💥Viva Enviva Drama?💥

💥Viva Enviva Drama?💥

Plus: a Cano Health Update and Ambri Inc. files.

We got some good news for the folks at Vinson & Elkins LLP in the Enviva Inc cases this past Wednesday. No, the UST objection to their retention application hasn’t been thrown out. That’s still set for a hearing on May 9, 2024 at 2pm ET.

The “win” that V&E got was in the form of a final DIP order. You’ll recall that the UCC had ample objections to the DIP from our previous coverage:

While most of the objections were solved by some tweaks and additions of language in the DIP order, the hearing on May 1 became contentious over one remaining issue: absolute priority.

Let’s rewind a bit here. As part of the DIP agreement, equity holders will receive the right to participate in a $100mm portion of the DIP facility via a two week syndication period. By the time of the May 1 hearing, the syndication period was finished and the $100mm portion was oversubscribed.

Okay, so does the UCC want the syndication to be open to GUCs instead of equity holders?

According to V&E’s David Meyer, “no” is the answer:

“[T]he creditors’ committee has not and is not advocating for general unsecured creditors to participate in the DIP instead of the eligible shareholders. I will also note, Your Honor, the company has not received any inbound interest from any general unsecured creditor that has expressed an interest in participating in the DIP financing. Instead, if you want to make it really simple, Your Honor, the creditors’ committee simply does not want certain DIP creditors to participate in the DIP financing.”

It’s important to note that the $100mm is completely backstopped by the ad hoc group, so even if the syndication gets vetoed, the allocation will just get picked up by the ad hoc group. GUCs are not set to receive any “value” either way.

Judge Kenney had questions:

“How are the unsecured creditors harmed by this?”

“Is it your position that every time the court is faced with a debtor in possession financing proposal [from] whomever - I mean it could be $100mm from Bank of America - that we have to go through a marketing process to satisfy the absolute priority rule on every debtor in possession financing? I mean, how is this different from that?”

Akin Gump Strauss Hauer & Feld LLP’s Scott Alberino, on behalf of the UCC, responded:

“The harm here is that there’s ultimately a pie. We don’t know the size of that pie, Your Honor. I think what we’ve heard is that the company has come into bankruptcy with no finalized business plan, no valuation, no finalized capital structure, what the pie looks like nobody knows at this point. What we do know as part of a consensual negotiation process, the Tranche A DIP syndication rights, those rights convert into equity in the company at a discount to plan value. And as part of this negotiation, the debtors are taking that piece of the pie, that value that they negotiated, the future reorganization value, they’re taking that slice of pie - I like to use pie metaphors - and they’re giving it to shareholders. And we’re sitting here today saying, Your Honor, we want that slice of pie returned to the pie because it’s not even time to slice it up.”

Okay, other than working up all our appetites, Mr. Alberino also seems to be making a good point. Since the Tranche A DIP has an equity conversion feature, the shareholders being offered the $100mm participation rights are essentially getting a skip-the-line fast pass to the reorganized equity. But, again, the $100mm is backstopped by the ad hoc group and nobody disputed the necessity of that funding. So if the syndication right is stricken, the value still flows back to the ad hoc group, not GUCs.

After a series of thrilling witness testimonies, we got a ruling from Judge Kenney:

“The court finds, number 1, addressing the absolute priority rule. I’m going to assume the absolute priority rule applies in this context.”

“But I find that the syndication rights, the right to participate in the DIP, is not being granted on account of the equity holders’ [interests] in the company, it’s being granted on account of their willingness to put in new money.”

“So I overrule the absolute priority objection.”

“Second, I do find that the DIP Facility, including the $100mm syndication rights, is an exercise of the sound business judgement of the debtor.”

“And finally, I find that it is in the best interest of the [estate].”

Hmmm, maybe Virginia isn’t that bad of a venue after all!

But, something something about counting eggs before they hatch. There’s still the UST’s objection to V&E’s employment application, to which we received a new brief in support from the UST.

The UST continues to poke holes at V&E’s disclosure (or lack thereof) and highlights several new issues, notably:

V&E’s representation of Oaktree Capital Management LP, a member of the ad hoc group; and

The nature of V&E’s representation of several other ad hoc group members including Ares Management LLC, Barclays Banks PLC, Morgan Stanley Investment Management Inc, and Morgan Stanley & Co LLC.

Lol, according to the UST, V&E isn’t allowed to play with any of the other kids in the playground, it seems.

The UST also makes a callback to the UCC’s DIP objection:

“Vinson concurrently represents the Debtor and its largest equity holder, Riverstone Investment Group LLC (“Riverstone”), and has violated its fiduciary duties to the bankruptcy estate by negotiating and advocating for the RSA, which puts the interests of Riverstone over the interests of general unsecured creditors in violation of the absolute priority rule.”

Unfortunately, this argument is now moot given Judge Kenney’s ruling on the UCC’s DIP objection.

In response, V&E’s David Meyer submitted a declaration in support of the employment application:

“Based upon V&E’s contacts search, V&E currently represents or has represented in the past certain Members of the Ad Hoc Group in certain matters unrelated to these chapter 11 cases. V&E has not, does not, and will not represent any of the Ad Hoc Group Members in connection with the Debtors or these chapter 11 cases. As far as I can determine, the factual and legal issues in this matter are unrelated to the work V&E does or is likely to do for any of these Members in other matters.”

Pretty standard stuff right there. Regarding the UST’s inquiry into relationships between V&E and ad hoc group members, Mr. Meyer basically laid out the details:

“V&E’s representation of Ares Management LLC and its affiliates (“Ares”) in matters unrelated to the Debtors accounted for 0.7% of V&E’s billings and 0.8% of V&E’s collections for V&E’s fiscal year ended December 31, 2023.”

“V&E’s representation of Morgan Stanley & Co. LLC and its affiliates (“Morgan Stanley”) in matters unrelated to the Debtors accounted for 0.3% of V&E’s billings and 0.4% of V&E’s collections for V&E’s fiscal year ended December 31, 2023.”

“V&E’s representation of Oaktree Capital Management, LP and its affiliates (“Oaktree”) in matters unrelated to the Debtors accounted for 0.2% of V&E’s billings and 0.2% of V&E’s collections for V&E’s fiscal year ended December 31, 2023.”

“V&E was also recently hired in April 2024 by Monarch Alternative Capital LP (“Monarch”) to represent it in a matter unrelated to the Debtors’ restructuring process.”

So yes, V&E has relationships with certain ad hoc members BUT V&E maintains that all of these representations are unrelated to the debtors’ restructuring process and therefore does not constitute any conflict of interest. Also, you go V&E!

V&E further states, in a reply:

“V&E reports to and takes direction from Enviva’s management and board of directors, not Riverstone.

There is no Riverstone-affiliated person appointed to the Debtors’ management team.

Riverstone has consented to V&E’s representation of the Debtors, provided an advanced waiver including as to litigation, and retained its own counsel, Weil, Gotshal & Manges, LLP, in connection with the Debtors’ restructuring efforts.”

Basically V&E is saying the ball is in the UST’s court and they have to prove that V&E is in fact not a “disinterested” person.

We’re sure to hear plenty of these arguments at the May 9 hearing.

Speaking of the May 9 hearing, remember the motion from Wilmington Savings Fund Society FSB to reconstitute the UCC? Yeah, that’s teed up for May 9 as well. The UCC ended up filing a statement responding to the motion, saying:

“The Committee, as presently constituted by the Office of the United States Trustee (the ‘U.S. Trustee’), is confident in its ability to discharge its duties under the Bankruptcy Code and function as a fiduciary for all unsecured creditors.”

“The Committee recognizes that because RWE and Drax have certain connections to the Debtors—as trade creditors and contract counterparties on creditors’ committees invariably do—that may at times require limiting the type of information provided to RWE and/or Drax. It is not anticipated, however, that those connections will require a blanket exclusion or recusal of both RWE and Drax from each of the Committee’s deliberations and key decisions regarding the important issues in these chapter 11 cases. While the Committee is cognizant of the concerns raised by the Reconstitution Support Parties, the Committee believes that the Committee Bylaws implement appropriate safeguards that should alleviate any such concern.”

Suffice it to say, this response did not mollify WSFS.

So while we can cross UCC on ad hoc group violence off our list (thus far), we’re still left with UST on debtors’ counsel violence and indenture trustee on UST violence!

Judge Kenney is in for a fun ride at this next hearing.

🔋New Chapter 11 Bankruptcy Filing - Ambri Inc.🔋

On May 5, 2024, MA-based Ambri Inc. (the “debtor”) filed a chapter 11 bankruptcy case in the District of Delaware (Judge Silverstein). The debtor is, despite being founded in 2010, a pre-revenue “Liquid Metal” battery technology company “…working to become a leading global provider of long-duration, grid-scale, energy storage that can solve the most critical issues facing today’s electricity grid and enable wide-spread adoption of intermittent renewable energy as a 24-7 power source.” Is it odd that we read that description of the debtor’s product and literally all we could think about was this guy ⬇️?

Anyway, the company raised a ton of venture money from this guy ⬇️ who, to some with a conspiratorial mindset at least, is equally terrifying:

Indeed, per Crunchbase, Mr. Gates participated in the company’s $4mm Series A round; he then participated in a $15mm B round in ‘12; then he participated in a $35mm C round in ‘14, presumably a $17.2mm D round in ‘18 (this is a bit unclear), and a $144mm Series E round in ‘21. The debtor’s cap table now looks like this:

Khosla? Paulson? There are some big names there with Billy. With all of that backing, how did this thing end up in bankruptcy?

It appears the debtor overreached when it expanded its business from R&D (with a goal of licensing its tech) to manufacturing. Per the debtor:

To scale effectively and meet its new goals, the Debtor took on substantial costly obligations including an increased employee census, an expanded real estate footprint, and millions of dollars in construction costs to build out what was supposed to be the Debtor’s first high-volume manufacturing pilot facility.

Perhaps failing to recognize that the non-ZIRP environment changed the fundraising landscape considerably, the debtor went out to the venture market and was unable to land a Series F financing. The debtor therefore pivoted towards debt and sought approximately $50mm to fund operations. It didn’t get the debt commitment it needed either, falling short by $8mm in commitments and, due to defaults in the midst of scheduled tranches, tapping only ~$25.2mm thereof.* Here’s how that is distributed among the debtor’s various supporters:

The inability to hit the necessary funding level plus litigation commenced by the debtor’s landlord at its new production facility, precipitated the chapter 11 bankruptcy filing.

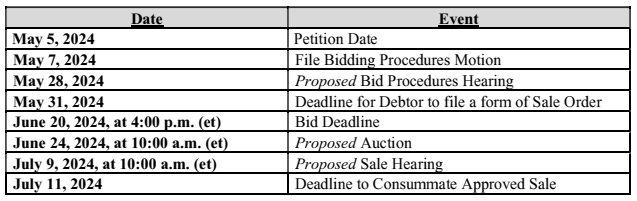

Before the filing, however, the debtor embarked on a sale and marketing process. Its investment banker contacted 125 parties and while some expressed interest in entering into a confidentiality agreement, “…no third-party has made an actionable proposal to the [d]ebtor.” All roads, therefore, for DIP financing and a stalking horse bid (via credit bid of the DIP), led back to certain the ~$25+mm of pre-petition secured lenders cum DIP lenders. The DIP consists of $9.5mm of 15% PIK new money ($3.75mm plus a 1:1 rollup of $3.75mm of pre-petition indebtedness upon an interim order) and a rollup of the remainder of the pre-petition secured indebtednesss upon a final order.** The DIP bakes in the following milestones:

Yup, yet ANOTHER expedited 363 case followed by a wind down. Who would’ve thought that the “higher for longer” interest rate environment would result in only cases like this…?

The debtors are represented by Goodwin Procter LLP (Kizzy Jarashow, Artem Skorostensky, Robert Lemons) and Potter Anderson & Corroon LLP (L. Katherine Good, Brett Haywood, Gregory Glasser) as legal counsel, and Portage Point Partners (Stephen Bremer) as financial advisor and investment banker. Gates Frontier LLC, as pre-petition lender and DIP lender, is represented by Kirkland & Ellis LLP (Chad Husnick, Christopher Koenig, Andy Veit) and Morris Nichols Arsht & Tunnell LLP (Robert Dehney, Andrew Remming, Sophie Rogers Churchill).

*With accrued interest, the debtor owes approximately $27mm (excluding various fees).

**The DIP carries a 1% PIK funding fee.

⚡️Update: Cano Health Inc⚡️

We’re going to revisit our favorite value based care deSPAC bankruptcy, Cano Health Inc., because the debtors have recently filed an amended plan and disclosure statement!

Yippee!

Well, “yippee” until you get to this line:

“No bids for a Whole-Co Sale Transaction were received by the Debtors by the Initial IOI Deadline.”

Womp womp.

No worries though, it’s called a “dual-path” process for a reason! Time to toggle to the RSA’s reorganization plan. We went over the RSA in our initial first day coverage here:

As you’ll recall, the first lien secured notes were set to become the new owners of reorganized Cano. Nothing has changed there. First lien claimants will receive 100% of the new equity interests for $468.5mm in first lien claims, leaving ~$505mm as deficiency claims which are dropped down into the GUCs basket.

The first lien claimants will also receive their pro rata share in $50mm worth of exit facility loans. That exit facility will also include a rollover of the $150mm DIP facility.* Add a planned new RCF loan on top of all that and you end up with a post emergence cap structure that looks like this:

GUCs are all but wiped. Total allowed GUCs sit at ~$900mm and claimants will receive warrants to purchase up to 5% of the new equity, proceeds from the sale of the company’s MSP Recovery Inc ($LIFW) shares ($5.5mm), and litigation trust proceeds. All that will result in a ~1.5% recovery.

And so of course the UCC raised objections to the disclosure statement, saying:

“In total, the Disclosure Statement estimates that general unsecured creditors will recover only approximately 1.5% on their claims under the Debtors’ proposed Plan; in reality, recoveries to general unsecured creditors are expected to be infinitesimal due to larger than expected claims that have been filed prior to the Bar Date (which has now passed).”

Yeah… we mean, do you see where the fulcrum is guys? Y’all are wayyy out of the money here. But, of course, they think the enterprise value of the emergeco is understated by the debtors:

“In addition, the Debtors appear to understate their total enterprise value, despite the Company’s budget out-performance during the Chapter 11 Cases, the recent uplift in the Company’s business plan and the Company’s continued upward trajectory in terms of its cost-savings initiative and corresponding financial results.”

The UCC will have to perform some Excel gymnastics to propose a plan value that is $505mm (the amount of the first lien deficiency claims) higher than the one from the debtors.

And the UCC continues:

“With regard to the Litigation Trust Proceeds, from the outset of the Chapter 11 Cases the Debtors have broadcasted allegations of misconduct by certain former officers or directors of the Company (“D&Os”), and have assigned those claims, but not other potential claims, to the Litigation Trust. Indeed, the Debtors focus on the Debtors’ former CEO, but divert creditor attention away from unconditional insider releases of all current D&Os, including those that were on the scene at the time of the pre-petition misconduct alleged by the Debtors.”

“Former CEO” being, of course, Marlow Hernandez.

The UCC also identified some troublesome cash retention rewards that were issued, apparently, just 48 hours before Cano’s bankruptcy filing:

“To put matters into perspective, these executive cash awards exceed the entirety of the cash distribution to be made to all general unsecured creditors under the Plan.”

The disclosure hearing is set for May 9, 2024 at 9:30am ET and replies from the debtors and the ad hoc first lien group have been filed in advance of the hearing.

Anyway, back to reorganized Cano. The go forward plan is for the emergco to run off of 80 locations (vs 170 back in March ‘23) and is projected to reach $199mm in EBITDA by FY’28:

Putting the equity value estimate at a midpoint of $451mm:

Throw back to the good ol’ days when Cano was valued at $4.4b in the original deSPAC transaction.

*Per the RSA (Exhibit A), the exit facility will carry an interest rate of, for the first 24 months, SOFR+100bps payable in cash plus either (i) 700bps in cash or (ii) 850bps PIK and, after 24 months, SOFR+800bps in cash. The exit facility has a 5 year maturity after the effective date.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.