💥US Trustee on Biglaw Violence💥

💥US Trustee on Biglaw Violence💥

An Enviva Update + new coverage of Delta Apparel Inc.

While Invitae Corp’s proposed sale moves towards an approval hearing on May 7, 2024, White & Case LLP and Kirkland & Ellis LLP continue to box over K&E’s retention. We discussed that battle here:

But they have no monopoly on professional retention drama. We previously mentioned another brewing situation here…

…when we, almost in passing, noted that the US Trustee (“UST”) had filed an objection to Vinson & Elkins LLP’s employment as debtors’ counsel in the Enviva Inc cases. Debtors’ counsel just seems to be taking fire from multiple directions these days. The entire objection warrants a deeper dive.

The UST says that V&E must provide sufficient information about its relationship with Riverstone Holdings LLC who is a large holder of Enviva’s equity and a client of V&E since 2015!

“Vinson’s representation of Riverstone ‘accounted for 0.8% of V&E’s billings and 1.4% of V&E’s collections for V&E’s fiscal year ended December 31, 2023.’”

Okay great, so some sort of relationship has been established. What’s the big deal???

There is none — at least according to V&E partner, David Meyer. In a declaration in support of V&E’s retention, Mr. Meyer notes:

“V&E currently represents, and in the past has represented, Riverstone Investment Group LLC and its affiliates (“Riverstone”) in a variety of other matters.”

“As far as I can determine, the factual and legal issues in this matter are unrelated to the work V&E does or is likely to do for Riverstone in other matters.”

“V&E will not represent Riverstone in connection with any matters related to the Debtors’ restructuring process. I do not believe V&E’s current or past representation of Riverstone in unrelated matters presents a conflict but have disclosed the connection out of an abundance of caution.”

This is, as far as we’re concerned, a fairly normal and mundane disclosure. And if Mr. Meyer says there’s no foul play here, we’re good right? Wrong. The UST, before even getting into any conflict of interest or lack of disinterestedness arguments, thinks that essential disclosure is still lacking. The UST basically looked at the employment application and said:

In its objection, the UST is asking for 23 additional items to be disclosed, everything from what V&E partners had for breakfast to whether they prefer monk strap or oxford shoes (we jest, it’s obviously oxfords).

Per the UST:

“As the applicant, Vinson is obligated to provide clear and candid disclosures regarding all connections to the debtor, creditors, and parties in interest in a verified statement and adequately disclose its compensation arrangement with the Debtors.”

“Moreover, it is not within the province of a professional to ‘usurp the court's function by choosing, ipse dixit, which connections impact disinterestedness and which do not. The existence of an arguable conflict must be disclosed if only to be explained away.’”

And the kicker:

“Vinson’s lack of full disclosures regardless of any prejudice to the estate is a sufficient basis, by itself, to warrant denial of its employment.”

V&E must be loving that choice of Virginia as venue right about now.

Where’s the UCC joinder to the objection to stir up some more sh*t??? Unfortunately there is none. But the UCC did file a preliminary objection to the debtors’ post-petition financing and cash collateral motion. In it, the UCC claims:

“By bundling the DIP Facility and the RSA together—before the Debtors have even developed a business plan, a valuation, or a viable capital structure—the Debtors have improperly ceded control over the direction and outcome of these cases to the Ad Hoc Group (who control the DIP Facility, 72% of the Prepetition Senior Secured Debt, and 95% of the 2026 Notes).”

Expanding further:

“The RSA provides, at best, a bare framework for the Debtors’ ultimate reorganization. Nevertheless, the careful interlocking of the DIP Facility and the RSA—through various cross-defaults and termination rights—ensures that the Ad Hoc Group maintains control over the trajectory of these Chapter 11 Cases, the terms of any equity conversion on account of the Tranche A Participation Election, the terms of any exit financing and equity rights offering, and the treatment of general unsecured creditors.”

And of course, it wouldn’t be an objection without some harping on the fees:

“In addition, the Debtors have agreed to a number of fees under the DIP Facility that are neither warranted nor justified by the facts and circumstances of these cases and which are not in the best interests of the estates, including (i) a $25 million Break Premium should the Debtors prepay or refinance the DIP Facility prior to maturity and (ii) the right to make the Tranche A Participation Election, which the Debtors make no effort to value.”

Okay, but what about the meat and bones of the plan? Does the UCC have issues with that? You bet:

“[T]he DIP Facility constitutes an impermissible sub rosa plan because the right to make the Tranche A Participation Election prematurely hardwires the right of Tranche A DIP Creditors to convert their claims to equity in the reorganized Debtors at an undetermined discount to an undetermined plan value for an undetermined percentage of equity. The Debtors have agreed to this conversion right without the benefit of a business plan, a valuation or a proposed capital structure.”

Lol yep, the UCC is spot on with this one. There’s no plan on file, we have no idea of where plan value lands and no idea what the equity distribution will look like (other than a 5% allocation + warrants for existing equity holders).

Debtors be like:

Actually, given the UST objection to V&E’s retention, maybe it’s more like:

Okay, no seriously, the debtors had this to say in a reply:

“The RSA purposefully leaves many plan terms open for future negotiation because, as the Objection recognizes, ‘[t]he Debtors intend to conduct an operational restructuring of its [sic] contractual arrangements and develop a comprehensive business plan . . . but that work remains in progress. Over the course of these chapter 11 cases, the Debtors intend to pursue contract renegotiation (raise-the-bridge or “RTB”) and related efforts to effect a value-maximizing restructuring that will benefit all of the Debtors’ stakeholders, including unsecured creditors. These efforts, of course, require time and liquidity—two precious commodities almost certainly unavailable to the Company in the absence of both the DIP Financing and the support embodied in the RSA.’”

Yeah! There’s a reason there’s no details on the RSA, duh.

The debtors continue:

“These important efforts also require openness to future developments. For example, the DIP Facility Agreement contemplates that DIP Creditors may participate in a future equity rights offering, the terms of which are subject to further approval from the Court (the “Tranche A Participation Election”). But many terms of the Tranche A Participation Election and any potential discount to plan value remain undetermined at this stage. In criticizing that flexibility, the Objection again seeks to have things both ways—on the one hand, complaining that various aspects of the rights offering are “undetermined,” while simultaneously failing to recognize, on the other, that performing a valuation and fixing the terms of a rights offering or equitization at this early stage, before taking into account any of the expected operational and balance-sheet improvements including RTB, would only increase the risk of undervaluing the Company to the detriment of its stakeholders, including its unsecured creditors.”

Boom. The absence of details is actually just “flexibility.” Flexibility that could prove to improve future recovery for unsecured creditors!

The ad hoc group also added a reply in support of the debtors’ final DIP motion. Much of it similar to the debtors’ reply. Discussions with the UCC resulted in a revised final DIP order that, according to the debtors, addresses much of the UCC concerns.

And recall that there’s a motion to reconstitute the UCC filed by the ‘26 notes indenture trustee, Wilmington Savings Fund Society FSB.* Well, the UST responded with an objection to the reconstitution motion and in it states:

“WSFS is ‘well organized, well represented by counsel, and adequate to the task of representing its interests without “official” status’ and therefore it already can participate without needing to be a member of the Committee. Moreover, the Ad Hoc Group, which constitutes over 95% of the 2026 Note holder constituency, has taken a highly active role in these cases and will presumably continue to do so regardless of the composition of the Committee. Thus, reconstitution will not meaningfully improve the participation of creditors in these cases.”

“[T]here appears to be a potential conflict between the duties of a Committee member and certain obligations under the 2026 Indenture and RSA, which may prohibit WSFS from acting in any way that may negatively impact its constituency including the formulation of an alternative chapter 11 plan and investigation of the DIP Stipulations.”

There it is. Conflict of interest because of the RSA participation is the real reason the UST refuses to include Wilmington on the UCC.

So to sum everything up in this case so far, there’s:

UST on debtors’ counsel violence;

UCC on ad hoc group violence; and

Indenture Trustee on UST violence related to the UCC’s composition and UST on Indenture Trustee violence in return.

Fun times are soon to come! The debtors’ second day hearing — which may include some additional DIP drama — is scheduled for later this morning at 10am ET on May 1, 2024. There’s another hearing scheduled for May 9, 2024 at 2pm ET to address the V&E retention and UCC composition issues.

*We mentioned this in passing on our previous piece, but it’s worth noting again that the composition of the UCC, currently consisting of RWE Supply & Trading GmbH (“RWEST”), Drax Power Limited, and Ryder Integrated Logistics, is being contested by the ‘26 notes trustee, Wilmington Savings Fund Society FSB, the debtors, and the Epes green bonds’ trustee, Wilmington Trust NA.

Wilmington, as trustee to the unsecured ‘26 notes, believes it’s ridiculous that they’re not included when the ‘26 notes obligations represents “42% of the funded debt and a much larger percentage of the Debtors’ total unsecured debt.”

Of course, the issue here is that holders representing 95% of the ‘26 notes have signed onto the RSA, precluding them from being included in the UCC. And the RSA (+associated DIP) is exactly what the current UCC’s objection centers around.

⏩One to Watch: Delta Apparel Inc ($DLA)⏩

Headquartered in Duluth, GA, Delta Apparel Inc ($DLA) is a vertically integrated, international wholesale apparel company. Under the primary brands Salt Life, Soffe, and Delta, the company designs, manufactures, and sources apparel for various distribution channels. The company also does a small amount of business DTC, though wholesale takes up most of the business.

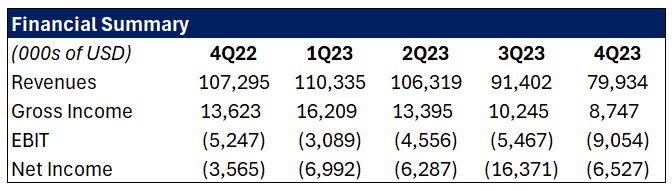

Outside of the sales breakdown in the above image, it is apparent that the company struggled in ‘23. Revenues were down ~13% QoQ and ~25% YoY in the quarter ending 12/31/23. The revenue decrease flows into a decrease in gross margins from 22% in ‘22 to 13% in ‘23.

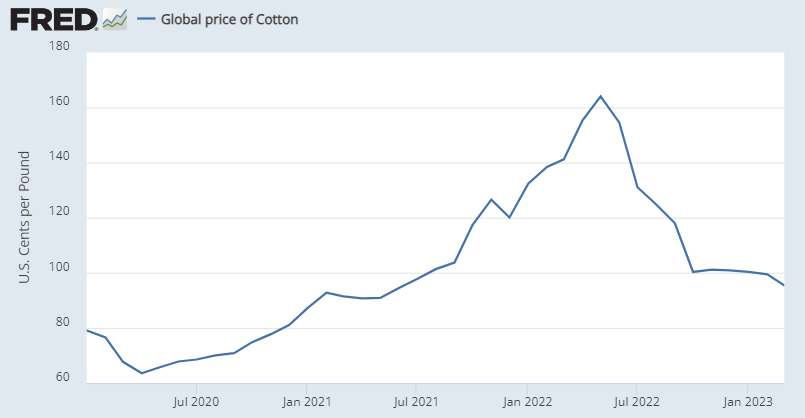

There are two main culprits for the poor operational performance. First, certain suppliers have announced that they will no longer extend the same amount of credit, citing factors such as inventory backlog stemming from the pandemic and a broader industry trend favoring larger, cheaper wholesalers. Second, the cost of cotton dramatically increased, inflating operational expenses.

Outside of the operational challenges, the company has amassed a debt burden that is trending toward becoming unsustainable. As of its most recent filing, the company has ~$125mm in debt outstanding, ~$111mm of which is a ‘27 revolving credit facility with Wells Fargo ($WFC), PNC Financial Services Group Inc ($PNC), and Regions Financial Corp ($RF) (the “RCF”). The facility bears interest at an average of 8.7%.

Amidst the poor performance, debt burden, and growing interest expenses, the company put out a going concern warning in its most recent 10-Q — none of which is working wonders for the company’s stock.

In the warning, the company mentioned that it may be at risk of breaching one or more financial covenants under the RCF. Cash and availability under the RCF totals just $7.4mm, so without a quick liquidity boost, the company recently indicated that it’s headed for trouble, “We believe we will need to obtain additional liquidity in the near term to fund our operations and meet the obligations specified in our U.S. revolving credit facility, and we are currently exploring a variety of options toward that end.”

We all know what one of those options might be.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.