💥New Chapter 11 Bankruptcy - Exactech Inc.💥

Medical implant devices manufacturer succumbs to “a relatively large litigation portfolio.”

On October 29, 2024, FL-based Exactech Inc. and four affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Silverstein). The debtors are in the business of manufacturing and selling medical implant devices such as replacement hips, joints, shoulders and feet. Hopefully you haven’t had one of these surgeries and gotten one of these devices implanted because a primary factor in this bankruptcy filing is the fact that these devices have allegedly been faulty as-all-f*ck. Luckily, the debtors’ lead counsel, Ryan Preston Dahl of Ropes & Gray LLP, has not had one of these implants, despite his “brief football career,” a detail that Mr. Dahl felt absolutely compelled to share at the debtors’ first day hearing.* Cue the soundtrack Johnny!

Snark aside, the football career is pertinent because it’s very clear that blocking and tackling is going to be (and has already been) a huge part of Mr. Dahl’s assignment here. This situation has it all: private equity duking it out with lenders duking it out with plaintiffs’ attorneys. Strap your helmets on, folks.

First, some background.

Founded in ‘85, the debtors first focused exclusively on products for the hip, according to the first-day declaration of CRO Jesse York, a Managing Director at the debtors’ financial advisor, Riveron RTS. The debtors in ‘92 developed their first knee implant. They IPO’d on NASDAQ four years later. In ‘05, they launched a shoulder product. In ‘14, the debtors bought a surgical technology company and used it to build ExactechGPS, a computer-assisted device that provides surgeons with a 3D view of patients’ joints. This “changed the way total joint replacement surgeries are performed,” York says.

You know who loves game changing sh*t? Private equity. In October ‘17, TPG Capital (“TPG) announced a definitive agreement to acquire the debtors for $42/share cash in a transaction valued at $625mm. Note the hefty premium ⬇️:

In the announcement, Jeff Binder, a “senior advisor” to TPG, waxed bullish on the “outstanding opportunities” available to “nimble, innovative and responsive companies” to compete with the big boys of the orthopedic industry. “I look forward to working with management to fully realize the potential of a company for which I have always had great respect.”

Well, that’s nice. The deal closed in the first quarter of ‘18 — and it’s been mile and mile of bad road ever since. Indeed, short after closing a former employee and two former sales reps (the “Relators”) filed a qui tam lawsuit (“Qui Tam Claims”) against the debtors in the Northern District of Alabama. Qui tam is derived from the Latin phrase qui tam pro domino rege quam pro se ipso in hac parte sequitur. Literally it means a plaintiff is suing on behalf of the king as well as for himself, or in other words, a private citizen who accuses a party of violating the law gets a piece of whatever financial penalty the government extracts as punishment. The Relators alleged the debtors violated the False Claims Act by seeking reimbursement for selling “allegedly misbranded knee devices and allegedly defective knee devices that were not medically reasonable and necessary.” The U.S. Department of Justice (“DOJ”) declined to pursue the Qui Tam Claims, but the Relators were undaunted. York says that the debtors have spent considerable amounts defending the case and seeking a settlement, which included negotiations with the DOJ beginning in October ‘23. To no avail:

“The Company and its advisors intend to continue working diligently with the DOJ during these chapter 11 cases to fully, fairly, and consensually resolve the Qui Tam Claims.” That’s not good. But there’s something way worse: the product recalls. The debtors in ‘21 commenced a recall of a hip product, which later expanded to include all hip liners, knee, and ankle Implants. In ‘24 they commenced a voluntary recall of shoulder replacement devices and knee patellar components. Why?

"The Recalls were voluntarily initiated due to Exactech Inc.’s vendor supplying nonconforming bags used to package the Company’s affected products. The non-conforming bags were determined to be missing one of the oxygen barrier layers that was designed to protect the medical devices from oxidation, a chemical reaction with oxygen that could potentially degrade plastic components over time. Oxidation, if it reaches a certain threshold, may lead to faster device wear or failure, which could potentially lead to revision surgeries."For the debtors, the operative phrases are “may lead,” and “potentially lead.” York states that the debtors initiated the recalls out of “an abundance of caution,” although they maintain — based on “science” — that the offending bags have not led to overall higher rates of revision surgeries. When has “science” ever gotten in the way of an industrious lawyer! 2.6k patients — or about 1.7% of patients in the U.S. potentially impacted — have filed lawsuits. On October 7, 2022, all federally-filed lawsuits were consolidated into a multi-district litigation (“MDL”) before the U.S. District Court for the Eastern District of New York. 1840 lawsuits are pending in the MDL. Some 740 other suits filed against the debtors in Florida were consolidated before Judge Donna M. Keim of the Eighth Judicial Circuit. Mr. Dahl describes all of this as “a relatively large litigation portfolio.” In-f*cking-deed.

As recently as July ‘24 the debtors offered to settle the MDL litigation. No luck: the parties were “unable to reach a consensual resolution.” It was clear, York says, that the product liability claims would not be solved out of bankruptcy court. The debtors also paused negotiations regarding settlement of the Qui Tam Claims, and pivoted to raising additional liquidity and preparing an in-court restructuring.

Additional liquidity? Why oh why might that have been needed? The debtors did $330mm in revenue for the 12 months ended 9/30/24, and ~$65mm of EBITDA over that span. That “relatively large litigation portfolio,” however, “has become a significant burden for the company over recent years.”

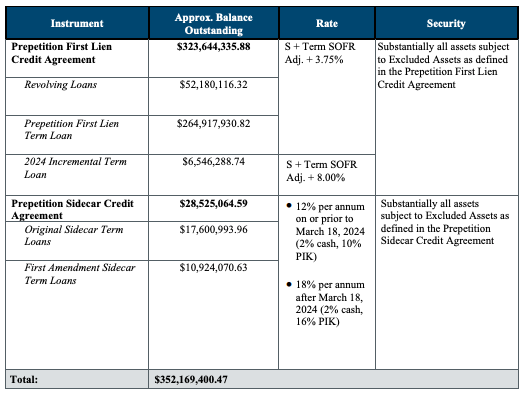

There’s also the debtors’ capital structure …

… which includes that ⬆️ revolver and its inconvenient November ‘24 maturity (followed by a February ‘25 maturity of the term loan).

Suffice it to say, the litigation overhang complicated negotiations over these maturities. Centerview Partners came on board in July ‘23. Note the “Sidecar” facility. TPG provided that facility to the debtors shortly thereafter in September ‘23. It was originally $15mm. TPG and the debtors later agreed to a $20mm upsize in April ‘24 (of which, as of the petition date, half has been drawn). In between the $15mm and $35mm, somebody thought it wise to, we don’t know, maybe get some independent oversight in the mix, 🙄. In November ‘23, the debtors brought on former RX banker Ms. Elizabeth Abrams as an independent director. One might be forgiven for thinking that maybe, just maybe, an independent ought to have been brought on board sooner, 🤔, like perhaps before the Sidecar facility.