💥New Chapter 11 Bankruptcy & CCAA - Coach USA Inc.💥

💥New Chapter 11 Bankruptcy & CCAA - Coach USA Inc.💥

Bus operator drives towards multiple asset sales; lenders still hung.

We’ve talked about buses in bankruptcy before but usually we’re referring to someone — say, a creditor or a professional or a former management team member — getting thrown under the bus.

It’s not very frequently that the bus, itself, drives into bankruptcy.

On June 11, 2024, bus operator and “mobility solutions” provider (wtf, lol) Coach USA Inc. and 94 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Walrath) — another company, similar to Vyaire Medical Inc. which also filed this week, to suffer from the long-arm of the COVID-19 pandemic.

That’s right. The pandemic. It’s still claiming victims. Driver shortages and severe declines in ridership caused by the pandemic helped do the debtors in. After all, it’s tough enough, on one hand, not to have the ridership your private equity overlords might have projected at the time of purchase…

… best timing ever btw … but even tougher when you don’t have the drivers to service what little demand you do have.

Oh c’mon, PETITION, how bad could demand still be this far after the pandemic receded?

Ridership declined a staggering-yet-unsurprising 90% in ‘20 compared to pre-pandemic ridership. In ‘21, the decline improved to 74%. In ‘22, to ‘61%. And in ‘23, ridership was still down 55% compared to pre-pandemic levels, 😬. You work from home types did this!

You might be wondering, “with ridership that atrocious, how the f*ck did the company even survive this long?” and that is an awfully fair question. And here is your answer:

Oh you didn’t actually think Variant Equity was cutting a steady stream of equity checks for four years, did you?

Nooooooooooooooooooooooooooooooooo.

Instead, the debtors tapped the Federal Reserve System’s Main Street Lending Program —created under the Coronavirus Aid Relief & Economic Security (CARES) Act — for a $35mm unsecured loan in December ‘20. And then in August and October ‘21, the debtors received a total of $78.3mm in grants from the federal government’s Coronavirus Economic Relief for Transportation Services program. Anyone want to guess who the debtors’ largest general unsecured creditor is? Money well spent, guys!

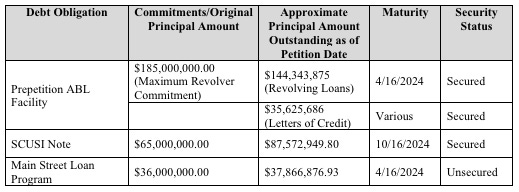

Unfortunately, the Main Street paper (which now sits at $37.9mm owed) is not the only debt on balance sheet. In fact, the debtors’ capital structure is, in large part, a remnant of Variant Equity’s ill-fated purchase. It consists of:

There’s also $134mm of trade debt.

By November ‘23, the debtors, despite lagging performance, continued to make their required payments of principal and interest on the ABL. Nevertheless, they tripped various financial covenants and triggered certain events of default. Shortly thereafter, the debtors and the ABL lenders entered into the first of what would become a pair forbearances while, simultaneously, the debtors pivoted from what had been ongoing refinancing/recap efforts to a sale and marketing process.

That process got a boost when the debtors discovered that it was sitting on a treasure trove. The debtors leased real property in New Brunswick, New Jersey that carried with it a purchase option with a $4.9mm strike price. It turns out that the property was appraised at a whole lot more than that so the debtors exercised their option and turned right around and sold the property in a sale/leaseback transaction for $16mm. The debtors got ~$8.225mm of net proceeds and the landlord got … well … here’s a live shot of the landlord:

From there — and armed with some fresh green to almost literally buy time — the debtors continued to execute on their sale strategy. Contemporaneously, the debtors forked over more collateral to the ABL lenders and appointed two new independent directors — Thomas Fitzgerald (who is also on the board of ICON Aircraft, which filed in April) and Lawrence Hirsh (who is also on the board of Red Lobster Management LLC, which filed in May). With the ABL lenders held at bay and new directors on board, the debtors were able to set the stage for these chapter 11 cases. This includes getting a DIP financing commitment.

The debtors have nailed down a $20mm new money commitment from the ABL lenders in addition to, OF COURSE, a roll-up of $180mm (LOL).* The DIP carries a Base Rate plus 4% interest rate, a $600k close fee, an unused lien fee, a monthly servicing fee, a 4% letter of credit fee, and a 10% coverage-by-PETITION-fee (oh c’mon, with so many fees how could you blame us for trying to slip in just one more!). The DIP is obviously necessary for the debtors to complete their sale process.

So, what of that sale process? Good news. Surprising news, in fact. At least in this market. There’s not one, not two, but THREE stalking horse purchasers lined up!**

📍One with affiliates of The Renco Group Inc. (creatively named Bus Company Holdings US LLC and 1485832 B.C. Unlimited Liability Company, and together “Renco”). This sale subsumes assets related to the debtors’ business segments known as Dillon’s, Elko, Megabus Retail, Montreal, Olympia, Trentway/Ontario, Perfect Body, Rockland, Shortline, Suburban, Van Galder and Wisconsin. The total consideration is $130mm, which includes the assumption of $130mm of the pre-petition ABL facility and post-petition DIP facility plus the assumption of specified leases and contracts. The buyer will also assume the collective bargaining agreements that govern the employment of approximately 1k unionized employees associated with these segments and look to otherwise preserve the jobs of approximately 1797 employees tied to these businesses. This APA bakes in a $1.15mm expense reimbursement plus a $3.45mm breakup fee (2.65%).

📍 The other with AVALON Transportation LLC (“AVALON”) for the debtors’ Lenzner, Kerrville, All West, and ACL Atlanta assets. Here, AVALON will pay $14,836,000 plus the assumption of certain liabilities; it is only saying that it will preserve “at least 80%” of the debtors’ current employees attached to these segments (which subsumes the employees governed by a CBA at the Lenzner unit). This APA bakes in a $148,360 expense reimbursement and $445,080 breakup fee (3%).

📍Another with ABC Bus Inc. (“ABC”) for the sale of 143 of the debtors’ double deck buses for $2,335,000. This APA bakes in a $25k expense reimbursement and a $93k breakup fee (3.98%).

📍The three aforementioned APAs exclude certain assets — namely Butler, Powder River, Anaheim, Community Coach, ONE Bus, Megabus Atlanta, Megabus Florida, Megabus Northeast, and Megabus Texas, all of which the debtors intend to continue to market pursuant to an in-court sale process.

Now, we’re not math experts by any stretch of the imagination but there appears to be a wee bit of a shortfall between the DIP amount (inclusive of the roll-up) and the aggregate proceeds from the three proposed sales (not taking into account professional fees and other admin costs).

Here’s to hoping those excluded assets fetch approximately $50mm! 🙄

The debtors are represented by Alston & Bird LLP (J. Eric Wise, Matthew Kelsey, William Hao, Christopher Coleman) — which served as Variant Equity’s legal counsel on the acquisition of the debtors back in ‘19 — as proposed lead counsel and Young Conaway Stargatt & Taylor LLP (Sean Beach, Joseph Mulvihill, Rebecca Lamb, Benjamin Carver) as local counsel. Bennett Jones LLP is the debtors’ Canadian counsel. CR3 Partners (Spencer Ware) is the debtors’ proposed CRO and financial advisor. Houlihan Lokey ($HLI)(John Sallstrom) is the debtors’ proposed investment banker. Elsewhere, Wells Fargo Bank NA ($WFC) as pre-petition and DIP agent is represented by Goldberg Kohn Ltd. (Randall Klein, Dimitri Karcazes, Prisca Kim, Nicole Bruno) and Richards Layton & Finger PA (John Knight, Paul Heath, Alexander Steiger). AVALON is represented by Thompson Coburn LLP (Mark Power, Joseph Orbach, Henry Thomas) and Landis Rath & Cobb LLP (Adam Landis, Matthew McGuire). We’ll update this list as more appearances are made.

*The DIP also provides for the ability to request the issuance of $40mm in letters of credit.

**The debtors did receive one indication of interest for substantially all of their assets but that the potential purchaser later revised the IOI to include only a subset of business segments before late withdrawing entirely.

Company Professionals:

Legal: Alston & Bird LLP (J. Eric Wise, Matthew Kelsey, William Hao, Christopher Coleman, Kennedy Bodnarek) and Young Conaway Stargatt & Taylor LLP (Sean Beach, Joseph Mulvihill, Rebecca Lamb, Benjamin Carver)

Canadian Legal: Bennett Jones LLP

Directors/Managers: Farhaad Chanduwadia, Thomas FitzGerald, Lawrence Hirsh

Financial Advisor/CRO: CR3 Partners (Spencer Ware)

Investment Banker: Houlihan Lokey (John Sallstrom)

Claims Agent: Kroll (Click here for free docket access)

Other Parties in Interest:

DIP Admin Agent: Wells Fargo Bank NA

Legal: Goldberg Kohn Ltd. (Randall Klein, Dimitri Karcazes, Prisca Kim, Nicole Bruno) and Richards Layton & Finger PA (John Knight, Paul Heath, Alexander Steiger)

Stalking Horse Purchaser: Renco

Stalking Horse Purchaser: AVALON

Legal: Thompson Coburn LLP (Mark Power, Joseph Orbach, Henry Thomas) and Landis Rath & Cobb LLP (Adam Landis, Matthew McGuire)

Stalking Horse Purchaser: ABC

Sponsor: Variant Equity Advisors