🍫New Chapter 11 BK - H-Food Holdings LLC🍫

Food manufacturer succumbs to macro conditions, bad publicity, and heaps of debt.

On November 22, 2024, Illinois-based and Charlesbank Capital Partners LLC and Partners Group-owned H-Food Holdings LLC and 22 affiliates (collectively, the “debtors”) filed prearranged chapter 11 bankruptcy cases in the Southern District of Texas (Judge Perez) — a shocking development that absolutely nobody leaked to the press ahead of time, 🙄.

Of course, distressed eyeballs have been looking at this name — a “world-class contract manufacturer of food products” with 28 manufacturing and packaging facilities across 11 US states and Canada — for roughly 18 months already. We first wrote about the name in March '23. We didn’t mince words:

Anyone who has read PETITION over the years has come to realize what restructuring pros have known for a long time: when you boil things down to their simplest form, there aren’t really that many catalysts to a bankruptcy filing. There can be balance sheet issues, e.g., too much debt, too much interest expense, breached covenants (where they exist, lol), unrefinanceable maturities. There can be operational issues, e.g., supply chain problems or inflationary pressures that push up the cost of inputs and/or wages. Maybe there are secular issues — like when an industry is in the midst of getting disrupted and no longer has a justifiable business model. There can be externalities like a crushing amount of litigation or brutal judgment. There are obviously others, but the aforementioned flavors are the most popular.

There are outliers — you know, weird “factors leading to chapter 11” that you’ll occasionally read in a set of chapter 11 bankruptcy “first day” papers. Like, 🤷♀️, “we had to file for bankruptcy because we became the target of an investigation alleging that we’re f*cking scumbags who enslave children.” That’s not one you see everyday.

Pardon us: we must have been in a mood. Something about (alleged) slave migrant labor…

…really gets us fired up.

We weren’t done:

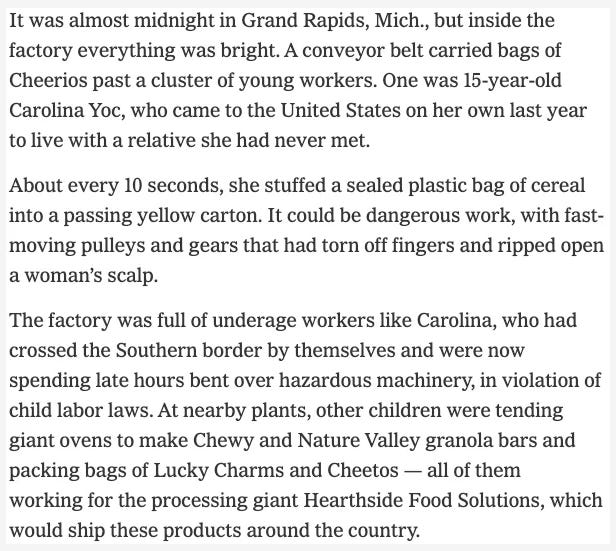

Sooooooooo about that. This week an Illinois-based contract manufacturer and private bakery that makes energy bars — Charlesbank-and-Partners Group-owned Hearthside Food Solutions — came under investigation by the US Department of Labor for alleged child labor law violations. WHOOPS. Who are these motherf*ckers? The anti-Oscar-Schindler?! Apparently your Chewy granola bars and bags of Lucky Charms and Cheetos are powered by little Timmy’s wee fingers. We wish we were actually joking.

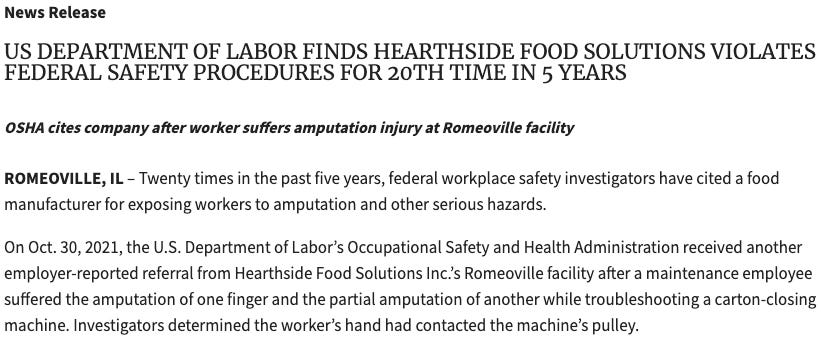

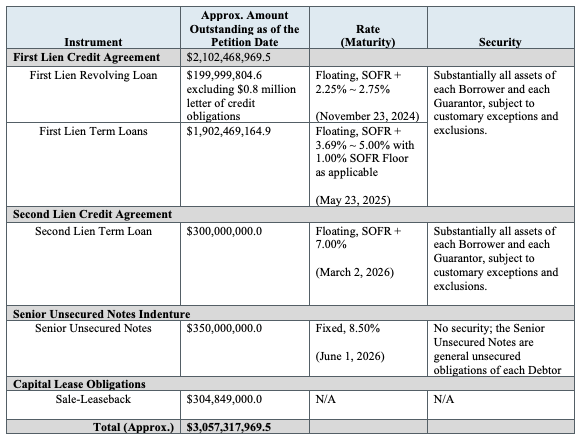

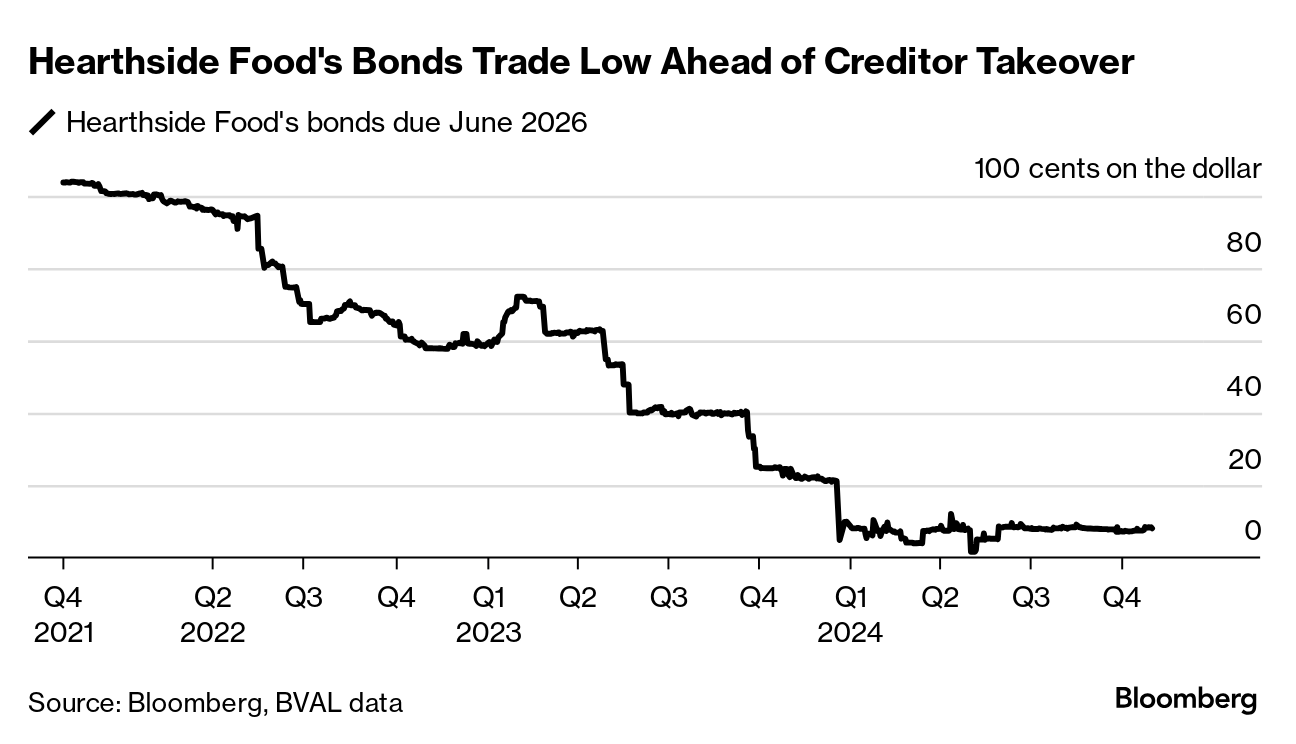

Aside from being awful, there are restructuring implications. The company, under the name H-Food Holdings LLC, has $350mm of 8.5% ‘26 unsecured notes outstanding (which sits behind a ~$200mm ‘24 RCF, a $1.7b ‘25 first lien term loan and a $300mm second lien loan). The notes were already under pressure in ‘22 — thank you rising wage costs, labor instability, and supply chain issues — before rebounding somewhat in ‘23 after news broke that the lenders might pursue a liability management transaction with Gibson Dunn & Crutcher LLP and PJT Partners ($PJT) leading the charge. Consequently, Moody’s and S&P Ratings rated the notes Caa2 and CCC (outlook negative) — and that was before this sh*t went down. Last week the notes were pricing in the low 70s with a 21+% yield. Suffice it to say the market reaction was fast and furious and the notes dipped into the low 60s on the news and the yield hit nearly 27%.Interestingly, Hearthside and The U.S. Department of Labor — which commenced a still-ongoing investigation into the company at the time — intimately know each other. The March ‘23 episode was just one among many, apparently.

Fines. External and internal investigations. Just another day for these debtors, it seems. So where do things stand with all of these (alleged) transgressions? This is about as delicate as you put things:

"…the Company has experienced a series of operational challenges, including wage rate increase and inflation, industry headwinds, certain labor issues and transitions, and adverse publicity."Do tell. With specifics please!

“In February 2023, the Company was the subject of a New York Times article raising certain labor issues which the Company maintains were principally connected to one or more third-party staffing agencies. The Company vigorously disputes the bases for the allegations raised by the New York Times, but the effects of that article were immediate and severe: adverse media attention, customer scrutiny, and a series of investigations begun by different government bodies.

For its part, the Company responded forcefully to review, assess, and further enhance its own labor policies and practices. The Company has made significant investments to ensure its ability to provide a strong employee base that is fully compliant with applicable laws and regulations, including by substantially reducing its use of third-party staffing agencies and ensuring that all employees are subject to appropriate identification, eligibility, and verification procedures. Additionally, the Company has been fully cooperative and actively engaged with government officials and regulators. Although certain of these government investigations remain ongoing, the Company does not expect such investigations to result in material judgments, fines, or penalties, if any; but the ultimate amounts cannot be predicted with any certainty.”Wow. That’s quite the impressive way of making something awfully salacious sound rather benign.

Fine, we’ll bite and move on.

Actually, hang on. These things have to be related, right?

“Significant wage rate increases connected to overall inflation growth has adversely affected the Company’s financials. In the last three years, wage rates have increased by 17.2% in the aggregate compared to 2021. Such wage pressure has, in turn, imposed substantial pressure on the Company’s operating margins as the Company has been unable to completely “pass through” such increased costs.”Imagine being the operator of a PE-owned food manufacturing facility. Margins are down and the bosses are breathing down your neck. They’re telling you do everything and anything to get margins back up. You might just be so inclined to take a flyer on lil’ Timmy, you know, can’t piss off the 25 year-old PE analyst lowering his McKinsey-branded glasses and telling you what to do! Isn’t everything today subject to “context?” We feel like we heard that somewhere (🖕).

Anyway, whatever. Let’s put aside the children and talk about something nearer and dearer to our collective hearts: debt and liability management!

Confronted with the aforementioned perfect storm of headwinds and an unwieldy capital structure …

… the debtors had to get creative.

In addition to various operational initiatives put into place — Alvarez & Marsal LLC’s efforts merit one paragraph, it seems, lol — the debtors engaged in a variety of asset sales in ‘23 and ‘24. Of note:

“In 2023, the Company sold its European nutritional functional bars business which generated approximately €235.0 million, with such cash proceeds held by ROS B.V., the Company’s Dutch unrestricted subsidiary. In July 2024, the Company repatriated approximately $187.9 million of the cash proceeds to Hearthside Sub, LLC, (the “US Unsub”), which for the avoidance of doubt, is not an obligor or guarantor on the Company’s prepetition debt.”We recall hearing rumors that this transaction had created a great deal of consternation among the term lenders back in Q4’23. In particular, they were worried that the now-debtors and sponsors had conspired to transfer the assets of the European bar business to an unrestricted subsidiary so that the proceeds wouldn’t necessarily be available to lenders. Stick a pin in this, folks, because it becomes relevant again when we discuss how the cases will be financed.

About the filing. There’s a restructuring support agreement (“RSA”) supported by approximately 81.2% of the first lien lenders, 100% of the second lien term lenders, and 77.7% of the senior unsecured notes. Last we checked the first lien term loan was in the low 60s and, well, you can see where the unsecured notes are:

There’s a reason for that. The value breaks clearly at the first lien term loan level. And so it is a group of first lien lenders who are driving the bus here.

The RSA has a number of primary features.

📍DIP Financing (“DIP”). The debtors will seek to use cash collateral on hand ($212.9mm, which includes the repatriated money from the US Unsub) and seek approval of an additional $300mm DIP at a second day hearing ($150mm new money + a rollup of some of the 1L TL dollar-for-dollar). The new money portion is at cash pay SOFR + 8.5%; the roll-up is at the same rate on a PIK basis (but the PIK will be waived if RSA transaction gets done). Fees include 2.5% and 1.5% commitment and exit fees, respectfully — both on new money only.

📍Exit Financing. Surely by now you’ve probably concluded that the first lien term lenders are getting completely equitized. That’s right, they’ll get 100% of the post-reorg equity (subject to dilution from an equity rights offering, “ERO,” and a management incentive plan). But they also get to participate in a $825mm exit TL ‘30 S+650 (2% floor, cash pay, 1% amort). As you might expect, not everyone got to be part of the 1L Ad Hoc Group (“1L AHG”) that’s backstopping the DIP. While all of the 1L guys will be able to elect into the DIP, they won’t get the same sweet sweeeeeeeeeet economics the 1L AHG guys are getting. Namely, the ability to backstop the proposed $200mm ERO at a 35% discount to implied equity value of $470mm (implying a total enterprise value of $1.4b upon emergence). The 1L AHG guys benefit from an allocated 35% ERO holdback (the other 65% is available to all 1L term lenders on a pro rata basis, including the ERO backstop parties). If you’re wondering what that means, it means that the 1L AHG gets the benefit of the DIP economics, the ERO holdback, the other 65% ERO piece, the pretty attractive minimum 8.5% cash pay term loan, AND a 10% backstop fee paid in equity at discounted value. When all is said and done, the post-reorg balance sheet will feature (a) a $300-375mm ‘30 Exit ABL (with interest rate TBD “subject to third-party financing process”), and the $825mm exit term loan. Quick napkin math gets to:

Combined with the ERO, the proceeds of the post-reorg balance sheet will pay down any remaining DIP amounts outstanding, take care of working capital, and leave $100mm of pro forma cash on hand.

Ok, so that’s the 1Ls.* What of the 2Ls and the unsecured?

Recoveries for both are … well … back to you Admiral:

Yup, contingent upon approval of the debtors’ to-be-proposed Plan. In the event of approval, the 2L lenders will get their pro rata share of $18mm in cash (less any pro fees) except if a UCC incurs more than $13mm, this recovery will be reduced on a ratable basis until the UCC fees reach $25mm, after which there’ll be no more reduction.** Meanwhile, the senior unsecured noteholders will get their pro rata share of $21mm (subject to the same UCC reduction). Finally, general unsecured creditors will get their pro rata share of $2.4mm plus some additional minor economics, all subject to the same UCC reduction. Frankly, we’re not sure we’ve seen such a UCC reduction provision before. But it basically pits the junior creditors against a UCC which is quite an interesting dynamic.

The debtors hope to have the cases confirmed within 110 days of the petition date. That leaves plenty of time for said UCC to start throwing some bombs at, among others, the PE sponsors. The debtors already have a special committee in place (Carol Flaton, Patrick Bartels — the same dynamic duo in Wellpath Holdings Inc.) to, we reckon, revisit PE governance but we all know the UCC will definitely want to “conduct its own investigation,” the BK process being one brimming with trust and efficiency.

The debtors are represented by Ropes & Gray LLP (Ryan Preston Dahl, Matthew Roose, Natasha Hwangpo, Stephen Iacovo, Eric Schriesheim, Eric Sherman, Tessa Ptucha, Dainel McCaughey, Ryan Weinstein, Peter Welsh) and Porter Hedges LLP (John Higgins, M. Shane Johnson, Jack Eiband) as legal counsel, Alvarez & Marsal LLC (Robert Caruso) as financial advisor, and Evercore Group LLC ($EVR)(Gregory Berube) as investment banker. The 1L AHG is represented by Gibson Dunn & Crutcher LLP (Scott Greenberg, Joshua Brody, Matthew Williams, Tommy Scheffer, Yifan Su) and Howley Law PLLC (Tom Howley, Eric Terry) as legal counsel and PJT Partners LP ($PJT) as investment banker. An ad hoc group of 2L term lenders is represented by XXXXXXXXX LLP and FTI Consulting Inc. ($FCN) as financial advisor. An ad hoc group of unsecured noteholders is represented by Paul Hastings LLP as legal counsel and Perella Weinberg Partners LP ($PWP) as investment banker. As if there aren’t enough heavyweights in this situation, Charlesbank has Kirkland & Ellis LLP (Brian Schartz, Patricia Loureiro, Jimmy Ryan) in its corner while Partners Group has Milbank LLP (Samuel Khalil, Michael Price). The sponsors share investment bankers at Greenhill & Co. LLC.

The debtors’ first day hearing will be later today on November 25, 2024 at 1pm (CT).

*The 1Ls also will get any cash that would have gone to the other classes if they’d accepted “death trap” terms, in the event that those classes reject the Plan. Significantly, the 1Ls have agreed to waive their deficiency claims so as not to dilute further what little economics those lower down the cap stack are getting.

**To the extent the 2L lenders get other rights (i.e., right to partake in the ERO), the senior unsecured notes shall get them too. We’re not sure why this would ever happen.

Company Professionals:

Legal: Ropes & Gray LLP (Ryan Preston Dahl, Matthew Roose, Natasha Hwangpo, Stephen Iacovo, Eric Schriesheim, Eric Sherman, Tessa Ptucha, Dainel McCaughey, Ryan Weinstein, Peter Welsh) and Porter Hedges LLP (John Higgins, M. Shane Johnson, Jack Eiband)

Special Committee: Carol Flaton, Patrick Bartels

Financial Advisor/CRO: Alvarez & Marsal LLC (Robert Caruso)

Investment Banker: Evercore Group LLC (Gregory Berube)

Claims Agent: Kroll (Click here for free docket access)

Other Parties in Interest:

DIP Agent: Wilmington Savings Fund Society FSB

1L Agent: Goldman Sachs Lending Partners LLC

2L Agent: Ares Capital Corporation

Unsecured Notes Indenture Trustee: US Bank NA

1L Ad Hoc Group + DIP Lenders

Legal: Gibson Dunn & Crutcher LLP (Scott Greenberg, Joshua Brody, Matthew Williams, Tommy Scheffer, Yifan Su) and Howley Law PLLC (Tom Howley, Eric Terry)

Investment Banker: PJT Partners LP

Financial Advisor: JZ Advisors LLC

2L Ad Hoc Group

Legal: Proskauer Rose LLP (Vincent Indelicato, Matthew Koch)

Financial Advisor: FTI Consulting Inc.

Notes Ad Hoc Group

Legal: Paul Hastings LLP (Kris Hansen, Charles Persons)

Financial Advisor: Perella Weinberg Partners LP

Consenting Sponsor: Charlesbank Capital Partners LLC

Legal: Kirkland & Ellis LLP (Brian Schartz, Patricia Loureiro, Jimmy Ryan)

Investment Banker: Greenhill & Co. LLC

Consenting Sponsor: Partners Group USA Inc.

Legal: Milbank LLP (Samuel Khalil, Michael Price)

Investment Banker: Greenhill & Co. LLC