💥New Chapter 11 Bankruptcy - Vyaire Medical Inc.💥

💥New Chapter 11 Bankruptcy - Vyaire Medical Inc.💥

Medical device manufacturer files with RSA to sell the business.

Not so much.

On June 9, 2024, Illinois-based Vyaire Medical Inc. (“Vyaire”) and 27 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Shannon) — a little over (i) six months after that ⬆️ ill-fated Insta post, (ii) six years after sponsor Apax Partners (“Apax”) acquired the entirety* of the debtors’ business from Becton Dickinson & Co. (“BD”) in a (leveraged) deal worth approximately $435mm, and (iii) one year after lenders organized with Gibson Dunn & Crutcher LLP to agitate for negotiations over the debtors’ unwieldy balance sheet ⬇️.**

A balance sheet that is, uh, a direct result of the Apax/BD transaction. Gotta hate when that happens!

Vyaire is a global company with two primary business segments:*** (i) ventilation, which focuses on helping patients in hospitals, health centers and private-practice facilities breathe (“Ventilation”); and (ii) respiratory diagnostics, which develops, manufactures and commercializes devices used to diagnose pulmonary and cardio pulmonary diseases (“Respiratory Diagnostics”). Your nana’s breathing powered by private equity! Apax’s healthcare company in need of a bankruptcy “breathing spell!!”

We won’t delve into the details but suffice it to say, the businesses have had their ups and downs in the pandemic and post-pandemic worlds. Per the debtors, “[t]he post-COVID-19 drop-off in demand for the Ventilation business, a difficult pivot in the [c]ompany’s go-to market strategy, and unsustainable overhead costs led to a downward spiral of liquidity” and, ultimately, “[t]he [c]ompany’s operational challenges and Ventilation’s negative cash flow have proved difficult to overcome.” Wait. Isn’t the whole private equity value proposition that they know how to streamline and operate businesses to full optimization? LOL.

A PJT Partners LP-attempt to save the day with an amend and extend transaction of the debtors’ first lien debt — a $339.3mm 1L term loan + $78.6mm in first lien notes — ground to a halt and by April ‘24 the debtors were in full on scramble mode. Apax be like …

…and all of a sudden disinterested directors started multiplying like flies on sh*t … the sh*t here, obviously, being Vyaire’s disintegrating business.**** The debtors pivoted to negotiating a DIP and simultaneously launched a pre-petition sale and marketing process of the business in parts or as a whole — a process that, as of the petition date, has allegedly yielded several expressions of interest but no formal stalking horse purchaser.

A chapter 11 bankruptcy sale process without a stalking horse?! How original, guys!!

There is, however, a restructuring support agreement (“RSA”). More originality!! The RSA outlined the terms of a proposed DIP credit facility (and use of cash collateral) — much needed given the debtors’ very limited $1.7mm of cash on hand as of the petition date — backstopped by an Ad Hoc 1L Group (Gibson loves its groups as much as we love our exclamation points!). It has the support of lenders holding over 90% of the first lien term loan, lenders holding 100% of the second lien term loan, and Apax.

So what of the DIP? Per usual, it’s the machine breathing life into this zombie (see what we did there?). There are aggressive milestones, of course: a July 24, 2024 auction date; a July 29, 2024 sale hearing; and an August 19, 2024 sale consummation deadline. The Ad Hoc 1L Group isn’t f*cking around. Per the debtors:

“Conducting a thorough marketing and bidding process and consummating a Sale Transaction(s) on the timeline contemplated herein is vitally important to the Debtors’ efforts to maximize value. Such Sale Transaction(s) would benefit not only the Debtors, but their vendors, dedicated employees, lenders, and other key stakeholders as well.”

A bid procedures motion is already on file because, you know, debtors love just giving away bid protections these days. It used to be that stalking horse purchasers negotiated bid protections as a necessary requirement to putting in the work. Now so many cases file without a stalking horse in the first place that the debtors have to preload the breakup fee — even when a partner isn’t even sitting across the table. “Take our money please!” We reckon an established industry standard of 3% helps tee that up.

Alas, that’s where we’re at here. The debtors propose a break-up fee of 3% of the total cash consideration (inclusive of an expense reimbursement) subject to certain disqualifying events such as, among other things, a credit bid. The debtors seek a $140mm minimum bid or they’re going to cancel the sh*t out of this proposed auction. Interestingly, the debtors have filed a motion seeking to keep certain potential interested parties in the debtors’ assets under seal — as opposed to list them in connection with conflicts checks run by the various proposed debtor professionals. We can’t wait to see what the UST has to say about that given the good stuff that’s been happening in other cases such as Invitae Corp. and Enviva Inc., see below … yeah, yeah, different jurisdiction blah blah blah.

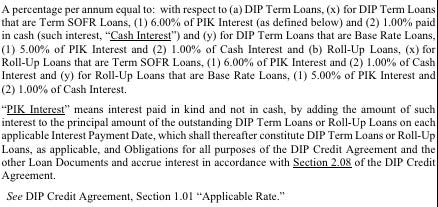

As for the actual DIP terms, there’s a new money portion and a roll-up portion because, like, this is the least original case of all time.

It’s all provided and backstopped by the Ad Hoc 1L Group. The breakdown is $45mm of new money ($25mm interim) and a $135mm roll-up of 1L term loans into the DIP ($75mm interim, 3:1 rollup of prepetition secured 1L term loans relative to $45mm of new money). The Ad Hoc 1L Group required this roll-up, of course, or, they say, they’re ✌️. They get liens on unencumbered assets and priming liens, OF COURSE. And for their trouble the 1L lenders get…

…plus a 2% commitment fee ($900k), a 5% backstop fee ($2.25mm)(!), and a 1.25% exit fee ($562.5k). Money. Money. Money.

After the sale(s) are consummated, the intent of the parties is to wind down what remains.

The debtors are represented by Kirkland & Ellis LLP (Joshua Sussberg, Spencer Winters, Yusuf Salloum, Christopher Ceresa, Tiffani Chanroo, Mark McKane, Tabitha De Paulo, Joseph D’Antonio) and Cole Schotz PC (Patrick Reilley, Michael Sirota, Warren Usatine) as legal counsel, AlixPartners LLC (Charles Braley) as financial advisor and PJT as investment banker (Michael Schlappig, Jaimie Baird, Dylan Friesner). As noted previously, Gibson Dunn & Crutcher LLP (Scott Greenberg, Jason Zachary Goldstein, Joshua Brody, Kevin Liang) represents the Ad Hoc 1L Group with co-counsel, Pachulski Stang Ziehl & Jones LLP (Laura Davis Jones, Timothy Cairns). Rothschild & Co. is their financial advisor. Apax is represented by Simpson Thacher & Bartlett LLP (Elisha Graff, Ashley Gherlone). Finally, Bank of America NA as 1L Admin Agent is represented by Haynes and Boone LLP (Eli Columbus, J. Frasher Murphy, Matt Ferris) and Ashby & Geddes PA (Michael DeBaecke) as legal counsel and RPA Advisors LLC as financial advisor.

A first day hearing will be held later today, June 11, 2024, at 10:30am ET.

*Apax acquired a majority stake in the business in Q4’16 and bought the remaining stake from Becton in Q2‘18.

**Rothschild & Co. came on board shortly thereafter.

***It had a third segment, a consumables business, that it divested in May ‘23 to SunMed Group Holdings LLC (d/b/a AirLife) for $310mm — $133.9mm net after pay down of a then-outstanding and now-terminated RCF — in an effort to shore up cash. Clearly this didn’t do the trick! SunMed has counsel that has made a notice of appearance — Goodwin Procter LLP (Kizzy Jarashow, Alexander Nicas, Liza Burton, Amanda Schaefer) and Potter Anderson & Corroon LLP (L. Katherine Good, Aaron Stulman), 🤔.

****Insert Paul Aronzon, Ron Labrum, Bret Wise and David Barse. What? No women disinterested directors wanted to touch this turd?

Company Professionals:

Legal: Kirkland & Ellis LLP (Joshua Sussberg, Spencer Winters, Yusuf Salloum, Christopher Ceresa, Tiffani Chanroo, Mark McKane, Tabitha De Paulo, Joseph D’Antonio) and Cole Schotz PC (Patrick Reilley, Michael Sirota, Warren Usatine)

Financial Advisor: AlixPartners LLC (Charles Braley)

Investment Banker: PJT Partners LP (Michael Schlappig, Jaimie Baird, Dylan Friesner)

Claims Agent: Omni (Click here for free docket access)

Other Parties in Interest:

DIP Agent: Wilmington Savings Fund Society NA

Legal: ArentFox Schiff LLP (Jeffrey Gleit, Brett Goodman, Matthew Bentley) and Morris James LLP (Eric Monzo, Brya Keilson, Siena Cerra)

1L Admin Agent: Bank of America NA

Legal: Haynes and Boone LLP (Eli Columbus, J. Frasher Murphy, Matt Ferris) and Ashby & Geddes PA (Michael DeBaecke)

Financial Advisor: RPA Advisors LLC

2L Admin Agent: Wilmington Trust NA

1L Ad Hoc Group

Legal: Gibson Dunn & Crutcher LLP (Scott Greenberg, Jason Zachary Goldstein, Joshua Brody, Kevin Liang) and Pachulski Stang Ziehl & Jones LLP (Laura Davis Jones, Timothy Cairns)

Financial Advisor: Rothschild & Co.

Sponsor: Apax Partners

Legal: Simpson Thacher & Bartlett LLP (Elisha Graff, Ashley Gherlone)

Interested Party: SunMed Group Holdings LLC

Legal: Goodwin Procter LLP (Kizzy Jarashow, Alexander Nicas, Liza Burton, Amanda Schaefer) and Potter Anderson & Corroon LLP (L. Katherine Good, Aaron Stulman)