🌮New Chapter 11 Bankruptcy - MRRC Hold Co. (Rubio's Coastal Grill)🌮

🌮New Chapter 11 Bankruptcy - MRRC Hold Co. (Rubio's Coastal Grill)🌮

Restaurant chain files to pursue a 363 sale; it seeks stalking horse purchaser.

First Tijuana Flats Restaurants LLC and now this!? Ay dios mio!

On June 5, 2024, California-based MRRC Hold Co. (a/k/a Rubio’s Coastal Grill) and two affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Goldblatt). You may know the debtors from their delightful Fish Tacos, or the Mexican Street Corn Shrimp Two-Taco Plate, offered at one of their 86 leased locations in California, Arizona and Nevada:

Or, more likely, you may remember the debtors from their late ‘20 appearance in bankruptcy court: one of the 630 companies filing during the “plague year.” We wrote about that previous filing here…

…and — ⚡️whoa boy⚡️— that prior coverage makes for an amusing read worth a revisit if we do say so ourselves.

Go ahead, take a second. We’ll wait.

We’ll wait because, as we wrote then, the debtors didn’t entirely remedy their balance sheet with that prior restructuring. Indeed, the debtors currently carry, in part as a remnant of the prior bankruptcy, nearly $73mm of funded secured debt on balance sheet. Golub Capital LLC (“Golub”) provided the $52mm of senior secured first-lien exit financing as reflected here at the time⬇️.

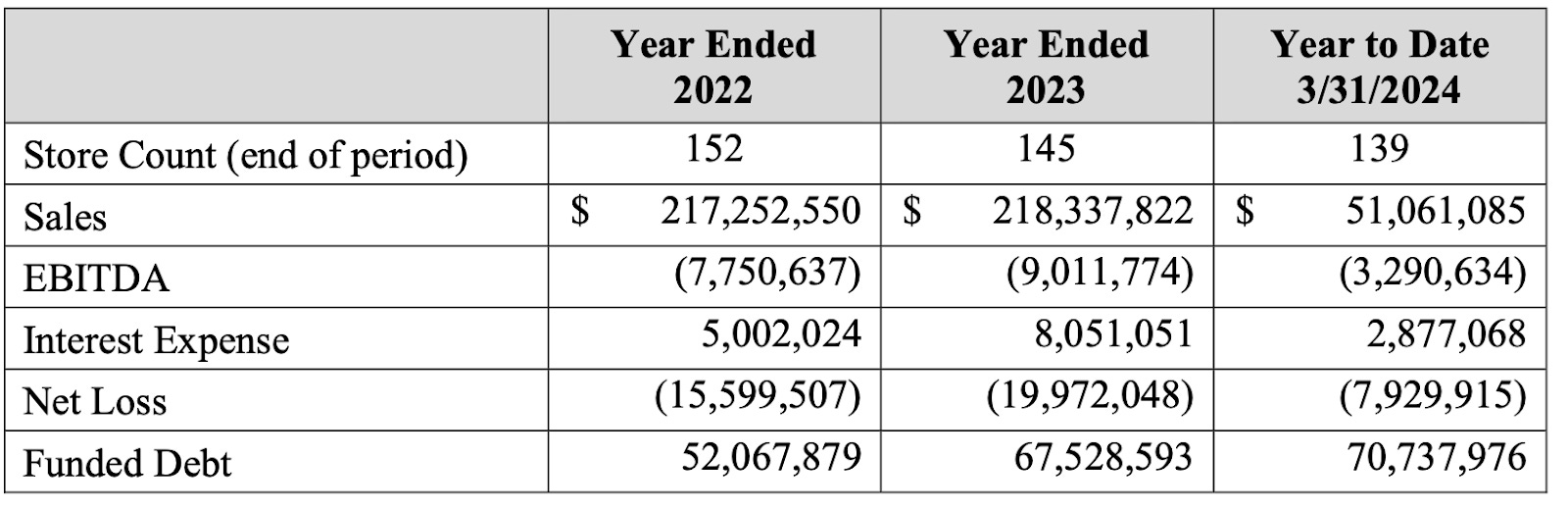

While somewhat helped by the easing of the “social distancing” diktats, foot traffic never really recovered and many stores have stubbornly refused to “bounce back” from the shutdown. What about food delivery services like DoorDash? “Achieving differentiation and a value proposition for online customers is increasingly challenging and results in lower operating margins,” the debtors’ CRO Nicholas Rubin of Force Ten Partners LLC states. Then factor in surging food utility prices, a tight labor market and labor costs. California’s minimum wage rose to $20/hour on April 1, 2024, compared to $13/hour at the start of ‘21. The debtors provided the following snapshot of financials:

Funded debt levels show an increase — the debtors were obliged to tap their senior credit facility — as does interest expense.

“The increased debt and associated reporting and oversight has added additional distraction to the management team attempting to enact a turnaround,” Rubin says. The debtors did what they could: store refreshes, a mobile app, a new website, a new menu, price increases, promotions. The debtors retained Hilco Real Estate LLC (“HRE”) in Nov. ‘23 to negotiate rent concessions with landlords and the debtors ultimately closed 53 underperforming locations in May. Also appearing in Nov. ‘23? Hilco Corporate Finance LLC (“HCF”), hired as investment banker to prepare and market the debtors, or “positions in the Company’s debt or equity securities,” for sale. Despite outreach to 293 financial sponsors and 63 strategic parties and entry into 43 noncompetes, there were no offers or indications of interest to acquire the debtors outside of an in-court process. Golub decided it had had enough: “In March 2024, TREW [Capital Management Private Credit LLC] acquired all of the senior secured first-lien debt obligations of the Company under the Prepetition Facility from Golub.” Can’t imagine Golub got anything near par. In April, Golub unloaded its equity interests. TREW, according to its website, “…focuses on distressed legendary brands, and brands with a proven business model, but require additional resources for growth.” Shortly thereafter, Alfred M. Masse, co-founder of management consultant Broadway Advisors LLC, became the debtors’ sole director.

So now what?

The debtors are ready for someone else to batter the shrimp and grill the corn: “The Debtors believe that a sale of substantially all of their assets as a going concern pursuant to section 363 of the Bankruptcy Code will deliver a value-maximizing result for their estates, creditors and other stakeholders.” To achieve this, the debtors are now “refocused on preserving cash and securing a stalking horse bid and debtor-in-possession financing,” Rubin says.

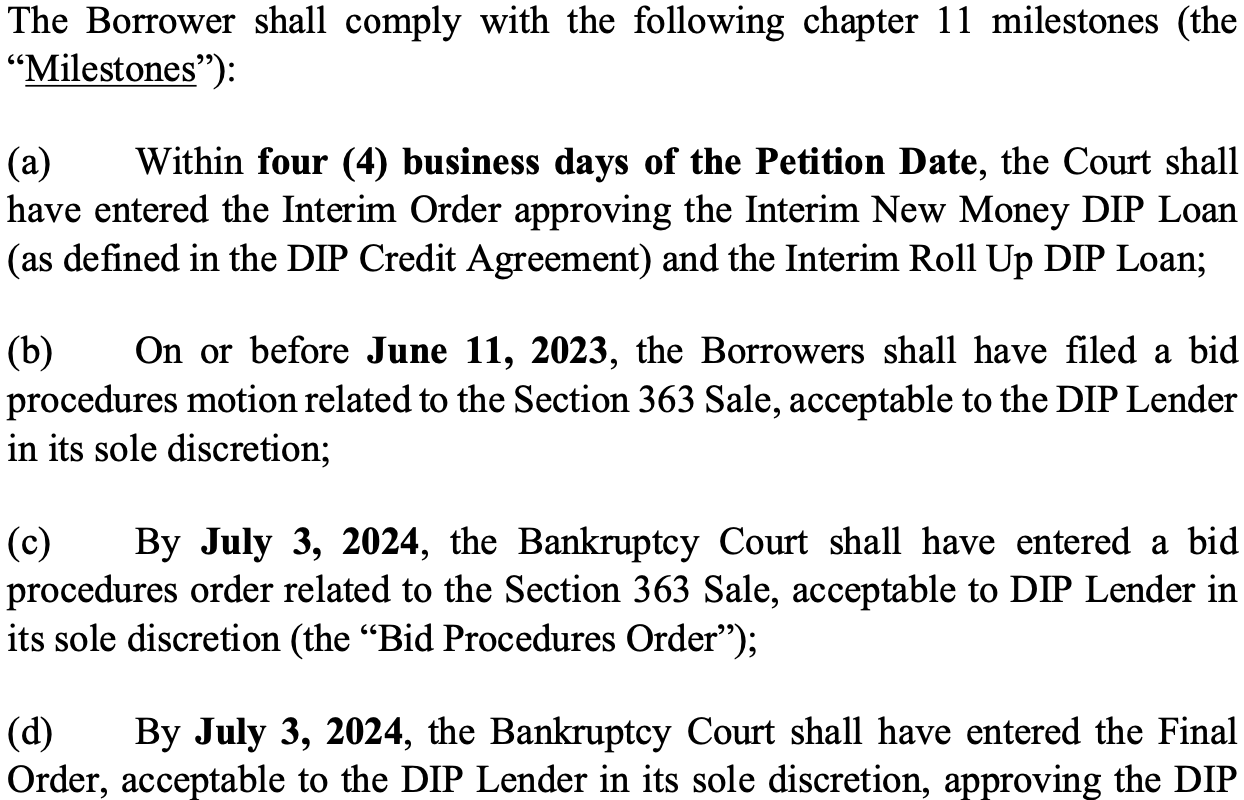

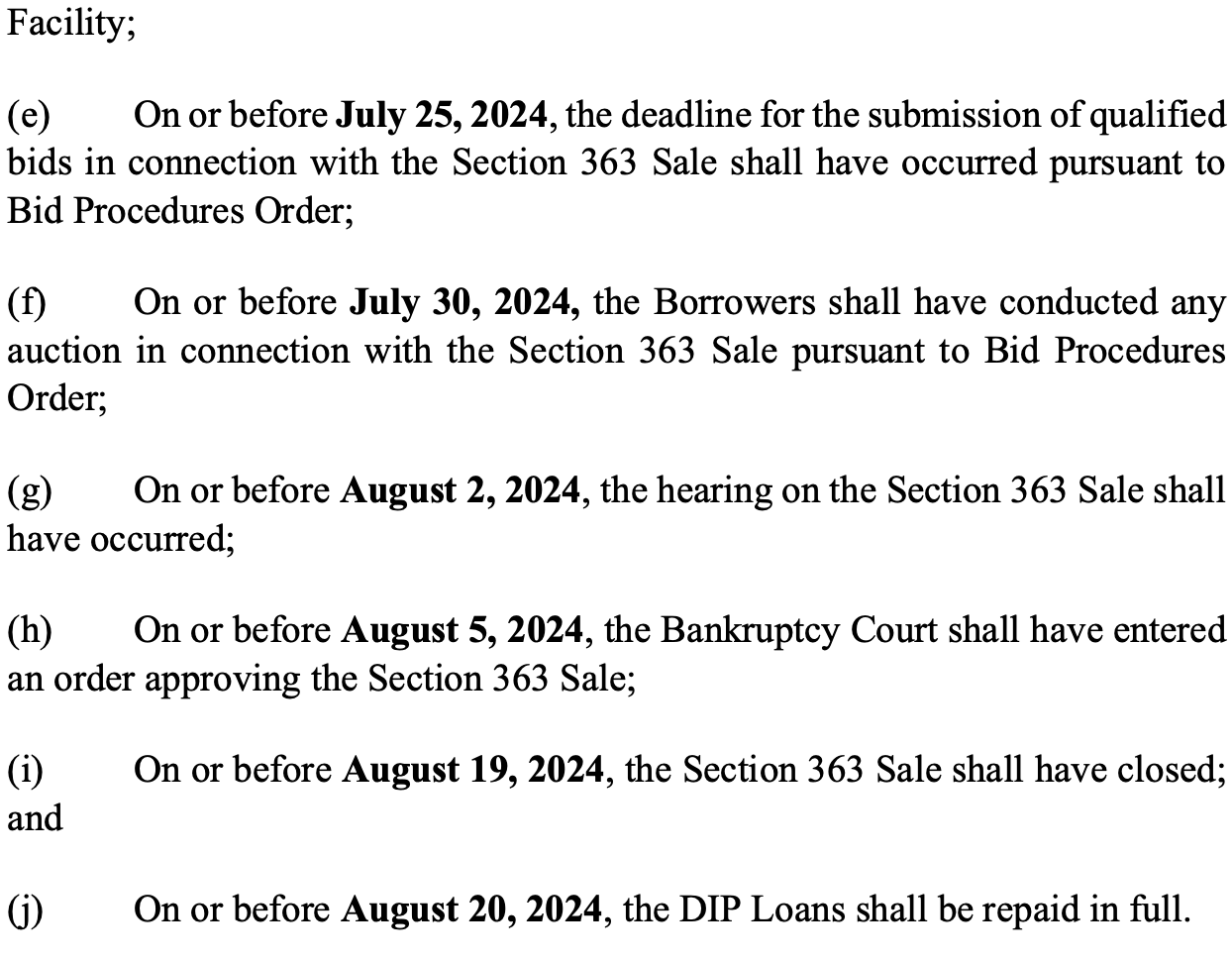

TREW is stepping up for the latter (and likely the stalking horse credit bid too, 🤔?). TREW’s proposed DIP financing consists of $4mm in a multiple-draw new money facility, with $1.5mm available in the interim period, and a $8mm rollup of prepetition loans, $3mm of that in the interim. Each bear interest of 13%. There are no commitment or exit fees. There are, however, some pretty tight milestones:

While the DIP matures in 90 days, clearly TREW doesn’t even want this dragging out that far: August 20, 2024, is right around the corner. Notably, TREW has also agreed to limit its credit bid in an attempt to foster robust bidding for the business.

A first day hearing occurred on Monday June 10, 2024 at 1pm ET with zero drama. ICYMI, the DIP milestones require a bid procedures motion on file by June 11, 2024.

The debtors are represented by Raines Feldman Littrell LLP (Hamid Rafatjoo, Robert Marticello, David Forsh) and Whiteford Taylor & Preston LLC (Thomas Francella Jr.). TREW is represented by Lathrop GPM LLP (Ryan Palmer, Brian Holland) and Culhane Meadows PLLC (Mette Kurth, Lynnette Warman).

Company Professionals:

Legal: Raines Feldman Littrell LLP (Hamid Rafatjoo, Robert Marticello, David Forsh) and Whiteford Taylor & Preston LLP (Thomas Francella Jr.)

Financial Advisor/CRO: Force 10 Partners (Nicholas Rubin)

Investment Banker: Hilco Corporate Fiance LLC (Terri Stratton, Sanjay Marken, Richard Klein)

Real Estate Advisor: Hilco Real Estate LLC

Claims Agent: Stretto (Click here for free docket access)

Other Parties in Interest:

Successor Pre-Petition Lender & DIP Lender: TREW Capital Management Private Credit LLC

Legal: Lathrop GPM LLP (Ryan Palmer, Brian Holland) and Culhane Meadows PLLC (Mette Kurth, Lynnette Warman)