💥Big Lots. Fisker. BUCA.💥

💥Big Lots. Fisker. BUCA.💥

Updates: Big Lots Inc. + Fisker, BUCA di Beppo files

💥Is Big Lots in BIG Trouble? Part V.💥

We covered Big Lots, Inc. ($BIG) disastrous Q1’24 results two months ago* …

… and the company is pushing on its twelfth straight quarter of comparable sales declines. The company’s stock price has reflected the atrocious performance:

And guess what? You ought not expect the revenue situation to improve any time soon: the company is seemingly set on putting the torch to its stores. Flame on!

Interestingly, BIG hasn’t been super aggressive with store closures; it only closed 137 stores between FY’21 and May 4, 2024 — a total that amounts to ~10% of the 1,431 stores open at the end of FY’21. On a net basis (inclusive of new openings), store count only decreased by 39 or ~2.7% of FY’21’s store count.

So, on July 31, 2024, management piqued our attention when they announced amendments to BIG’s revolver and term loan agreements, increasing the number of permitted store closures from 150 to 315. The original limit of 150 permitted store closings is a net number and, again, store count is only down 39 on a net basis from FY’21. Lawyers, get your strikethroughs ready ⬇️!

Not to mention counting would’ve, at the earliest, started on April 18, 2024 — the date of the first amendment — thus the actual net number of stores closed since then is … 0.** And in the Q1’24 report, management guided to 35-40 store closures and 3 store openings for ‘24.

So what’s going on? Has the plan changed? Is management preemptively amending this number in preparation of mass store closures? If so, and the company hits 150 store closures (the previous cap), that would represent ~11% of the current store count. If BIG closes 315 stores (the current cap), that would represent ~23% of the current store count.

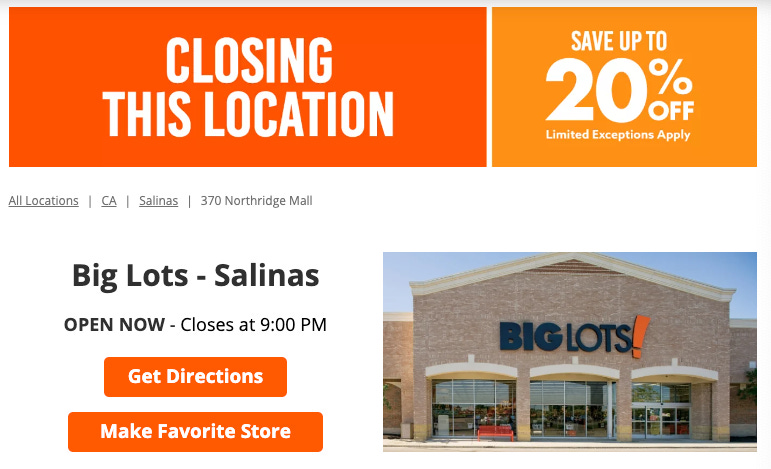

So, what’s the answer? If one were to browse through every single store on the company’s locations page, you’d find that ~300 locations are earmarked for closure. R.I.P. Salinas and others:

Here’s a shot surreptitiously taken at the last management meeting:

And that’s not all.

In exchange for raising the store closure cap, aggregate commitments under the revolver reduced from $900mm to $800mm, and the interest rate on the revolver increased by 50bps. Lenders want to get paid to de-risk! We love it.

We’re looking forward to some BIG fire sales both in the lead-up to bankruptcy and after.

*You can also refer to our previous other coverage here, here, here, and here.

**April 18, 2024 is also the date that the company entered into its $200mm commitment term loan with Gordon Brothers Capital, a firm generally known for liquidating sh*t stain retailers like this one.

⚡Update: Fisker Inc.⚡

The Fisker Inc. chapter 11 bankruptcy cases were recently dubbed “the most telegraphed Chapter 7 conversion in history.” But apparently parties have been able to postpone the inevitable.

As you’ll recall from our previous coverage …

… the debtors were able to get the $45.25mm American Lease LLC fleet sale approved at their July 16, 2024 hearing. So yay! There’s money coming in to actually fund these cases.

Unfortunately, Heights Capital Management (“Heights”) as prepetition secured lender remained undeterred; it still pushed for a chapter 7 conversion.

Heights believes that there’s no justifiable reason for these debtors to incur a hefty admin burn (read: professional fees) and argues that whatever needs to be done post-sale can be accomplished outside of chapter 11.

And on the other side of the ring is … literally everyone else. Opponents to Heights’ motion to convert include the debtors, the official committee of unsecured creditors (“UCC”), the National Highway Traffic Safety Administration (“NHTSA”), and even some equity holders.

All of this was supposed to culminate at a July 29, 2024 hearing (also the deadline date for cash collateral approval) but it turned out the debtors and Heights reached an agreement where the issue was put off once again for three weeks — to August 19, 2024 — via a fifth cash collateral motion. This cash collateral motion is a bit different from the rest: if parties can’t reach a resolution by the deadline, the debtors will support a chapter 7 conversion and file the corresponding motion to convert. One last chance guys, one last chance.

A resolution on what?

Well, like we mentioned last time:

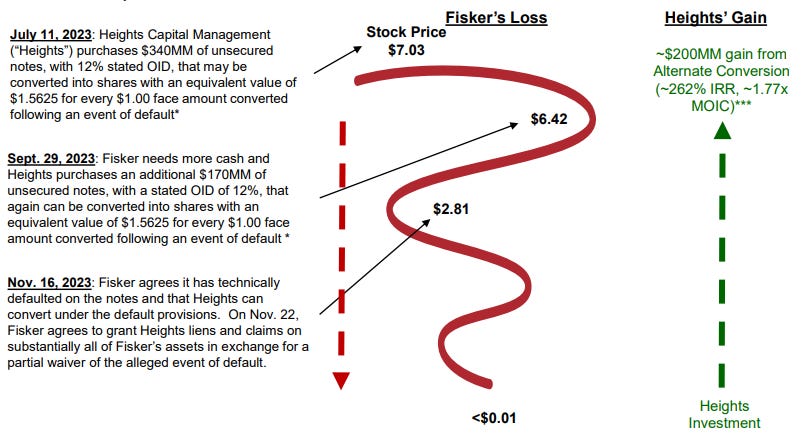

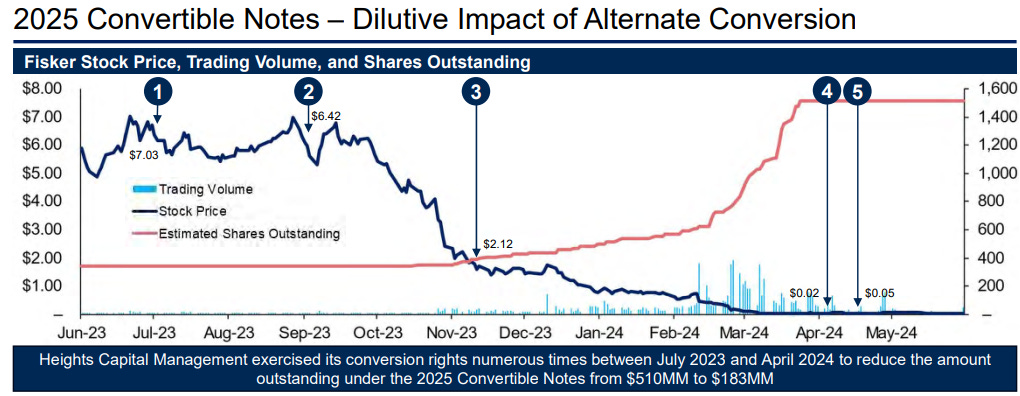

“Ohhh we don’t know … maybe … just MAYBE … it’s the contentious transaction that secured Heights’ previously unsecured indebtedness in November ‘23?”

The UCC brought the bombs. And by bombs we mean pretty PowerPoint slides:

According to the UCC, Heights pocketed $57mm in profits through its convertible notes and then used those same notes to upjump into secured lender status.

Parties didn’t get an opportunity to clash heads during the July 29 hearing so now we just wait to see if a settlement is reached regarding the secured/unsecured allocation of proceeds.

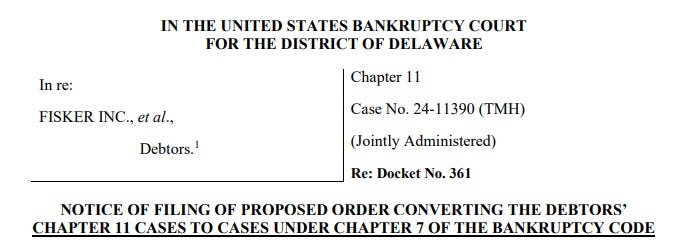

So far things look less than promising. The debtors were obligated to file the proposed order to convert by August 9, 2024 unless Heights said otherwise (aka a resolution was reached) and … voila! Here it is:

A hearing regarding the motion to convert is set for August 19, 2024 at 1pm ET.

💥New Chapter 11 Bankruptcy - BUCA Texas Restaurants LP💥

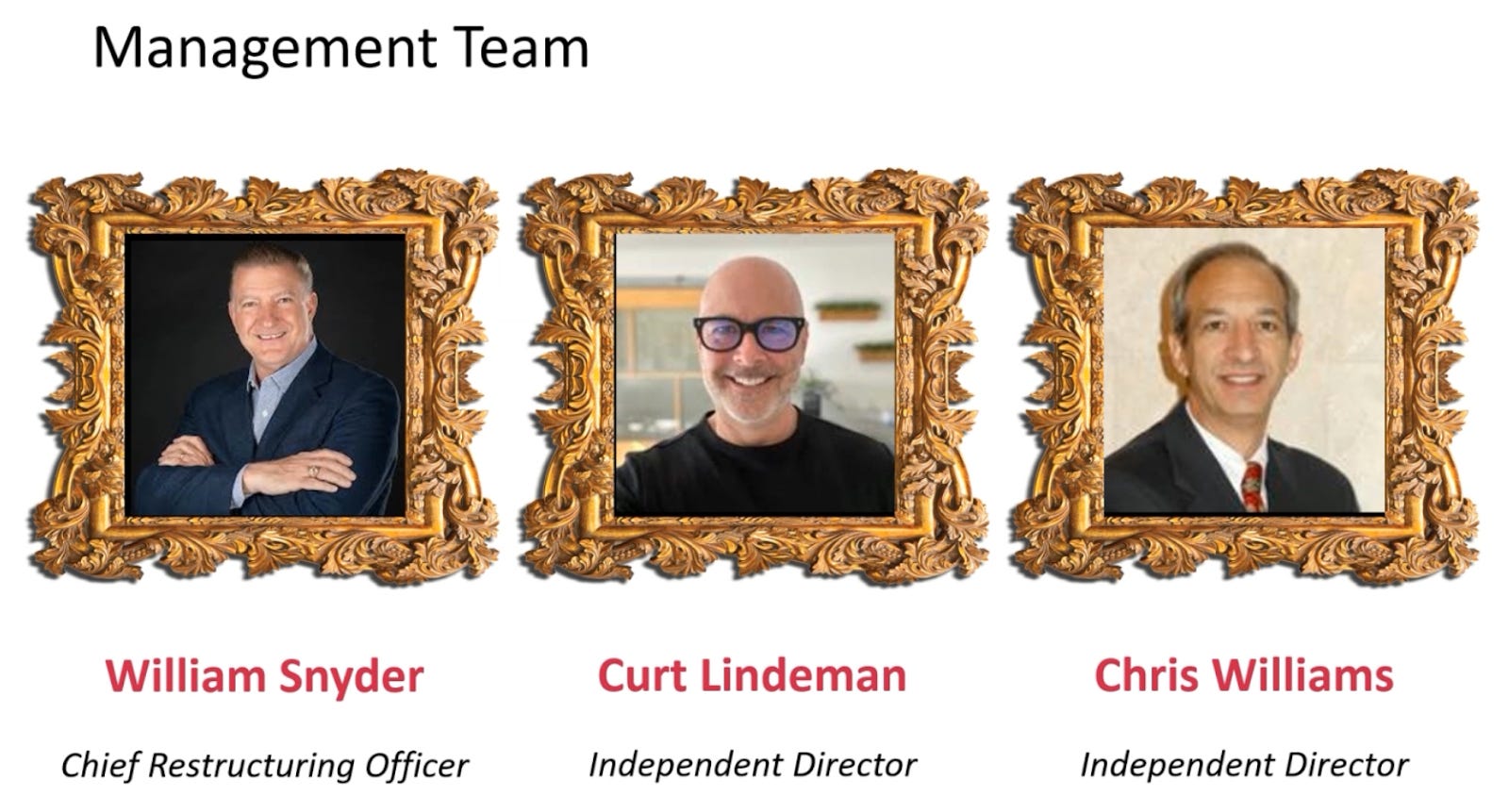

On Aug. 4, 2024, Dallas-based BUCA Texas Restaurants LP and nine affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the Northern District of Texas (Judge Jernigan). “Buca” means “hole” in Italian which is such low hanging fruit in this context that even we(!) feel reluctant to pick it; in actuality, the word references the debtors’ founding in a Minneapolis basement in ‘93.* The debtors are “celebrated” for their “family-style dining,” “unique dining experience and communal approach to meals,” which includes “generous portions, and vibrant atmosphere,” at least according to the first-day declaration of CR3 Partners LLC partner and CRO William Snyder, who clearly demonstrates zero hesitation to overstate his client’s case.

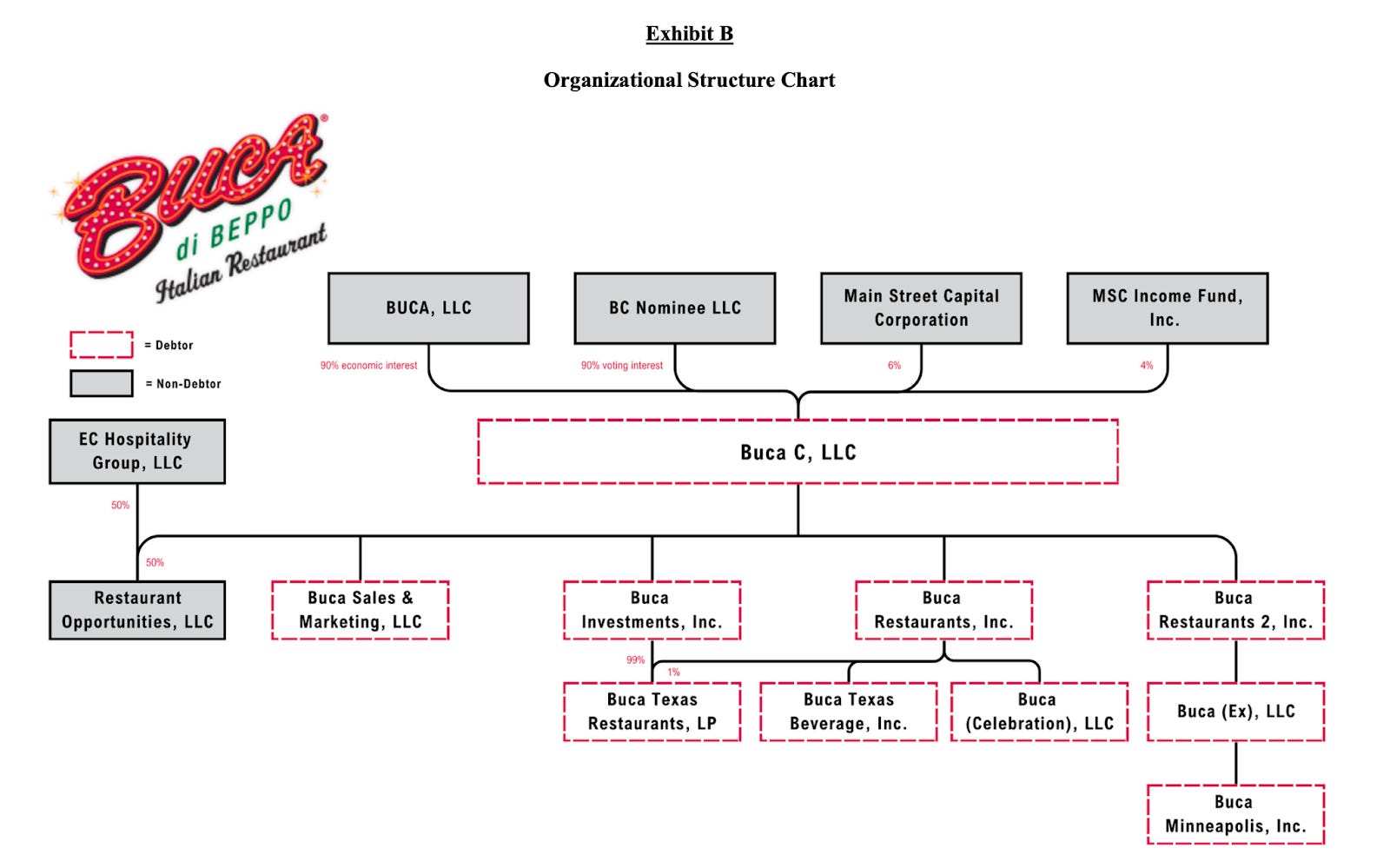

In ‘08, Planet Hollywood International Inc. n/k/a/ PB Restaurants, LLC (“Planet Hollywood”) acquired the debtors. In ‘15, the debtors entered into a $47mm term loan with Main Street Capital Corp. ($MAIN)(“Main Street”) as admin and collateral agent. Main Street is a Houston-based private debt and private equity firm that invests in lower and middle market private companies. “Neither BUCA Sales & Marketing, LLC nor BUCA (Celebration), LLC signed as Borrowers under the Term Loan or any amendments to the Term Loan. Similarly, neither of these entities signed the security agreement corresponding to the Term Loan and neither appear to be subject to Main Street’s security interests,” Synder states, somewhat ominously. Snyder also points out that in June ‘15, Buca LLC granted to Main Street “…for the ratable benefit of the Lenders, a continuing security interest in, and pledged and collaterally assigned to Main Stret (sic), all of Parent’s right, title, and interest in and to all of Parent’s membership interests in BUCA C.”

Before we proceed, the following visual aid may be of use. Note that non-debtor parent Buca LLC is “…owned and/or controlled, directly or indirectly, by an entity that also owns Planet Hollywood.”

All went well until, yes, 2020. Is it necessary to repeat the impact of the lockdowns on small businesses and restaurants? In December of that baleful year, the debtors received their first notice of default under the loan agreement from Main Street. Another followed in March ‘21. In April, the parties amended the loan: Main Street waived certain defaults, Planet Hollywood’s owner was obligated to make a subordinated loan to debtor entity Buca C (see above) in the amount of $3mm, the debtors were required to make certain prepayments of the term loan and use their “reasonably best efforts” to refi the debt or arrange a sale.

Something didn’t work out. Main Street sent two more default notices, one in Dec. ‘22, the next in May ‘23. The loan matured on June 30, 2023. The debtors seem to have skipped it. In July — inside the 30-day grace period, the maturity was extended by two months to August 31, 2023. Not enough. Two more default notices: one on January 23, 2024 and the other on April 9, 2024. And then another amendment: Main Street agreed to extend a protective advance not to exceed $150k for the sole purpose of paying debtor financial advisor CR3.

Not long after, Main Street realized it was hopeless. Per Snyder:

Due to the asserted multiple ongoing defaults under the Loan Agreement, on July 3, 2024, Main Street exercised its asserted default-related rights and remedies to (a) have all of Parent’s BUCA C Membership Interests registered in the name of its nominee, BC Nominee, LLC, (b) exercise the voting power to act in respect of the BUCA C Membership Interests, and (c) have BC Nominee, LLC admitted as an equity owner and substituted for the Parent as a member of BUCA C. Subsequently, BC Nominee, LLC assigned the economic interests of BUCA C back to Parent. The effect of these transactions was that Parent holds only an economic interest in BUCA C as of the Petition Date, but is no longer a member of BUCA C and no longer has voting or consent rights or the right to participate in the management of BUCA C.

To make it clear they weren’t f*cking around, BC Nominee then sacked the managers of BUCA C and appointed Curt Lindemann and Christopher Williams as managers. They promptly fired all officers and directors at each of the debtors, and added CRO Snyder. Main Street then provided a $2mm protective advance “...to permit the Debtors to continue operating during the transition period away from the Parent and assess restructuring options.” This was supplemented with another proactive advance, this one of $2.9m, on July 24, 2024.

⚡️By the way, if you’re getting Red Lobster vibes from all of this …

… well, yes, this is very similar in the way that the senior lender took control of the situation at hand.⚡️

Anyway, all told, the debtors owe Main Street $38.9mm, and so here they are. “The Debtors plan to use these chapter 11 cases to shed or renegotiate unfavorable leases, institute operational efficiencies, and complete a value-maximizing sale for the benefit of all stakeholders,” Snyder states. Here are the rejected leases, attached to the proposed order (docket 38).

The debtors seek to fund the cases with a $36.3mm DIP provided by … yes, Main Street. 🦞

The DIP includes $12.1mm of new money and a $24.2mm roll-up, including the $5.05mm in protective advances. The $5.05mm of prepetition obligations (fees and principal) will be rolled into DIP loans on an interim basis, and $19.15mm on a final basis. The facility bears an interest rate of 15%. Most intriguing: the super-expedited sale process, “Specifically, the proposed DIP financing agreement and interim order, if approved, will require the Debtors to file a bidding procedures motion within 8 days of the Petition Date. The proposed DIP financing agreement and interim and final orders also contemplate the Debtors seeking approval of a sale transaction within 75 days of the Petition Date.” The speed is necessary to preserve cash and expedite recoveries, Synder said.

The first-day hearing held on August 7, 2024 in the Dallas chambers of Judge Jernigan, commenced in a … well, vibrant and family-like atmosphere, just as the debtors are advertised. Parties shared their favorite Buca memories. Her Honor praised decorative elements in debtor attorney Gray Reed’s presentation, which attorney Amber Carson said were sourced from Buca. Like these:

Hmm. Those frames (not Lindeman’s) look more French than Italian to us. But Her Honor liked the Art, especially this one of a nun in a bumper car:

We reckon that, early in the hearing, parties may have been longing for a quick adjournment to, uh, perhaps gather at the Buca de Beppo in Dallas and contemplate the art in situ? 15 minutes from chambers in normal traffic, but anywhere from one to three hours once that Dallas-Fort Worth lunchtime traffic kicks in. Docket 10 came before the court. Wages and salaries: what could go wrong? Pretty mundane and customary sh*t, right? No one’s going to screw the workin’ man (or at least not this obviously.) At which juncture Michael Mervis of Proskauer Rose LLP, representing Planet Hollywood, asked if he might say a few words.

Mr Mervis, we note, is the vice-chair of Proskauer’s litigation department; he has represented Britney Spears, and went to college in Maine, which is about as far from Texas as is imaginable, especially in August. He began somewhat apologetically, admitting to a “choreography faux pas” with his iPad, as a result of which he did not signal an interest in making opening comments. He assured the Court that the last thing he wanted to do was break the “debtor’s flow,” and he’d be happy to take direction from Her Honor and save it till later. But look. There are these certain … issues relevant to the whole idea of employment and ownership, so the wages motion, good a time as any, he figured.

Proceed, Judge Jernigan said. And proceed Mr Mervis certainly did.

“July 3 of this year was a very consequential day for Buca from our client's perspective,” Mervis said, in a masterpiece of understatement. Planet Hollywood and the debtors had been in the midst of a “workout negotiation,” or at least, that’s what he thought up until July 3, 2024, when toward the evening of that remarkable day, Main Street swept in and seized control of the debtors. “Now that in itself is not necessarily impermissible, but it has consequences, and those consequences from what our clients can see have not been appropriately addressed and are not being addressed, and that's what I want to talk to you about,” he said. Because, you see, stripping Planet Hollywood of control and ownership, he followed, has led to “potential problems.”

What kind of problems? Possible disassociation with some employee programs! And issues with booze!! What’s a nice vibrant, family-style meal without freely flowing booze? But there’s this thing called a liquor license, and … hey, we’re hearing the Bucas are still selling booze, and maybe they should not be, 🤷♀️? At which point Mervis drew his rapier:

We have concerns about whether these debtors are in compliance with all the things that they need to be in compliance with as a result of what Main Street did on July 3rd. We are also frankly concerned about the debtors’ estates and preserving value.”

Planet Hollywood shared these concerns with the debtors and their advisors several weeks ago, Mervis said. Crickets from the debtors, leaving Planet Hollywood in a state of consternation. They’d very much like to negotiate an amicable divorce and they’re a bit concerned that the whole case will now languish in an adversarial posture with Main Street. Mr. Mervis doesn’t seem to accept that Main Street has moved on without his client, though he raises some interesting concerns about liquor licenses and the like.

“It would be great if this case didn't get mired in litigation,” Mervis said, and even greater if Planet Hollywood, the debtors, and Main Street could all “…agree that the concerns that we've raised have been adequately addressed.” But hold on. Isn’t a company derived from Hollywood supposed to bring the drama? Color us confused about all of this “let’s agree” prattle.

Porter Hedges LLP’s Joshua Wolfsholl, Main Street’s attorney, answered along the lines of “yeah, a group hug sounds amazing but Main Street does not control the debtors, independent parties control the debtors” but the“...expectation is that the parties are going to work collaboratively….” The earlier positive mood ostensibly recaptured, and there being no objections, Her Honor approved the wages motion. Next up was the DIP, approved after testimony from Snyder.

Judge Jernigan approved all submitted motions on an interim basis, with the cash management motion to be considered at the second day hearing on August 29, 2024, along with the final DIP motion.

The all-important bidding procedures motion hit the docket on August 12, 2024 and — ⚡️SHOCKER⚡️ — Main Street is the stalking horse purchaser.** Like we said, Red Lobster vibes. The debtors filed an emergency motion to have the bidding procedures motion heard on expedited notice on August 19, 2024.

Selfishly, we hope Mr. Mervis is back to keep things interesting.

In addition to CR3 Partners as financial advisor, the debtors are represented by Gray Reed & McGraw LLP (Amber Carson, Jason S. Brookner, Micheal W. Bishop, Emily F. Shanks) as legal counsel and Stout Risius Ross LLC (Michael Krakovsky, Luis Pilich, Andrew Masotta) as investment banker.

*Other famous — but not quite as famous as BUCA — companies that started in basements include Amazon Inc., Melissa & Doug, Epic Games, and others. 😜

**Main Street didn’t require any bid protections.

📸Caption Contest📸

Johnny was visiting family and he came across … well … this ⬇️. We figured our audience might be able to come up with a good caption for it given the wave of recent pain in retail:

Email us at petition@petition11.com. The winner, if any,* will get a shoutout to our audience or maybe even a mini Notice of Appearance segment.

*If all submissions suck we’ll just ignore them, lol.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

I’m not in restructuring but your posts all bring the lols guys keep it up

Great article as usual. What ever happened to MGBW furniture bankruptcy?