💥A "Hawkish Hold" = Companies Fold?💥

Mitchell Gold + Bob Williams, Aerotech Miami Inc., American Physician Partners, BioSteel Sports Nutrition Inc. + More.

These ⬆️ quotes from last week more or less teed up the Fed for a hawkish stance and Jerome POW-ell and his gang, unlike Phillies slugger and MLB season strikeout leader Kyle Schwarber, didn’t swing and miss. The Fed nevertheless managed to surprise markets this week — not because it opted to press the ‘pause’ button on the Fed funds rate, everyone expected that — but because it signaled conviction around “higher for longer,” a phrase uttered not long ago by Mr. POW-ell but forgotten by everyone drinking the “soft landing” Kool-Aid. Mr. POW-ell said,

"In terms of inflation, you are seeing - the last three readings are very good readings. It's only three readings. You know, we were well aware that we needed to see more than three readings … If the economy comes in stronger than expected, that just means we’ll have to do more in terms of monetary policy to get back to 2%, because we will get back to 2%."

Riiiiiiight. And so what are we talking about exactly? The Fed’s dot plot remains unchanged for ‘23: the median projection is 5.6%, implying an additional hike before a calendar turn. In ‘24, however, the forecast has shifted upward from 4.6% to 5.1% while the forecast for ‘25 is up to 3.9% from 3.4%. Read: higher for longer. Just as POW-ell had previously said.

As you might expect, the equity market reacted negatively:

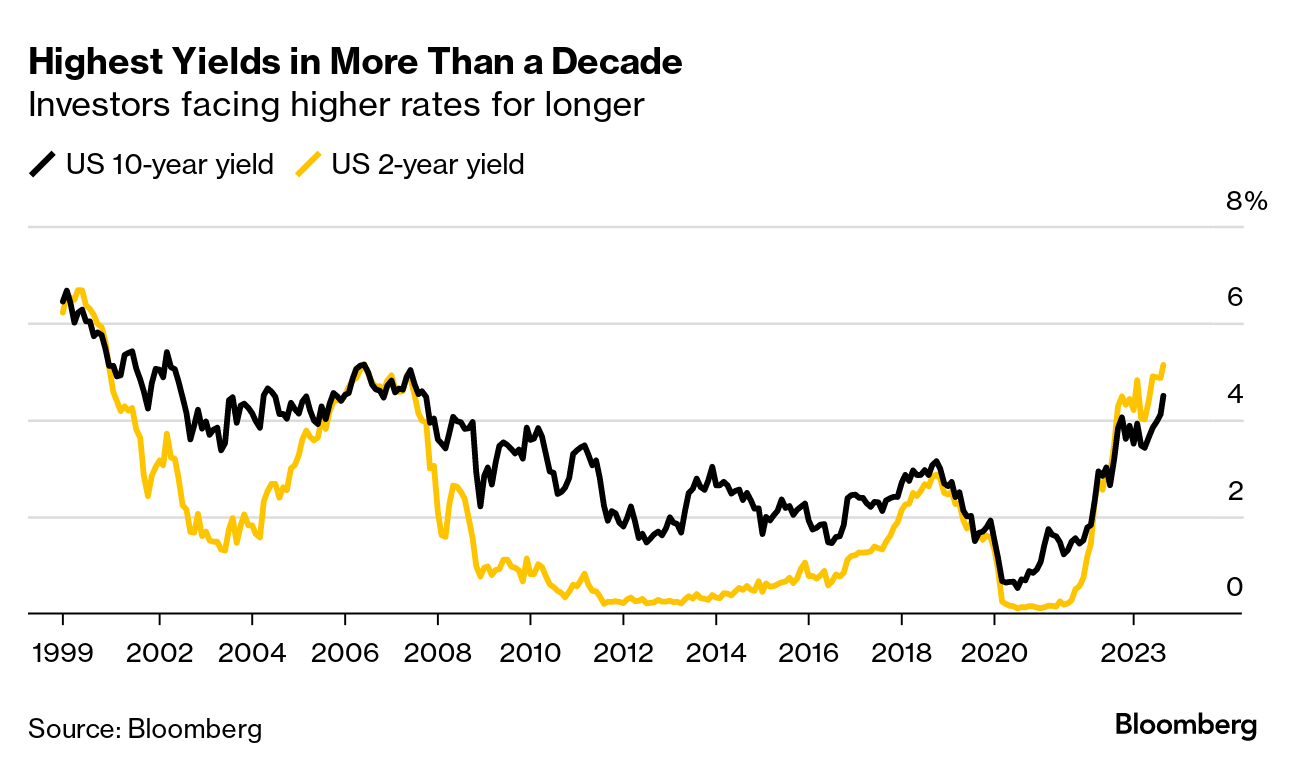

Similarly, bonds got smoked and treasury yields continued to move up (note the continued inversion):

The move on the 10Y is bananas. Good luck house hunting folks.

Query whether, as we’ve discussed before, a growing collection of powerful forces may combine to help alleviate Mr. POW-ell’s burden. By some measures — the San Francisco Fed’s data, for one — all of the pent-up pandemic-era excess savings are set to runoff by year end. The resumption of student loan payments ought to help accelerate that depletion. As should oil prices, now that oil is back soundly above $90/gallon. The consumer — though still healthy — is getting besieged on all sides.

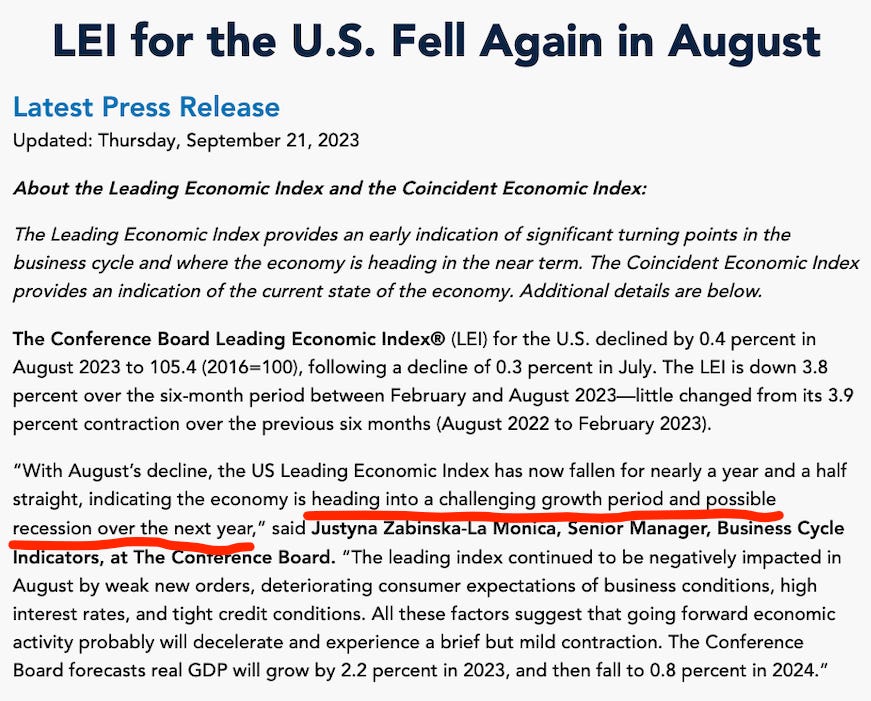

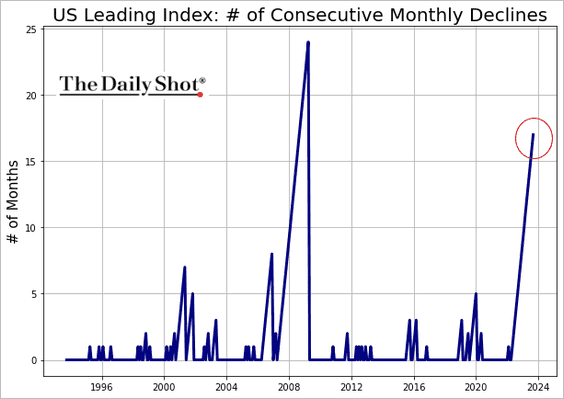

The Conference Board, which factors the consumer into its measures, published its latest findings on Thursday:

The index is now down 10.5% from its December ‘21 peak. Declines of this size have historically been tied to recession and the consecutive decline (17 months!) is a pattern not seen since the Great Financial Crisis. ⬇️ 👀

Notably, per Bank of America, household credit card spending declined 0.2% YOY in the week ending September 16. Credit card utilization and delinquency rates are increasing but both remain below or near historic and pre-pandemic levels (but look out for the delinquency rate on subprime auto loans, eesh).

With higher rates for longer poised to batter the economy and inevitably shake consumer confidence, perhaps all of that talk about a “soft landing” and recession avoidance was wishful thinking…? 🤔

*****

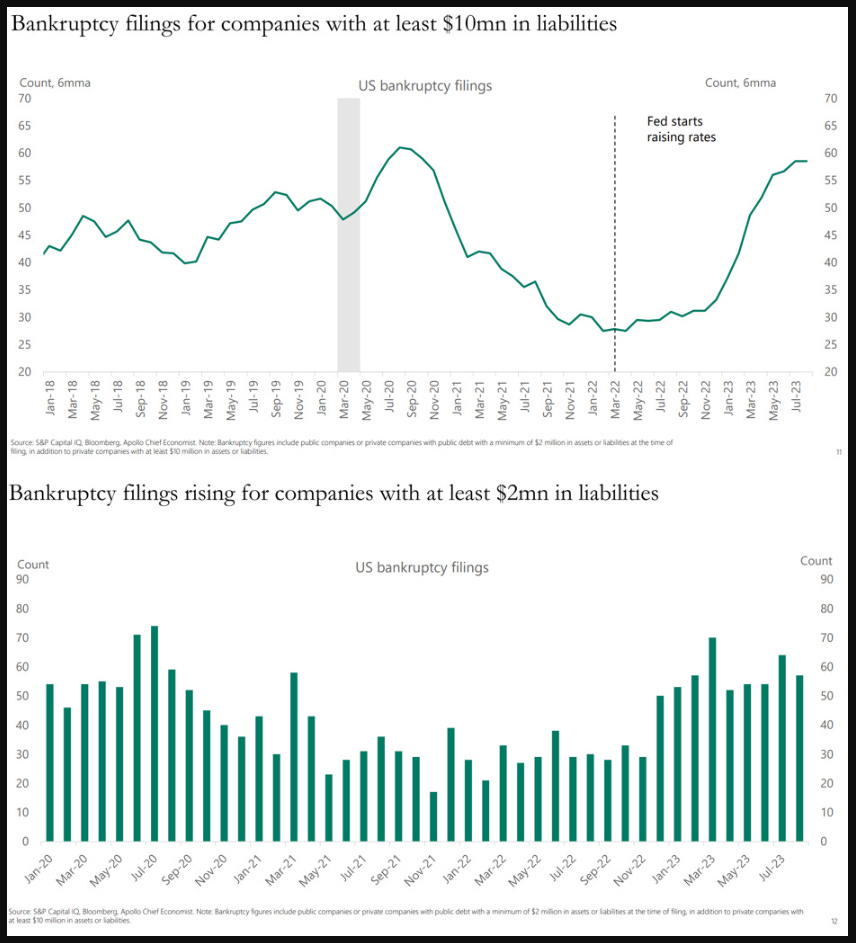

Which gets us to restructuring stuff. Yes, there have been, and will continue to be, some filings. Here ⬇️ is Epiq diving into its own bankruptcy data:

Unfortunately, however, Epiq doesn’t delve deeper into the size of these filings. Luckily, we have Apollo Capital Management to fill in that gap:

The focus on $10mm and $2mm in liabilities, respectively, is fascinating because that right there is a commentary on the distressed market. Sure, cases may be up but “quality” cases of size? Not so much. We continue to see a number of prepacks, 363s (many filing sans stalking horse), wind downs and just general overall turd burgers (continue reading for examples). Sure, sure, default rates have been increasing and the distressed debt universe is … well … existent …

… but right now — Rite-Aid Corporation ($RAD) notwithstanding — the action is in the small to middle market while the larger debt stack cases focus on liability management and, for now, get deals done out of court (still fees there tho 🤷♀️).

Think we’re exaggerating? Let’s revisit with Epiq. Here is a list of the cases they’ve been involved in over the last two months: