💥Express Lane to Bankruptcy💥

💥Express Lane to Bankruptcy💥

Plus: More on Double Dip Financings!

On April 22, 2024, OH-based Express Inc. ($EXPR) and 11 affiliates (collectively, the “debtors”) filed chapter 11 bankruptcy cases in the District of Delaware (Judge Owens). EXPR is an omnichannel fashion retail company (comprised of brands, Express, UpWest and Bonobos) with (i) 600 stores throughout the United States and Puerto Rico and (ii) e-commerce websites like this one ⬇️ where you can get 40% off “your new season wardrobe” literally right now, lol.1

We previously covered the now-debtors’ troubles here…

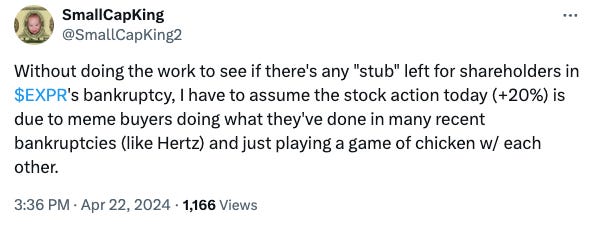

…when EXPR’s stock was trading at $8.84/share. It is now trading decidedly lower than that. And it has, of course, been delisted. Still, a delisting followed by the inevitable and predictable bankruptcy filing shouldn’t get in the way of anyone’s fun, now should it? Indeed, a meme-stonk rally appears to have taken place on the petition date because, like, 🤷♀️. Apparently this idiotic sh*t is still happening for *reasons.*

Why? Well, here is one person’s view:

Yes, good assumption @SmallCapKing2 and, no, you clearly didn’t do the work.

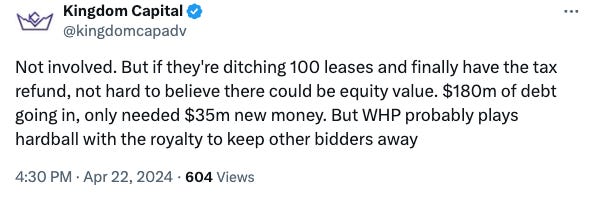

No, just no!, @kingdomcapadv!!!

Let’s discuss what these cases are and what they’re not because there are — in addition to some bad hot takes on the platform formerly known as Twitter and now known as X (see again above 👆) — headlines and SEC filings that bury the lede.

But…

This is a bankruptcy. This is a retail bankruptcy. And this is a Kirkland & Ellis LLP bankruptcy joint. And your MC for the first day hearing was Mr. Joshua Sussberg so, OF COURSE, the hearing featured ridiculously unnecessary and cute anecdotes. There’s not a company on the planet that Mr. Sussberg doesn’t have some sort of history with, apparently:

“My very first job ever in high school was at Structure. Alright, now if you saw in [Stewart Glendinning’s] declaration, Structure was the beginning of the men’s footprint for Express. It was sold to Sears in the early 90s. But that was my very first job. And I spent most of the money that I made there buying clothing at Structure because you needed to be in uniform. But I learned some valuable lessons, and I know everybody can clearly remember their first job.”

Ah. We missed you, Josh.2 😍

You know this is getting out of control when the judge — here Judge Owens — feels compelled to join the fun:

“I'll note you really dated yourself by mentioning your job was at Structure as opposed to Express. So now I have a good idea of how old you are. Only a few of us probably spent time at Structure.”

Not to be left out of the party, Kirkland’s Emily Geier added:

“I can also date myself to say that I tried to get my boyfriend at the time to actually shop at Structure for our homecoming dance because he was not well-styled and that was my best idea for getting him to look right.”

Get a lawyer started on a topic — in this case a prehistoric men’s retailer (R.I.P. Structure) — and they’ll never stop (especially when someone else is paying for these trips down memory lane). Ms. Geier continued:

“Bonobos sort of revolutionized menswear. Men aren't necessarily known for putting fashion in their mind, but they figured out a way to pitch fashion in a way to make men dress well, bringing them into the modern age and do it very conveniently.”

Okay first, ouch. Second, somewhere Ralph Lauren, Tom Ford, Jon Varvatos, and Bonobos founder Andy Dunn be like…

And third, Bonobos is also having a sale so if any of our male readers want to bring their fashion game to the “modern age,” well, knock yourselves out:

Back to the headlines.

The biggest headline is that the debtors currently have in hand a non-binding letter of intent (“LOI”) from a consortium (read: joint venture) led by WHP Global (“WHP”) and the debtors’ two biggest landlords, Simon Property Group, L. P. (“Simon”) and Brookfield Properties (“Brookfield” together with WHP and Simon, the “Phoenix JV”), for the potential going concern sale of a substantial majority of the debtors’ retail stores and operations. The debtors and the debtors’ proposed DIP lenders (more on this below) have agreed to a 30-day sprint within which to finalize any such transaction. If unsuccessful, however, the debtors “…will be forced to pivot to an orderly liquidation process pursuant to the terms of the debtor-in-possession financing agreements.” Or as Mr. Sussberg put it:

“We have a letter of intent. We do not have an enforceable asset purchase agreement. We are going to work like crazy to get to an enforceable asset purchase agreement.”

Ms. Geier added:

…the good news is this letter of intent, you know, not to hide the ball, this letter of intent to say, well, this consortium is strongly considering a going concern transaction of, for this company, I think.”

“Strongly considering” and “I think” are doing some very heavy lifting there folks.3 In other words, this sucker is not in the bag — headlines notwithstanding.

The details? Per the LOI filed in connection with the debtors’ first day papers:

The Joint Venture is expected to be capitalized with at least $200 million, including an equity commitment from WHP Global of at least $100 million, providing ample capital to create a strong operation with a footprint of over 280 stores already identified to continue the Express and Bonobos brands and legacies.

280 stores? Out of … gulp … 600? 😳

Also don’t let that headline capitalization figure misdirect you. There’s more:

…the Joint Venture would acquire and assume the Acquired Assets and Assumed Liabilities pursuant to Section 363 of the Bankruptcy Code in exchange for aggregate consideration (the “Purchase Price”) consisting of an amount payable in cash equal to (a) $10,000,000 plus (b) 100% of the net orderly liquidation value of the Acquired Merchandise (calculated in a manner reasonably acceptable to the Joint Venture).

Come again? $10mm? Plus some abstract figure? Surely “100% of the net orderly liquidation value of the Acquired Merchandise” is, combined with the $10mm, more than the $35mm of new money the lenders are committed to with the DIP, right?

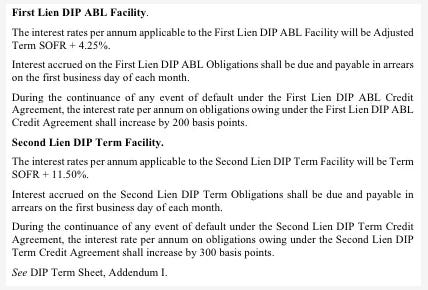

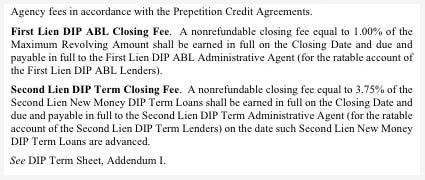

Let’s dig into that DIP. The debtors have obtained a commitment for a DIP credit facility that injects new money into their coffers4 while also rolling up pre-petition amounts. Here is what the pre-petition capital structure looks like:

And here is some of the detail:

The DIP facility has two parts. There’s (i) via Wells Fargo Bank NA ($WFC), a $10mm new money + a complete ABL roll-up (“DIP ABL”) and (ii) a 2L asset-based DIP Term Loan (“DIP Term Loan”) with ReStore Capital LLC, comprised of new money single draw term loan of $25mm + a roll-up of the FILO TL in the amount of $65mm, $25mm which shall be rolled up upon entry of an interim order and the remaining $40mm rolled-up upon entry of the final order.5 The roll-ups are obviously meant to protect against the possibility of a liquidation scenario. And this is NOT cheap paper:

So, great! There’s a limited financial and temporal leash for this retailer to survive!! Gotta love these retail bankruptcies.

Some other highlights:

📍The debtors have retained Hilco Merchant Resources LLC to liquidate 95 stores and A&G Realty as real estate advisor to negotiate with landlords.

📍As of the petition date, the debtors will no longer accept gift cards on the e-commerce platform. Express loyalists will have 30 days to use their gift cards in stores. Nothing like forcing customers to get in the car and venture into a B&M location!

📍There were lovely one-time cash retention bonus awards given to the CEO and new CFO days before BK ($500k for the former,6 $429k for the latter) with an open-ended promise of more juice to potentially come later (“An additional amount payable upon the consummation of a going-concern transaction will be negotiated at a later date by the Company and key stakeholders.”).

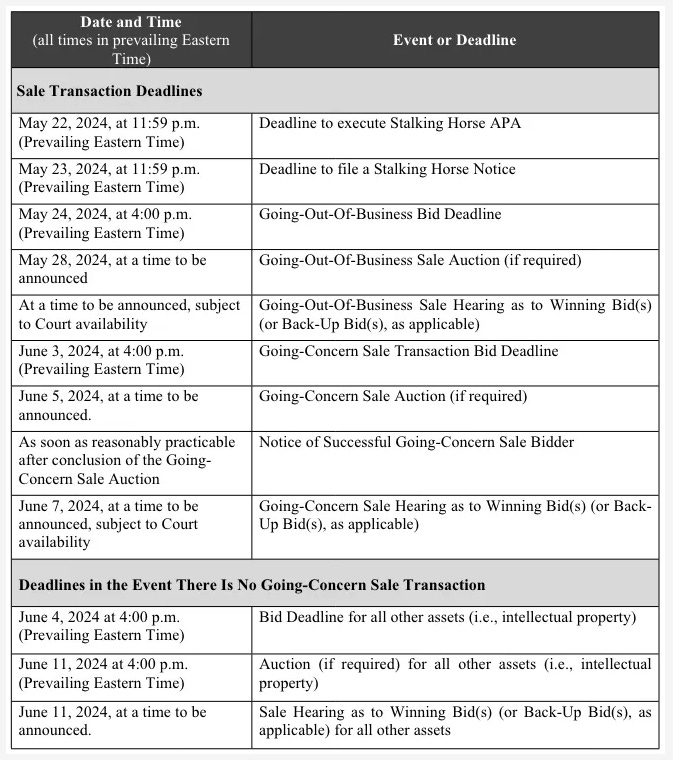

📍A bid procedures motion is already on file. Phoenix JV proposed a 5% break-up fee plus a $5mm expense reimbursement in its LOI but the debtors’ bid procedures motion reflects a 3% break-up fee plus a 3% expense reimbursement. You can do the math as to how those two different ways of framing it compare to one another. This is what the proposed sale timing looks like:

As already made abundantly clear, the debtors are represented by Kirkland & Ellis LLP (Joshua Sussberg, Emily Geier, Nicholas Adzima, Charles Sterrett) as legal counsel with Klehr Harrison Harvey Branzburg LLP (Domenic Pacitti, Michael Yurkewicz, Alyssa Radovanovich) as local support. M3 Advisory Partners LP (Kunal Kamlani) is the debtors’ proposed financial advisor, and Moelis & Company LLC (Adam Keil) their proposed investment banker. WHP is represented by Wachtell Lipton Rosen & Katz (Joshua Feltman, Benjamin Arfa) and Morris Nichols Arsht & Tunnell LLP (Derek Abbott). WFC as ABL admin agent is represented by Goldberg Kohn Ltd. (Randall Klein, Dimitri Karcazes, Keith Radner, Eva Gadzheva) and Richards Layton & Finger PA (John Knight, Paul Health, Alexander Steiger) while 2L Agent ReStore Capital LLC is represented by Ropes & Gray LLP (Gregg Galardi, Stephen Iacovo) and Chipman Brown Cicero & Cole LLP (Mark Desgrosseilliers).

Mark your calendars for 30 days out.

💥Everybody's "Double Dipping," Part II.💥

This week PETITION is double-dipping into the brain of Michael Handler, a Partner in King & Spalding LLP’s restructuring group for more on the latest in greatest in liability management exercises….

*****

Immediately after reviewing my brilliant and humorous draft on Double DIP financings (ultimately published here), PETITION knew it struck gold and asked me to write a Part II on Double DIP financings that discuss some of the actual transactions and their nuts and bolts. And since I am a young(ish), ambitious restructuring lawyer focused on growing my profile, I immediately said “yes” to my new PETITION overlords (even submitting to the stupid-all-caps-emphasis thing that they do).

So in what I hope is more The Empire Strikes Back than Attack of the Clones, below is a Part II on Double DIP financings — the sequel you didn’t think you needed, but will be glad you got.

*****

A. The Double DIP Exchanges

The first transaction to kick off the Double DIP financing craze was a recapitalization transaction consummated by At Home Group Inc. whereby the home and holiday retailer sought to raise new money to bolster liquidity and deleverage by capturing discount (i.e., exchange debt at a discount to face) by uptiering its unsecured notes into secured notes.

I will refrain from commenting on how the years have not been particularly kind to Alec Baldwin’s waistline like I did with Russell Crowe; Alec has been through a lot lately.

To accomplish its goals, At Home Group issued $200mm of new senior secured notes through a newly formed subsidiary domiciled in the Cayman Islands, which was a non-guarantor/non-loan party restricted subsidiary of the company. The new notes were guaranteed by the company’s domestic operating subsidiaries. The At Home Cayman sub likely had no other assets other than the $200 million of loan proceeds, which it lent in exchange for an intercompany loan to the At Home operating entities. The At Home Cayman Sub then pledged its only asset — the intercompany receivable — to secure the new $200mm of “Double DIP” senior secured notes.

Once At Home issued the $200 million of new senior secured notes, it then offered to all holders the opportunity to exchange their outstanding unsecured notes for a different tranche of new secured notes with the same double dip structure (but with a lower interest rate and a PIK toggle feature) at a 10% discount to par. The holders of the existing unsecured notes were able to get both a secured claim and a second claim at the expense of taking a 10% haircut on the face value of their unsecured notes. The maturity actually moved up from ‘29 to ‘28. Thus, unless the holder of the unsecured notes was virtually positive that a home decor superstore was not going to file for chapter 11 prior to maturity, the exchange was likely tough to pass up. Given that “Retail apocalypse” has its own Wikipedia entry, participating in the exchange — even with the discount (which is minimally mitigated by the earlier maturity) — was a reasonable decision.

The chart below ⬇️ shows the pre- and post-transaction capital structure:7

Generally speaking, using my lawyer math (checked by PETITION), approximately 89% of the holders of the unsecured notes participated in the exchange, so the company was able to deleverage by about $35MM or 7% through the unsecured notes (excluding the additional leverage added via the new money senior secured notes issuance, the proceeds of which were used by the company for general corporate purposes to “strengthen its balance sheet”). And, as I explained in Part I, the intercompany loan portion does not adversely affect the company and the equity sponsors if the company stays out of bankruptcy (obviously a big “if”). Any payment of interest on the intercompany loan (and it is often paid in kind) is going from one subsidiary of the company to another, and the leverage of the enterprise as a whole does not increase since the intercompany liability is netted out by the intercompany asset. The parties that benefited the least (or who suffered the most harm) from the transaction are the existing first lien term lenders, who were not only diluted by the new money and uptier first lien debt, but also the intercompany loan.

*****

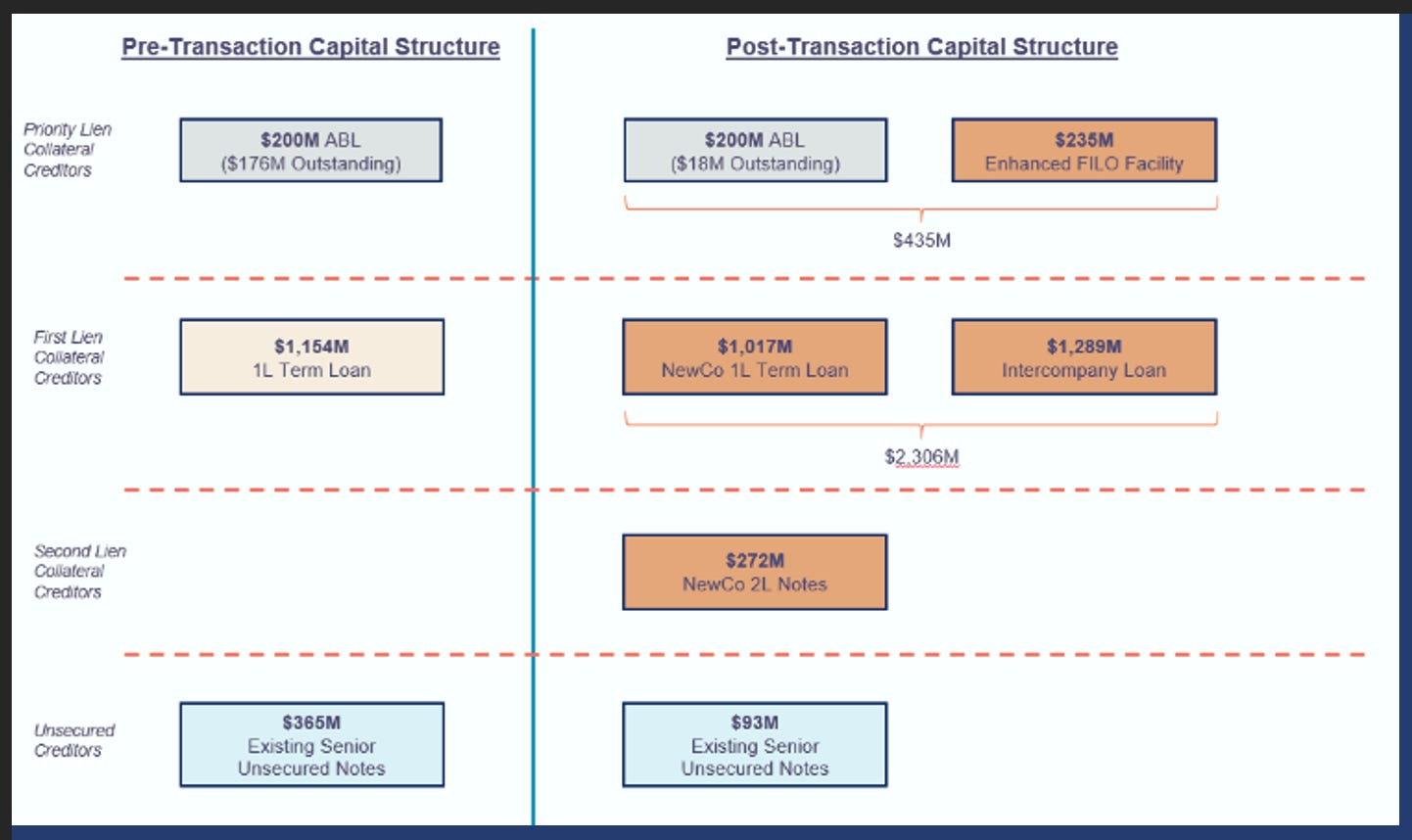

In Wheel Pros, the sponsor and management and their advisors, like in At Home, had the goals of raising new money and capturing discount.

Whereas the At Home Group financing transaction had a coercive aspect given that a holder of the unsecured notes would be layered by new secured debt with a double dip claim if it did not participate in the exchange, it arguably was an ancillary component given that there was also an uptier (unsecured to secured) feature. In Wheel Pros, however, the holders offered the exchange already held first lien debt, so the opportunity (or threat) to exchange into double dip first lien debt was the primary coercive aspect of the exchange.

An ad hoc group of first lien term loan lenders holding 70% of the outstanding first lien term loans backstopped a new $235mm first out term loan facility, of which 30% of the commitments were offered to the minority first lien term loan lenders on a pro rata basis. I know what you are thinking: “Pro rata? That sounds so pre-2020.”

In addition to funding and backstopping the new money FILO senior term loan (senior on the term priority collateral, junior on ABL priority collateral), the ad hoc group exchanged via open market purchases the existing first lien term loan for a new first lien term loan. The new first lien term loan was issued by a newly created non-guarantor restricted subsidiary with proceeds loaned to the operating entities via a secured intercompany loan pari passu to the existing term loan. This exchange was done at a 15% discount to par (i.e., 85 cents on the dollar); the ad hoc group also received a backstop fee in the form of additional new first lien term loans (in addition to a separate backstop fee paid on the FILO, also in kind). Although I know what the backstop fees were, I am not sure they are public, so let’s just say they were meaningful but not obnoxious.

But now we get to the part that was coercive AF (French for “very” coercive). The minority (i.e., non-ad hoc group) first lien term loan lenders were offered the following deal:

📍If you participate in the new money FILO, you can exchange your existing term loans at 85c on the dollar (i.e., the same deal offered to the ad hoc group (excluding the backstop fees); or

📍If you do not participate in the new money FILO, you can exchange your existing term loans at 60s on the dollar (or a 40% discount); or

📍 If you do not participate in the exchange, then you can keep your first lien term loans, but say ✌️ to all covenants and events of default (because those were stripped by the ad hoc group constituting the “Required Lenders” right before they exchanged the existing first lien term loans for new double dip term loans).

Finally, the company exchanged 75% of $365mm of unsecured notes due ‘29 (held by members of the ad hoc group) for a new double dip second lien term loans. The new second lien term loan was junior to both the existing term loan and new first lien term loan, but was secured by an intercompany loan in an amount equal to the second lien term loan that was pari passu with the existing first lien term loan, the new first lien term loan, and the new intercompany loan in respect of the new first lien term loan—yet another incentive to non-ad hoc group first lien term lenders to play ball.

The pre-and post-transaction capital structure is illustrated in the chart immediately below ⬇️:

In sum, the exchange had a very high participation rate (100% according to Bloomberg), as the minority term lenders decided it was better to take a discount than be significantly diluted by hundreds of millions of additional pari passu claims and lose all covenants. And if you participated in the new money (and I assume most of the minority term lenders did), the 15% discount is relatively modest (especially given that the first lien term loans were trading below 70 prior to the exchange).

Wheel Pros also illustrates why it is important, if possible, to restrict the incurrence of liens for intercompany loan debt, as the company presumably used junior lien baskets for the second lien term loan debt that uptiered the unsecured notes, but was able to give the second lien term lenders a first lien claim via the first lien secured intercompany loan owed to the non-loan party restricted subsidiary borrower via a lien basket that could secure intercompany loans in respect of the second lien term loans. Note that this maneuver may only work where the parties negotiating the 1L/2L intercreditor agreement are the same, as the 1L would otherwise may not agree to a carve-out on its first lien with respect to proceeds realized from the pari lien intercompany loan.

In contrast to At Home, where existing first lien term lenders were significantly diluted by the transaction and arguably worse off on a post-transaction basis, the non-participating holders of the unsecured notes received that dubious distinction here, underscoring how cross holders (holders of different tranches of debt) controlling (or blocking control) of multiple tranches can drive LME strategy and outcomes.

B. Pari Plus Double DIP Transaction

When I hear the name “Sabre” I think of three things (in exactly this order): (i) hummus (a solid mass market choice) (even though the brand, as the PETITION team politely pointed out to me, is spelled “Sabra”), (ii) the fifteenth episode of the sixth season of The Office (IYKYK8), and (iii) an LME transaction involving a recapitalization and refinancing of a “software and technology company that powers the global travel industry” that juiced up downside protection by providing foreign non-loan party guarantees.

Sabre Corporation ($SABR) raised a $700mm term loan from a group of lenders that was used to redeem several series of senior secured notes due in ‘25 and ‘27. Sabre manufactured issuance of the term loan out of a new bankruptcy-remote special purpose vehicle (the special purpose being to issue the loan). The SPV borrower funded the loan via an intercompany loan (DIP #1) to Sabre GLBL, which was the issuer under Sabre’s existing debt. Sabre GLBL and the same guarantors under Sabre’s existing debt guaranteed the intercompany loan and the loan issued by the SPV Borrower (DIP #2). Not satisfied with merely two claims, the Sabre lenders also got additional guarantees from certain foreign subsidiaries. The foreign subsidiary guarantees are the above-noted “plus.” Note that the guarantees provided by the foreign subsidiaries are capped at $400mm, rather than the full amount of the term loan.

For the benefit of 98% of the audience that may not understand this meme, Tousa is an Eleventh Circuit decision issued in ‘12 that upheld avoidance of guarantees from subsidiaries as constructive fraudulent transfers because such subsidiaries were found not to have sufficiently benefited from the loan (i.e., they did not receive “reasonably equivalent value” and were insolvent and/or rendered insolvent at the time they entered into the guarantees). And the meme itself from famous dialogue from a 1948 film The Treasure of Sierra Madre, which was itself parodied in the 1974 Mel Brooks film Blazing Saddles, which is how the author became aware of it. Like the retail apocalypse, the phrase also has its own Wikipedia entry.9 While foreign subsidiaries guaranty loans with domestic borrowers all of the time, guarantees added as part of an LME transaction may be examined in a subsequent bankruptcy by multiple constituents, including (i) the estate of the foreign subsidiary to the extent it is a debtor, (ii) the creditors of the foreign subsidiary, and (iii) the general unsecured creditors of the domestic obligors, which may view avoidance of the guarantees as unlocking equity value in the foreign subsidiaries for the benefit of general unsecured creditors. The aforementioned TOUSA risk can be mitigated where there is contemporaneous evidence that the new guarantors are benefiting from the loan/LME transaction beyond just keeping the enterprise out of bankruptcy (as the Eleventh Circuit upheld the bankruptcy court’s ruling that keeping the enterprise of bankruptcy alone did not constitute “reasonably equivalent value” for purposes of providing the upstream guarantees).

Not to be outdone, Trinseo PLC ($TSE) structured a $1b dollar term loan facility used to refinance existing debt with a double dip structure AND the novel use of an unrestricted subsidiary whereby a business segment was transferred to an unrestricted subsidiary in connection with the financing, and such unrestricted subsidiary was a co-borrower and guarantor of the new double dip loan. In connection with the loan, the business segment held by the unrestricted subsidiary was required to be shopped. Upon the sale of the business segment, 100% of the net proceeds from the sale were required to be used to repay the loan.

Note that some existing loan documents expressly prohibit unrestricted subsidiaries from guaranteeing debt guaranteed by loan parties and/or restricted subsidiaries. Most importantly, such prohibition can be amended or waived with the consent of “Required Lenders,” so it probably is not going to be a relevant prohibition in an LME situation where the company has the consent of “Required Lenders” or in a refinancing situation, where the terms of the existing debt being refinanced do not matter (unless there is other debt that is not being refinanced and the “Required Lenders” of such other debt are not participating in, or otherwise consenting to, the proposed transaction).

C. Conclusion

While this is by no means a comprehensive summary of all of the Double DIP financing transactions, it generally describes how the Double DIP financing structure is being used in connection with recapitalizations, coercive debt exchanges, and refinancings. Indeed, as I was writing this article, two companies, Alvaria and City Brewing were reported to have consummated LME-style new money financings and debt exchanges that involved double dip financing structures.

In sum, my young apprentice, the only limits to structuring liability management financings is your imagination. So go forth – think about ways the mundane plumbing of moving money can create additional claims. Use non-loan party restricted subsidiaries and unrestricted subsidiaries as guarantors. No restrictive covenant capacity should be wasted.

Finally, you may be expecting a Part III on “triple dips.” Notwithstanding recent press reports, there is no such thing. At least outside of a Dairy Queen.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥. We’ve added, “The Credit Investor's Handbook: Leveraged Loans, High Yield Bonds, and Distressed Debt,” by Michael Gatto and have high hopes for its arrival.

💰New Opportunities💰

Looking for quality people? PETITION lands in the inbox of 1000s of bankers, advisors, lawyers, investors and others every week. Email us at petition@petition11.com to learn about posting your opportunities with us.

Click through and you can even get an extra 50% off clearance wares!

Sadly, the other three cases filed by Kirkland this year — Sientra Inc., Invitae Corporation, and Thrasio Holdings Inc. — have left very little room for charming yarns.

Ms. Geier added, “I do think that the phoenix rising from the ashes is probably why they named their consortium Phoenix, but this is a group of stakeholders that are, that know the value of this business, that it needs to be preserved as a going concern.” We shall surely see.

The EXPR debtors filed with $23mm of cash on hand.

Additionally, on April 15, 2024, the debtors received $49mm cash refund from the Internal Revenue Service related to the CARES Act. Great, right? Wellllll, it turns out that the debtors had, as of March 28, 2024, insufficient liquidity to comply with the necessary availability requirements under the pre-petition ABL and the ABL Agent, therefore, triggered a cash dominion period. Consequently, the refund went straight towards paydown of the ABL once it (finally) came in. Womp womp.

The Letter Agreement between the debtors and the CEO, dated April 18, 2024, notes that the $500k is “a reduced amount” compared to the amount originally set forth in the CEO’s employment agreement.

This chart was taken from the article my colleagues and I wrote for King & Spalding’s award-winning Hub application entitled How Did They Do It? At Home Group and the “Double Dip” Claim Financing Structure, which was published in September of last year.

IYKYK is what the kids use to shorthand, “if you know, you know.”

https://en.wikipedia.org/wiki/Stinking_badges

Respect to the OG's of Finance Substack.