plant, make sure you get a MMR for backup power. Nuclear is reliable; the wind and sun are more fickle.

The MMR is currently in the licensing stage with authorities in the U.S., Canada and the U.K. But there’s a lot more FFM Fuel can do besides feed the MMR. It’s suitable for most reactor types. The debtors once created a special version for the National Aeronautics and Space Administration, “…as the agency seeks to develop technologies for nuclear-powered space propulsion.”

That came as a surprise. Who knew NASA was still in the “space exploration” business? Well, Houston, the debtors have you covered. First up is the Nuclear Thermal Propulsion Engine (“NTP”), which uses nuclear fission to heat up a gas, which is then spit through a nozzle to produce thrust. Terrani says it will get astronauts to Mars “significantly faster” than chemical propulsion, “thereby decreasing astronauts’ exposure to cosmic and solar radiation.”

The thing — which bears a suggestive resemblance to the Monolith from Stanley Kubrick’s classic 2001: A Space Odyssey — is a “10-ton class micro reactor that builds on the MMR and FCM Fuel technologies.” This puppy is built for travel too; it is particularly suitable for “off-grid locations” … which is to say, it is “…a viable solution to provide critical energy to defense applications such as the U.S. military’s forward operating bases.” The screenplay writes itself: you and your regiment of Space Grenadiers are underway in your NTP-powered space fleet to some distant galaxy to … defend democracy, or something. The troops gotta have their Netflix and Instagrams. What better to charge those gadgets than a Python or two? The debtors understand the assignment, as the kids say.

All so ultra-cool. “Dream big,” we’re told, and by damn, these debtors did. But sometimes there’s this lag between the dream and when the eagle screams (aka, the conversion of dreams into hard cash). Sure thing, the debtors are “actively engaged” with NASA, the Department of Energy (“DOE”) and the Department of Defense (“DOD”). “However, aside from the Pilot Fuel Manufacturing Facility for production of FCM Fuel and TRISO particles, many of the Debtors’ products are still being developed, and, as a result, the Debtors’ historical revenue is low compared to operating losses.” Well, we were wondering about that “commercial” reference. So how bad is it? In ‘23, the debtor booked $6.15mm of revenue compared to $81.2mm of expenses. In ‘22, revenues were $5.75mm, with operating expenses just short of 10x that, at $53.9mm.

The debtors historically depended on outside investors for funding, Terrani writes. And they were fortunate enough to have found a devoted, motivated and well-heeled backer: Richard Hollis Helms. Maybe he was a science-fiction fan. He sunk some $100mm of equity into the debtor. That equity is held by USNC Investment LLC, a non-operating SPV (“USNC”). Helms, through USNC, also loaned the debtors roughly $24.5mm under a senior secured convertible promissory facility (the “prepetition secured note”), under which $28.2mm of principal and interest remained due as of the petition date.

That’s a lot of money.

Who is this dude?

“Richard Hollis Helms believed in the Debtors’ inventions and their mission to provide reliable and safe zero-carbon energy anywhere.” Note the tense.

The late Richard Hollis Helms, alas.

The U.S. lost a true patriot and hero in March ‘24, but he lived a life that qualifies him as the World’s Most Interesting Man, next to which the likes of Napoleon Bonaparte are but pale caricatures.

That’s the picture painted by Helms, or whoever did his obituary: an “aviator, spy, entrepreneur, mentor, venture capitalist,” he joined the Central Intelligence Agency (“CIA”) as a security guard in the early ‘70s. He parlayed that into a thirty-year hitch at an agency whose blunders, failures and ineptitude — the Bay of Pigs, the Iranian Revolution, the collapse of the Soviet Union, 9/11, Iraq and there is much, much more — should be far better known than they are (as should be, on the flip side, the successes). His fellow agents considered him a “rock star.” But he wanted more, more, more:

"Upon retirement he entered the private sector where he encountered an inflexible corporate structure unable to utilize his skillset. When the agency did not call on his and his colleagues' profound expertise after 9/11, he founded Abraxas Corporation for which he won the 2006 Ernst and Young National Entrepreneur of the Year Award for Emerging Technology. 10 years after it was created, Richard sold Abraxas and started Ntrepid Corporation which is still successfully developing cutting-edge software to save the world."“Save the world,” huh? How’d that go for you and your pals, Helms? Abraxas, you may recall (lol, jk), was an early entrant in the “intelligence contracting” industry — entities created, cynics might say, for the sole purpose of scarfing down the billions made available by the Patriot Act. This is what Ntrepid claims to do: “…managed attribution technology solutions for the national security community.” Well, we did wonder where Helms got his millions, and now we know.

Helms had suffered various illnesses, Terrani writes, so in ‘22, they began working with Citibank NA ($C) to line up another sugar daddy. Citi knocked on the doors of “asset managers, pension funds, utilities, family offices, large IT companies, corporate investment funds, and various other private equity funds.” Plenty of interest, but all contingent on the debtors’ obtaining an anchor investor, Terrani said. They found one, but this investor was unable to raise sufficient funds. A Canadian labor pension fund kicked in $18mm, but that was it. By early ‘24, liquidity, or its absence, was reaching crisis proportions.

Helms had been board chairman. Dr. Venneri served as the board. When Helms died, the debtors reconstituted it: they added three new directors, asked Dr. Venneri to resign (which he did, effective July 31) and appointed Tanneri as Interim CEO on August 2. The new board’s task was obvious: address the liquidity issue. They retained advisors, including Intrepid Investment Bankers LLC (“Intrepid”). The board tasked Intrepid with drumming up the financing to carry them through a sales and marketing process. Intrepid contacted 38 lenders — a process hampered by the debtors’ “lack of operating history, existing capital structure, and lack of traditional working capital collateral” — but nevertheless managed to identify a helpful lender.

Some of Helms’ old pals at Langley, looking to honor the “rock star’s” memory? A CIA front company, some sort of United Fruit Company for the new millennium? No, JMB Capital Partners LLC, which agreed to provide financing of up to $23mm. The package consisted of a $8mm bridge loan and $15mm of new money DIP financing, with $10mm available on an interim basis. The facility bears interest at 14% and carries a 6% exit fee. The $8mm bridge will be rolled up on a 1:1 basis into the DIP. USNC, lender under the prepetition secured note facility, agreed to subordinate the prepetition secured note to the DIP. The debtors also sought the use of cash collateral.

Great, there’s money. Now what?

A sale, of course!

A company called Standard Nuclear Inc. agreed to serve as stalking horse bidder with an offer of $28mm cash for all of the debtors’ assets. That falls just short of covering the $28.2mm owed under the prepetition secured note issued by Helms’ USNC. The only other secured debt is $650k owed Austin Building and Design for construction work. Unsecured debt, amounts due under a convertible promissory note as well as trade claims, landlords and others, stands at $35.9mm. Bid protections include a 5% breakup fee; Standard Nuclear has not, however, sought expense reimbursement.

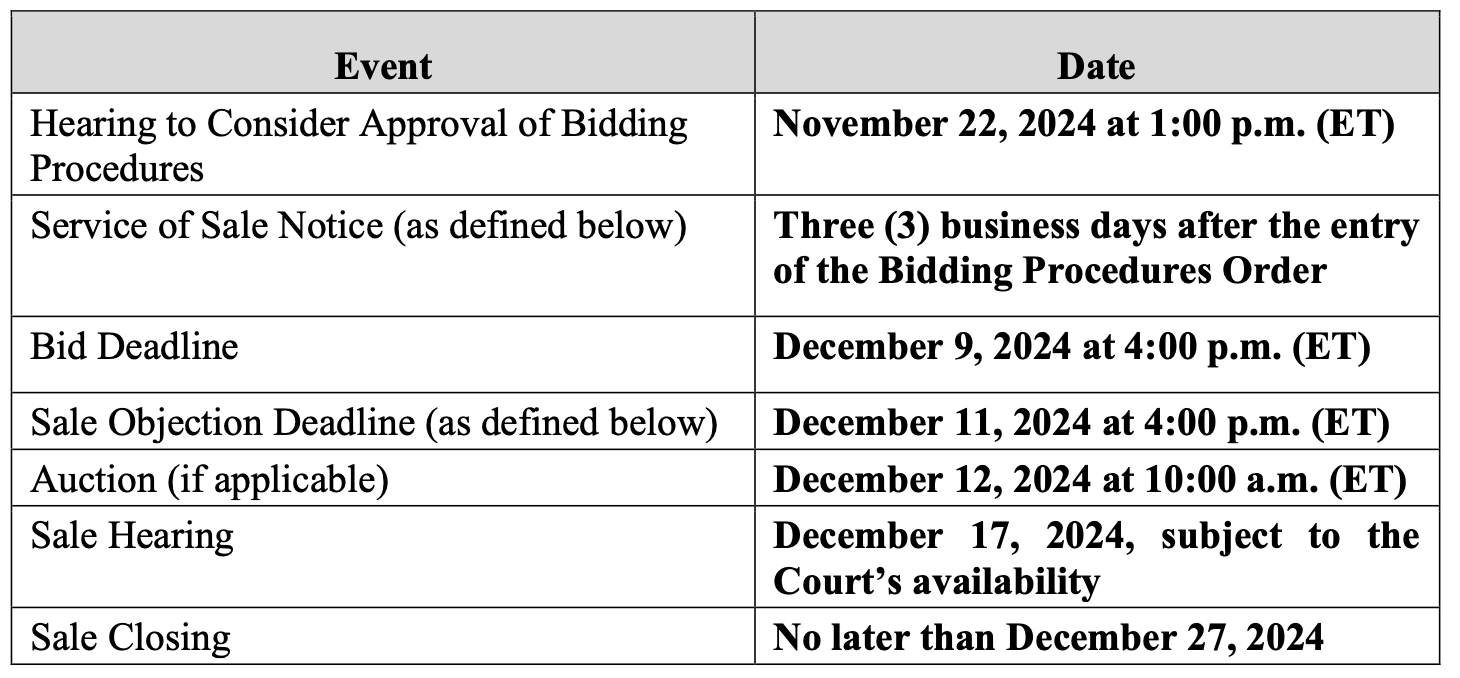

The debtors obtained all requested relief at the efficient 40-minute first day hearing on October 30, 2024. The sale motion proposes the following milestones:

On November 13, 2024, the office of the United States Trustee appointed a three-member official committee of unsecured creditors (“UCC”). The UCC subsequently retained Seward & Kissel LLP (Robert Gayda, Catherine LoTempio, Andrew Matott) and Potter Anderson & Corroon LLP (Christopher Samis, Jeremy Ryan, Levi Akkerman) as legal counsel. And now we wait to see if they bring some CIA-level bombs to this situation.

The debtors are represented by Young Conaway Stargatt & Taylor LLP (Michael R. Nestor, Matthew B. Lunn, Elizabeth S. Justison, Shella Borovinskaya) as legal; Ankura Consulting Group LLC (Alan Dalsass) as financial advisor and Intrepid Investment Bankers LLC (Lorie Beers) as investment banker. JPM Capital Partners LLC is represented by Norton Rose Fulbright US LLP (Robert M. Kirsh, Francisco Vazquez, Emily Hong) and Morris James LLP (Eric J. Monzo, Jason S. Levin, Christopher M. Donnelly). USNC Investment LLC is represented by Greenberg Traurig LLP (Nathan A. Haynes, Dennis A. Meloro) and stalking horse bidder Standard Nuclear Ltd is represented by Sullivan Hazeltine Allinson LLC (William D. Sullivan) and Nelson Mullins Riley & Scarborough LLP (Peter J. Haley).

Company Professionals:

Legal: Young Conaway Stargatt & Taylor LLP (Michael Nestor, Matthew Lunn, Elizabeth Justison, Shella Borovinskaya)

Financial Advisor: Ankura Consulting Group LLC (Steve Moore, Alan Dalsass)

Investment Banker: Intrepid Investment Bankers (Lorie Beers)

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

Prepetition First Lien Lender + DIP Lender

Legal: Norton Rose Fulbright US LLP (Robert Hirsh, Francisco Vazquez, Emily Hong) and Morris James LLP (Eric Monzo, Jason Levin, Christopher Donnelly)

Large Shareholder: USNC Investment LLC

Legal: Greenberg Traurig LLP (Dennis Meloro, Nathan Haynes)

Stalking Horse Purchaser: Standard Nuclear Inc.

Legal: Nelson Mullins Riley & Scarborough LLP (Peter Haley) and Sullivan Hazeltine Allinson LLC (William Sullivan)

Official Committee of Unsecured Creditors

Source: Docket 71 Legal: Seward & Kissel LLP (Robert Gayda, Catherine LoTempio, Andrew Matott) and Potter Anderson & Corroon LLP (Christopher Samis, Jeremy Ryan, Levi Akkerman)