💥Ebix Needs a Fix💥

Akumin & Air Methods prepack. PE roll-up headwinds? And More.

It’s been a hell of a week.

Some macro bits caught our attention:

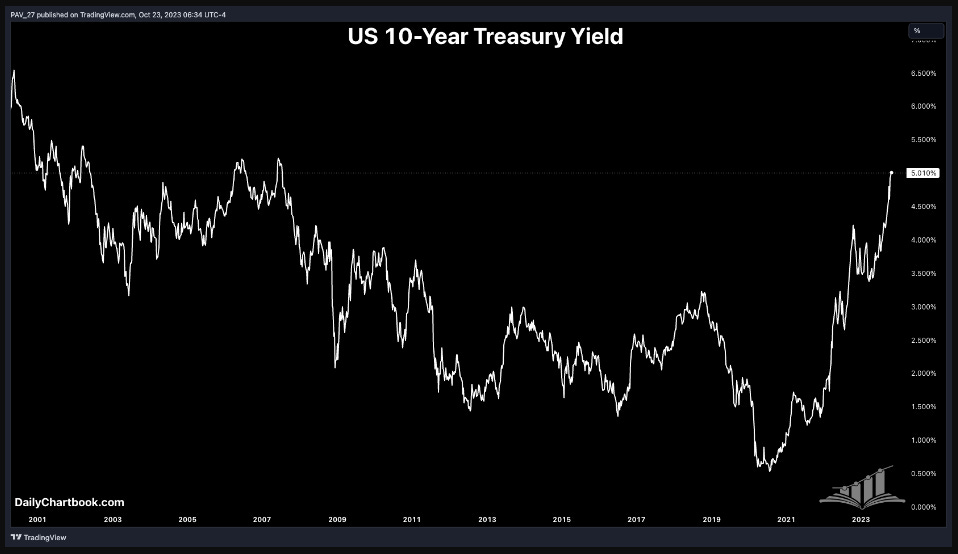

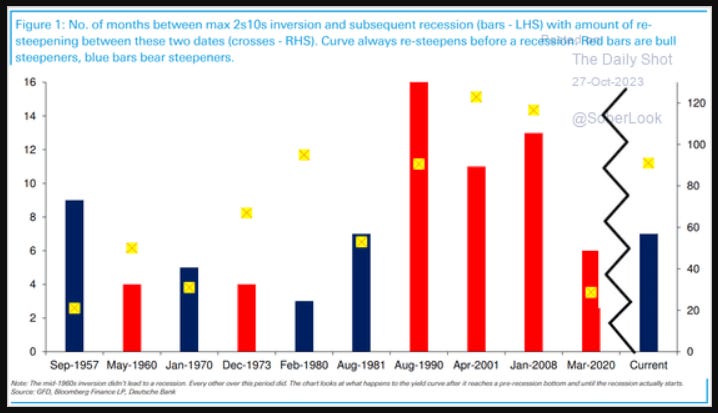

The 10Y Treasury pushed above 5% earlier this week for the first time since ‘07. The dreaded inverted yield curve is in self-correction mode …

…which may be a bad thing:

HY YTW was just off the ‘23 high around 9.6%, widened considerably off the ‘23 lows of 7.8%. Yields are pushing higher and spread are widening. The result? New issue is (basically) nowhere to be found. Non-defaulted USD bonds yielding > 15% hit 144 at $99b of face value against $93b the previous week.

Similarly leveraged loan yields (to maturity) have widened along with spreads. After a robust month of issuance in September, October is looking like a desert. New CLOs are coming online, however, so that should be a tailwind for future issuance.

Speaking of CLOs, ratings agency downgrades have been all the rage in ‘23 which has been causing some problems for CLOs that have pretty tight baskets for holding CCC loan at par. What effectively amounts to forced selling is on the increase.

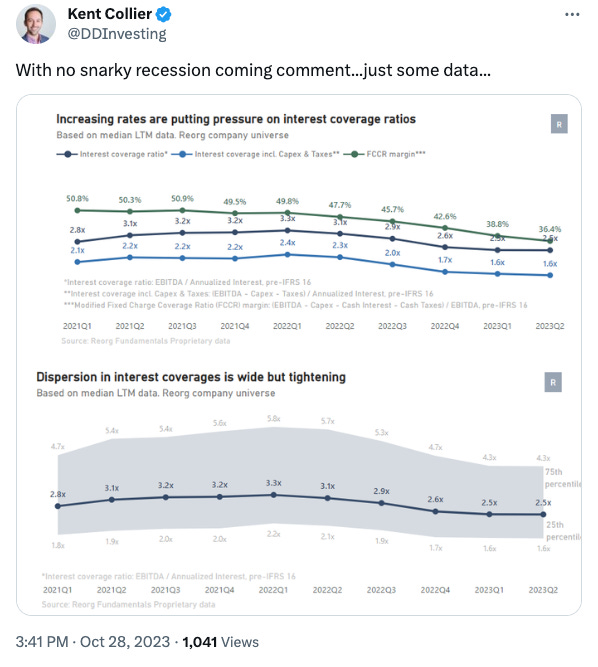

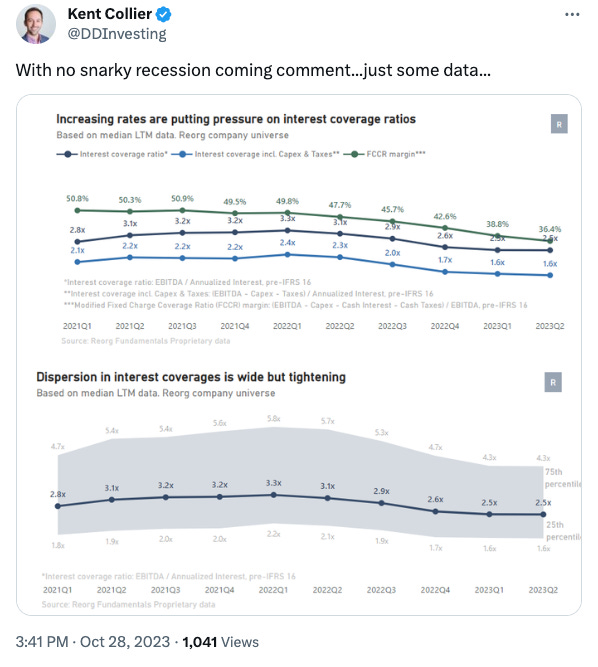

With interest rates rising quickly, leveraged buyouts currently feature much bigger equity checks from PE sponsors. The debt that has been issued by buyout targets yielded, on average in Q3’23, 11% (according to PitchBook LCD). The dividend recaps — and fraudulent conveyance allegations — to come are going to be spectacular.

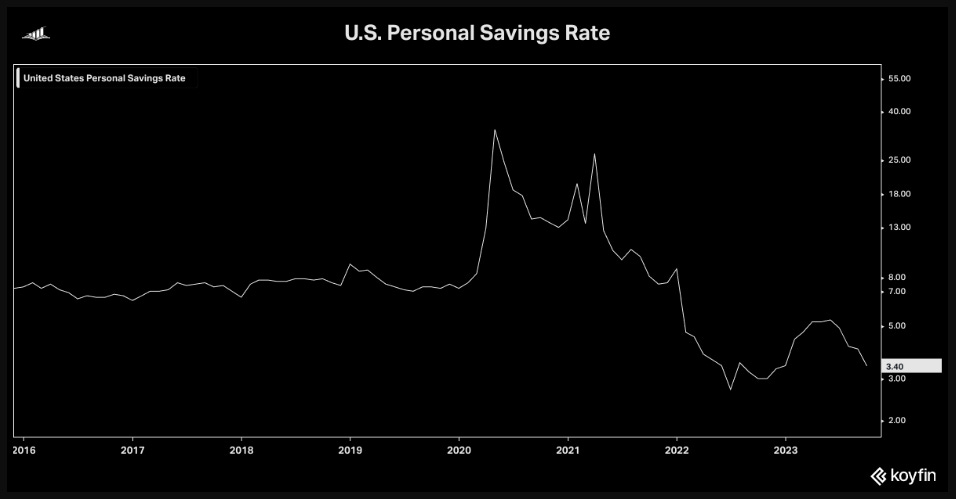

The Q3’23 GDP print blew the pants off of pretty much everybody and most definitely Jerome POW-ell. 4.9% was a massive upside surprise (against relatively robust consensus in the low 4s). People are still spending, spending, spending, and we haven’t even gotten to the key holiday shopping season yet. Watch these trends:

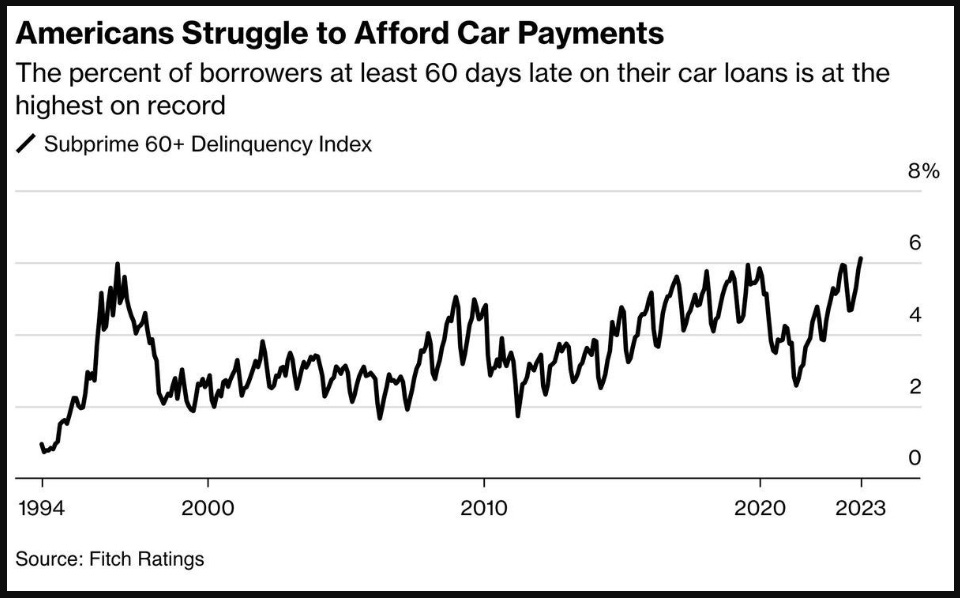

Of course, there are pockets of pain. Check out the increase in borrowers at least 60 days late on their subprime auto loans:

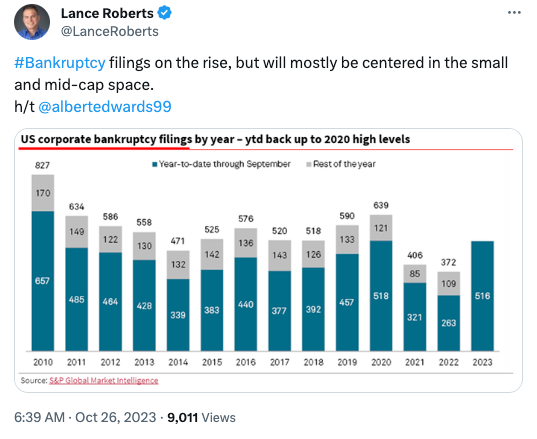

Bankruptcies are up. Per the Administrative Office of the U.S. Courts, “[t]otal bankruptcy filings rose 13 percent, and business bankruptcies rose nearly 30 percent, in the twelve-month period ending Sept. 30, 2023. This continues a moderate rebound after more than a decade of sharply dropping totals.”

Private credit providers may want to bolster their in-house workout teams. Per Bloomberg:

“Direct lenders have been siphoning business from the broadly-syndicated leveraged loan market in recent years, in part by staking a claim to increasingly larger deals. But an analysis by the credit-rating firm shows that legal safeguards that protect investors tend to weaken as the size of the transactions increase. “Private credit is dropping maintenance covenants in larger deals,” analysts including Derek Gluckman wrote in a Thursday report, referring to a type of investor protection that requires companies to periodically meet certain tests of financial health. Leveraged loans discarded the safeguards years ago and most are now considered ‘covenant-lite.’ Direct lenders are following suit, Moody’s says, noting that only 7% of private credit loans larger than $500 million in its analysis had maintenance covenants, compared to 67% of loans smaller than $250 million. Moody’s has already written that the competition between banks and direct lenders in the leveraged buyout arena will likely result in more defaults as riskier debt deals get done, part of a “race to the bottom” between the two groups as they compete for a limited number of financings. Weaker protections suggest private credit firms could be in store for more pain than previously expected should their loans sour.

”

And, finally, on Friday we learned that Jerome POW-ell & the Gang’s fave inflation measure — core PCE — clocked in at an accelerated rate in the month of September, up 0.3%. Core inflation (annualized) hit 3.7%. We’re not math experts by any stretch of the imagination but that figure still seems meaningfully above the Fed’s 2% target rate. Combined with the GDP print and consumer spending data, the Fed has all of the ammo it needs to keep hiking rates. Just probably not at the upcoming meeting. Or so says the market. We’re old enough to remember when people thought rates would be coming down in ‘24 but it sure doesn’t look that way right now. Those of you who expected things to be busier at this point than they are have something to look forward to in 1H’24. 💪

⏩One to Watch: Ebix Inc. ($EBIX)⏩

We’ll see if this one makes it that far without tripping into a bankruptcy court first…

GA-based Ebix Inc. ($EBIX) is an international supplier of on-demand software and e-commerce services to insurance, financial, and healthcare companies; its product offerings include infrastructure exchanges, carrier systems, agency systems, and risk compliance solutions. Put simply, if you’re an insurance/financial/healthcare company and you need to better manage policies, claims, customer information, etc., you might reach out to Ebix and say, “Hey, help us run our business more efficiently with cool software!” and they’ll likely jump at the opportunity.