💥SBF ... ing ... himself💥

💥SBF ... ing ... himself💥

FTX Update, WeWork's Struggles Continue, Littlefinger/XClaim Update & More

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.” — Mr. John J. Ray III, speaking of FTX Trading Ltd.

Confirmed! FTX is a five-star horror show.1

The long-awaited — ⚡️four days!⚡️ — First Day Declaration (“FDD”) from John J. Ray III, the newly-appointed CEO2 of the hot mess that is “the FTX Group,” dropped on the District of Delaware bankruptcy court docket on Thursday (November 17, 2022).3 To say that it is extraordinary would be understating the case. It’s a 30-page jaw-dropper with a lot to unpack.

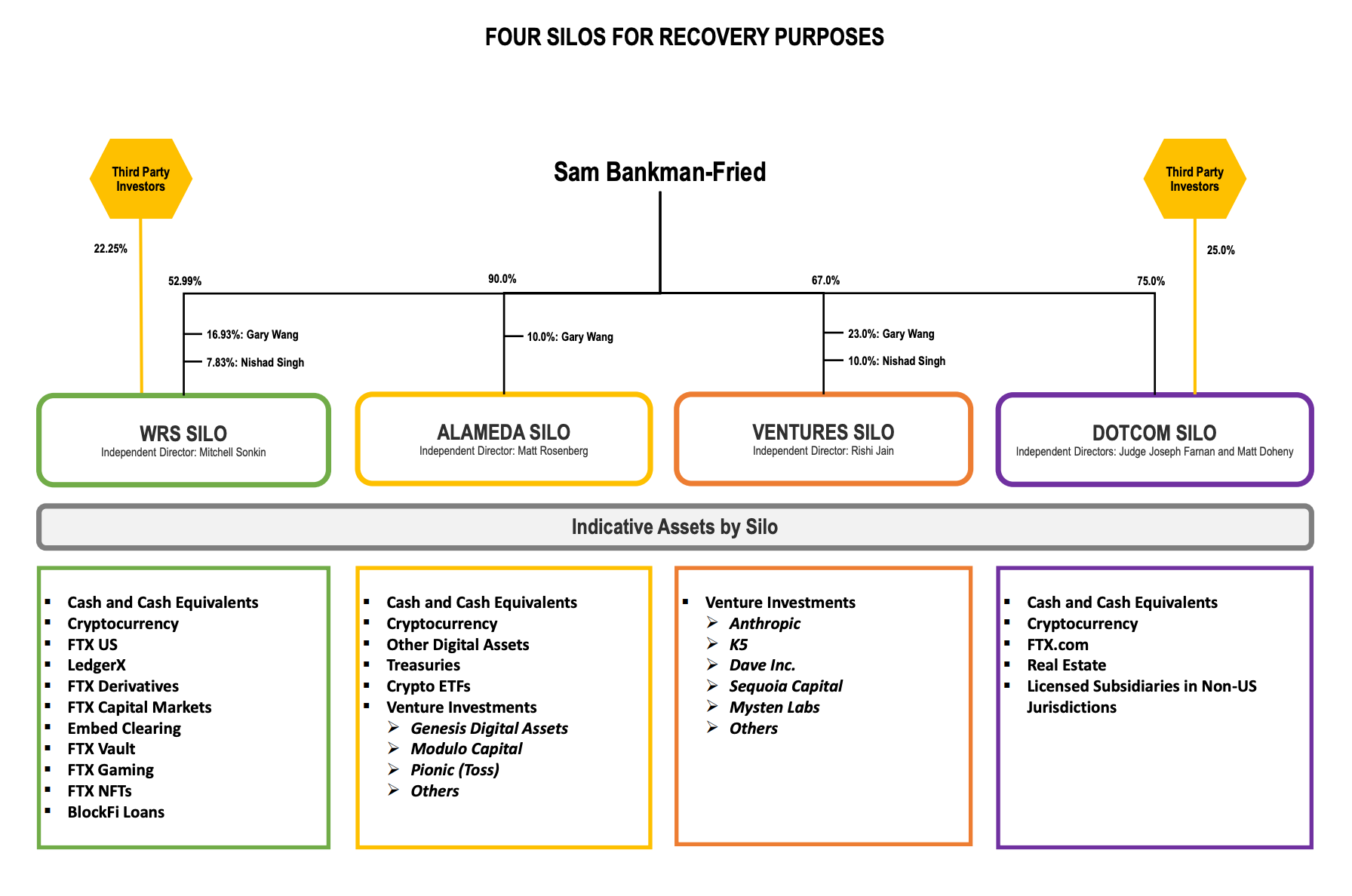

Mr. Ray and his teams have made VERY impressive progress in the week-or-so that they’ve been embedded at the company. Notably, they’ve distilled FTX Group into four distinct silos — a feat that, given the multitude of entanglements here and the haphazard manner with which Sam Bankman-Fried and his team managed (or, shall we say, didn’t manage) the business(es), is a testament to what we’re sure is around-the-clock work by he and the fine folks at Sullivan & Cromwell LLP and Alvarez and Marsal LLC, among others.4 You’ve got:

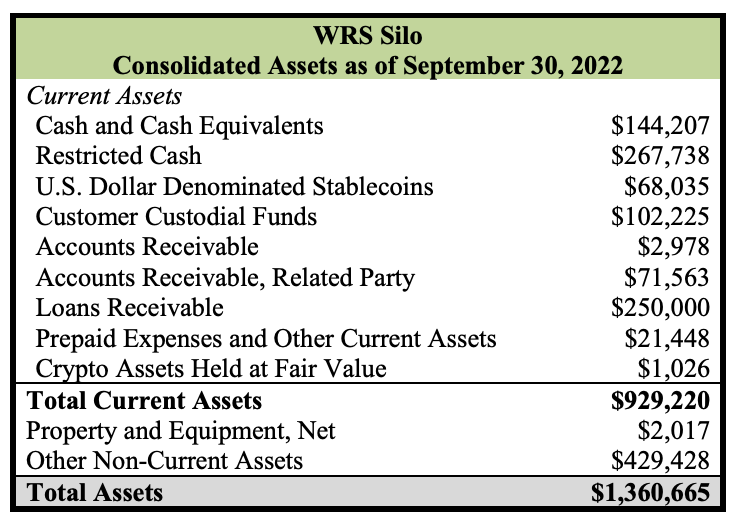

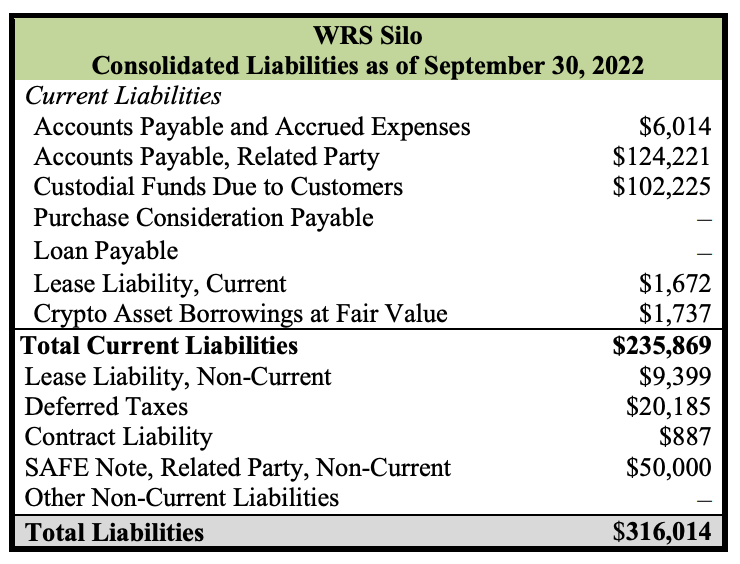

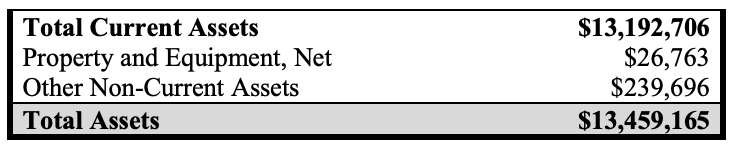

Mr. Ray then goes on to post financials for each of the silos. Here, for instance, is the WRS Silo:

Significantly, the balances of customer crypto assets deposited were not recorded as assets on the balance sheet and are not presented in the chart. That $250mm loan receivable, though, that’s BlockFi right there.

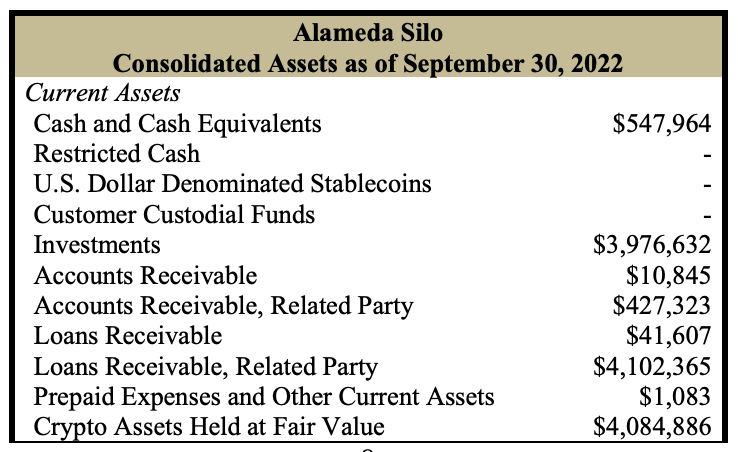

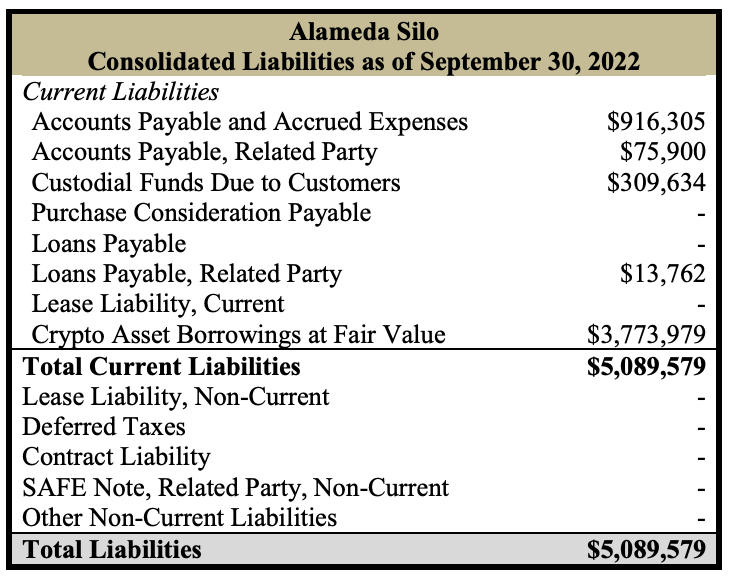

And here is the Alameda Research silo:

What’s staggering about each of the four silos and the financial information Mr. Ray provided about each of them, however, is this pervasive caveat placed throughout the FDD, each of which more or less takes this form (per Mr. Ray):

…because this balance sheet was produced while the Debtors were controlled by Mr. Bankman-Fried, I do not have confidence in it, and the information therein may not be correct as of the date stated.

Man, SBF was a monumental f*ckup. In other words, we have more official financial information today than we did before November 17th but … uh … yeah … take it with a massive grain of salt. The TL;DR: there’s a massive hole. The exact magnitude will take some time to sort out.

Putting aside the seemingly unreliable financials, there are some other interesting bits in the FDD:

📍Governance. Alarm bells always start ringing whenever we see passive voice. It’s obviously great that the FTX Group now has new independent directors in place at the various silos. But what does Mr. Ray mean when he says “new independent directors have been appointed….?” By whom? What was the process? Did Mr. Ray appoint them himself? Did S&C recommend these directors? What are the previous ties between Mr. Ray and these new independent directors? We’re not pointing fingers or casting aspersions or anything of the sort: what we do think is critical for this sh*t show is 100% transparency about what is going on, who is pulling the strings, and who is accountable to whom. Potentially millions of people owed meaningful sums of money are owed that much.

📍Cash Management. Here we’ll state the obvious: you don’t typically see a debtor CEO say that he has to build a cash management system from scratch. It appears that A&M will have to deploy a whole team of folks just to track fund flows to determine how much cash is in the estate. Un-f*cking-believable. To date, they’ve seemingly performed a Herculean feat, attributing cash as follows:

By the way, for those of you wondering how bankruptcy professionals stand to get paid in this situation well … there’s ⬆️ your answer. Trust us: nobody is diving headfirst into this clusterf*ck without ensuring there’s a paycheck coming.

Anyway, it appears that A&M and Mr. Ray are making quick work of this project. On Friday, the debtors filed a motion seeking authority to enter into a proposed new cash management scheme.

📍Financial Reporting. You know, that small thing. So you’ve got four silos. Mr. Ray has found no audits for two of the silos: Alameda or Ventures. The WRS Silo has apparently been audited (for the period ended December 31, 2021 — a lifetime ago in crypto land) by a reputable firm. But then there is the Dotcom Silo which was audited by the “first-ever CPA firm to officially open its Metaverse headquarters in the metaverse platform Decentraland.” Mr. Ray left it at that which leaves things pretty clear as to how he feels about it (LOL). There is no accounting department at FTX to help clarify matters. Repeat: there’s no accounting department at FTX to help clarify matters. 🤡🤡

📍Human Resources. A bit about first day pleadings. Hopefully — hopefully — professionals are in place and there’s time to establish a clear line of communication for information flow back and forth between company employees and restructuring professionals so that the proper first day pleading package can be completed. So, one junior S&C associate, for instance, would usually be tasked with liaisoning with an HR representative for purposes of constructing an “employee wage” motion — a motion that seeks authority from the bankruptcy court to pay certain limited pre-petition amounts to employees to, you know, like keep the lights on and stuff. It’s easy to take this typical work stream for granted until you run into a situation like FTX where “the Debtors have been unable to prepare a complete list of who worked for the FTX Group as of the Petition Date, or the terms of their employment.” To state the obvious: this is absolutely not normal.

The good news is that by Friday, November 19th, it appears that Mr. Ray and team have made progress and there is now a limited employee wage motion on file. This is a good thing. Those employees who have remained behind to assist Mr. Ray and his team ought to be taken care of given that the rest of their colleagues apparently scurried like rats abandoning a sinking ship:

The Debtors experienced extraordinary attrition among their Employees in the period shortly before and following the Petition Date, and the Debtors are working diligently with their advisors to determine and assess the remaining Employee population.

In this spirit, the debtors are seeking to pay a handful of employees compensation in excess of the statutory priority caps set forth in section 507 of the bankruptcy code.

📍Disbursement Controls. TL;DR: they didn’t really have any. Employees bought personal homes with corporate funds. Employees. Bought. Personal. Homes. With. Corporate. Funds. This is gonna get interesting.

📍Digital Asset Custody. Painful. Absolutely painful. Apologies for the block quote but…wow:

The Debtors have located and secured only a fraction of the digital assets of the FTX Group that they hope to recover in these Chapter 11 Cases. The Debtors have secured in new cold wallets approximately $740 million of cryptocurrency that the Debtors believe is attributable to either the WRS, Alameda and/or Dotcom Silos. The Debtors have not yet been able to determine how much of this cryptocurrency is allocable to each Silo, or even if such an allocation can be determined. These balances exclude cryptocurrency not currently under the Debtors’ control as a result of (a) at least $372 million of unauthorized transfers initiated on the Petition Date, during which time the Debtors immediately began moving cryptocurrency into cold storage to mitigate the risk to the remaining cryptocurrency that was accessible at the time, (b) the dilutive ‘minting’ of approximately $300 million in FTT tokens by an unauthorized source after the Petition Date and (c) the failure of the co-founders and potentially others to identify additional wallets believed to contain Debtor assets.

It is here where we get a taste for what the overall tenor of this case is going to look like: it is going to mostly be a gigantic exercise in forensic analysis and litigation. Sure, sure, maybe there’ll be some transactions in the midst of it all but in the interim period this is a search-and-rescue mission followed by an offensive maneuver targeted towards grifters who pillaged this company with intent or destroyed it with gross negligence. In addition to that, you have to wonder to what degree the debtors will aggressively pursue preferences and fraudulent conveyances — including those much-maligned political