💥New Chapter 11 Bankruptcy - Nevada Copper Inc.💥

💥New Chapter 11 Bankruptcy - Nevada Copper Inc.💥

Copper miner runs into the ominous sounding "geotechnical problem."

On June 10, 2024, Nevada Copper Inc. and five affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Nevada (Judge Barnes).

Founded in ‘05, Nevada Copper, Inc. is a copper mining company based in northwestern Nevada. Under the “NCU” ticker, Nevada Copper, Inc. is a publicly listed company traded on the Toronto Stock Exchange. As of the most recent quarterly filing, the debtors’ largest shareholders are Pala Investments Limited (“Pala”), holding roughly 61.66% of the stock, and Mercuria Energy Trading S.A. (“Mercuria”), holding approximately 17.24%.

The debtors’ primary asset is the Pumpkin Hollow project, a plot of land near Yerington, Nevada, containing “substantial” mineral reserves and resources, mainly copper but also gold, silver, and iron. The project opened in Dec. ‘19 and was initially slated to bring in an annual average of 50mm pounds of copper over the mine’s lifetime.

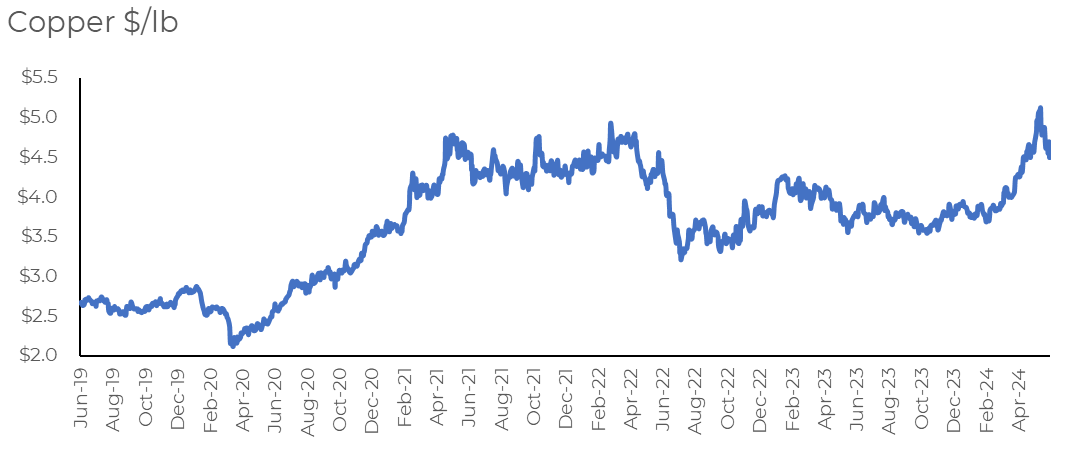

At this point, you might be thinking, “Wasn’t copper just at an all-time high??” It certainly was and is still up close to 80% from ‘19 prices.

So we wondered, does the price of copper not correlate with the performance of the copper miners? Answer: it definitely does. Here is the Global X Copper Miners ETF over the same period.

So, what went wrong with Nevada Copper? According to company filings, the Pumpkin Hollow project “...encountered an unidentified weak rock structure in the main ramp to the East South Zone which delayed access to planned stopes and required additional drilling and geotechnical mitigation work.” The geotechnical problem eliminated the debtors' primary source of operating income (which was negative to begin with). According to the 2Q22 earnings filing, the debtors had $3.9mm in cash and nearly $200mm in debt. Repeat: the debtors had $3.8mm in cash and nearly $200mm in debt.

With liquidity clearly an issue, the debtors negotiated a new financing package with certain stakeholders (“Restart Financing Packages”). The Restart Financing Packages initially included $15mm of new A-2 loans (“Tranche A-2 Loans”) from Pala, Triple Flag International Ltd. (“Triple Flag”), and Mercuria (the “Tranche A-2 Lenders”). The Tranche A-2 Lenders later provided an additional $16mm.

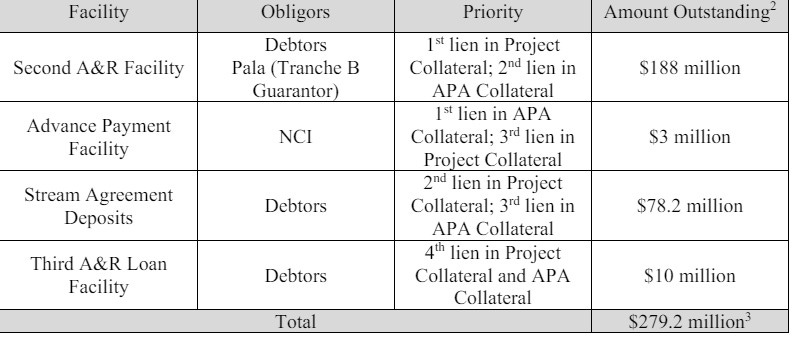

With the Tranche A-2 Loans in place, the debtors’ current capital structure came into place. In total, they have prepetition secured obligations totaling $279.2mm and prepetition unsecured obligations totaling $226.6mm.

The debtors entered into the Second A&R Facility in May ‘19 with KfW IPEX-Bank GmbH (“KfW”). The Second A&R Facility originally provided the debtors with access to $115mm (Tranche A), with an additional $15mm added in Oct. ‘21 (Tranche B). The debtors later tacked on theTranche A-2 Loans as part of the Restart Financing Packages. The chart above reflects both lien priority and the total outstanding amount under the Second A&R Facility as of the petition date.

The Advance Payment Facility is an advanced payment agreement with Concord Resources Limited (“Concord”), which stipulated that Concord would provide the debtors with advance payments in exchange for copper concentrate. If the value of the debtors’ copper concentrate deliveries were worth less than what Concord paid, the debtors would be obligated to make a cash payment equal to the difference, which totaled roughly $3mm as of the petition date.

The Stream Agreement is a similar arrangement in which the debtors received upfront cash from Triple Flag in exchange for a percentage of future metal production. Until the deposit is fully credited with metal deliveries (which won’t be anytime soon), the delivery obligations represent a secured debt held by Triple Flag. As of the petition date, there’s roughly $78mm is outstanding.

Finally, the Third A&R Facility was a $5.6mm advance from Pala as part of the Restart Financing Packages. Interest on the facility is payable in kind, resulting in an outstanding balance of $10mm as of the filing.

The debtors also have their fair share of unsecured obligations, consisting of deferred funding agreements and intercompany loans totaling $226.6mm.

With their debt an albatross and liquidity severely strained, the debtors’ struggled. Ultimately, they decided that a sale would be the most efficient step forward. In Oct. ‘23, the debtors engaged Citigroup Global Markets Inc. ($C) to begin an out-of-court sale and marketing process. The debtors, however, could not agree to terms with any interested parties, and with time (read: money) running out, they switched focus to pursuing an in-court 363 sale process with bankruptcy protection.

To fund their proposed 363 sale process, the debtors secured a DIP financing commitment from affiliates of Elliott Investment Management L.P. (“Elliot”) – Manchester Securities Corp, and Ziwa Investments Limited – of$60mm ($20mm interim). Interest on the facility is equal to S+900, with a credit spread adjustment. The facility includes a 5% upfront fee, a 1% unused commitment fee, and a 1% exit fee. To date, the debtors have only received consent for $51.4mm from KfW, due to concerns over adequate protection. The debtors hope to obtain full consent from KfW prior to a final hearing on the DIP.

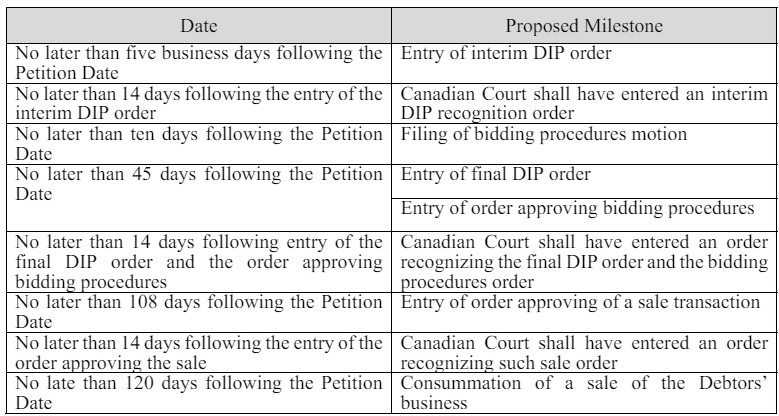

The debtors plan to file a bidding procedures motion by June 20, 2024. Here’s the case timeline:

The debtors’ first day hearing went off without a hitch.

The debtors are represented by Allen Overy Shearman Sterling US LLP (Fredric Sosnick, Sara Coelho) or, according to the debtors’ claims agent Epiq, Fredric’s doppelganger, Frederic Sisnick…

…and McDonald Carano LLP (Ryan Works, Amanda Perach) as legal counsel, Torys LLP as Canadian legal counsel, AlixPartners LLP as financial advisor, and Moelis & Company (Zul Jamal) as investment banker. KfW is represented by Parsons Behle & Latimer (Rew Goodenow) and the DIP lenders are represented by Akin Gump Strauss Hauer & Feld LLP (Ira Dizengoff, Brad Kahn, Joseph Szydlo, Kate Doorley) and Shea Larsen (James Patrick Shea, Bart Larsen, Kyle Wyant).

Company Professionals:

Legal: Allen Overy Shearman Sterling US LLP (Frederic Sosnick, Sara Coelho) and McDonald Carano LLP (Ryan Works, Amanda Perach)

Canadian Legal: Torys LLP

Financial Advisor: AlixPartners LLP

Investment Banker: Moelis & Company LLC (Zul Jamal)

Claims Agent: Epiq (Click here for free docket access)

Other Parties in Interest:

DIP Lenders: Elliott Investment Management LP, Manchester Securities Corp., Ziwa Investments Limited

Legal: Akin Gump Strauss Hauer & Feld LLP (Ira Dizengoff, Brad Kahn, Joseph Szydlo, Kate Doorley) and Shea Larsen (James Patrick Shea, Bart Larsen, Kyle Wyant)

DIP Admin Agent: U.S. Bank Trust Company NA

KfW

Legal: Parsons Behle & Latimer (Rew Goodenow)