💥Concepts of a Plan💥

Vertex Energy Inc. files chapter 11 cases with many pathways to pursue.

💥New Chapter 11 Bankruptcy - Vertex Energy Inc. ($VTNR)💥

On September 24, 2024, Houston-based Vertex Energy Inc. ($VTNR) and 23 affiliates (the “debtors”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez). We saw trouble brewing with this name early in the summer and so we’re not surprised the debtors are here:

Founded in ‘01, the debtors began as collectors and re-refiners of used motor oil (“UMO”) — a humble role perhaps, far from the boom-and-bust high drama of wildcatting, but essential to the petrochemical food chain. The debtors, though, had bigger ambitions. They wanted to be a “new kind of UMO company,” CRO Seth Bullock, a managing director at Alvarez & Marsal North America LLC, writes in his first day declaration.

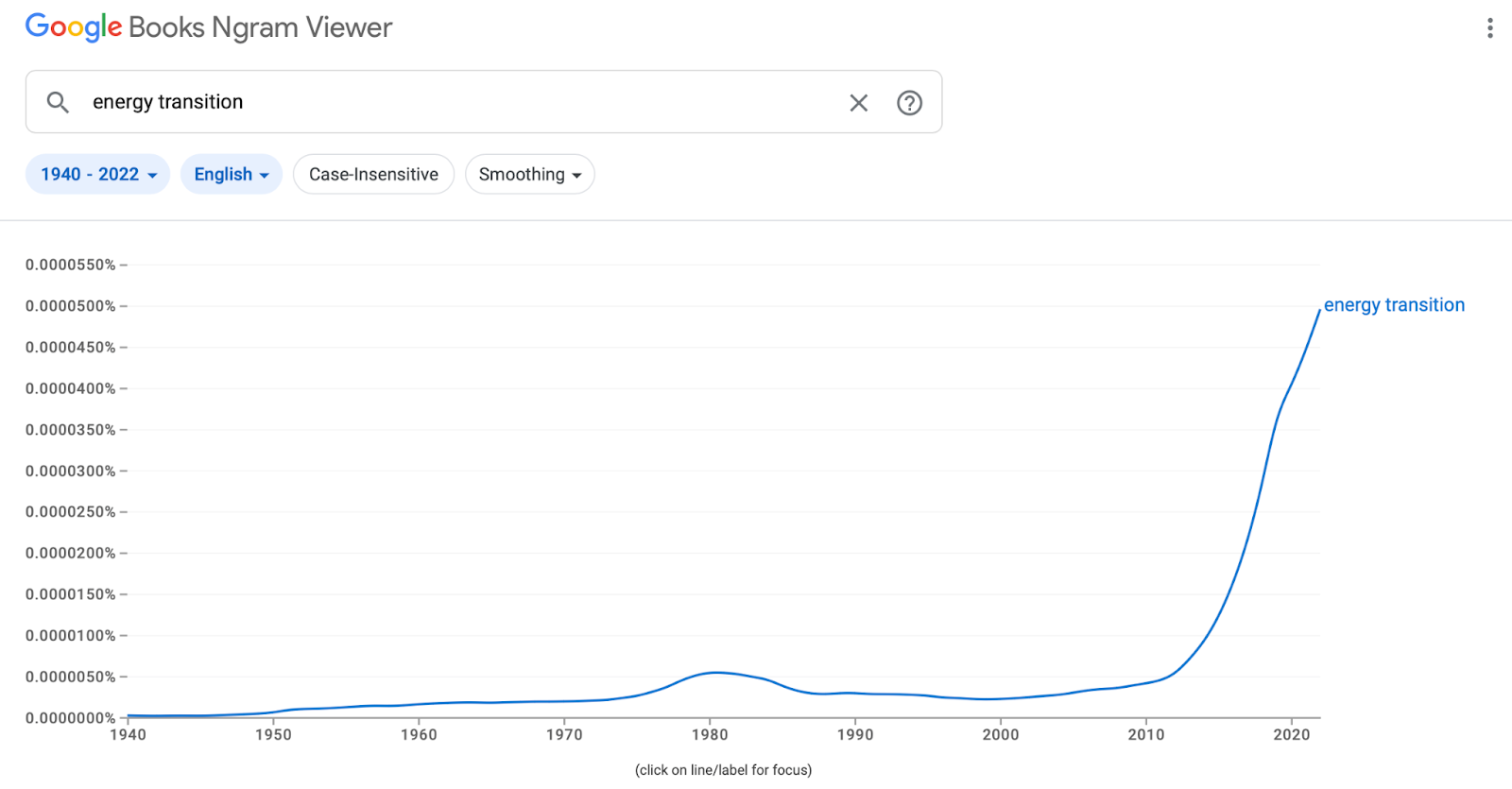

“Energy transition” offered an opportunity. The idea has experienced a dramatic increase in interest over the past decade, according to Google’s NGram Viewer.

And in ‘20 or so, it did not go unnoticed at the debtors that the U.S. was throwing gargantuan sums into this energy transition. That the technologies were unproven did not matter: mistakes just happen during revolutions, the thing is to keep the eyes on the prize and get the projects funded. And for all we know, the debtors wanted to be the “good guys,” on the side of “environmental justice” and “the right side of history.” So on May 26, 2021, the debtors announced the purchase of a refinery in Mobile, Alabama, part of which the debtors would convert to biofuel production, specifically renewable diesel. A cynic might say they were looking to goose the share price, pretty much dead money since the Great Financial Crisis. It worked — energy transition was the AI of ‘20.*

“Renewable diesel was not only a sizable growth opportunity, but also an industry shift that the Company was especially well-positioned to seize,” Bullock writes. “In order to make the most of this moment,” the debtors hired Matheson Tri-Gas Inc. (“Matheson”) to build a “steam reformer hydrogen facility” in the plant, renewable diesel requiring that element. Once that was finished, the debtors could “reformat” parts of the refinery’s infrastructure to produce the precious bio-juice and then …

“Vertex anticipates that the refinery will have the potential to generate at least $3 billion in annual sales and $400 million of gross profit annually beginning in 2023, given current refining economics,” the debtors said in the press release announcing the deal (our emphasis).

Some smart, or at least, deep-pocketed, investors — BlackRock Financial Management Inc., Whitebox Advisors LLC, and Highbridge Capital Management LLC — bought this malarkey, and backed the debtors’ schemes with a $125mm term loan. They weren’t the only ones. Shareholders were also over-joyed and the stock surged:

The joy proved fleeting. Failing to deliver on lofty promises of dramatic increases in gross profit is a good way to get the sh*t sued out of you. Enter “shareholder rights” shops like Brager Eagel & Squire PC, or Kahn Swick & Foti LLC or the Gross Law Firm — all of which have filed against the debtors because of “…the Company’s more recent attempt to capitalize on the growing market for renewables fell short of expectations,” Bullock writes. Whoops!

The debtors sold their first batch of renewable diesel in June ‘23. “The Company forecasted that the Mobile Refinery’s renewable diesel production volumes would increase to approximately 8,000 bpd by the third quarter of 2023. Unfortunately, reality fell far short of expectations,” Bullock says. It often does, Seth, it often does. We shared this glimpse of “reality” in our initial story:

The debtors did what they could with their limited options. CFO Christopher Carlson stated on the Q1 ‘24 earnings call that the debtors made a “strategic decision” to “pause and pivot” from renewables to higher-margin conventional products until the “conversion” was finished. Which will be … when, exactly?

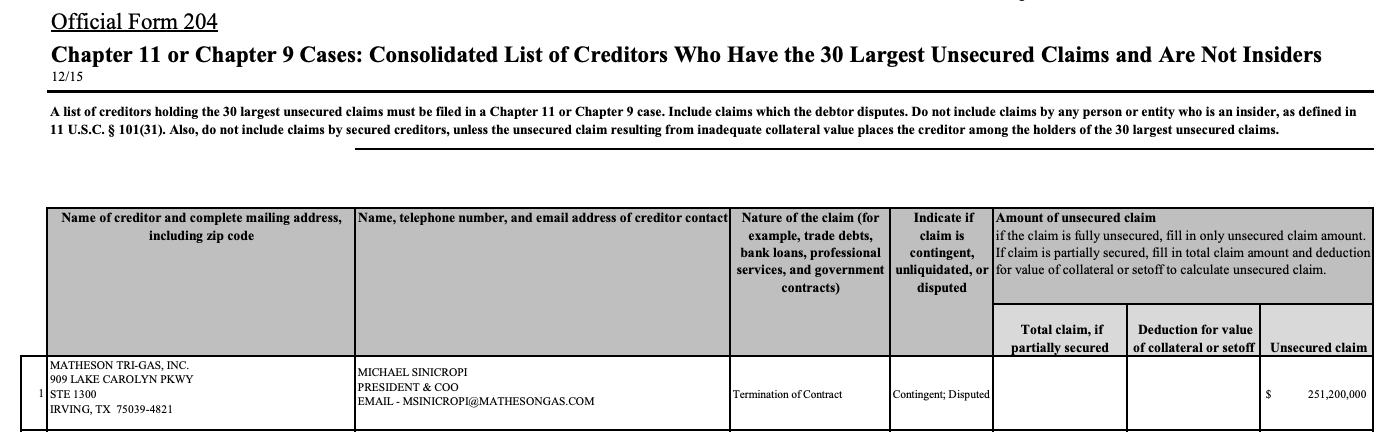

The debtors and Matheson originally targeted August ‘23 for the start of commercial operations. The debtors and A&M now estimate construction will not be completed until Q3‘25, meaning it’s unlikely to be fully operational by 2Q‘26. “Moreover, my understanding is that the Company and A&M’s July 2024 site visit to the Mobile Refinery eroded what little confidence they had left in Matheson’s management of the project, which has, to date, resulted in significant construction delays and cost overruns,” Bullock states. The delays have exposed the debtors to some $251mm of liabilities that “will only continue to balloon in tandem with the prolonged timeframe for completion.” Not surprisingly, the debtors intend to reject the Matheson contract, which would have the extra benefit of conferring this honor upon Matheson:

That’s right. Matheson would be the debtors’ top general unsecured creditor. But don’t weep for Matheson, y’all: general unsecured creditors are set to get paid in full in these cases, right?

Well, dear friends, keep reading to find out!

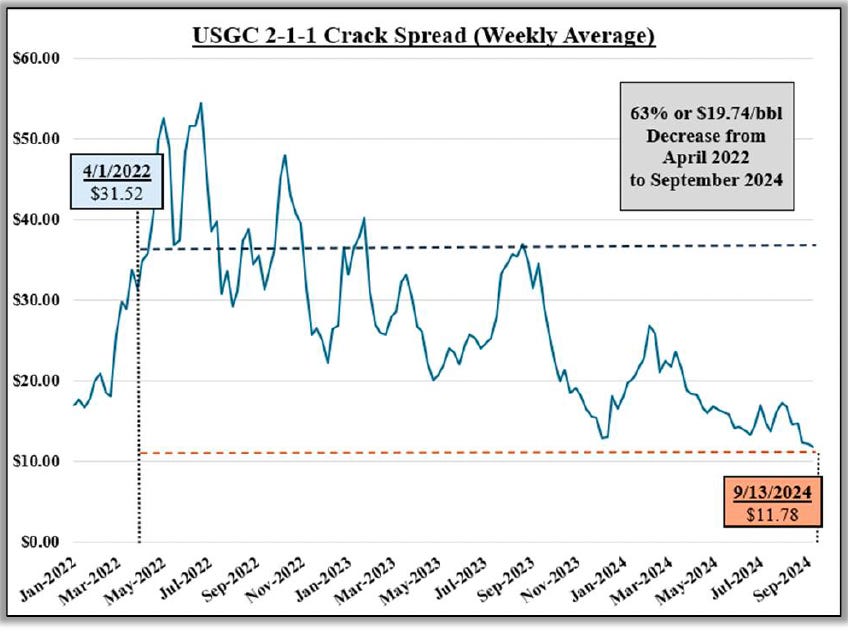

It would be bad enough if a non-functioning refinery was the debtors’ only aggravation, but it wasn’t. There was something arguably worse: the crack spread.

Crack spreads measure the difference between the cost of crude oil and the price of refined gasoline; refiners use it as a back-of-the-envelope method to guesstimate the profitability of a given refinery configuration. The debtors use the “2-1-1” spread, which measures the cost of two barrels of crude oil against the price of a barrel of diesel and the price of a barrel of gasoline. The spread has gone drastically against the debtors over the past several years:

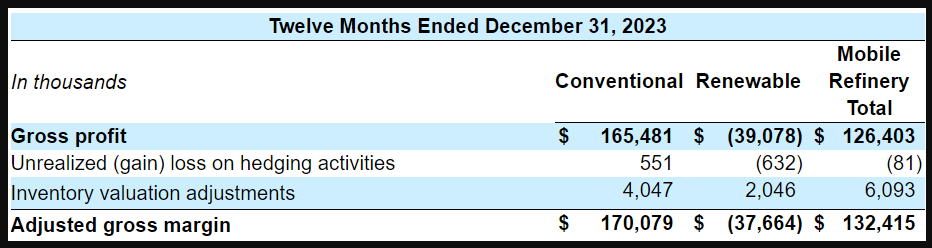

This explains the ugliness of the Mobile refinery’s gross profit in 2Q‘24, reported on August 8, 2024: $6.4mm compared to $37.5mm in Q1’24. As a reminder, that was conventional production. The absence of renewable production brought woes of its own.

The Federal government looks dimly upon those refiners unable to produce their assigned quota of renewables under the Federal RFS, or “renewable fuel standard” program (the “Program”). The Program requires refiners “to blend a minimum amount of on-road transportation biofuels, such as gasoline mixtures that incorporate renewable products like ethanol,” Bullock writes. Should refiners fail to produce the volumes required by the EPA, they will “accrue monetary obligations payable to the federal government.”

The EPA sets renewable volumes annually, based on factors including “current climate change policy” and air quality. Uh oh: “Just as Vertex and the rest of the private sector responded to the sharp increase in biofuel demand, so too did the EPA—the Agency saw the moment as an opportunity to increase the renewable volume obligations even more to encourage even faster adoption of renewable fuels.” Never let a crisis go to waste, after all. The EPA demanded an additional 120mm gallons in ‘23, “which required fuel refiners like Vertex to blend nearly 21 billion gallons of renewable fuel in 2023 and 21.5 billion gallons in 2024.” The debtors were unable to meet their obligations, as a result of which $72.5mm of “monetary obligations payable to the federal government” will “accrue” by Q1‘25. Ironically, even if the debtors had produced the required volumes, they would not have been as profitable as they’d hoped. Why not? Because the debtors were not the only ones to think of “pivoting” to biodiesel in ‘20; there’s now a supply glut.

“Thus, in 2023, the Company faced a ‘perfect storm’ made up of the looming renewable volume obligations, a shell of a Hydrogen Facility, unstable crack spreads, and a surplus of renewable energy supply in the market. Simply put, the rich renewables market that the Company once projected and planned for was slipping away just as crack spreads more generally were compressing.”

The debtors explored asset sales, including the renewable diesel segment at Mobile. “No actionable transactions materialized,” which is hardly surprising.

We mentioned Q2 earnings and the disastrous plunge in refinery gross profits. The debtors in their press release disclosed the “continued safe operation” of the refinery, but that was about it for the not-bad news. They reiterated the “pause and pivot,” and confirmed they are on-schedule for the conversion of the renewable diesel unit back to conventional production.

CEO Benjamin P. Cowart said in the same release that the debtors were continuing to explore strategic options. He announced the appointment of Bullock as CRO. “We believe that continued support from our lenders is key to executing our strategic priorities which are focused on managing our liquidity position.”

The lenders have been helpful. Over the summer of ‘24, the debtors and their advisors —A&M, Kirkland & Ellis LLP as legal counsel and Perella Weinberg Partners LP ($PWP) as investment banker — sat down with an ad hoc group of term loan lenders represented by Sidley Austin LLP and Houlihan Lokey ($HLI). “It became clear that any viable path forward would require incremental liquidity,” Bullock observes. A third-party lender under the existing term loan facility provided $20mm on July 24; the Consenting Lenders did their bit with a $25mm bridge on August 23, again under the pre-petition facility, as talks continued and the parties got their papers in order. The debtors appointed Mr. Jeffrey Stein — fresh off of his hotly contested, and highly lucrative, seat as CEO/CRO of Rite-Aid — as an independent director “to ensure a thorough and fair process” as they reviewed strategic alternatives, considered transactions, and pondered what to do with their funded debt:

And hallelujah! The debtors cut a deal!! And it doesn’t cost anyone a $20mm pay package for Mr. Stein (as far as we know)!!! 🖕

A deal? The debtors filed with a restructuring support agreement (“RSA”) backed by 100% of term loan lenders (the “consenting lenders”). The RSA conjures up memories of former President Donald J. Trump who recently said:

Why? Because the plan — small “p” — is to leave every imaginable option open for the time being, LOL, so long as it occurs within a super tight timeframe. Ok, fine, a bit of hyperbole, but the plan does leave open three main pathways:

📍A sale to a third party;

📍A sale to existing lenders (DIP and/or pre-petition) via credit bid; or

📍A recapitalization.

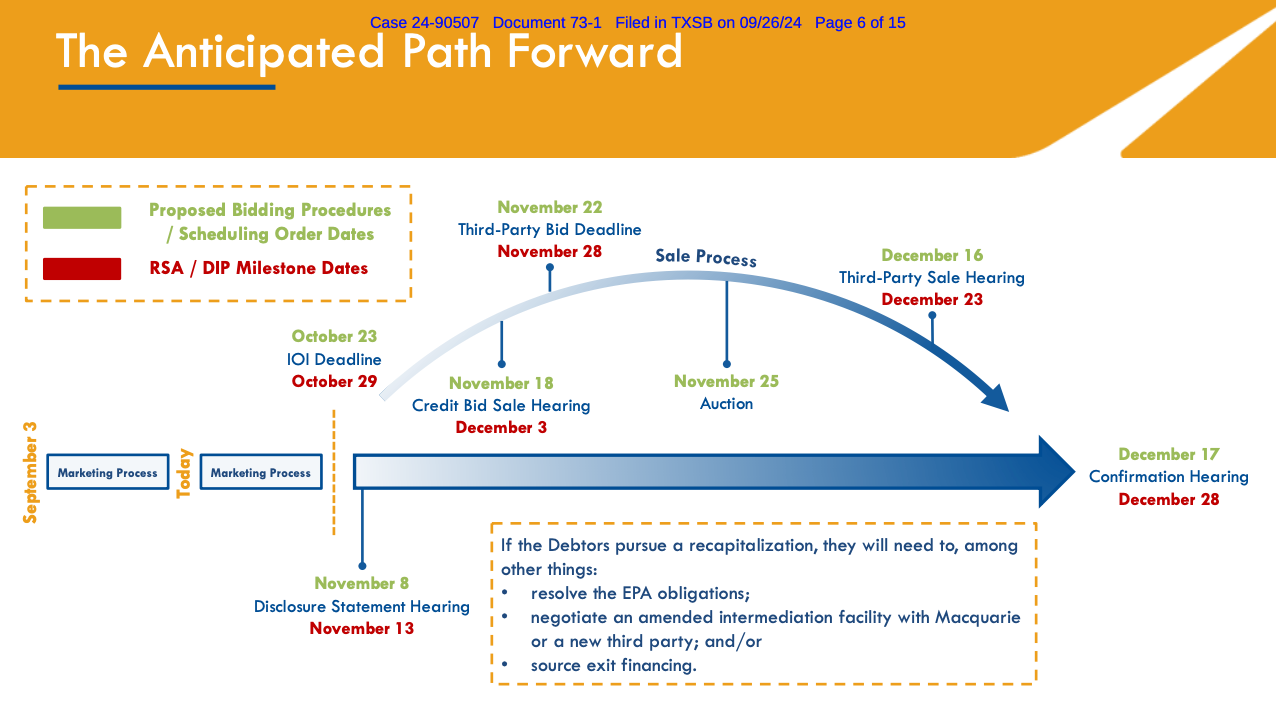

And there’s already a bid procedures order entered by Judge Lopez on the docket. Is there a stalking horse? Obviously not, lol. Are there bid protections? Nope, not yet. Optionality, people, c’mon! Don’t want to chill any interested parties from submitting their completely non-binding “indications of interest” (“IOI”) by October 23, 2024. That’s right, the process affords PWP the next three-ish weeks to see if they can find potential buyers under a rock somewhere. Per the debtors:

The Indications of Interest will provide the Debtors a clear picture of the ultimate shape of these chapter 11 cases.

In other words, we have an RSA and even a Plan — capital “P” — and disclosure statement on file but it’s still kind of a plan, small “p”, until late October. If parties do submit IOIs, they’ll then be required to submit a qualified bid by November 22, 2024.

Pursuant to the proposed Bidding Procedures, if the Debtors receive one or more Indications of Interest for an actionable proposal, the Debtors will move swiftly toward an auction.

If this plays out, a sale hearing would follow on December 16, 2024.

But what if said rock isn’t sheltering any interested parties? Well, the consenting lenders have an opportunity to submit a credit bid. Per the debtors:

However, if the Debtors do not receive any Acceptable Indications of Interest for any of the Assets prior to the Indication of Interest Deadline, the Debtors may terminate the marketing process and cancel the Successful Bidder Sale Hearing. Moreover, to the extent the Consenting Term Loan Lenders submit a Credit Bid for all or a portion of the DIP Claims and/or Term Loan Claims (the “Credit Bid Sale”), the Debtors may pursue the accelerated timeline contemplated under the Bidding Procedures.

Bullock provides the following illustration of the dual-track sale process:

Honestly, it’s all kinda “weird” — a word that seems to be making the rounds these days. GUCs like Matheson, however, had better hope there’s a deep-pocketed buyer. The only way they get a recovery is if there’s “Excess Distributable Cash” from a sale that clears the DIP and term loan.

So what happens if there is no sale process? The debtors will pivot to a recapitalization transaction. This basically means that the term loan will be equitized. Bullock says, should the debtors choose the recapitalization, “there are a number of key issues that they will need to address during this process.” Top of the list is (i) the $72.3mm owed the Federal government under the Program, (ii) negotiating an amended intermediation facility and/or (iii) sourcing exit financing. You know what Matheson gets under this scenario? A big fat 🍩. At least the consenting lenders agreed to a wind-down reserve though to help get this sucker to a plan of liquidation! Magnanimous!!

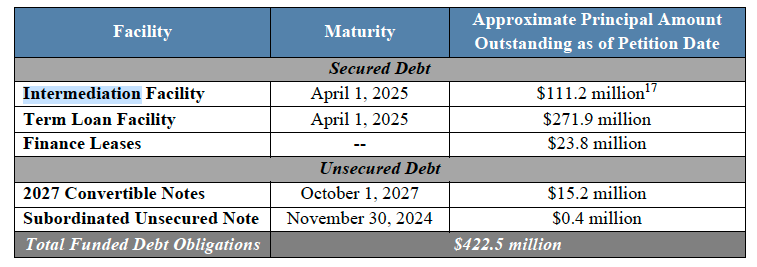

There’s another component to the RSA that is a bit more definitive: a DIP credit facility. Indeed, the debtors seek to fund the cases via the use of their lenders’ cash collateral and a $280mm super-senior secured DIP facility committed to by the consenting lenders, comprising $80mm of new money term loans bearing interest at S+950bps and a roll-up of certain pre-petition loans. Of the new money, approximately $39.4mm will be available on an interim basis and $40.6m on a final basis. Regarding the roll-ups, $37.9mm of 2024-1 Term Loans will be rolled into the DIP facility on an interim basis. On entry of a final DIP order, $135.2mm of initial term loans or additional term loans (“restricted roll-up”) and $26.8mm of 2023 term loans (“final roll-up”) will roll up. All will be on a pari passu basis, with the initial and final roll-ups bearing interest of S+940bps and the restricted roll-ups S+960. The “Maximum Roll-Up Ratio” of DIP Roll-Up Loans to DIP New Money Loans will not be greater than 2.5:1 in the aggregate. The facility bears a 3% commitment fee and a 3% closing fee.

The debtors won interim approval of the DIP at the first day hearing held on September 25, 2024; they also received authorization for the use of an amended intermediation facility and amended hedging agreements — both with Macquarie Bank Limited (“Macquarie”) –used to finance purchases of crude oil and feedstocks. A “second day” hearing is scheduled for October 16 at 9 a.m. ET in Houston.

The debtors are represented by Kirkland & Ellis LLP (Brian Schartz, Josephine Fina, Brian Nakhaimousa, Rachael Bentley, John Luze) and Bracewell LLP (Mark Dendinger, Jason Cohen, Jonathan Lozano) as legal counsel; Alvarez & Marsal North America LLC (R. Seth Bullock) as financial advisor and Perella Weinberg Partners LP (Douglas McGovern) as investment banker. The consenting lenders are represented by Sidley Austin LLP (Genevieve Weiner, Ian Ferrell) as legal counsel and Houlihan Lokey ($HLI) as financial advisor.

And now we wait and see what comes by October 23, 2024. We reckon PWP hopes no prospective buyers do this:

*The company reviewed its history and discovered that it had been on the side of the angels all along! Corporate history was rewritten reimagined: “Vertex has helped lead the energy transition by reducing carbon impacts for over 20 years.” It has? Vertex is no humble scavenger of UMO: it is an “energy transition catalyst,” or something.

🍾Congratulations to…🍾

Dundon Advisors LLC (Peter Hurwitz) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the Blink Holdings Inc. chapter 11 bankruptcy cases.

Eversheds Sutherland US LLP (Todd Meyers, Jennifer Kimble, Sameer Alifarag) and Morris James LLP (Jeffrey Waxman, Eric Monzo, Christopher Donnelly) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Fulcrum BioEnergy Inc. chapter 11 bankruptcy cases.

Faegre Drinker Biddle & Reath LLP (Kristen Perry, Kaitlin Prior, Richard Bernard) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Barrow Shaver Resources Company LLC chapter 11 bankruptcy case.

Kelley Drye & Warren LLP (James Carr, Jason Adams, Philip Weintraub, John Ramirez, Connie Choe) and Chipman Brown Cicero & Cole LLP (William Chipman Jr., Mark Olivere) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Edgio Inc. chapter 11 bankruptcy cases.

McDermott Will & Emery LLP (Darren Azman, Kristin Going, Stacy Lutkus, Natalie Rowles) and Cole Schotz PC (Justin Alberto, Stacy Newman, Sarah Carnes) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Big Lots Inc. chapter 11 bankruptcy cases.

Riveron RTS LLC (Paul Jansen) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the Barrow Shaver Resources Company LLC chapter 11 bankruptcy case.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.