💥Vyaire Gets a Breathing Spell💥

💥Vyaire Gets a Breathing Spell💥

Plus: Rubio's gets its first day relief + an Enviva Update

Not so much.

On June 9, 2024, Illinois-based Vyaire Medical Inc. (“Vyaire”) and 27 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Shannon) — a little over (i) six months after that ⬆️ ill-fated Insta post, (ii) six years after sponsor Apax Partners (“Apax”) acquired the entirety/remainder* of the debtors’ business from Becton Dickinson & Co. (“BD”) in a (leveraged) deal worth approximately $435mm, and (iii) one year after lenders organized with Gibson Dunn & Crutcher LLP to agitate for negotiations over the debtors’ unwieldy balance sheet ⬇️.**

A balance sheet that is, uh, a direct result of the Apax/BD transaction. Gotta hate when that happens!

Vyaire is a global company with two primary business segments:*** (i) ventilation, which focuses on helping patients in hospitals, health centers and private-practice facilities breathe (“Ventilation”); and (ii) respiratory diagnostics, which develops, manufactures and commercializes devices used to diagnose pulmonary and cardio pulmonary diseases (“Respiratory Diagnostics”). Your nana’s breathing powered by private equity!

We won’t delve into the details but suffice it to say, the businesses have had their ups and downs in the pandemic and post-pandemic worlds. Per the debtors, “[t]he post-COVID-19 drop-off in demand for the Ventilation business, a difficult pivot in the [c]ompany’s go-to market strategy, and unsustainable overhead costs led to a downward spiral of liquidity” and, ultimately, “[t]he [c]ompany’s operational challenges and Ventilation’s negative cash flow have proved difficult to overcome.” Wait. Isn’t the whole private equity value proposition that they know how to streamline and operate businesses to full optimization? LOL.

As the business continued to decline, a PJT Partners LP-attempt to save the day with an amend and extend of the debtors’ first lien debt — the ⬆️ above-noted $339.3mm 1L term loan + $78.6mm in first lien notes — ground to a halt and by April ‘24 the debtors were in full on scramble mode. Apax be like …

…and all of a sudden disinterested directors started multiplying like flies on sh*t … the sh*t here, obviously, being Vyaire’s disintegrating Ventilation business.**** The debtors pivoted to negotiating a DIP and simultaneously launched a pre-petition sale and marketing process of the business in parts or as a whole — a process that, as of the petition date, has allegedly yielded several expressions of interest but no formal stalking horse purchaser.

A chapter 11 bankruptcy sale process without a stalking horse?! How original, guys!!

There is, however, a restructuring support agreement (“RSA”). More originality!! The RSA outlined the terms of the proposed DIP credit facility (and use of cash collateral) — much needed given the debtors’ very limited $1.7mm of cash on hand as of the petition date — backstopped by an Ad Hoc 1L Group (Gibson loves its groups as much as we love our exclamation points!). It has the support of lenders holding over 90% of the first lien term loan, lenders holding 100% of the second lien term loan, and Apax.

So what of the DIP? Per usual, it’s the machine breathing life into this zombie (see what we did there?). There are aggressive milestones, of course: a July 24, 2024 auction date; a July 29, 2024 sale hearing; and an August 19, 2024 sale consummation deadline. The Ad Hoc 1L Group isn’t f*cking around. Per the debtors:

“Conducting a thorough marketing and bidding process and consummating a Sale Transaction(s) on the timeline contemplated herein is vitally important to the Debtors’ efforts to maximize value. Such Sale Transaction(s) would benefit not only the Debtors, but their vendors, dedicated employees, lenders, and other key stakeholders as well.”

A bid procedures motion is already on file because, you know, debtors love just giving away bid protections these days. It used to be that stalking horse purchasers negotiated bid protections as a necessary requirement to putting in the work. Now so many cases file without a stalking horse in the first place that the debtors have to preload the breakup fee just to entice motherf*ckers to come out of the woodwork. “Take our money please!” We reckon an established industry standard of 3% helps tee that up.

Alas, that’s where we’re at here. The debtors propose a break-up fee of 3% of the total cash consideration (inclusive of an expense reimbursement) subject to certain disqualifying events such as, among other things, a credit bid. The debtors seek a $140mm minimum bid or they’re going to cancel the sh*t out of this proposed auction. Interestingly, the debtors have filed a motion seeking to keep certain potential interested parties in the debtors’ assets under seal — as opposed to list them in connection with conflicts checks run by the various proposed debtor professionals. We can’t wait to see what the Delaware UST has to say about that given the good stuff that’s been happening in other cases such as Invitae Corp. and Enviva Inc. (see below) … yeah, yeah, different jurisdiction blah blah blah. Still, disclosure! Transparency! More exclamation points!!

As for the actual DIP terms, there’s a new money portion and a roll-up portion because, like, this is the least original case of all time. It’s all provided and backstopped by the Ad Hoc 1L Group. The breakdown is $45mm of new money ($25mm interim) and a $135mm roll-up of 1L term loans into the DIP ($75mm interim, 3:1 rollup of prepetition secured 1L term loans relative to $45mm of new money). The Ad Hoc 1L Group required this roll-up, of course, or, they say, they’re ✌️. They get liens on unencumbered assets and priming liens, OF COURSE. And for their trouble the Ad Hoc 1L Group also gets…

…plus a 2% commitment fee ($900k), a 5% backstop fee ($2.25mm)(!), and a 1.25% exit fee ($562.5k).

After the sale(s) are consummated, the intent of the parties is to wind down whatever remains.

The debtors are represented by Kirkland & Ellis LLP (Joshua Sussberg, Spencer Winters, Yusuf Salloum, Christopher Ceresa, Tiffani Chanroo, Mark McKane, Tabitha De Paulo, Joseph D’Antonio) and Cole Schotz PC (Patrick Reilley, Michael Sirota, Warren Usatine) as legal counsel, AlixPartners LLC (Charles Braley) as financial advisor and PJT as investment banker (Michael Schlappig, Jaimie Baird, Dylan Friesner). As noted previously, Gibson Dunn & Crutcher LLP (Scott Greenberg, Jason Zachary Goldstein, Joshua Brody, Kevin Liang) represents the Ad Hoc 1L Group with co-counsel, Pachulski Stang Ziehl & Jones LLP (Laura Davis Jones, Timothy Cairns). Rothschild & Co. is their financial advisor. Apax is represented by Simpson Thacher & Bartlett LLP (Elisha Graff, Ashley Gherlone). Finally, Bank of America NA as 1L Admin Agent is represented by Haynes and Boone LLP (Eli Columbus, J. Frasher Murphy, Matt Ferris) and Ashby & Geddes PA (Michael DeBaecke) as legal counsel and RPA Advisors LLC as financial advisor.

A first day hearing will be held later today, June 11, 2024, at 10:30am ET.

*Apax acquired a majority stake in the business in Q4’16 and bought the remaining stake from Becton in Q2‘18.

**Rothschild & Co. came on board shortly thereafter.

***It had a third segment, a consumables business, that it divested in May ‘23 to SunMed Group Holdings LLC (d/b/a AirLife) for $310mm — $133.9mm net after pay down of a then-outstanding and now-terminated RCF — in an effort to shore up cash. Clearly this didn’t do the trick! SunMed has counsel that has made a notice of appearance — Goodwin Procter LLP (Kizzy Jarashow, Alexander Nicas, Liza Burton, Amanda Schaefer) and Potter Anderson & Corroon LLP (L. Katherine Good, Aaron Stulman), 🤔.

****Insert Paul Aronzon, Ron Labrum, Bret Wise and David Barse. What? No women disinterested directors wanted to touch this 💩? In comparison, for what it’s worth, the Respiratory Diagnostics business seemed to be holding up.

⚡️Update: Enviva Inc⚡️

The Enviva Inc. chapter 11 bankruptcy cases are the gift that just keeps on giving.

After Judge Kaplan approved Kirkland & Ellis LLP’s retention application over a conflicts/disinterestedness objection by White & Case LLP in the District of New Jersey in the Invitae Corp. cases, which we wrote about here…

… we then went on and covered Eastern District of Virginia Judge Kenney’s rejection of Vinson & Elkins LLP’s retention application in the Enviva cases here:

In short, since the onset of these cases, the US Trustee has been on the warpath; it objected to V&E’s employment application due to V&E’s relationship with Riverstone Holdings LLC (“Riverstone”), a major player in the case. See, Riverstone owns 43% of Enviva’s common stock and sought to be more than just a passive shareholder on the verge of getting its equity wiped out. Judge Kenney saw problems with V&E negotiating against Riverstone given how Riverstone represented 1.4% of V&E’s ‘23 revenue. Conflict of interest! Not disinterested!! These are not phrases you hear very frequently in bankruptcy courts, lol. The fine folks at V&E had to check their ears.

And so V&E limped away from the ruling — surely vowing to never file in the Eastern District of Virginia as a long term measure — and pondering what to do as a near term move. Would they just walk away from potentially millions in fees or would they dig in, get in fighting stance, and start throwing some jabs? The industry waited with bated breath.

Jabs it is!

Shortly after the ruling, V&E filed a motion to reconsider the decision. This dog’s still got its bite!

Recall that in their original reply to the UST’s objection, V&E made mention about how unnecessary an ethical wall was:

“The record is clear: these representations do not impact V&E’s disinterestedness, nor do they require a wall of separateness.”

Well, V&E has since changed its tune. It didn’t mean to suggest that a wall was impossible, LOL, just unnecessary, LOLOL. Whoops! Should’ve been clearer!! V&E argues:

“The Debtors respectfully submit that a wall is not impossible. There are only a limited number of lawyers who recently worked for both clients,[] and V&E can effectively erect a wall—without harm to either client—to ensure these lawyers do not work for both clients for the balance of these chapter 11 cases.[] Although V&E previously argued that a wall was unnecessary, V&E is willing to implement a wall, and a prospective wall[] would be vastly preferable to the Debtors as opposed to having V&E’s retention denied outright.”

The proposed ethical wall will split up V&E lawyers into two camps. “Team A” will consist of lawyers who have billed time to the debtors but not Riverstone (since the petition date) while “Team B” will consist of lawyers who have billed time to Riverstone but not the debtors (since the petition date). Team A will be prohibited from working Riverstone matters until the effective date of any confirmed plan while Team B will be prohibited from working for the debtors.*

And what of the 13 attorneys who have billed time to both the debtors and Riverstone? Any of those 13 attorneys who have billed less than 12.5 hours to Riverstone will be placed on Team A (debtors representation) while any attorney who have billed 12.5 or more hours to Riverstone will be placed on Team B (Riverstone representation).

How did V&E get to the 12.5 hours cutoff? It wasn’t just an arbitrary number. Per the declaration of V&E’s David Meyer:

“This cutoff is designed so that the two leading V&E finance attorneys for the Debtors would be able to continue their representation. If the number were to be lowered to ten hours, the Debtors would lose one attorney who has regularly represented the Debtors since September 2016.”

Of the 13 attorneys, this proposed ethical wall would place a grand total of two lawyers on Team B.**

V&E has gone from “an unethical wall is wholly unnecessary and a conflict doesn’t exist” to “an ethical wall is totally doable and we’ll do anything — okay not ‘anything,’ but kinda sorta stuff — to save our retention application.”

Man, the things that the EDVA does to law firms.

Too bad they’ll never get a chance to do things again after this debacle.

A hearing to consider V&E’s motion to reconsider is set for June 14 at 2:00pm ET.

*V&E lawyers who bill more than ten hours to the debtors in ‘24 will also agree not to participate in any net profits associated with Riverstone engagements in ‘24. Oh man. Someone please quantify what that could mean.

**Although to be fair, V&E’s top Riverstone billing lawyer comes in at a whopping 313.5 hours (Andrew Jackson) vs the second most at 13 hours.

🌮New Chapter 11 Bankruptcy - MRRC Hold Co. (Rubio's Coastal Grill)🌮

First Tijuana Flats Restaurants LLC and now this!? Ay dios mio!

On June 5, 2024, California-based MRRC Hold Co. (a/k/a Rubio’s Coastal Grill) and two affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Goldblatt). You may know the debtors from their delightful Fish Tacos, or the Mexican Street Corn Shrimp Two-Taco Plate, offered at one of their 86 leased locations in California, Arizona and Nevada:

Or, more likely, you may remember the debtors from their late ‘20 appearance in bankruptcy court: one of the 630 companies that filed during the “plague year.” We wrote about that previous filing here…

…and — ⚡️whoa boy⚡️— that prior coverage makes for an amusing read worth a revisit if we do say so ourselves.

Go ahead, take a second. We’ll wait.

We’ll wait because, as we wrote then, the debtors didn’t entirely remedy their balance sheet with that prior restructuring. Indeed, the debtors currently carry, in part as a remnant of the prior bankruptcy, nearly $73mm of funded secured debt on balance sheet. Golub Capital LLC (“Golub”) provided the $52mm of senior secured first-lien exit financing as reflected here at the time⬇️.

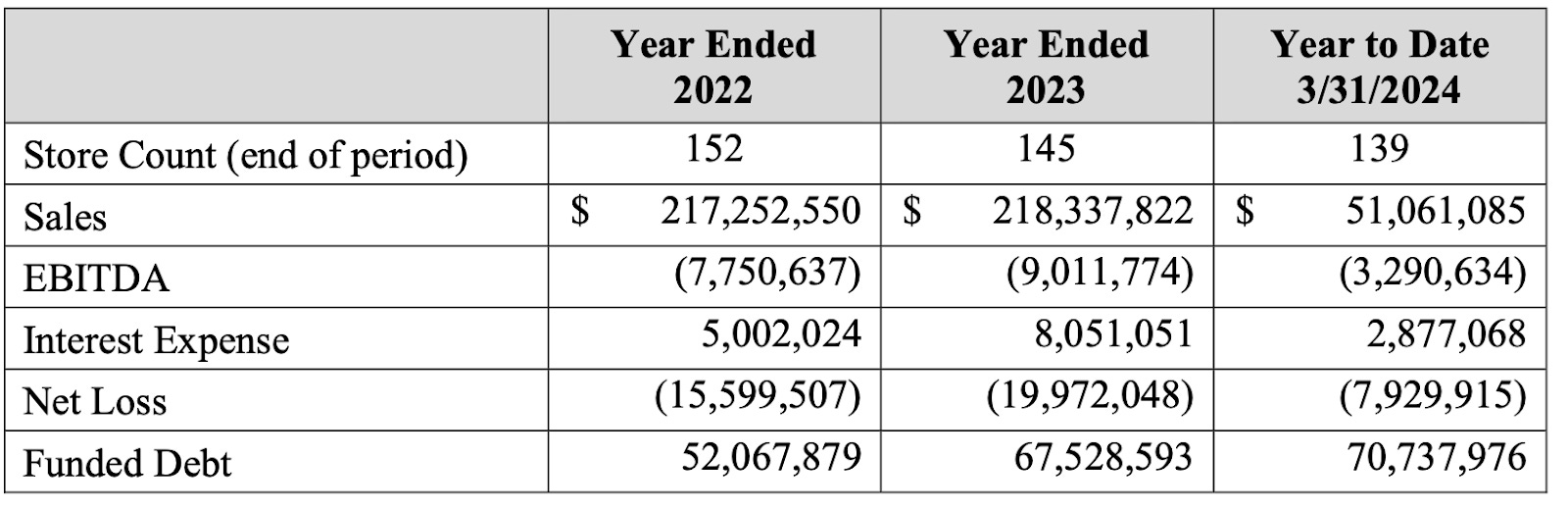

While somewhat helped by the easing of the “social distancing” diktats, foot traffic never really recovered and many stores have stubbornly refused to “bounce back” from the shutdown. What about food delivery services like DoorDash? “Achieving differentiation and a value proposition for online customers is increasingly challenging and results in lower operating margins,” the debtors’ CRO Nicholas Rubin of Force Ten Partners LLC states. Then factor in surging food utility prices, a tight labor market and labor costs. California’s minimum wage rose to $20/hour on April 1, 2024, compared to $13/hour at the start of ‘21. The debtors provided the following snapshot of financials:

Funded debt levels show an increase — the debtors were obliged to tap their senior credit facility — as does interest expense.

“The increased debt and associated reporting and oversight has added additional distraction to the management team attempting to enact a turnaround,” Rubin says. The debtors did what they could: store refreshes, a mobile app, a new website, a new menu, price increases, promotions. The debtors retained Hilco Real Estate LLC (“HRE”) in Nov. ‘23 to negotiate rent concessions with landlords and the debtors ultimately closed 53 underperforming locations in May. Also appearing in Nov. ‘23? Hilco Corporate Finance LLC (“HCF”), hired as investment banker to prepare and market the debtors, or “positions in the Company’s debt or equity securities,” for sale. Despite outreach to 293 financial sponsors and 63 strategic parties and entry into 43 noncompetes, there were no offers or indications of interest to acquire the debtors outside of an in-court process. Golub decided it had had enough: “In March 2024, TREW [Capital Management Private Credit LLC] acquired all of the senior secured first-lien debt obligations of the Company under the Prepetition Facility from Golub.” Can’t imagine Golub got anything near par. In April, Golub unloaded its equity interests. TREW, according to its website, “…focuses on distressed legendary brands, and brands with a proven business model, but require additional resources for growth.” Shortly thereafter, Alfred M. Masse, co-founder of management consultant Broadway Advisors LLC, became the debtors’ sole director.

So now what?

The debtors are ready for someone else to batter the shrimp and grill the corn: “The Debtors believe that a sale of substantially all of their assets as a going concern pursuant to section 363 of the Bankruptcy Code will deliver a value-maximizing result for their estates, creditors and other stakeholders.” To achieve this, the debtors are now “refocused on preserving cash and securing a stalking horse bid and debtor-in-possession financing,” Rubin says.

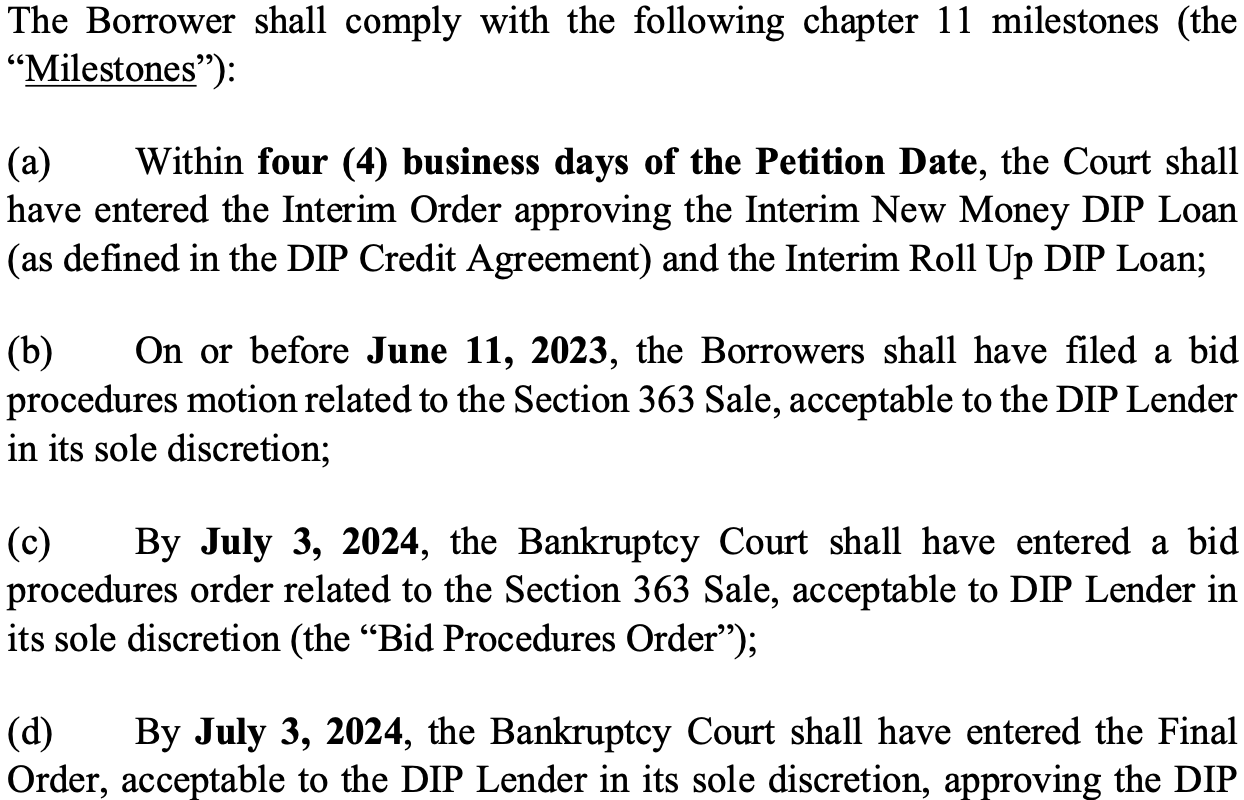

TREW is stepping up for the latter (and likely the stalking horse credit bid too, 🤔?). TREW’s proposed DIP financing consists of $4mm in a multiple-draw new money facility, with $1.5mm available in the interim period, and a $8mm rollup of pre-petition loans, $3mm of that in the interim. Each bear interest of 13%. There are no commitment or exit fees. There are, however, some pretty tight milestones:

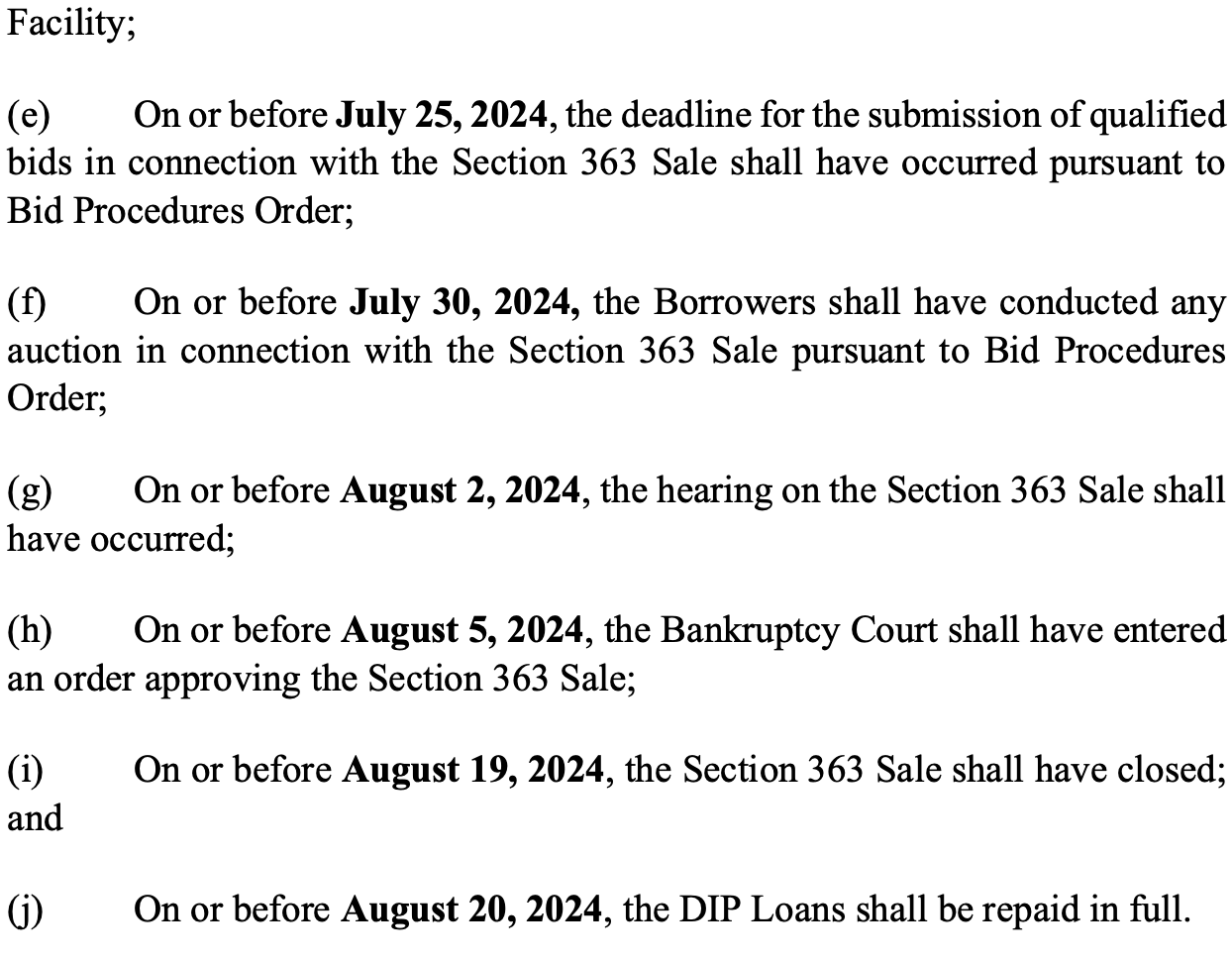

While the DIP matures in 90 days, clearly TREW doesn’t even want this dragging out that far: August 20, 2024, is right around the corner. Notably, TREW has also agreed to limit its credit bid in an attempt to foster robust bidding for the business.

A first day hearing occurred on Monday June 10, 2024 at 1pm ET with zero drama. ICYMI, the DIP milestones require a bid procedures motion on file by June 11, 2024.

The debtors are represented by Raines Feldman Littrell LLP (Hamid Rafatjoo, Robert Marticello, David Forsh) and Whiteford Taylor & Preston LLC (Thomas Francella Jr.). TREW is represented by Lathrop GPM LLP (Ryan Palmer, Brian Holland) and Culhane Meadows PLLC (Mette Kurth, Lynnette Warman).

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.