🦞(Blood) Red Lobster. Part II.🦞

🦞(Blood) Red Lobster. Part II.🦞

Also: Another AMC Entertainment Holdings Inc. ($AMC) update.

THE. MOTHERF*CKING. GOLDEN. AGE. OF. PRIVATE. CREDIT. Y’ALL.

You’ll recall that nearly three months ago, on May 19, 2024, Orlando-based Red Lobster Management LLC (“Red Lobster”) and 14 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the Middle District of Florida (Judge Robson).* The so-called Seafood Alliance, made up of Thai Union Group Public Company Ltd ($TU), former management, and other third party investors, ran this f*cker into the ground with, among other things, misguided all-you-can-eat seafood specials. Apparently the Thai failed to remember that North Americans — and especially Americans — are fat and unhealthy as f***********ck. The masses stormed the doors of the 551 locations and ate enough shrimp to empty an ocean. Luckily TU engaged in some insider-y supply side shenanigans that may or may not have, 🙄, vastly undermined the debtors’ operational performance, 🤷♀️.

One day some poor schmo of an analyst at Fortress Credit Corp. (“Fortress”), the debtors’ pre-petition term loan lender, happened to drive by a local Red Lobster and see a line around the block. He was like, “daaaaaaaaaamn” with a big satisfied smile on his face; he started dreaming about that sweet, sweet bonus check. That is, until he saw the debtors’ actual financial performance, which stunk like a unplunged kid’s camp toilet. At that point he be like, W.T.F., and called in the cavalry. Fortress’ big wigs took one look at the financials, said “f********ck this!,” and exercised proxy rights existing under the pre-petition credit agreement, sacked the board, inserted its own representative, sh*tcanned existing professionals, hired its own professionals, and lent the debtors some bridge financing for working capital purposes as they scoped the landscape.

What did they see? Well, the ~$294mm of funded secured debt was hard to miss. And so was the fact that this sucker was going to have to file and Fortress was gonna have to drive the bus. As we covered here …

… Fortress and the debtors entered into a restructuring support agreement (“RSA”) that teed up ownership of the company in Fortress’ favor. There was a DIP commitment featuring a big roll-up of the pre-petition term loan. There was a proposed credit bid. And, naturally, there was a wink and a nod towards an in-court sale process constrained by some pretty aggressive sale milestones in the DIP. The RSA also contemplated aggressive shedding of leases. On the first day of the case, the debtors filed four motions to reject a total of 228 leases.

So what’s happened since?

Suffice it to say the nine-member official committee of unsecured creditors (“UCC”) — which included some names like PepsiCo Inc. ($PEP) and Realty Income Corporation ($O) — wasn’t too pleased with Fortress. The UCC hired Pachulski Stang Ziehl & Jones LLP (Bradford Sandler, Robert Feinstein, Cia Mackle, Paul Labov, Maxim Litvak, Theodore Heckel)(“Pachulski”) and Pack Law (Joseph Pack, Jessey Krehl) as legal counsel and Genesis Credit Partners LLC (Edward Kim) as financial advisor and they got to work constructing some homemade grenades. The first target? The proposed DIP roll-up.

On June 12, 2024, the UCC filed an objection to the proposed DIP and boy was it a stem-winder. Contemporaneously, the UCC filed a motion seeking standing to pursue “certain claims” on behalf of the estates. Claims? What? Why? Will TU be called to answer for Endless Shrimp? Will TU explain why their shrimp is rubbery and tasteless compared to those from the Gulf Coast? No, it’s the liens and security interests. The UCC sought to reverse certain acknowledgements and agreements of the debtors set forth in the proposed final DIP order and go on the attack with their basement-built projectiles. The lawyers rage against “…the massive and inappropriate ‘land grab’ at the expense of unsecured creditors. The Prepetition Term Loan Lenders want to roll-up (i.e., cross-collateralize) $175 million of their prepetition debt, some of which is presumably underwater, and secure it with new liens on extremely valuable, previously unencumbered assets of the Debtors.” Add some fists-pounding –- mahogany FX, and by damn, we’re 12 … well 9 … Angry Men! At the heart of the UCC’s argument: that Fortress had no evidentiary basis for a “finding that the Prepetition Secured Parties have a valid, perfected lien, claim, or interest in any of the Unencumbered Assets and any inconsistent finding should be stricken from the DIP Order.” The UCC was also offended that the DIP would allow Fortress to credit-bid on assets – specifically, restaurant locations – on which they have no lien. The proposed DIP’s terms are “unconscionable,” the UCC said.

The debtors gave back as good as they got:

“The Committee Objection paints a fanciful picture in which the DIP Facility is a devious scheme designed to bootstrap an allegedly undersecured prepetition debt into a bountifully oversecured DIP loan. The Committee’s unsupported allegations are divorced from reality.”

It’s all perfectly legal, in other words. Pachulski, the debtors sniff, is “armed with no evidence.”

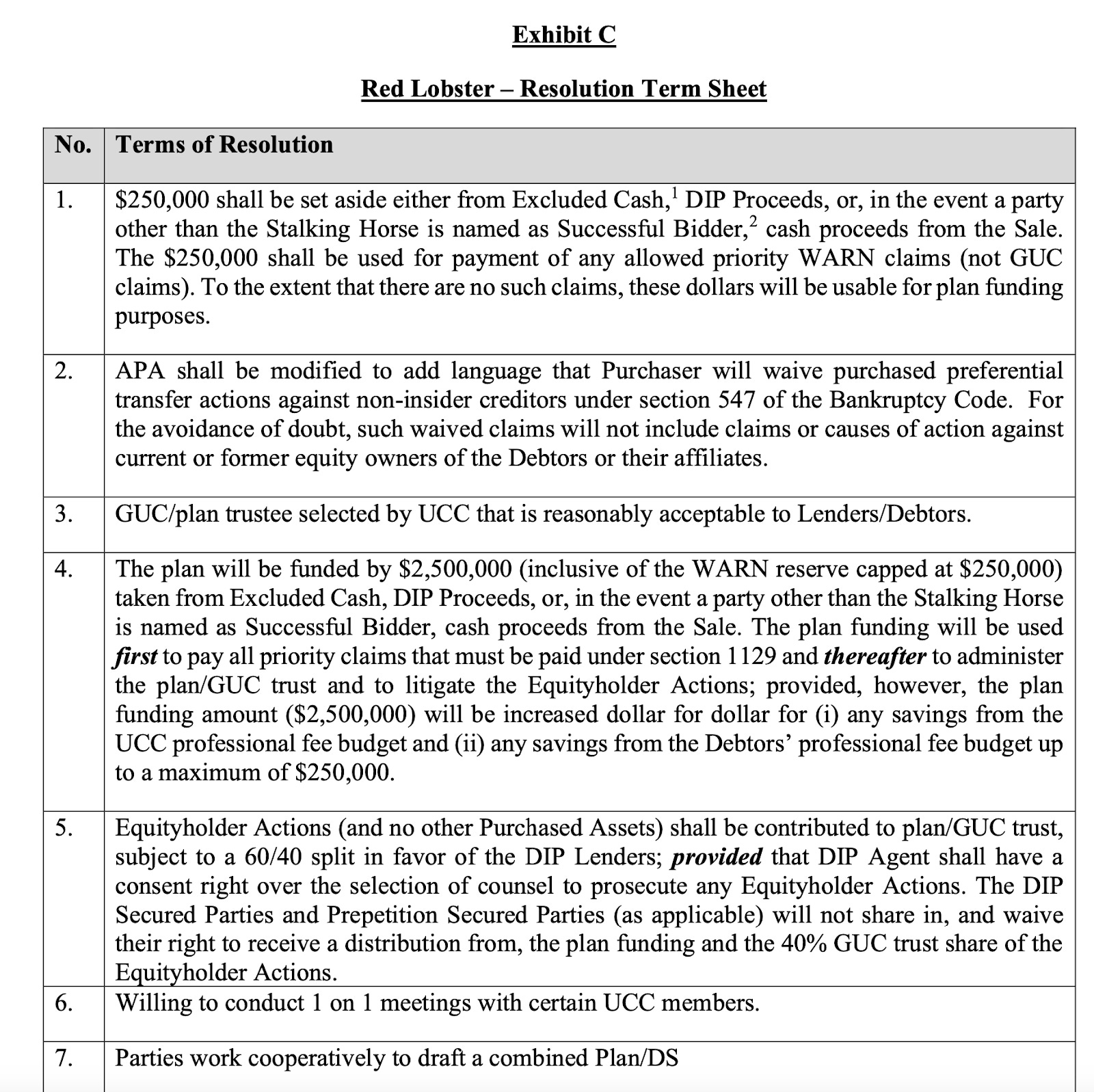

Well, maybe they weren’t properly armed, but the UCC got the debtors’ attention. On June 14, the debtors obtained final approval for the DIP motion. It maintained the “land grab” roll-up, and the fees, but this placated the UCC:

What does that resolution involve in plain english? Fortress ponied up! There’s actual money — technically $2.5mm — going to the general unsecured creditors. And there’s upside!! The UCC will get to go after TU and former directors and officers who are elegantly carved out of any plan releases. Any recovery from actions against TU will be split 60/40 in favor of Fortress to account for Fortress’ deficiency claim. As part of the settlement, Fortress also agreed to waive any potential preferential transfer actions against non-insider creditors which basically means that someone on the UCC didn’t want to have pre-petition monies it received clawed back and thrust into Fortress’ pockets. Finally, the UCC agreed to withdraw its standing motion.

So with that short battle out of the way, everyone could turn their attention to the mass of potential qualified bidders lining up at the debtors’ doors, right?

The bid deadline came and went with no one willing to challenge Fortress for ownership of this turd. Judge Robson approved the proposed sale on July 29, 2024. That happened to be one day after Judge Robson granted conditional approval of the debtors’ disclosure statement and authorized the solicitation of votes on the debtors’ proposed plan of reorganization.

There was one big modification, though. The proposed plan originally included “opt out” releases but in a post-Purdue-Pharma world, this may no longer be any bueno.

A combined disclosure statement and plan confirmation hearing is scheduled for Sept 5, 2024 with objections due on August 28, 2024. The debtors will emerge smaller: at least 93 restaurants will be shuttered through the bankruptcy process, according to the disclosure statement, which suggests that a good number of the landlords subject to the original first day rejection motions had a “come to Jesus” moment and executed new deals (from 228 to 93…?).

We’ll be keeping an eye out to see if any drama erupts at confirmation but it seems this thing is all but good to go. See you at the local Red Lobster for a bad drink and even worse shrimp — all powered by your friendly neighborhood Fortress. 👍

*You can find the PETITION case roster here.

** The United States Trustee also (“UST”) filed a limited objection, noting the roll-up “will give the lenders’ pre-petition debt to the entire post- petition collateral package and may render the pre-petition debt impossible to cram down in the context of an 11 U.S.C. § 1129(b) motion.”

***Unencumbered assets which included “avoidance actions, cash on hand in store locations, liquor licenses, and critical leases and real estate utilized in the Debtors’ ongoing operations.”

🔥AMC!!!🔥

We’ve been spending a lot of time on AMC Entertainment Holdings Inc. ($AMC) lately, in part because (i) it just pulled off one of the more interesting — and friendlier — liability management deals in quite some time and (ii) it’s CEO, Adam Aron, is, on one hand, a creative manager who excels at capturing cap/equity markets opportunity and, on the other, a liar who gets off on rug pulling (read: diluting) unsuspecting “investors” who, for some reason, happen to adore apes.* On Friday, AMC went ahead with what some might dub a cynical Friday aftermarket Q2’24 earnings dump.**

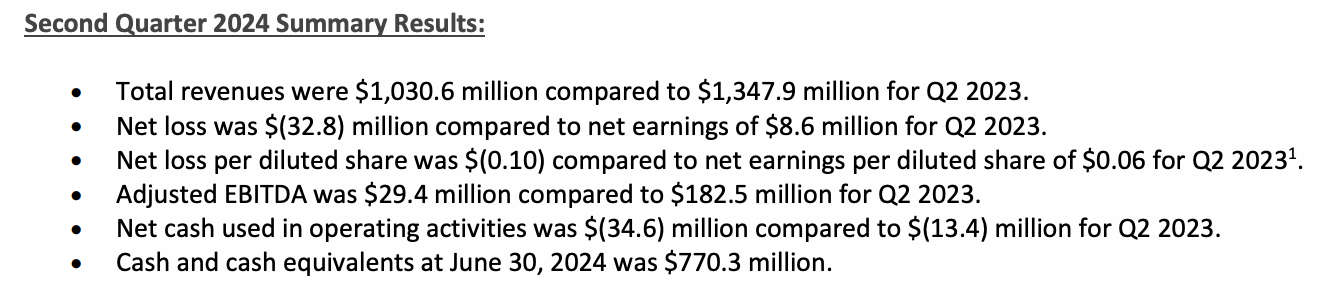

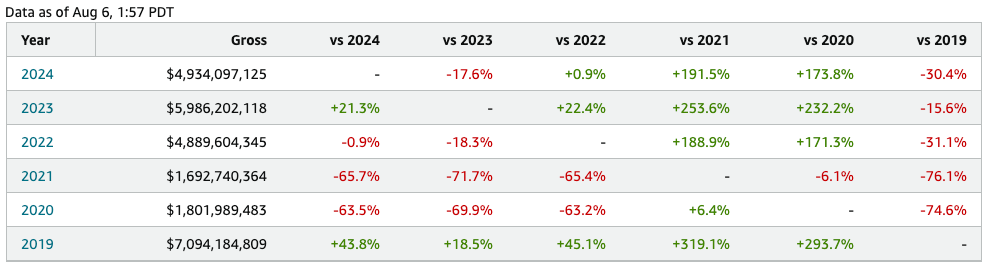

And “dump” is the right word. Here’s AMC’s summary results — which basically speak volumes:

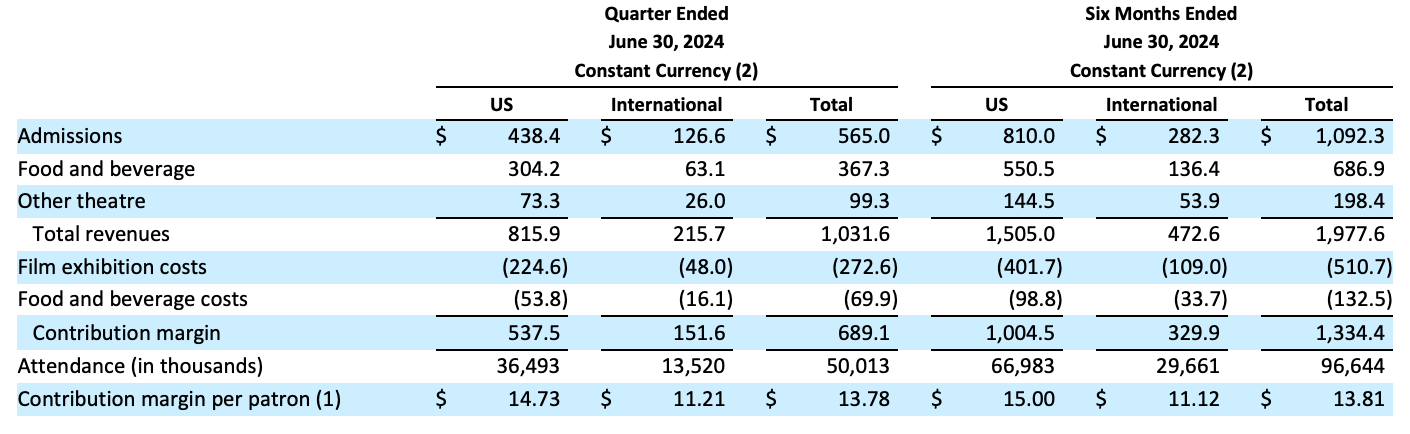

One result left out of the summary? Attendance in the US for the quarter and the six months ended June 30, 2024, were at depressed levels:

How depressed? Well, the company had 50mm total attendees in Q2’24 and 96.6mm attendees in 1H’24. In Q2’23, the company had 66mm total attendees and 114mm attendees in 1H’23.

You can see how that is problematic.

But Mr. Aron is, as we’ve said previously, quite the spider, and he spun like only Mr. Aron can. Read: exceedingly well.

“As expected, the second quarter started slowly with the box office adversely impacted by the 2023 Hollywood writers and actors strikes. However, the quarter finished with incredible strength powered by the success of Disney’s INSIDE OUT 2, which is now the highest grossing animated movie of all time. AMC saw a remarkable contrast between the early quarter with a dearth of movie releases and the end of the quarter with a record setting movie delighting audiences in our theatres. That difference between AMC’s early quarter performance and our late quarter performance was as if we were two totally different companies, surrounded by two completely different industry dynamics. Indeed, in June of 2024, AMC achieved our highest-ever June Adjusted EBITDA in our company’s entire 104-year history.” (emphasis added)

That “however” left skid marks it was such a rapid pivot.

But, sigh, as much as we hate to admit it, it’s understandable. The Q2’24 results don’t take into account the releases of Despicable Me 4 ($752mm worldwide, $314mm domestic), Twisters ($275mm worldwide, $196mm domestic) and Deadpool & Wolverine ($824mm worldwide, $396mm domestic), all of which are bona fide hits that have drawn moviegoers to theatres. To Mr. Aron’s point, INSIDE OUT 2 was just the start and Q3’24 is setting up rather well — even though the slate for August and September looks so weak that The Matrix is getting a re-release.

On the earnings call, an absolute “giddy” Mr. Aron was nothing short of “ecstatic”:

“You might think that, someone reporting an 84% drop in adjusted EBITDA this quarter compared to the same quarter last year might be in a foul mood. But to the contrary, as I sit here today and look at what has transpired so far this year and especially over the past seven weeks, I am ecstatic.”

“Pick any attitude you want. Ecstatic, euphoric, all those giddy and AMC's prospects for near term and medium term improvement and recovery. In fact, I'm now more confident that I've been in more than four years about how well AMC will perform over the next 6 to 30 months.”

Like we said: spinster. Why is Mr. Aron ecstatic? Well isn’t it obvious at this point?

“Just last week, we announced that, AMC completed several transformative capital market transactions that took up to $2.45 billion of our debt previously due in 2026 and extended the maturities to 2029 and 2030. This was an enormously complex effort, but one that will have profound positive impact on AMC.”

“The years 2029 and 2030 are a long way away. We have years and years of additional breathing room before them to further build, grow, and strengthen our company. For full disclosure and complete transparency, we did not move all of our debt that was due in 2025 or 2026 to 2029 and 2030, which remains that is still due in 2025 or 2026 in my view is de minimis compared to the previous amounts due and we believe it's thoroughly and entirely manageable.” (emphasis added)

A solid chest-pounding is incomplete without some good ol’ fashioned sh*t talking:

“I cannot even begin to count the number of nervous nellies, bloggers and journalists who are agonizing in the press about our looming debt repayment obligations just 20 months from now prior to this debt refinancing, and they were just over and over again … predicting our demise in '25 or '26 as a result of the debt payment that until last week was owed 21 months from now.”

Ouch, straight shot to our super fragile feelings. LOL, jk, surely you know by now that we here at PETITION don’t have feelings.

But wait. $2.45b? What? Where did that figure come from? Back to the press release:

AMC and its subsidiaries issued approximately $2.0 billion of new term loans due 2029 (“New Term Loans) in consideration for the open market purchase of approximately $1.9 billion of its existing Senior Secured Term Loans due 2026 (“Existing Term Loans”) and approximately $100 million of its 10%/12% Cash/PIK Toggle Second Lien Subordinated Secured Notes due 2026 (“Second Lien Notes”). The New Term Loans bear interest at the Term Secured Overnight Financing Rate (“Term SOFR”) plus between 600 and 700 basis points depending on leverage levels.

Callback to our previous coverage …

… wherein in the former we wrote:

Muvico and AMC jointly and severally issued $1.2b of new ‘29 term loans.[] These funds were used to address those near-term maturities; they were used for the “open market purchase of $1.1 billion” of the ‘26 term loans and exchanged for $104.2mm of the 10%/12% Cash/PIK Toggle second lien subordinated notes due in ‘26. If you’re looking at these figures and these issuances and wondering, “wait, wasn’t there $1.9b outstanding under the ‘26 term loan” and “wait, aren’t there other notes in the capital structure senior to the 10%/12% Cash/PIK Toggle second lien subordinated notes due in ‘26,” consider yourself an LME green belt. Not everyone is on board for this transaction, y’all.

And:

Notably, the transaction leaves open the possibility of additional future $800mm of open market purchases of the ‘26 term loan (read: the remainder) — an attempt to make LME deals a bit more user friendly?!? So this is violent, but a bit less “violent,” if you will?

In the latter we added:

The left-behind or “non-participating” holders of the original senior secured term loan due ‘26 … have seen their liens subordinated by a simple majority and are now weighing whether to join the new deal or hold out.

They joined! There remains only a stub piece of the term loan outstanding:

AMC and its subsidiaries are entitled to issue up to an additional $31 million of New Term Loans in order to purchase Existing Term Loans.

While it remains to be seen what the holders of the 7.5% first lien notes due ‘29 that were excluded from the transaction will do, Mr. Aron has a glidepath to the future laid out ahead of him. He’s bought himself a significant amount of amend-and-extend runway and now must hope that Hollywood starts cranking out content — for theatres not streaming! — now that the strike is a thing of the past. Notably, there’ve been 400 releases in ‘24 YTD. In ‘23, there were 590 at this point. Does this differential explain the delta in attendance levels? Does it explain the differential in YTD revenue?

Mr. Aron is betting we’ll find out soon enough with a larger slate scheduled in ‘25.

*Interestingly, the stock closed up 0.2% while the rest of the stock market imploded on Monday, August 5, 2024, with the Dow and S&P both down well over 2%.

**Though, to be fair, Mr. Aron had already foreshadowed results.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

Omg this is the best 🤣