😷New Chapter 11 Bankruptcy - CareMax Inc. ($CMAX)😷

Steward's bankruptcy filing dominoes into a CareMax filing.

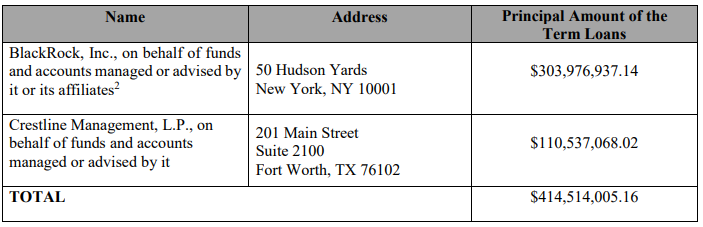

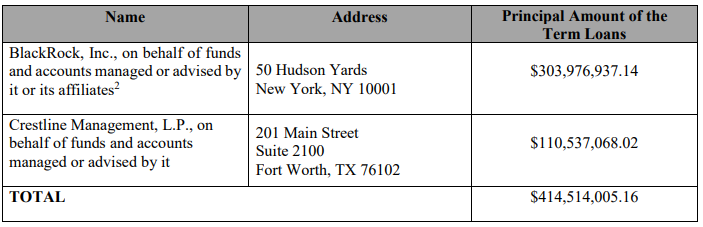

On November 17, 2024, CareMax Inc. and 53 affiliates (collectively, the “debtors”) FINALLY filed chapter 11 bankruptcy cases. The filing, which dropped in the Northern District of Texas (Judge Larson), sets the stage for a sale of the debtors’ management services organization (“MSO”) and, separately, the debtors’ core center assets — all pursuant to a prearranged plan of reorganization supported and backstopped by 100% of the debtors’ existing secured lenders who are the holders of the debtors’ only funded debt: a $422.6mm prepetition term loan.

We initially covered the debtors following the chapter 11 filing of Steward Health Care System LLC:

In that piece, we remarked that the Steward bankruptcy filing could put significant pressure on CareMax. And yep…

Here’s CRO, Paul Rundell, in his first day declaration:

“Specifically, CareMax contracted with Stewardship Health, Inc. ('Stewardship Health') across Steward’s (a) employed physician providers and (b) the non-employed, affiliated physician providers in Stewardship Health’s network. On June 22, 2024, Stewardship Health filed a motion seeking to wholesale and abruptly reject its business relationship with CareMax in connection with the Steward chapter 11 cases, which posed an existential threat to CareMax’s MSO Business (including the ACO Business).”The debtors acquired Steward’s value-base care business in November ‘22 and integrated it into the MSO business. The debtors and Steward maintained certain contracts following the transaction and the debtors became the exclusive value-based MSO across Steward’s Medicare network.

That is until Steward broke up with the debtors using the powers invested in them through the bankruptcy court.

Lol actually, according to Steward in their June ‘24 rejection motion, it most definitely was “you”:

“However, the CareMax-Steward Contracts are not profitable for the Debtors, present potential impediments to the Debtors’ maximizing value for the benefit of their estates and creditors, and are burdensome to the Debtors (as well as to the Providers, who, since the Closing, have experienced operational challenges in their relationship with CareMax). More specifically, the Debtors do not yield economic benefits from the CareMax-Steward Contracts. The Medicare VBC Contracts and CareMax-Steward Contracts are structured such that CareMax earns a significant profit from the time and resources expended by the Debtors and their Providers while the Debtors only receive a limited amount of such earnings from the provision of services, including the transition services that are necessary for CareMax to profit from the Medicare VBC Contracts. Further, CareMax, who is experiencing its own financial distresses, has failed to perform its payment obligations under its transition services agreement with the Debtors.”And when the debtors started exploring strategic alternatives, one of the discussed options was a sale of the MSO business. But the business was so inextricably intwined with Steward that potential buyers were unwilling to participate without the cooperation of Steward. Thus, in ‘23, the debtors and Steward teamed up and jointly marketed CareMax’s MSO business and Steward’s managed care business, Stewardship Health. By February ‘24, Steward terminated the joint sale agreement and then filed its chapter 11 bankruptcy cases in May ‘24.

😬 … it turns out that the rejection motion was actually break-up number 2.

This left the debtors alone to continue their marketing process and in a turn of good fortune (as good as a prepackaged bankruptcy can get), the buyer of Stewardship Health, RHG Network LLC (a subsidiary of Kinderhook Industries LLC), stepped in to also swoop up the three accountable care organizations (“ACOs”) operating under the MSO business. The purchase agreement was entered into on November 17 (same day as the filings) and will see the debtors receive $10mm in cash along with a portion of future Medicare Shared Savings Program (“MSSP”) payments. Luckily there’s a fiduciary out clause the debtors could exercise if a better offer pops up during bankruptcy but the debtors will have to eat a $2mm break-up fee.

With the MSO business transaction done and dusted, the debtors have been marketing their remaining 40 value-based care medical centers in Florida (the “core centers”). There’s currently a third party purchaser that is potentially stepping up to the plate as stalking horse for these centers. Talks are still ongoing and definitive documentation for the stalking horse purchase is expected to be filed on or around November 24th (as of the time of this writing, however, we haven’t seen it hit the docket). But, if the stalking horse purchase falls through, the prepetition secured lenders are prepared to come in with a backup credit bid.

So while there is a plan on file, there are still a lot of unknowns, specifically on the core centers sale.

To effectuate the two sale transactions, the debtors have secured a $122mm DIP facility from the prepetition term loan lenders of which $30.5mm is new money ($12mm on interim order and $18.5mm on final order). The $91.5mm roll-up will occur upon the entry of the final order.

The DIP facility carries an interest rate of S+1100 bps PIK and an exit premium of 10% on the new money portion.

The debtors are set to emerge early ‘25, just in time for Donald Trump’s nominee, Dr. Mehmnet Oz, to (potentially) helm the Centers for Medicare and Medicaid Services (“CMS”).

Failing upwards Dr. Oz! Hopefully you don’t have the taste of the ‘22 Pennsylvania Senate defeat still in your mouth.

The debtors are represented by Sidley Austin LLP (Thomas Califano, Julliana Hoffman, Stephen Hessler, Anthony Grossi, Jason Hufendick, Margaret Alden, Ryan Fink, Veronic Courtney, Hayden Golemon, Andreas Rauch) as legal counsel, Alvarez & Marsal LLC (Paul Rundell) as financial advisor, and Piper Sandler & Co. (Dustin Mondell, Bilal Bazzy) as investment banker. Kinderhook Industries LLC is represented by Kirkland & Ellis LLP (Brian Schartz, Peter Candel) and Bracewell LLP (Jason Cohen, Jonathan Lozano). The prepetition term loan lenders are represented by Ropes & Gray LLP (Matthew Roose, Tessa Ptucha) and Kelly Hart & Hallman LLP (Katherine Hopkins) as legal counsel.

Company Professionals:

Legal: Sidley Austin LLP (Thomas Califano, Julliana Hoffman, Stephen Hessler, Anthony Grossi, Jason Hufendick, Margaret Alden, Ryan Fink, Veronic Courtney, Hayden Golemon, Andreas Rauch)

Financial Advisor: Alvarez & Marsal LLC (Paul Rundell)

Investment Banker: Piper Sandler & Co. (Dustin Mondell, Bilal Bazzy)

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

ACO Purchaser: Kinderhook Industries, LLC

Legal: Kirkland & Ellis LLP (Brian Schartz, Peter Candel) and Bracewell LLP (Jason Cohen, Jonathan Lozano)

Prepetition Term Loan Lenders, DIP Lender, and Ad Hoc Group

Legal: Ropes & Gray LLP (Matthew Roose, Tessa Ptucha) and Kelly Hart & Hallman LLP (Katherine Hopkins)