💥New Chapter 11 Bankruptcy + CCAA - Accuride Corporation💥

Commercial wheel manufacturer gets nailed by COVID, seeks in-court sale or ownership transfer to term lenders.

Everything old is new again. Gen X darling Pearl Jam (“PJ”) is out on the road touring and Coldplay is out with a new album — one that its lead singer Chris Martin says will be the band’s last and we’ve never prayed …

… for a statement to be more accurate.

Of the two bands, our very own Johnny Dumas prefers PJ and he recommends PJ’s cover “Last Kiss” as your background music for this reading.

Why? It is about a fatal car accident and nothing screams car crash like Crestview Partners-owned wheel manufacturer and supplier Accuride Corporation …

… which is back in bankruptcy almost fifteen years to the day after previously visiting our cute little industry.* On October 9, 2024, it and 15 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Stickles).** Between this sucker and Wheel Pros, the smell of burnt rubber (and cash) is infesting bankruptcy courts these days.

Why is yet another auto supplier — in this case, to the medium and heavy-duty commercial truck and trailer markets — in bankruptcy? Anyone want to pause and take a guess before reading on?

Well …

… if you guessed COVID-19, give yourself a pat on the back. The long arm of the pandemic reaches out to claim another victim! Per the first day declaration of CRO Chuck Moore of Alvarez & Marsal LLC (“A&M”):

The Debtors have faced significant headwinds from the lingering effects of the COVID-19 pandemic on the Debtors’ business, operational difficulties, business integration challenges, inflation, supply chain disruption, and other geopolitical and macroeconomic forces that depressed revenue and increased costs. The COVID-19 pandemic left the Debtors reeling, with the sudden seizure of commercial transportation (other than essential goods and services) driving softness in the commercial vehicle market compounded by long-term elevation in labor and materials costs. During and after the pandemic, operational and business integration challenges at certain non-Debtor affiliates required capital support from the Debtors.

Absolutely nothing new here folks. Nor anything original about this either:***

Then, as inflation swelled beginning in 2021, the Federal Reserve reacted by raising interest rates to the highest level seen in decades. This sea change in the global macroeconomic environment contributed to a major decrease in demand for imports and finished manufactured goods; this caused a resulting depression in the freight industry and knock-on effects on freight vehicle manufacturing, which comprises an irreplaceable portion of the Debtors’ customer base. On top of these challenges, Russia’s invasion of Ukraine, and the resultant sanctions regimes against the Russian Federation, left the Debtors unable to access cash at their non-Debtor Russian affiliate—a business that was otherwise an operational bright spot.

It was time to break out the playbook.

The debtors kickstarted an operational restructuring to reduce costs and extend liquidity runway. That’s code for f*cking over vendors. The debtors also started divesting assets. No doubt Mr. Moore was turning over a couch cushion for spare change. Alas, it didn’t matter. By summer ‘24, the debtors had to engage an ad hoc group of consenting first lien lenders and consider strategic alternatives, including a pre-petition sale and marketing process. Enter Perella Weinberg Partners ($PWP)(“PWP”). Given that this sucker is now in bankruptcy, it’s clear that none of the interest was robust enough to make the term lenders happy. Or, as the debtors put it, “…the existing bids have not generated sufficient value to present an attractive opportunity to transact.” Word salad, anyone?

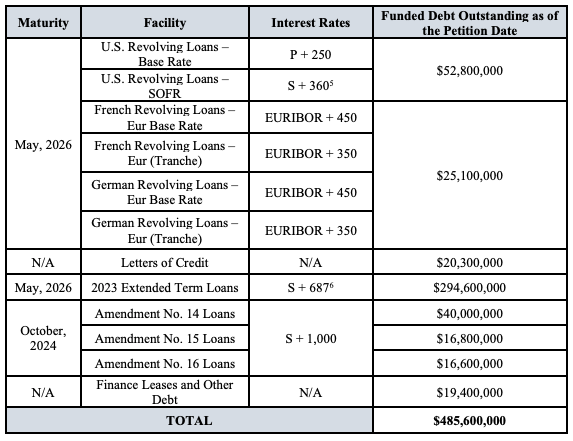

Let’s talk about that debt. The debtors’ capital structure looks like this:

What you see there, at least with Amendments 14-16, is an awful lot of pre-DIP DIP or “bridge financing” tacked on to the original term loans. Which also explains the proposed DIP in these cases: it is a $103mm headline number but that is comprised of only $30mm of new money and the roll-up of $73mm (which comports with the bridge financing amounts). The amount of cash infused into this business pre-filing suggests another reason for the filing: the ad hoc group of consenting term lenders were sick of shoveling money into this thing without the protections afforded to financings under chapter 11 (read: section 364 super-priority status). The debtors seek the complete roll-up on an interim basis along with $20mm of the new money. Fees include a 5% PIK upfront fee, a 2% exit fee, and certain backstop fees to Jefferies Capital Services LLC, as fronting lender.

Indeed! The DIP also contained an interesting 10% “sale premium” feature in the event that the debtors sell all of their assets (or equity). The premium would apply to both the new money and roll-up amounts so we’re talking roughly $10mm for doing … looks 👉, looks 👈 … not entirely sure, frankly, 🤷♀️. We’ll come back to this seeming-backdoor-breakup-fee in a hot sec.

So, now that this thing is in bankruptcy and we know there’s new money coming in, what are the debtors hoping to achieve while in chapter?

Well, speaking of playbooks, middle market specialist Kirkland & Ellis LLP (“Kirkland”) is company counsel here.**** And so, in typical Kirkland fashion, we have a restructuring support agreement (“RSA”). The RSA contemplates (i) the ABL revolving facility remaining in place (and riding through the cases)***** and (ii) an equitization of the term loan subject to a sale toggle should any potential buyer come forward offering “…sufficient value to present an attractive opportunity to transact.” In addition to agreeing to the equitization, the consenting term loan lenders have agreed to a $128mm takeback DIP-to-exit loan ($112mm) which would include $15mm of new money (distributed pursuant to a debt rights offering)(the backstopping DIP lenders also get an equity kicker such that, in the end, they’ll end up with more equity than term lenders who weren’t part of the ad hoc group).

What about general unsecured creditors? Well, here comes their recovery:

With one catch. The critical vendor motion here is pretty robust; it consists of ~$12mm to be paid on an interim basis and another ~$8mm on a final basis. In other words, its 67% of the new money DIP.

What’s in line for Crestview’s equity? C’mon now, that’s a trick question fools! Clearly with GUCs getting a big fat 🍩, Crestview stands to as well.

The DIP requires a confirmed plan of reorganization memorializing the terms of the RSA within 95 days of the petition date.

At a first day hearing held on October 11, 2024, the debtors obtained their requested relief. They did not, however, get approval of that funky sale premium. Indeed, prior to the hearing, the debtors submitted a revised order indicating the following:

Notwithstanding anything to the contrary in the Motion, this Interim Order or the DIP Documents, the Exit Fee (as defined in the DIP Credit Agreement) and the Sale Premium (as defined in the DIP Credit Agreement) are not being approved pursuant to this Interim Order and shall only be approved in accordance with a Final Order granting such relief.

We reckon an official committee of unsecured creditors (“UCC”) may have something to say about it. After all, the UCC isn’t going to have much to work with under this case construct.

As noted, the debtors are represented by Kirkland as legal counsel (Ryan Blaine Bennett, Alexander McCammon, Derek Hunter) along with Young Conaway Stargatt & Taylor LLP (Joseph Barry, Kenneth Enos, Jared Kochenash, Andrew Mark) as local counsel (a pairing you don’t see everyday). A&M is financial advisor and providing the debtors’ their CRO (the aforementioned Mr. Moore) while PWP (Alexander Svoyskiy) is investment banker. The ad hoc group of term lenders is represented by Weil Gotshal & Manges LLP (Matthew Barr, David Griffiths, F. Gavin Andrews) and Richards Layton & Finger PA (Zachary Shapiro) as legal counsel — which just goes to show that Eaton Vance isn’t in every single credit on planet earth and Gibson Dunn & Crutcher LLP doesn’t have 100% market share of ad hoc groups, just 99.9%, 😜. There’s a special committee of the board involved here too, featuring frequent independent director Steven Panagos (formerly of Moelis) and Ted Stenger (formerly of AlixPartners LLP … welcome to the party pal); they’re investigating … stuff (while advised by counsel selected from “a slate of law firms acceptable to the Consenting Term Loan Lenders” … something that must have those firms who frequently get BoD referrals from Kirkland a little nervous). Crestview Partners is represented by Paul Weiss Rifkind Wharton & Garrison LLP (Paul Basta, Jacob Adlerstein, Xu Pang) and Klehr Harrison Harvey Branzburg LLP (Domenic Pacitti, Sally Veghte)

*It previously filed for bankruptcy on October 8, 2009, also in the District of Delaware (Judge Shannon).

**There’s also a CCAA here for a Canadian affiliate.

***This bit, however, was different and interesting and has a bit of a political undercurrent to it:

On June 20, 2024, one of the Debtors’ competitors, Webb Wheel Products, Inc. (“Webb”), filed petitions against the imports of certain brake drums from the People’s Republic of China and the Republic of Türkiye alleging that brake drums from these countries were being sold in the United States at less than full value. The net impact of these petitions on the Debtors’ business remains to be seen. Debtor KIC, LLC, purchases brake drums from certain Chinese manufacturing partners. Antidumping and countervailing duties, if imposed, would significantly increase the cost of Wheel Ends’ imported products. At the same time, Debtor Gunite, LLC may face increased demand for its domestic production capacity for wheel end products. The uncertainty resulting from the outstanding petitions filed by Webb appear to have contributed to discouraging potential acquirers of Wheel Ends from transacting at a price that would be profitable for the Debtors (net of projected wind-down and exit costs).

****We’re not poking fun at Kirkland here; rather, we’re indirectly providing commentary about where the supermajority of chapter 11 bankruptcy deals are these days. The dearth of volume necessitates a “drop down” of the likes of Kirkland (and A&M) to keep bodies busy and mouths fed. There are a lot of high-priced firms involved here for a capital structure of this size, that’s an objective fact.

*****Notably, the ABL lenders took some paydown from the bridge financing to de-risk exposure.

Company Professionals:

Legal: Kirkland & Ellis LLP (Ryan Blaine Bennett, Alexander McCammon, Derek Hunter, Kyle Trevett, Mason Zurek, McClain Thompson, Rebecca Ritchie) and Young Conaway Stargatt & Taylor LLP (Joseph Barry, Kenneth Enos, Jared Kochenash, Andrew Mark)

Special Counsel: Quinn Emanuel Urquhart & Sullivan LLP (Victor Noskov, Susheel Kirpalani, Philip Lockwood-Bean, Kenneth Hershey, Kate Scherling, Derek Hunter, Daniel Holzman)

Board of Directors: Jason Luo, Thomas Murphy Jr., Alexander Rose, Bradford Williams, Robin Kendrick, Steven Panagos, Edward Stenger

Financial Advisor/CRO: Alvarez & Marsal LLC (Charles Moore)

Investment Banker: Perella Weinberg Partners LP (Alexander Svoyskiy, Douglas McGovern, Anthony Schwartz, Ry Sanderson, Sam Bagley, Zach LaPasso, Richard Jove, Sam Koby, Bridget Mahoney, Ethan Lee)

Claims Agent: Omni (Click here for free docket access)

Other Parties in Interest:

Prepetition ABL Agent: Bank of America NA

Legal: Davis Polk & Wardwell LLP (Eli Vonnegut, Stephanie Massman) and Morris Nichols Arsht & Tunnell LLP (Robert Dehney, Tamara Mann, Austin Park, Erin Williamson)

Prepetition Term Loan Agent & DIP Agent: Alter Domus US LLP

Ad Hoc Group of Term Loan Lenders

Legal: Weil Gotshal & Manges LLP (Matthew Barr, David Griffiths, F. Gavin Andrews) and Richards Layton & Finger PA (Zachary Shapiro)

Sponsor: Crestview Partners

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Paul Basta, Jacob Adlerstein, Xu Pang) and Klehr Harrison Harvey Branzburg LLP (Domenic Pacitti, Sally Veghte)

Official Committee of Unsecured Creditors

Legal: Morrison & Foerster LLP (Lorenzo Marinuzzi, Doug Mannal, Oksana Lashko, Raff Ferraioli, Miranda Russell, Joseph Murphy, Jennifer Marines, Ilayna Guevrekian, Theresa Foudy, Benjamin Butterfield, Chane Buck) and Morris James LLP (Eric Monzo, Brya Keilson, Siena Cerra)

Financial Advisor: AlixPartners LLP (David MacGreevey)